- Pharmaceuticals

- Alopecia Treatment Market

Alopecia Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Alopecia Treatment Market by Treatment Type (Topical Drugs, Oral Drugs, Injectable, Hair Transplant Services, Low-Level Laser Therapy), by End-user, by Regional Analysis, 2026 - 2033

Alopecia Treatment Market Size and Trend Analysis

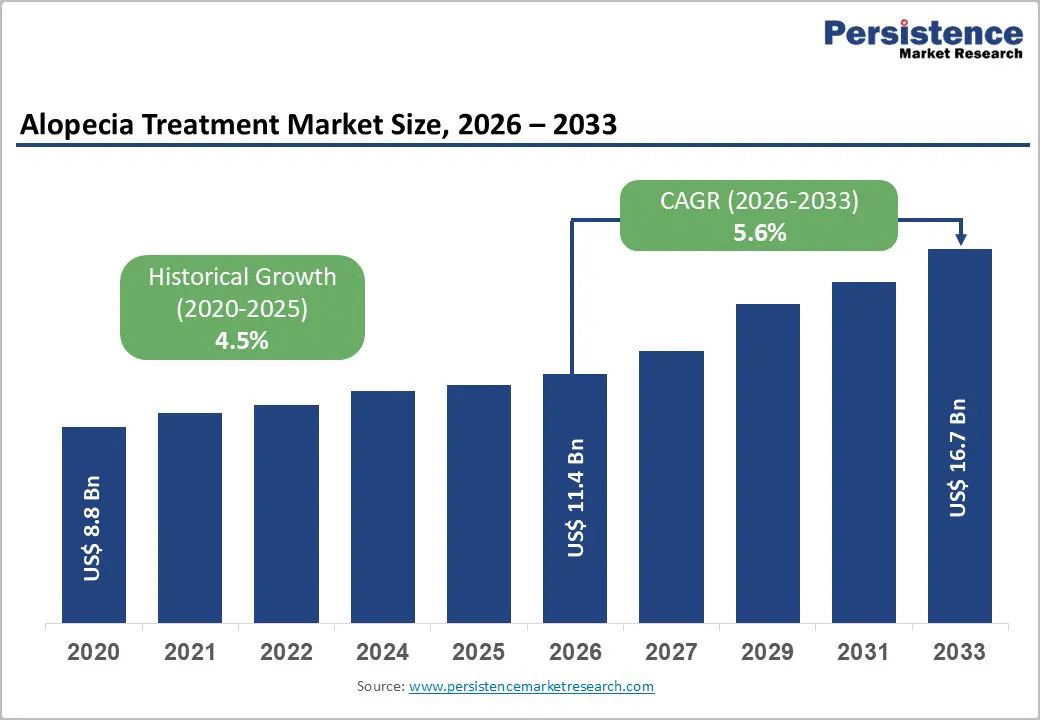

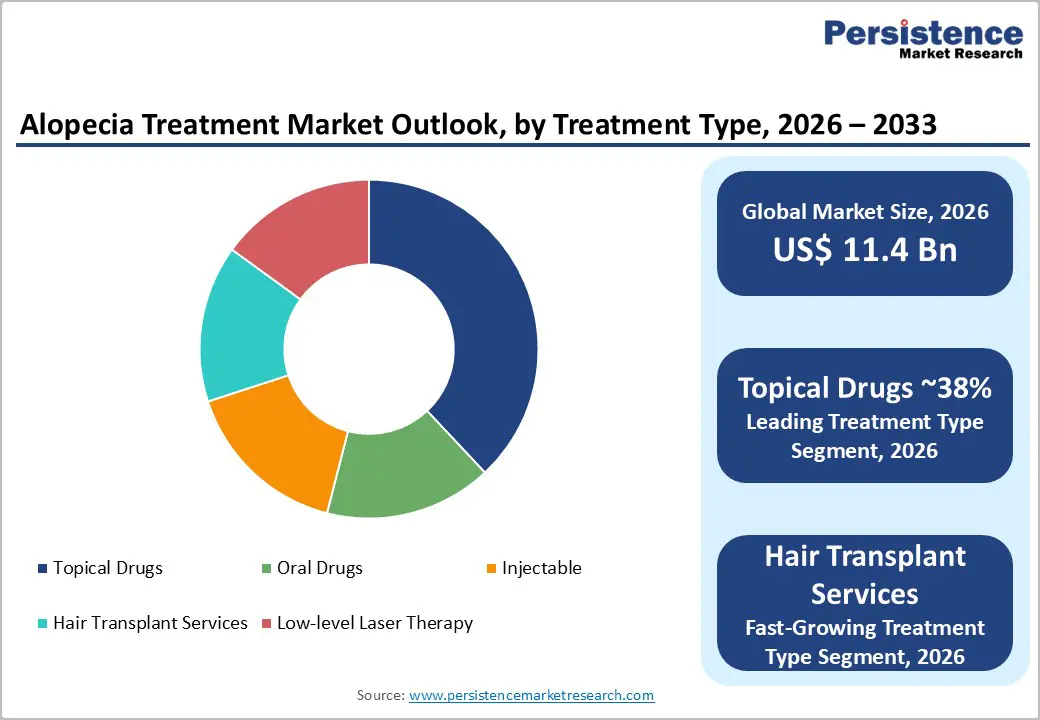

The global alopecia treatment market size is expected to be valued at US$ 11.4 billion in 2026 and projected to reach US$ 16.7 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The alopecia treatment market focuses on therapies and procedures designed to manage hair loss conditions such as androgenetic alopecia and alopecia areata. This steady growth trajectory is driven by the rising global prevalence of hair loss disorders, growing consumer awareness of evidence-based treatments, and increasing FDA-approved innovations, including JAK inhibitors and advanced topical formulations.

The American Academy of Dermatology estimates that over 80 million Americans experience hereditary hair loss, while the National Alopecia Areata Foundation reports that alopecia areata affects around 6.8 million people in the U.S. alone. Expanding demand from pharmaceuticals, aesthetic clinics, and advanced hair restoration services continues to strengthen global market growth through 2033.

Key Industry Highlights:

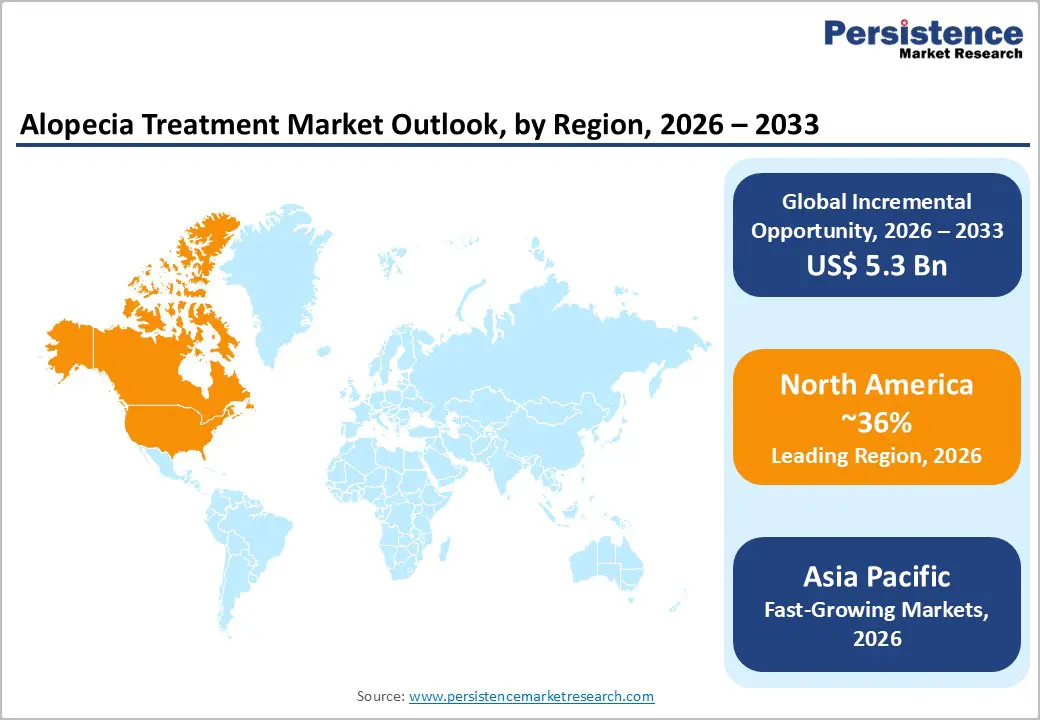

- Leading Region - North America is likely to lead with 36% share in 2026, driven by FDA-approved therapies, advanced treatment infrastructure, and high hereditary hair loss prevalence.

- Fastest Growing Region - Asia Pacific is poised for a fast-growth due to JAK approvals, rising alopecia cases, strong medical tourism, and expanding regional treatment access.

- Dominant Leading Type - Topical drugs dominate with 38% share, supported by widespread OTC minoxidil use, affordability, and strong global product availability.

- Fast-Growing Treatment Type - Hair transplant services grow fastest due to FUE adoption, rising procedure demand, and affordable medical tourism destinations like India.

- Key Opportunity - JAK inhibitor expansion and home-use LLLT devices create strong opportunities through advanced therapies, convenience, and direct-to-consumer treatment models.

Market Dynamics

Drivers - FDA Breakthrough Approvals of JAK Inhibitors Transforming Alopecia Areata Treatment Landscape

The landmark regulatory approvals of oral Janus kinase (JAK) inhibitors for alopecia areata represent the most transformative development in the alopecia treatment market in decades, creating an entirely new and rapidly growing pharmacological segment.

The U.S. Food and Drug Administration (FDA) approved baricitinib (Olumiant) by Eli Lilly and Company in June 2022 as the first systemic treatment for severe alopecia areata in adults, followed by ritlecitinib (Litfulo) by Pfizer in June 2023 for patients aged 12 and older. These approvals the first systemic drugs specifically approved for alopecia areata, addressing a long-unmet clinical need for the estimated 147 million people worldwide affected by the condition per the NAAF. The commercial rollout of these therapies is generating significant prescription volume and broadening pharmaceutical revenue, validating investment in alopecia oral drug development and stimulating further pipeline activity across the sector.

Rising Prevalence of Hair Loss Disorders and Growing Demand for Aesthetic Hair Restoration

The escalating global prevalence of androgenetic alopecia, combined with growing societal acceptance of cosmetic hair restoration procedures, is fueling multi-segment demand across the alopecia treatment market. The AAD estimates that androgenetic alopecia, the most common form of hair loss, affects ~50 million men and 30 million women in the U.S.

Globally, studies published in the Journal of Investigative Dermatology indicate that androgenetic alopecia affects up to 50% of men by age 50 and 25% of women by age 50. Post-pandemic psychological stress, a documented trigger for telogen effluvium and stress-related alopecia, further expanded the patient population seeking treatment. The expanding middle-class population in Asia Pacific and Latin America, combined with increasing disposable income and the destigmatization of male aesthetic procedures, is driving growing demand for hair transplant services and premium topical treatment products.

Restraints - Side Effect Profiles of Systemic Treatments Limiting Broad Adoption

Despite the therapeutic breakthrough represented by JAK inhibitors, the side effect profiles of oral systemic alopecia treatments remain a significant commercial constraint. FDA labeling for baricitinib (Olumiant) and other JAK inhibitors includes a Boxed Warning for serious infections, major adverse cardiovascular events (MACE), thrombosis, and malignancy risks. These safety warnings prompt cautious prescribing behavior, particularly among primary care physicians, limiting penetration to specialist dermatology settings and restricting the eligible patient population to severe disease cases, thereby constraining the maximum addressable market for this highest-value pharmacological segment.

High Cost of Hair Transplant Procedures and Limited Insurance Coverage

Hair transplant services while the fast-growing segment are predominantly classified as elective cosmetic procedures and are generally excluded from health insurance reimbursement in most markets globally. In the U.S., a single follicular unit extraction (FUE) hair transplant session can cost between USD 4,000 to USD 15,000 or more depending on graft count and clinic reputation.

This out-of-pocket cost barrier restricts market penetration to higher-income consumer segments, limiting procedure volume growth particularly in lower- and middle-income markets where alopecia prevalence is also significant. Economic downturns and consumer discretionary spending sensitivity add further volatility to this procedure-based revenue stream.

Opportunities - Hair Transplant Services are the Fast-Growing Segment Driven by FUE Technology and Medical Tourism

Hair transplant services represent the fastest-growing treatment type, driven by rapid advancement of minimally invasive follicular unit extraction (FUE) and robotic-assisted hair transplantation technologies, significantly improving procedural outcomes and reducing recovery time relative to traditional strip harvesting methods. The International Society of Hair Restoration Surgery (ISHRS) Practice Census reported that hair restoration procedures have increased substantially year-on-year, with over 703,183 surgical hair restoration procedures performed globally in its most recent survey.

The dramatic growth of medical tourism for hair transplantation, particularly in Turkey, India, and Thailand, where procedure costs are 60-80% lower than in the U.S. and Western Europe, is expanding the global addressable market significantly. Robotic systems, including ARTAS iX by Restoration Robotics, are further elevating procedure quality and clinic capacity, driving premium service positioning.

Low-Level Laser Therapy and Emerging Technology-Driven Home Care Expansion

Low-level laser therapy (LLLT) for hair loss represents a compelling commercial opportunity at the intersection of clinical efficacy and growing consumer interest in non-pharmacological, technology-driven treatments. The FDA has cleared multiple LLLT devices for androgenetic alopecia through its 510(k) pathway, including devices from Theradome and LUTRONIC, validating the technology for both professional clinic and at-home consumer applications.

Published clinical studies in the Journal of the American Academy of Dermatology have demonstrated statistically significant improvements in hair count density following LLLT treatment. The growing home care settings end-user segment enabled by FDA-cleared consumer LLLT devices, subscription-based topical treatment regimens, and teledermatology platforms represents an emerging direct-to-consumer revenue model that bypasses clinic-based channels and dramatically expands the total addressable market for technology-driven alopecia management.

Category-wise Analysis

Treatment Type Insights

Topical drugs lead the treatment type category, accounting for ~38% of the total share in 2026. The dominance of topical treatments reflects the global ubiquity of minoxidil, the most widely used topical hair loss treatment, which is available over the counter in most major markets following its initial FDA approval as a 2% topical solution for men in 1988 and subsequent extensions to 5% formulation and women's use. The FDA's approval of over-the-counter topical minoxidil formulations and the 2022 OTC approval of women's minoxidil 2% foam significantly expanded consumer access.

Topical DHT-blocking serums, ketoconazole shampoos, and novel peptide-based formulations by companies including The Himalaya Drug Company, Cipla, and Dr. Reddy's Laboratories further diversify this segment. The accessibility, affordability, and non-invasive nature of topical treatments ensure their continued leadership in both developed and emerging markets.

End-user Insights

Dermatologic and trichology clinics represent the leading end-user segment, accounting for an estimated 35% of global market share in 2025. These specialized clinical settings serve as the primary point of care for all non-OTC alopecia treatments, including prescription oral drugs such as JAK inhibitors and finasteride, platelet-rich plasma (PRP) injections, and in-clinic LLLT sessions commanding both high visit frequency and premium service pricing. The growth of trichology as a recognized subspecialty within dermatology is institutionalizing systematic hair loss evaluation protocols that drive multi-modality treatment uptake.

Aesthetic Clinics are the fastest-growing end-user segment, reflecting the destigmatization and premiumization of hair restoration as an elective cosmetic service. In the U.S., the AAD's practice guidelines for alopecia management are standardizing dermatology clinic workflows and expanding the number of qualified providers offering both medical and procedural hair loss treatments.

Regional Insights

North America Alopecia Treatment Market Trends and Insights

North America leads the global market with ~36% of market share in 2026, underpinned by the landmark FDA approvals of baricitinib and ritlecitinib, a well-established dermatology clinical network, high consumer health awareness, and growing adoption of premium hair restoration services by both men and women across the U.S. and Canada.

U.S. Alopecia Treatment Market Size

The U.S. dominates North America, accounting for ~89% of regional revenue in 2025, estimated at around US$ 3.6 billion. With over 80 million Americans experiencing hereditary hair loss per the AAD, robust prescription drug reimbursement frameworks, FDA-cleared LLLT devices, and expanding robotic hair transplant clinic networks, the U.S. remains the world's most commercially advanced alopecia treatment market.

Europe Alopecia Treatment Market Trends and Insights

Europe is the second-largest regional market, with Germany, the UK, France, and Italy as key national markets. EMA regulatory alignment with U.S. JAK inhibitor approvals, strong NHS and statutory health insurance dermatology referral networks, and growing aesthetic clinic density are driving multi-treatment segment demand. Medical tourism for hair transplantation, particularly to Turkey, also generates regional awareness and post-procedure topical treatment demand.

Germany Alopecia Treatment Market Size

Germany is Europe's largest alopecia treatment market, estimated at ~US$ 560 million in 2025, representing around 24% of European revenue. Germany's strong pharmaceutical industry, GKV statutory insurance coverage for prescription dermatological treatments, and well-developed trichology clinic network support consistent multi-modality alopecia treatment adoption.

UK Alopecia Treatment Market Size

The UK holds ~17% of the regional share in 2026, valued at around US$ 397 million. NHS dermatology services, NICE clinical guidelines for alopecia management, and a rapidly growing private aesthetic hair clinic sector, including rising demand for FUE transplants, sustain strong and diversified alopecia treatment demand.

Asia Pacific Alopecia Treatment Market Trends and Insights

Asia Pacific is the fastest-growing regional market for alopecia treatment, driven by a large and underserved patient population, rapidly expanding dermatology and aesthetic clinic infrastructure, and growing consumer spending on personal care and hair health. China represents the region's largest and most dynamic market, with the National Medical Products Administration (NMPA) approvals of novel alopecia treatments, including JAK inhibitors, expanding clinical treatment access. Rising urban-professional stress levels are a significant alopecia trigger, and the cultural importance of hair in East and Southeast Asian societies is fueling demand across all treatment modalities.

India Alopecia Treatment Market Size

India is a high-growth emerging alopecia treatment market, estimated at ~US$ 310 million in 2025, representing around 12% of the Asia Pacific revenue. India's large young adult population susceptible to stress-induced alopecia, growing pharmaceutical sector with domestic generic minoxidil and finasteride manufacturers, including Cipla and Dr. Reddy's Laboratories, and expanding medical tourism for hair transplantation are key growth drivers.

Japan Alopecia Treatment Market Size

Japan is the second-largest alopecia treatment market, likely to be valued at ~US$ 450 million in 2026, representing around 17% of regional revenue. Japan's well-developed pharmaceutical sector, with domestic players including Taisho Pharmaceutical Holdings and Shiseido offering established hair care and treatment products combined with MHLW-regulated dermatological drug access, sustains a mature and premium alopecia treatment market.

Competitive Landscape

The global market is moderately fragmented, with pharmaceutical multinationals including Eli Lilly, Pfizer, and Merck & Co. dominating the prescription oral drug segment, while consumer healthcare companies and generic manufacturers, including Cipla, Dr. Reddy's Laboratories, and Johnson & Johnson, lead topical treatment portfolios. Medical device companies, including Theradome and LUTRONIC, compete in the LLLT segment. Key differentiators include FDA approval status for novel indications, pipeline depth, brand equity in OTC markets, and geographic aesthetic clinic network scale.

Subscription-based DTC topical treatment models and telehealth-integrated trichology consultations are emerging as disruptive business model trends.

Key Developments:

- In July 2025, Sun Pharmaceutical Industries Limited announced that LEQSELVI™ (deuruxolitinib) 8 mg tablets became available in the U.S. for healthcare providers and adult patients with severe alopecia areata, indicated for the treatment of severe alopecia areata in adults.

- In October 2024, Dr. Batra's Group introduced XOGEN, a treatment for hereditary hair loss using exosomes for targeted growth, requiring four to five sessions and a simple hair care routine.

- In September 2024, Eli Lilly and EVA Pharma agreed to extend baricitinib's access to 20,000 people in 49 low- to middle-income African countries by 2030, treating rheumatoid arthritis, alopecia areata, atopic dermatitis, and COVID-19.

- In September 2024, Amplifica Holdings Group conducted its first-in-human trial of AMP-303, a new injectable treatment for androgenetic alopecia. The study found no severe adverse events and showed significant non-vellus hair count increases.

- In July 2024, Aveda introduced the Invati Ultra Advanced Collection, a five-step anti-hair loss system combining Ayurvedic remedies and vegan ingredients, including shampoo, conditioner, serum, and foam.

Companies Covered in Alopecia Treatment Market

- Elli Lilly and Company

- Teva Pharmaceutical Industries Ltd.

- Merck & Co., Inc.

- Johnson & Johnson, Inc.

- Dr. Reddy’s Laboratories Ltd.

- Cipla Ltd.

- Cellmid Ltd.

- The Himalaya Drug Company

- Taisho Pharmaceutical Holdings Co., Ltd

- Shiseido Co., Ltd.

- Zhangguang 101 Science & Technology Co., Ltd.

- Pfizer

- Thera dome

- LUTRONIC

- Others

Frequently Asked Questions

The global alopecia treatment market is estimated at US$ 11.4 billion in 2026.

FDA-approved JAK inhibitors, rising hereditary hair loss cases, growing hair restoration demand, and expanding OTC topical treatments are driving strong market growth.

North America leads with ~36% of global market share in 2026.

Global expansion of JAK inhibitor therapies and rapidly growing hair transplant services through FUE and robotic systems offer major growth opportunities.

Elli Lilly and Company, Teva Pharmaceutical Industries Ltd., Merck & Co., Inc., Johnson & Johnson, Inc., and Dr. Reddy’s Laboratories Ltd. are considered the leading players.