- Inks, Coatings, Adhesives & Sealants (ICAS)

- Anti-corrosion Coatings Market

Anti-corrosion Coatings Market Size, Share, and Growth Forecast 2026 - 2033

Anti-corrosion Coatings Market by Technology (Solvent-based, Water-based, Powder Coatings, Others), Material (Epoxy, Polyurethane, Acrylic, Alkyd, Zinc-based, Others), Coating Type (Barrier Coatings, Sacrificial Coatings (Zinc-rich), Inhibitive Coatings, Others), End-user (Oil & Gas, Construction/Infrastructure, Marine, Automotive & Transportation, Power Generation, Aerospace & Defense, Others), and Regional Analysis, 2026 - 2033

Anti-corrosion Coatings Market Size and Trend Analysis

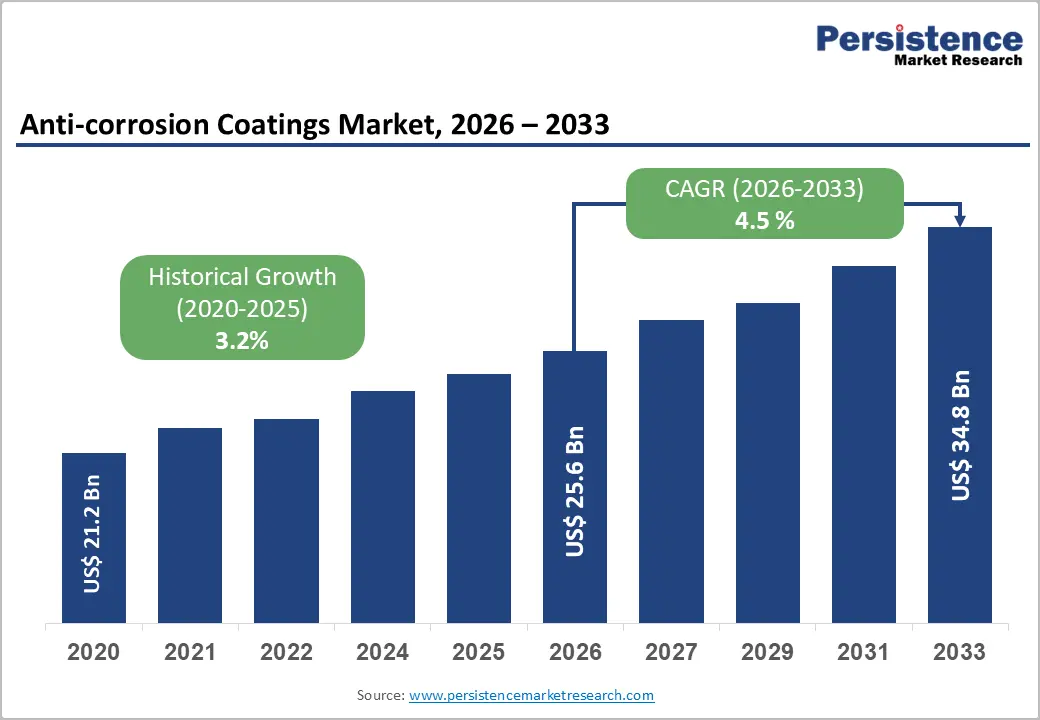

The global anti-corrosion coatings market size is expected to be valued at US$ 25.60 billion in 2026 and is projected to reach US$ 34.84 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

Expanding industrial infrastructure, rising awareness of asset lifecycle costs, and tightening regulatory mandates around corrosion protection exhibit a growing curve for anti-corrosion coatings market.

Key Industry Highlights:

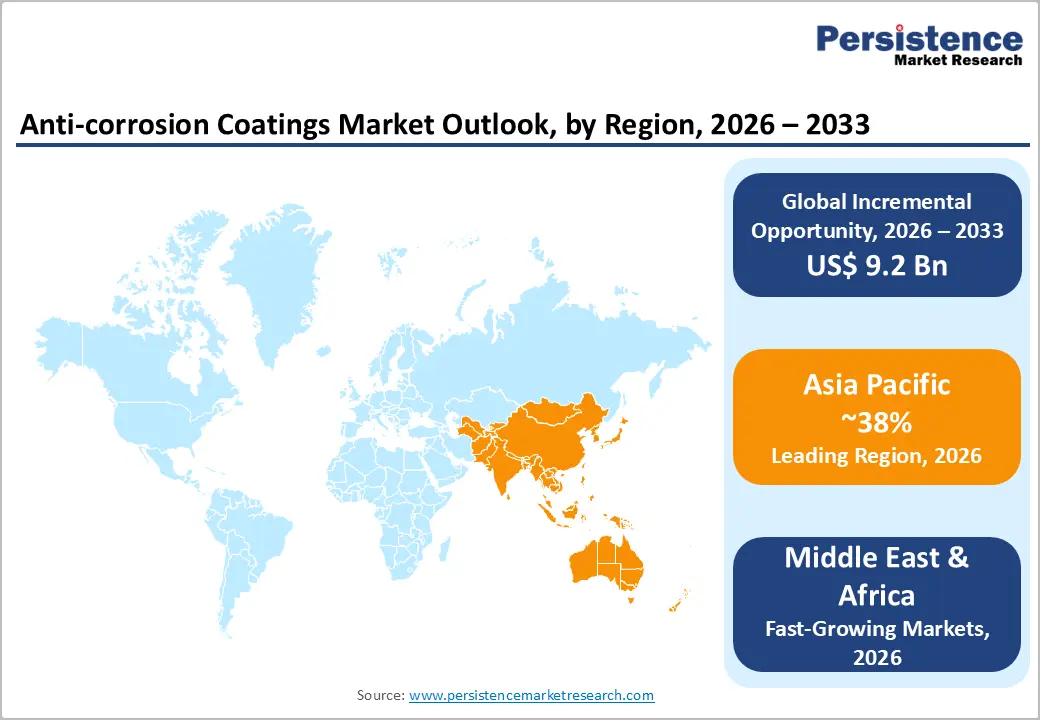

- Leading Region: Asia Pacific leads the global anti-corrosion coatings Market with a 38% share in 2026, representing US$ 9.73 billion, driven by China's dominant shipbuilding industry, India's multi-trillion-dollar infrastructure investment pipeline, and Southeast Asia's accelerating industrial base, structural forces that reinforce the region's leadership well beyond the current forecast period.

- Fastest Growing Region: The Middle East & Africa regions are attributed as fast-growing markets projected to reach a CAGR of 5.8% through 2033, primarily catalysed by Gulf state economic diversification programmes, large-scale desalination infrastructure build-out, and rising oil & gas upstream investment that demands intensive corrosion protection across pipelines and processing facilities.

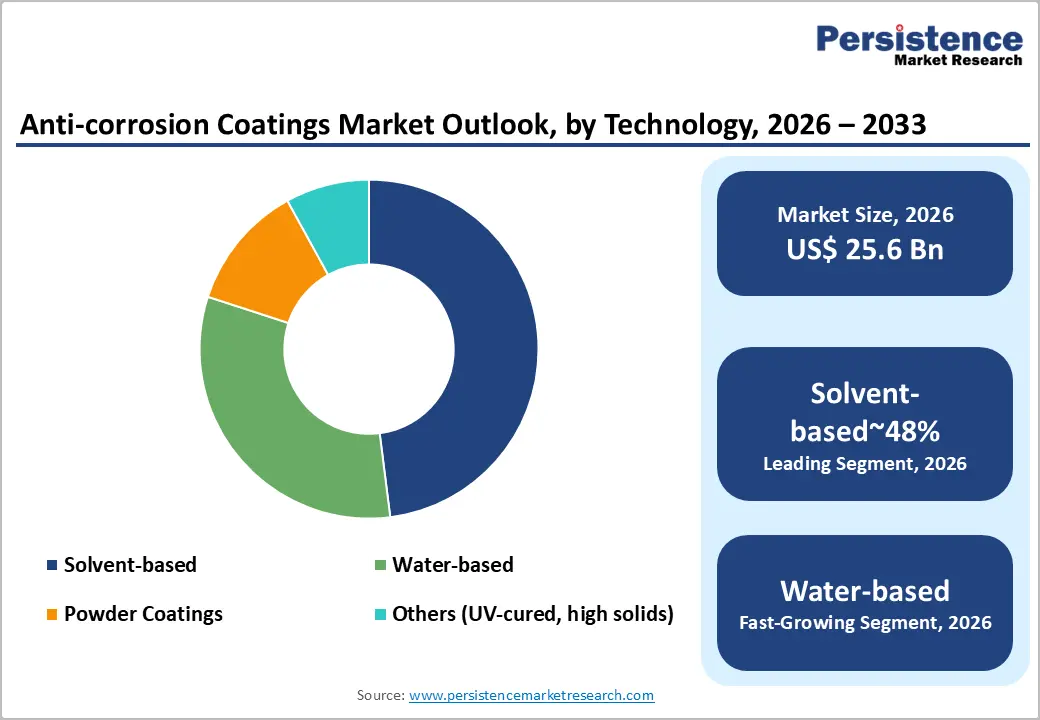

- Leading Segment: Solvent-based coatings dominate the anti-corrosion coatings market by technology with a 48.0% share in 2026, justified by their superior adhesion, chemical resistance, and applicability across heavy-duty industrial environments, attributes that continue to justify specification preference in oil & gas and marine end-uses despite increasing VOC regulatory pressure.

- Fast-Growing Segment: Water-based coatings represent the fastest growing technology segment in the anti-corrosion coatings market, with acceleration driven by tightening VOC regulations across the EU, US, and China, combined with genuine formulation improvements that are narrowing the performance gap with solvent-based systems, making early investment in waterborne product platforms a commercially strategic priority for manufacturers targeting the 2026 - 2033 growth window.

- Key Opportunity: The renewable energy sector represents the highest-conviction opportunity in the anti-corrosion coatings market between 2026 and 2033, as the quadrupling of global offshore wind capacity creates a multi-billion-dollar demand pool for premium marine-grade zinc-rich and polyurethane coating systems, favouring manufacturers that secure early classification society certification and build dedicated offshore energy application portfolios.

Market Dynamics

Drivers - Surging Global Infrastructure Development Fuelling Demand for Industrial Coatings

Governments and private developers across Asia Pacific, the Middle East, and North America are deploying multi-decade infrastructure programmes that structurally elevate demand for corrosion protection at scale. Construction and infrastructure projects, bridges, pipelines, water treatment facilities, and energy networks require protective coatings that deliver long-term durability against moisture, chemicals, and mechanical stress.

Global construction output is expected to grow by more than $4.5 trillion annually through the late 2020s, creating a sustained pipeline of new coating applications. Anti-corrosion coatings market demand drivers within this space include the increasing use of high-strength steel substrates that require advanced barrier and inhibitive coating systems to meet design-life specifications.

Expanding Oil & Gas Capital Expenditure and Asset Maintenance Spending

The oil & gas industry remains the single largest end-use vertical in the anti-corrosion coatings space, and renewed upstream and midstream investment cycles are creating direct demand for solvent-based and epoxy-based corrosion protection systems. As reported by regulatory bodies and industry associations, global upstream oil & gas capital expenditure exceeded $500 billion in 2024 for the first time since the commodity downturn of the mid-2010s, signalling a durable recovery in exploration and production infrastructure.

Offshore platforms, subsea pipelines, and onshore refineries require aggressive corrosion protection regimes given their exposure to saline environments, high temperatures, and chemical contaminants. The maintenance, repair, and overhaul (MRO) segment further amplifies this demand, as aging assets in the US, Middle East, and Southeast Asia require periodic recoating to extend operational life and comply with safety regulations.

Restraints - Volatile Raw Material Prices Creating Margin Pressure Across the Value Chain

The anti-corrosion coatings industry depends heavily on petrochemical-derived raw materials, including epoxy resins, titanium dioxide, and zinc, whose prices fluctuate in line with crude oil markets, supply chain disruptions, and geopolitical tensions. When raw material costs spike, manufacturers face a difficult choice between absorbing margin compression and passing costs onto customers in price-sensitive segments such as construction and automotive.

Based on authenticated market intelligence, epoxy resin prices alone experienced volatility exceeding 30% year-over-year during the 2021-2023 period, undermining the financial predictability that industrial coatings producers need to fund R&D and capacity expansion. This cost instability disproportionately affects mid-tier and regional players who lack the purchasing scale of global leaders like PPG Industries or Akzo Nobel.

Stringent VOC Regulations Increasing Reformulation Costs and Compliance Burdens

Regulatory frameworks governing VOC emissions, including the EU's Industrial Emissions Directive and US EPA standards, are compelling manufacturers to reformulate high-performance solvent-based coatings, which currently dominate the anti-corrosion coatings market share by technology. Reformulating to meet lower-VOC thresholds while preserving the adhesion, chemical resistance, and durability characteristics that end-users demand is technically complex and capital-intensive.

Smaller manufacturers in emerging markets, where regulatory enforcement is catching up to developed-market standards, face the prospect of abrupt compliance costs that threaten their competitive viability. The timeline misalignment between regulatory deadlines and product development cycles creates a real risk of product gaps in certain application segments, which in turn can slow overall anti-corrosion coatings market growth in the near term.

Opportunities - Accelerating Transition to Waterborne and Eco-friendly Protective Coatings

The structural shift away from solvent-based formulations toward water-based coatings represents one of the most commercially significant opportunities in the global Anti-corrosion Coatings Market over the 2026 - 2033 forecast window. Stricter VOC regulations across Europe, North America, and increasingly China and India are creating a regulatory tailwind that rewards manufacturers who invest early in waterborne technology platforms.

Industry participants that develop high-performance water-based anti-corrosion coatings with performance parity to solvent-based alternatives will be positioned to capture disproportionate market share as end-users in the marine, construction, and automotive sectors update their approved product lists. The waterborne industrial coatings segment is growing at a rate approximately 1.5 to 2 percentage points faster than the overall protective coatings market. Analysts advise that companies prioritise R&D investment in waterborne epoxy and polyurethane coatings hybrids, which offer the best near-term path to meeting both performance and sustainability requirements simultaneously.

Rising Demand from Renewable Energy and Power Generation Infrastructure

The global build-out of wind energy, solar farms, and grid infrastructure creates a sizeable incremental demand pool for corrosion protection solutions that the anti-corrosion coatings industry is only beginning to fully address. Offshore wind turbines, in particular, present an exceptionally demanding corrosion environment, combining saline spray, mechanical fatigue, and ultraviolet exposure, that requires premium zinc-rich, polyurethane, and epoxy coating systems. Based on authenticated market intelligence, global offshore wind capacity is projected to more than quadruple between 2024 and 2033, translating directly into multi-year procurement cycles for marine-grade anti-corrosion coatings.

Manufacturers that develop application-specific coating systems certified for wind turbine and solar racking substrates will secure long-term supply agreements with energy developers and EPC (Engineering, Procurement, and Construction) contractors. The power generation end-use segment is therefore emerging as a high-value, high-growth pocket within the broader anti-corrosion coatings market opportunities landscape, and early movers with certified product portfolios hold a durable advantage.

Category-wise Analysis

Technology Insights

Solvent-based coatings account for 48.0% of the global anti-corrosion coatings market in 2026, making them the leading technology across industrial coating applications. Their dominance is mainly due to strong adhesion, reliable film formation, and high chemical resistance across a wide range of surfaces and environments, capabilities that alternative technologies still struggle to fully match.

Industry data shows that sectors such as oil & gas and marine, which operate in highly corrosive conditions, continue to rely heavily on solvent-based epoxy and polyurethane coatings as their preferred choice, supporting steady demand. At the same time, water-based coatings are the fastest-growing segment, driven by stricter VOC regulations in regions like Europe, the U.S., and China, along with improvements in formulation performance. While solvent-based coatings will remain dominant in the near term, growing regulatory pressure and performance gains in waterborne systems are expected to gradually shift market dynamics over time.

Material Insights

Epoxy coatings account for 34.0% of the global anti-corrosion coatings market in 2026, making them the leading material segment by chemistry. Excellent adhesion, chemical resistance, moisture protection, and flexibility to work with both solvent-based and water-based systems are some of major advantages, it offers. These advantages enable epoxy coatings the preferred choice in key industries such as oil & gas, marine, and industrial construction.

Industry data also highlights that epoxy coatings dominate primer applications, especially in offshore platforms, where long-term durability is critical. Meanwhile, polyurethane coatings are the fastest-growing segment, driven by rising demand for UV resistance, glossy finishes, and color stability in automotive, aerospace, and marine applications. Epoxy’s leadership is expected to remain stable due to high switching costs and established industry standards. However, increasing adoption of polyurethane and hybrid systems suggests manufacturers should expand their offerings to meet evolving customer needs.

Coating Type Insights

Barrier coatings hold a 48.0% share of the global anti-corrosion coatings market in 2026. Their leadership comes from their simple yet effective function of protecting metal surfaces by blocking moisture, oxygen, and other corrosive elements. This makes them suitable for a wide range of industries, including construction, infrastructure, power generation, and industrial equipment. Industry data shows that epoxy-based and modified alkyd barrier coatings are widely used in maintenance applications, especially in oil & gas and construction sectors, due to their proven long-term performance.

On the other hand, sacrificial coatings, particularly zinc-rich types, are the fastest-growing segment, supported by increasing investments in offshore wind and marine infrastructure. While barrier coatings will continue to dominate, demand for zinc-based systems is rising due to their strong performance in harsh, high-moisture environments, encouraging the development of combined coating solutions.

End-use Insights

The oil & gas segment leads the anti-corrosion coatings market by end-use, accounting for 24.0% of the global market in 2026, equivalent to US$ 6.14 billion. This leadership is driven by the industry’s exposure to extremely harsh environments, including offshore platforms, pipelines, refineries, and LNG facilities, where corrosion protection is critical for safety and operations. Industry data estimates that corrosion costs the global oil & gas sector over $60 billion annually, highlighting the essential role of protective coatings.

The marine segment is the fastest-growing end-use category, supported by increasing investments in offshore wind projects, expansion of global shipping fleets, and rising naval defense spending, particularly in Asia Pacific and the Middle East. While oil & gas will maintain its strong position due to ongoing maintenance needs, the marine sector is gaining momentum. Suppliers with certifications from global classification bodies will have a competitive advantage in capturing this growing demand.

Regional Insights

North America Anti-corrosion Coatings Market Trends and Insights

North America holds 25.0% of the global anti-corrosion coatings market in 2026, US$ 6.40 Billion, driven by pipeline maintenance, infrastructure rehabilitation funding, and reindustrialisation. Strict EPA and OSHA regulations sustain premium demand. Future growth will be supported by LNG terminal expansion and offshore wind development along the Atlantic coast.

- United States Anti-corrosion Coatings Market Size

The United States represents 82% of North America’s market, reaching about US$ 5.25 Billion in 2026. Growth is driven by pipeline maintenance, infrastructure rehabilitation, and aerospace demand. Strong manufacturer-contractor relationships ensure stability, while semiconductor fabs and EV manufacturing expansion will create additional demand for specialised corrosion protection applications.

Europe Anti-corrosion Coatings Market Trends and Insights

Europe accounts for 20.0%, US$ 5.12 Billion of the global market in 2026, shaped by strict regulations and decarbonisation. REACH and emission directives drive waterborne and powder coatings adoption. Offshore wind growth offsets slower heavy industry, while green infrastructure and energy security investments will sustain long-term market expansion.

- Germany Anti-corrosion Coatings Market Size

Germany holds 22% of Europe’s market, reaching about US$ 1.13 Billion in 2026. Demand is driven by automotive manufacturing, machinery, chemicals, and wind turbines. Future growth will be supported by energy transition initiatives and offshore wind expansion, sustaining strong demand for marine and power-generation corrosion protection coatings.

- United Kingdom Anti-corrosion Coatings Market Size

The UK accounts for 15% of Europe’s market, valued at US$ 768 Million in 2026. Demand is led by North Sea oil and offshore wind. Marine coatings dominate consumption. Future growth is driven by the government’s 50 GW offshore wind target by 2030, increasing demand for zinc-rich and polyurethane coatings.

- France Anti-corrosion Coatings Market Size

France holds 13% of Europe’s market US$ 666 Million in 2026, driven by nuclear infrastructure requiring specialised coatings. Aerospace demand also contributes significantly. Future growth will be supported by new nuclear reactor development and offshore wind expansion, sustaining demand for high-performance corrosion protection systems.

Asia Pacific Anti-corrosion Coatings Market Trends and Insights

Asia Pacific leads with 38.0% share US$ 9.73 Billion in 2026, driven by China’s infrastructure, India’s manufacturing growth, and Southeast Asia’s industrial expansion. While the Middle East & Africa grows fastest, Asia Pacific remains dominant, supported by construction, shipbuilding, and automotive demand through 2033.

- China Anti-corrosion Coatings Market Size

China holds 45% of Asia Pacific’s market, valued at US$ 4.38 Billion in 2026. Shipbuilding drives major demand, supported by infrastructure expansion and Belt and Road projects. Stricter VOC regulations will accelerate adoption of waterborne coatings, benefiting manufacturers with advanced environmentally compliant product portfolios.

- Japan Anti-corrosion Coatings Market Size

Japan accounts for 18% of Asia Pacific’s market US$ 1.75 Billion in 2026, driven by automotive, marine, and industrial sectors. Aging infrastructure supports maintenance demand. Future growth will come from offshore wind expansion and ongoing industrial facility upgrades under national productivity enhancement initiatives.

- India Anti-corrosion Coatings Market Size

India represents 12% of Asia Pacific’s market US$ 1.17 Billion in 2026, with strong growth momentum. Demand is driven by infrastructure projects under NIP, shipbuilding, and defense manufacturing. The PLI scheme boosts industrial expansion, positioning India among the fastest-growing regional markets through 2033.

Competitive Landscape

The anti-corrosion coatings market operates as a moderately consolidated global industry, where a small number of multinational coating majors, including PPG Industries, Akzo Nobel, Sherwin-Williams, and BASF, command significant scale advantages in technology, distribution, and customer relationships, while a large population of regional and specialty players compete on formulation agility, price, and application expertise. The primary basis of competition at the top tier is technology differentiation and specification approval depth, companies with the broadest portfolio of certified, application-specific corrosion protection solutions command premium pricing and long-cycle contracts.

At the mid-market level, price competitiveness and local technical support are the dominant competitive variables. Key strategic themes shaping the anti-corrosion coatings competitive landscape in 2025 include accelerated M&A activity targeting waterborne technology capabilities, sustainability-driven product innovation, and digital coating management services that extend manufacturer relationships beyond point-of-sale into ongoing asset maintenance programmes.

Key Developments:

- January, 2025: Akzo Nobel N.V. announced the commercial launch of a new generation of low-VOC, waterborne epoxy primer system targeting offshore wind turbine applications across the European and North American markets, designed to meet the most current EU emission standards while matching the corrosion resistance performance of solvent-borne equivalents.

- March, 2025: PPG Industries, Inc. completed the acquisition of a specialty marine coatings manufacturer in Southeast Asia, expanding its geographic presence in high-growth shipbuilding markets and reinforcing its anti-corrosion coatings market share in the Asia Pacific region's vessel maintenance and newbuild segments.

- October, 2024: Jotun A/S unveiled a proprietary antifouling and corrosion protection coating system combining zinc-rich sacrificial protection and bio-inspired surface chemistry, targeting the global commercial shipping fleet and positioning the company at the intersection of the marine coatings and sustainability investment narratives.

Anti-corrosion Coatings Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 21.19 Billion |

| Current Market Value (2026) | US$ 25.60 Billion |

| Projected Market Value (2033) | US$ 34.84 Billion |

| CAGR (2026 - 2033) | 4.5% |

| Leading Region | Asia Pacific (38%) |

| Dominant Technology | Solvent-based (48.0%) |

| Top-ranking Material | Epoxy (34.0%) |

| Top-ranking Coating Type | Barrier Coatings (48.0%) |

| Top-ranking End-use | Oil & Gas (24.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 9.24 Billion |

Companies Covered in Anti-corrosion Coatings Market

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- BASF SE

- Jotun A/S

- Hempel A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Axalta Coating Systems Ltd.

- RPM International Inc.

- Ashland Global Holdings Inc.

- 3M Company

- Sika AG

- Chugoku Marine Paints, Ltd.

- Wacker Chemie AG

- Tikkurila Oyj

- Teknos Group

- Henkel AG & Co. KGaA

- Rust-Oleum Corporation

- Dampney Company, Inc.

Frequently Asked Questions

The global Anti-corrosion Coatings Market is valued at US$ 25.60 billion in 2026 and is projected to reach US$ 34.84 billion by 2033, growing at a CAGR of 4.5%.

Growth is driven by rising infrastructure investments and expanding oil & gas capex, which increase demand for durable corrosion protection solutions across industrial, energy, and construction sectors globally.

Solvent-based coatings lead with 48.0% share in 2026 due to superior adhesion, durability, and chemical resistance, making them ideal for heavy-duty industrial and marine environments.

Asia Pacific dominates with 38.0% share, supported by strong shipbuilding activity, large-scale infrastructure projects, and rapid industrial growth across China, India, and Southeast Asia.

Key opportunities lie in waterborne and zinc-rich coatings for offshore wind and marine sectors, driven by rising renewable energy investments and long-term infrastructure maintenance requirements.

Leading companies include AkzoNobel, PPG Industries, Sherwin-Williams, Jotun, and Hempel, operating in a highly competitive, innovation-driven market.