- Biotechnology

- Arbovirus Testing Market

Arbovirus Testing Market Size, Share, and Growth Forecast 2026 – 2033

Arbovirus Testing Market by Test Type (Serological Tests, Molecular Diagnostic Tests, Others), Virus Type (Dengue Virus, Zika Virus, Chikungunya Virus, Yellow Fever Virus, West Nile Virus, Others), End-user (Hospitals and Clinical Laboratories, Public Health Laboratories, Blood Banks and Transfusion Centers, Research Institutes and Academic Laboratories, Others), and Regional Analysis, 2026–2033

Arbovirus Testing Market Share and Trends Analysis

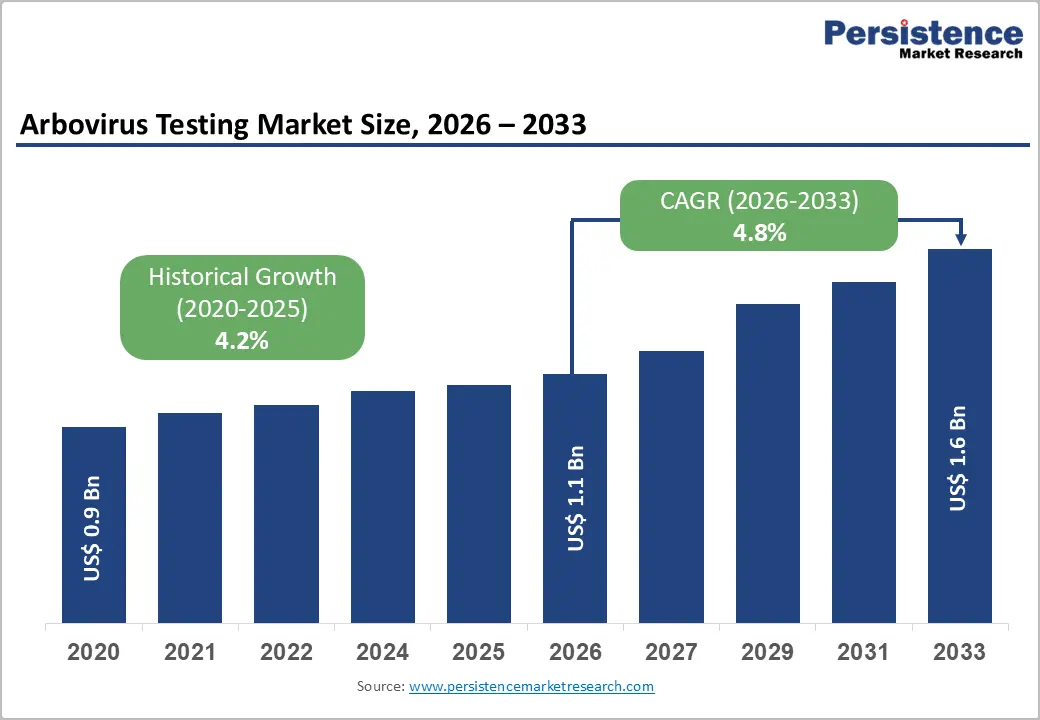

The global arbovirus testing market size is expected to be valued at US$ 1.1 billion in 2026 and projected to reach US$ 1.6 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033. The market is expanding steadily due to the rising prevalence of mosquito-borne viral infections such as dengue, Zika, chikungunya, yellow fever, and West Nile virus. The rise in global outbreaks, climate-driven vector expansion, and growing international travel have strengthened the need for early and accurate diagnosis. The demand for molecular diagnostics, ELISA tests, rapid antigen kits, and multiplex PCR panels continues to rise across hospitals, diagnostic laboratories, and public health agencies. Government surveillance programs and outbreak preparedness initiatives further support market growth. Technological advancements in portable and point-of-care testing solutions are also creating strong opportunities for global market expansion.

Key Industry Highlights

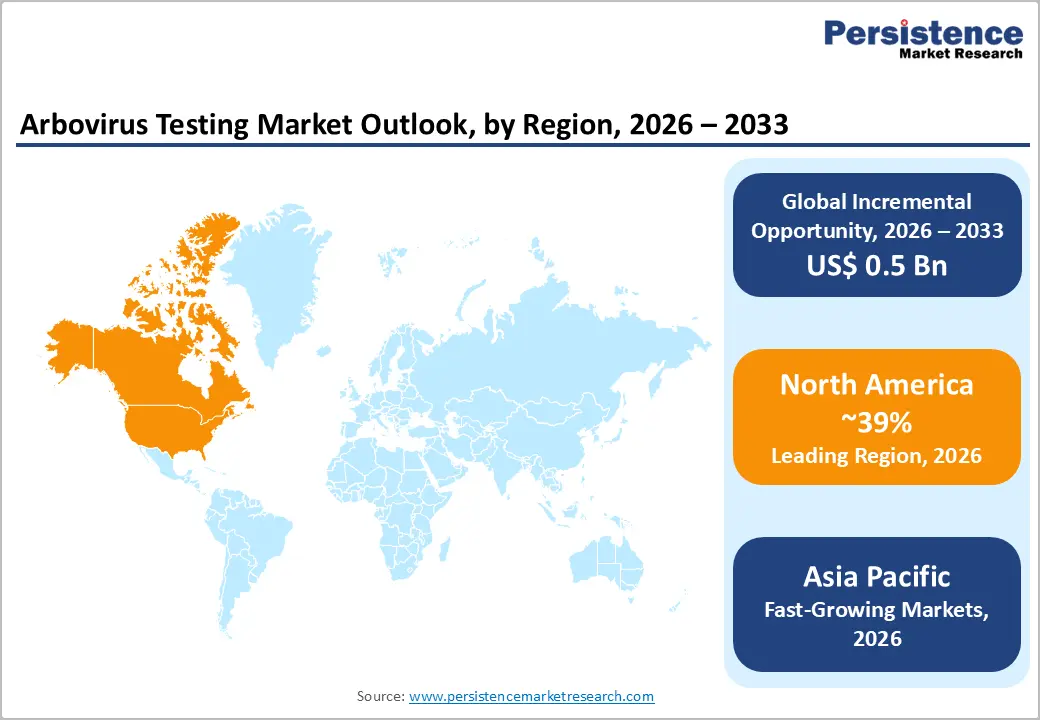

- Leading Region – North America is likely to account for approximately 39% of the global arbovirus testing market share in 2026, driven by mandatory FDA-mandated blood donor screening for West Nile and Zika viruses, the CDC's ArboNET surveillance network, and premium molecular diagnostic platform adoption across U.S. reference laboratories.

- Fast-Growing Market – Asia Pacific is the fast-growing arbovirus testing region, underpinned by the world's highest dengue endemic burden over 289,000 confirmed Indian cases in 2023 per NVBDCP, expanding government health infrastructure investment, and growing point-of-care rapid test adoption.

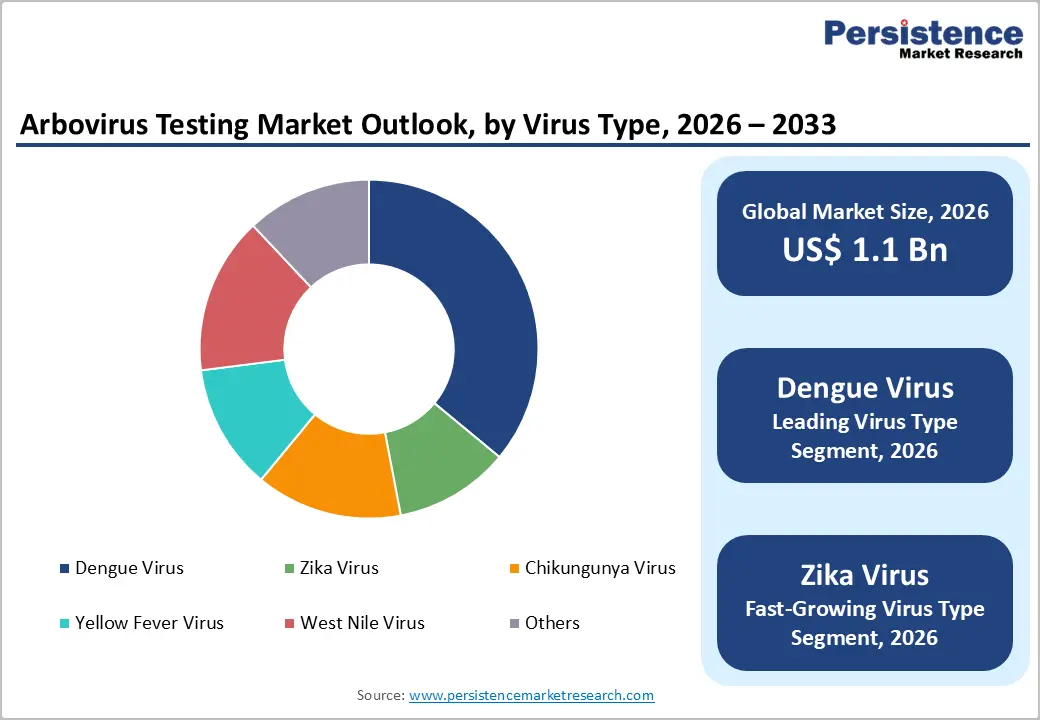

- Dominant Virus Type – Dengue Virus testing leads the Virus Type category with approximately 36% market share in 2025, directly reflecting dengue's status as the world's most prevalent arboviral disease, affecting 390 million people annually per WHO, with a record 13.3 million American cases in 2024 per PAHO.

- Fast-Growing Virus Type – Zika Virus testing is the fastest-growing virus type segment through 2033, driven by ongoing transmission in the Americas and Pacific, mandatory blood donor screening programs, and active surveillance expansion following the WHO-declared Zika public health emergency that transformed global diagnostic investment and preparedness.

- Key Opportunity: Point-of-care rapid antigen/antibody combination RDTs validated under WHO prequalification and adopted through PAHO and UNICEF procurement frameworks represent the highest-volume growth opportunity, unlocking arbovirus testing access across primary care settings in 40+ dengue-endemic low-income countries through 2033.

Market Dynamics

Drivers – Rise in Global Arboviral Disease Burden Amplified by Climate Change and Urbanization

The global burden of arboviral diseases has escalated dramatically over the past two decades, driven by climate change-related warming of previously temperate regions, expanding urban mosquito breeding habitats, and accelerating international travel and trade. The WHO reports that dengue fever now affects approximately 390 million people annually across 129 countries, while chikungunya has spread into Europe and the Americas.

The European Centre for Disease Prevention and Control (ECDC) documented unprecedented autochthonous dengue transmission in Italy, France, and Spain in 2023–2024, previously considered non-endemic regions. The Aedes aegypti and Aedes albopictus mosquito vectors continue to expand their geographic range northward. Each new geographic incursion by arboviruses into previously unaffected populations triggers public health surveillance programs and diagnostic procurement, directly expanding the addressable testing market beyond traditionally endemic tropical regions.

Blood Safety Screening Requirements and Public Health Surveillance Investments Expanding Test Volumes

Mandatory arbovirus screening of blood donations, particularly for Zika virus, West Nile virus, and dengue, has become an increasingly important institutional demand driver for the Arbovirus Testing market. The U.S. Food and Drug Administration (FDA) issued guidance requiring universal Zika virus screening of all blood donations in the United States in 2016, and blood donation screening for West Nile Virus (WNV) has been mandatory in the U.S. since 2003.

The European Blood Alliance has similarly expanded arboviral donor screening recommendations across EU member states. According to the Pan American Health Organization (PAHO), increasing dengue transmission intensity in the Americas has prompted multiple national blood bank systems to implement pre-transfusion dengue screening protocols, creating a significant, recurring institutional demand stream for validated arbovirus testing platforms beyond acute clinical diagnostics.

Market Restraints

High Assay Cross-Reactivity Among Flaviviruses Complicating Accurate Diagnosis

A fundamental scientific challenge constraining the Arbovirus Testing market is the significant serological cross-reactivity among closely related flaviviruses, including dengue, Zika, West Nile, and yellow fever viruses, which share structural protein epitopes. The CDC and WHO have documented that dengue-immune individuals can generate antibodies that produce false-positive Zika serology results, and vice versa. This cross-reactivity limitation reduces the diagnostic specificity of commercially available serological assays, necessitating confirmatory molecular testing and limiting the standalone clinical utility of rapid point-of-care antibody tests, particularly in co-endemic regions where multiple flaviviruses circulate simultaneously, increasing diagnostic complexity and the burden of confirmatory testing workflows.

Infrastructure Gaps and Limited Laboratory Capacity in High-Burden Low-Income Countries

The majority of arboviral disease burden is concentrated in low- and middle-income countries (LMICs) in South Asia, Southeast Asia, Latin America, and Sub-Saharan Africa, where laboratory infrastructure, cold chain logistics, and trained diagnostic workforce capacity often remain severely limited.

Several high-burden countries rely on clinical diagnosis alone for the majority of arboviral disease cases, foregoing laboratory confirmation entirely. The WHO's Global Arbovirus Initiative has highlighted diagnostic capacity gaps as a primary challenge to outbreak response. These infrastructure constraints suppress confirmed test volume relative to actual disease incidence, limiting per-capita testing market penetration in the regions with the highest arboviral disease burden.

Opportunities - Point-of-Care Rapid Diagnostic Innovation Transforming Testing Access in Endemic Regions

The development and commercialization of next-generation rapid diagnostic tests (RDTs) for arboviral diseases, particularly dengue, Zika, and chikungunya, represents a transformative market opportunity as healthcare systems in endemic regions seek rapid, decentralized diagnostic decision-making tools. The WHO prequalification program for dengue RDTs has created a regulatory fast track for high-quality, affordable rapid tests suitable for deployment in resource-limited settings. SD Biosensor (South Korea) and Abbott's Panbio™ dengue rapid test series have demonstrated strong market penetration in the Asia Pacific and Latin America with WHO-prequalified or CE-marked products. Investment in antigen-antibody combination RDTs, which simultaneously detect NS1 antigen (acute phase) and IgM/IgG antibodies (later phase) is expanding the diagnostic window and clinical utility of point-of-care tests, unlocking high-volume market penetration in primary care and community health settings across high-burden endemic countries.

Category-wise Analysis

Test Type Insights

Serological Tests are the dominant test type in the Arbovirus Testing market, accounting for approximately 58–62% of the total market share in 2025. This leadership reflects serological testing's established role as the primary arbovirus diagnostic modality in clinical settings. ELISA-based IgM/IgG antibody detection and NS1 antigen tests provide confirmatory diagnosis of dengue, Zika, and chikungunya in the post-acute phase of infection when patient presentation typically occurs. The WHO and CDC recommend serology as a primary diagnostic approach for dengue in patients presenting more than 5 days post-symptom onset, covering the majority of clinical presentations. The widespread availability and relatively lower cost of serological platforms compared to molecular diagnostics, combined with established laboratory infrastructure compatibility, ensure serological tests maintain a dominant market share across both high-income and resource-limited healthcare settings globally.

Virus Type Insights

Dengue virus testing dominates the virus type segment with approximately 36% share in 2026. This dominance directly reflects dengue's status as the world's most prevalent arboviral disease: the WHO estimates 390 million infections annually across 129 countries, with approximately 96 million manifesting clinically. PAHO reports that dengue cases in the Americas reached a record 13.3 million in 2024 more than twice the previous annual record, highlighting both the scale and accelerating trajectory of dengue burden. The disease's clinical heterogeneity (ranging from mild fever to severe hemorrhagic dengue and dengue shock syndrome) necessitates laboratory confirmation for clinical management decision-making, generating consistent high-volume test demand across hospitals, clinics, and blood banks globally.

End User Insights

Hospitals and clinical laboratories represent the leading end-user segment in the arbovirus testing market, commanding approximately 52% share in 2026, owing to the clinical workflow for arboviral disease management: symptomatic patients presenting with febrile illness in endemic or travel-exposed settings are triaged to hospital emergency departments or outpatient clinics where blood samples are drawn and dispatched to in-house or reference clinical laboratories for serological or molecular arbovirus testing.

Major teaching hospitals and tertiary care centers in high-burden countries, including across India, Brazil, Thailand, and Colombia manage high seasonal dengue patient volumes that generate consistent arbovirus test procurement. The establishment of Arboviral Diseases Branch-affiliated reference laboratories by the CDC and WHO collaborating centers further reinforces the institutional clinical laboratory's dominant role in the diagnostic testing ecosystem.

Regional Insights

North America Arbovirus Testing Market Trends and Insights

North America leads the global arbovirus testing market with approximately 39% of the total share in 2026, driven by the United States' diagnostic infrastructure, mandatory blood donation screening programs for West Nile virus and Zika, active CDC-supported arboviral surveillance networks, and high diagnostic test unit values reflecting advanced adoption of molecular and serological platforms. The region benefits from robust regulatory frameworks and high per-test reimbursement, driving a premium product mix.

U.S. Arbovirus Testing Market Size

The United States accounts for approximately 88% of the North American arbovirus testing market revenue, underpinned by FDA-mandated West Nile virus and Zika blood donor screening, the CDC's ArboNET national arboviral surveillance system, and consistent dengue case importation from endemic travel destinations. The U.S.'s world-class reference laboratory network and active molecular diagnostic adoption sustain premium market value.

Europe Arbovirus Testing Market Trends and Insights

Europe is an increasingly significant Arbovirus Testing market, driven by growing autochthonous dengue and West Nile virus transmission documented by the ECDC across southern European countries, including Italy, France, Greece, and Spain, combined with strong travel-associated arboviral case importation volumes. The region's advanced clinical laboratory infrastructure and active ECDC surveillance programs drive consistent serological and molecular test demand.

Germany Arbovirus Testing Market Size

Germany is likely to account for approximately 22% share, primarily driven by imported arboviral disease cases among travelers and migrants, active surveillance under the Robert Koch Institute (RKI), and Germany's role as a major European reference laboratory hub. The RKI's comprehensive arboviral disease monitoring generates consistent confirmatory testing demand across Germany's reference laboratory network.

U.K. Arbovirus Testing Market Size

The United Kingdom holds approximately 19% revenue share in 2026. The UK Health Security Agency (UKHSA) manages a robust imported arboviral disease surveillance program, and the U.K.'s status as a major international travel hub generates substantial dengue, Zika, and chikungunya imported case volumes requiring laboratory confirmation and clinical management.

France Arbovirus Testing Market Size

France is expected to account for approximately 16% share in 2026. France has documented autochthonous dengue and chikungunya transmission in its mainland and overseas territories (particularly Martinique, Guadeloupe, and Réunion), and Santé publique France operates active surveillance programs that drive sustained arbovirus testing procurement both in metropolitan France and its tropical territories.

Asia Pacific Arbovirus Testing Market Trends and Insights

Asia Pacific is the fast-growing arbovirus testing market regionally, also home to the dengue, chikungunya, and Japanese encephalitis. China, while historically a lower-burden dengue market, has documented increasing locally transmitted dengue outbreaks in Guangdong Province in recent years, per the Chinese Center for Disease Control and Prevention (China CDC), and is expanding dengue surveillance infrastructure. The region's massive endemic case volumes, government health ministry investments in diagnostic capacity, and adoption of rapid point-of-care tests are collectively driving substantial volume growth.

India Arbovirus Testing Market Size

India is likely to account for approximately 25% share in 2026. India reports among the world's highest dengue case burdens, with the National Vector Borne Disease Control Programme (NVBDCP) reporting over 289,000 confirmed dengue cases in 2023. Government investments in diagnostic infrastructure under the National Health Mission are expanding laboratory testing access across states.

Competitive Landscape

The global arbovirus testing market is moderately competitive, driven by rising demand for accurate detection of dengue, Zika, chikungunya, and other vector-borne infections. Companies compete through advanced molecular diagnostics, multiplex PCR panels, ELISA-based assays, and rapid point-of-care testing solutions. Innovation focuses on improving sensitivity, faster turnaround time, and field-based portable testing for outbreak-prone regions. Strategic collaborations with public health agencies, diagnostic laboratories, and research centers strengthen market presence.

Key Developments:

- In May 2025, the UK Health Security Agency (UKHSA) and the Animal and Plant Health Agency (APHA) reported the first detection of West Nile virus genetic fragments in mosquitoes in the United Kingdom.

- In February 2025, Bavarian Nordic A/S entered into a contract manufacturing agreement with Biological E. Limited to produce VIMKUNYA™ (CHIKV VLP), the first FDA-approved chikungunya vaccine for individuals aged 12 and older.

Global Arbovirus Testing Market – Key Insights and Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 900 million |

|

Current Market Value (2026) |

US$ 1.1 billion |

|

Projected Market Value (2033) |

US$ 1.6 billion |

|

CAGR (2026–2033) |

4.8% |

|

Leading Region |

North America, ~39% market share in 2026 |

|

Dominant Category (Test Type) |

Serological Tests, ~58–62% market share in 2026 |

|

Top-ranking Category (Virus Type) |

Dengue Virus, ~36% market share in 2026 |

|

Incremental Opportunity |

US$ 500 million (Absolute Dollar Opportunity, 2026–2033) |

Companies Covered in Arbovirus Testing Market

- Abbott Laboratories

- Roche Diagnostics

- Thermo Fisher Scientific Inc.

- Bio-Rad Laboratories, Inc.

- Siemens Healthineers AG

- Danaher Corporation (includes Cepheid, Beckman Coulter)

- QIAGEN N.V.

- bioMérieux SA

- Meridian Bioscience, Inc.

- NovaTec Immundiagnostica GmbH

- InBios International, Inc.

- Artron Laboratories Inc.

Frequently Asked Questions

The global Arbovirus Testing market is expected to be valued at US$ 1.1 billion in 2026.

The primary demand drivers are the escalating global burden of arboviral diseases, with the WHO reporting 390 million annual dengue infections and record 13.3 million Americas cases in 2024 per PAHO, combined with mandatory blood donor screening requirements for West Nile and Zika viruses, and climate change-driven geographic expansion of arbovirus vector mosquitoes into previously non-endemic regions.

North America leads the global Arbovirus Testing market with approximately 39% share in 2026. The U.S. drives regional dominance through FDA-mandated blood donor screening programs, the CDC's ArboNET surveillance network, high per-test reimbursement values for advanced molecular platforms, and sophisticated reference laboratory infrastructure for confirmatory arboviral disease diagnosis.

Expansion of point-of-care testing and portable molecular diagnostics offers strong potential for faster disease detection in remote and low-resource settings. Rising government investments in vector-borne disease surveillance, public health screening, and epidemic preparedness further create growth opportunities.

The arbovirus testing market is led by global diagnostics companies, including Abbott Laboratories, Roche Diagnostics, Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., and Siemens Healthineers AG.