- Technology

- Agritech Platform Market

Agritech Platform Market Size, Share, and Growth Forecast 2026–2033

Agritech Platform Market by Offering (Platform, Services), by Deployment (Cloud-based, On-Premises, Hybrid), by Application (Precision Farming, Irrigation Management, Livestock Management, Supply Chain Management, Financial Services, Advisory & Decision Support Systems, Digital Market Linkages, Others), and Regional Analysis, 2026–2033

Global Agritech Platform Market Size and Trend Analysis

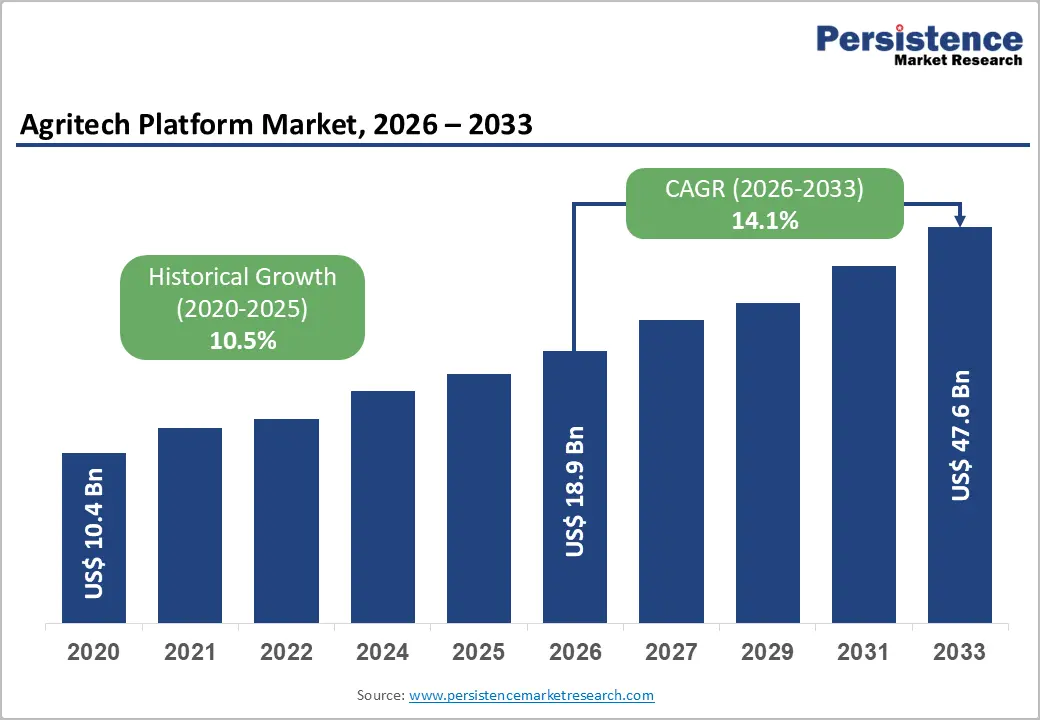

The global agritech platform market is expected to be valued at US$ 18.9 billion in 2026 and is projected to reach US$ 47.6 billion by 2033, growing at a CAGR of 14.1% between 2026 and 2033, driven by accelerating smallholder digitisation in emerging economies, large-scale government investment in smart farming infrastructure, and the rapid maturation of IoT sensor networks, satellite imagery analytics, and AI-driven advisory tools. Rise in food security pressures driven by climate volatility and a global population expected to reach 9.8 billion by 2050 are compelling both public and private stakeholders to prioritise platform-based agricultural solutions at an unprecedented pace.

Key Industry Highlights:

- Prominent Offering Type: Platform segment dominates with over 63.0% market share in 2026, valued at more than US$ 11.9 Bn, driven by its role as the core data orchestration layer integrating IoT, satellite imagery, analytics, and farm workflows.

- Leading Deployment: On-Premises holds over 42% share in 2026, valued at more than US$ 7.9 billion, driven by data sovereignty concerns, regulatory requirements, and limited rural connectivity in emerging markets.

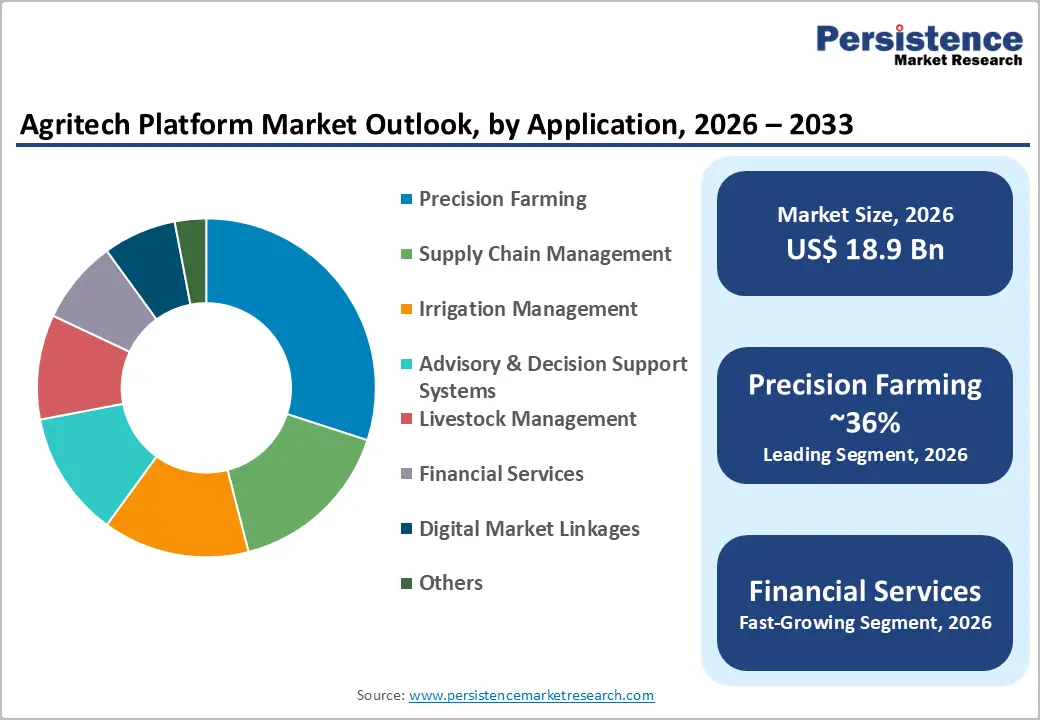

- Leading Application: Precision Farming leads with over 36.0% market share in 2026, valued at more than US$ 6.8 Bn, driven by strong ROI through yield optimization and input cost reduction.

- Fastest Growing Application: Financial Services is the fastest-growing segment, supported by the expansion of digital credit, crop insurance, and embedded finance models in emerging markets.

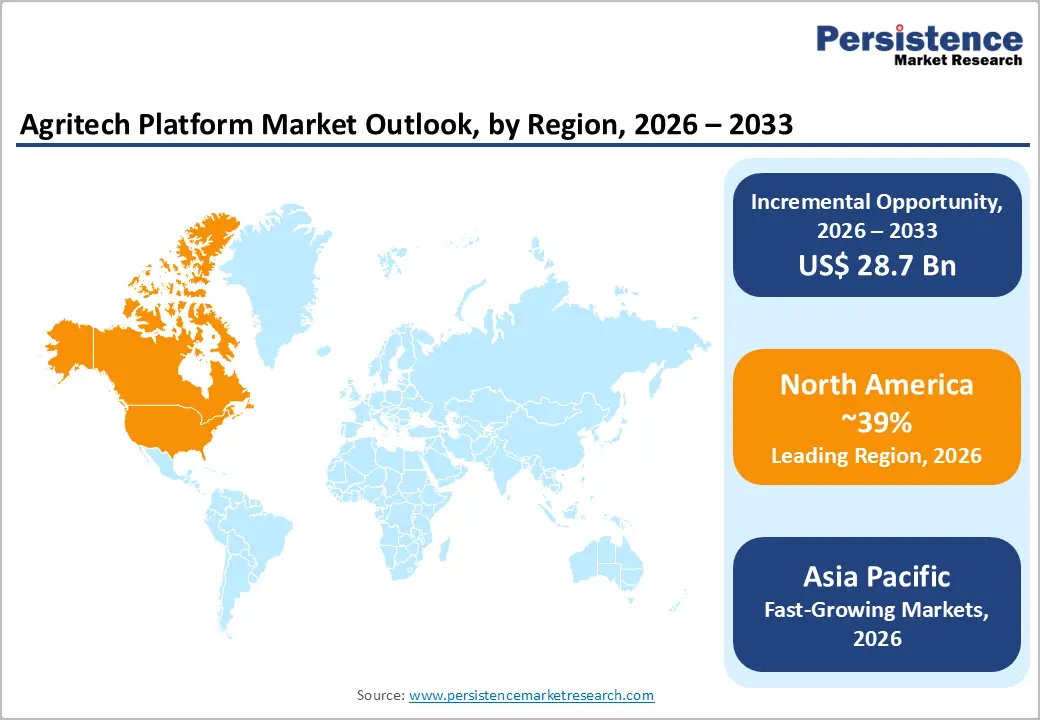

- Regional Leadership: North America dominates with over 39.0% share in 2026, valued at more than US$ 7.4 Bn, supported by large-scale commercial farming, a strong investment ecosystem, and policy backing.

- Fast-Growing Market: Asia Pacific is the fast-growing market with a positive CAGR driven by a massive smallholder base, government digitization initiatives, and rapid mobile internet penetration.

Market Dynamics

Drivers – Rise in Demand for Precision Agriculture and Data-Driven Farm Management

Farmers and agribusinesses worldwide are increasingly demanding real-time, actionable intelligence rather than relying on reactive, experience-based decision-making. The growth of the agritech platform sector is driven by the proven yield improvements and cost efficiencies delivered by integrated solutions. Studies indicate that precision agriculture technologies reduce input waste by up to 15–20% while improving crop yields by an average of 10–12% per season.

Governments across North America, the European Union, and South Asia have incorporated digital agriculture initiatives into national food security strategies, creating sustained, policy-backed demand that remains resilient across economic cycles. The proliferation of affordable IoT sensors, drone-based imaging, and edge computing has further lowered the technical barriers to adoption, enabling mid-sized and smallholder farms to participate in the digital agriculture ecosystem.

Surge in Private Investment and Strategic Public-Private Partnerships

Venture capital and strategic corporate investment flowing into agritech platforms reached record levels between 2022 and 2024, signalling strong investor confidence in the sector's long-term revenue potential and competitive moats. Global agritech investment has increased significantly, with platform-layer companies capturing a disproportionate share as investors prioritise scalable, recurring-revenue business models over hardware-intensive alternatives.

Public-private partnerships, such as those embedded within the European Union's Common Agricultural Policy (CAP) 2023–2027 framework and India’s Digital Agriculture Mission, are channelling structured subsidies and co-investment into platform infrastructure, thereby reducing adoption friction at the farm level. These funding dynamics create a positive flywheel, where more capital enables richer platform features, which attract more users, generating more agronomic data and ultimately strengthening the platform's AI and advisory capabilities.

Restraints - Infrastructure Deficits and Connectivity Gaps in Key Agricultural Geographies

The most consequential structural restraint is the persistent absence of reliable broadband and mobile connectivity across rural agricultural regions in Sub-Saharan Africa, parts of South Asia, and inland Latin America. Without stable connectivity, cloud-dependent platform features become operationally unreliable, undermining farmer trust and stalling adoption precisely in the markets with the highest latent demand.

Approximately 35% of rural agricultural communities in low-income countries lack access to consistent 4G or broadband internet, creating a technology access divide that platform vendors cannot solve unilaterally. This compresses total addressable market penetration timelines and forces vendors to invest in costly offline-first or hybrid architecture alternatives that erode margin and complicate product roadmaps.

Fragmented Data Standards and Interoperability Barriers

The agritech platform industry suffers from a critical interoperability challenge. The absence of universally adopted data standards means that platform ecosystems frequently cannot communicate with one another, locking farmers into single-vendor relationships and inhibiting the ecosystem-wide data aggregation that powers superior AI and advisory outcomes. This fragmentation discourages farm operators, particularly large commercial enterprises managing multi-vendor technology stacks, from committing to any single platform, elongating sales cycles and increasing churn risk. Industry bodies, including the AgGateway Consortium and Open Ag Data Alliance (OADA), have advanced interoperability frameworks, but adoption remains uneven across geographies and vendor categories.

Opportunities - Monetising the Agronomic Data Layer Through Embedded Financial and Insurance Products

Transforming proprietary agronomic data such as yield histories, soil health indices, and climate risk profiles into underwriting intelligence for embedded credit, crop insurance, and input financing products creates substantial opportunities. Platform operators that have accumulated multi-season farm-level datasets are uniquely positioned to partner with agricultural lenders, insurance companies, and development finance institutions to offer parametric insurance and digital credit products directly through the platform interface. This embedded finance model generates high-margin, recurring fee revenue that is structurally differentiated from the commoditizing software subscription layer.

According to a study, less than 12% of smallholder farmers in emerging markets currently hold any form of formal agricultural insurance, representing a vast underserved population that agritech platforms are structurally positioned to serve. Vendors that move quickly to establish fintech partnerships and regulatory licences in growth markets, particularly India, Nigeria, and Indonesia, will create durable competitive advantages that pure-software platforms cannot easily replicate.

Expansion into Climate-Smart Agriculture and Carbon Credit Monetisation

The global policy pivot toward carbon neutrality and climate-resilient food systems is creating a monetisable opportunity to serve as the measurement, reporting, and verification (MRV) infrastructure for agricultural carbon markets. Platforms that integrate satellite-based soil carbon monitoring, irrigation efficiency tracking, and regenerative practice verification enable farmers to participate in voluntary carbon markets, earning incremental income while platform operators capture transaction fees and data licensing revenue.

The voluntary carbon market is projected to grow 15-fold by 2030, with soil sequestration credits from agricultural land representing one of the fastest-scaling credit categories. Agritech platform vendors with robust geospatial data capabilities and credible third-party verification partnerships are best positioned to capture this opportunity, particularly as COP commitments from governments in the European Union, United States, and India translate into funded national carbon farming programmes.

Category-wise Analysis

Offering Insights

The platform segment accounts for 63.0% of the global agritech platform market in 2026, with a value exceeding US$ 11.9 Billion. This dominance reflects the fundamental economics of agricultural digitization, as farm operators, agribusinesses, and government agencies all require a centralised data orchestration layer integrating IoT inputs, satellite imagery, weather analytics, and farm management workflows before any advisory or transactional service delivers value. Enterprise-grade platform deployments across North America and Europe carry average contract values 2.5 to 3.5 times higher than equivalent service-only engagements, reinforcing the segment's disproportionate revenue contribution.

Services are growing at a significant rate, accelerating as platform penetration deepens and farm operators demand implementation support, agronomic advisory, and data integration consulting to maximise platform ROI. The Platform segment’s dominance is expected to remain structurally stable in the near term, but Services revenue will grow proportionally faster as the installed base matures and post-deployment engagement becomes the primary competitive battleground. This trajectory signals that while platform sales are necessary, they are insufficient; vendors must build scalable service delivery capabilities to defend customer lifetime value and reduce churn.

Deployment Insights

On-premises deployment model accounts for over 42% share in 2026, reaching over US$ 7.9 Billion in value. This growth is driven by large commercial farming operations, state-owned agribusinesses in Asia Pacific and the Middle East, and government-linked agricultural agencies, which universally prioritise on-premises deployment to maintain sovereign control over sensitive farm productivity data, avoid cloud connectivity dependencies in low-infrastructure environments, and comply with national data residency regulations. More than 60% of government-affiliated agricultural platform procurement contracts in markets such as China, Russia, and the Gulf Cooperation Council specify on-premises or private cloud deployment as a contractual requirement, underpinning the segment’s baseline demand.

Cloud-based deployment is the fastest-growing segment, driven by the economics of SaaS scalability, the declining cost of cloud infrastructure, and the growing comfort among mid-market agribusinesses with off-premises data management. The share leadership of on-premises deployment faces a gradual but tangible erosion as cloud security frameworks mature, connectivity infrastructure improves in rural regions, and younger farm operators who are more comfortable with subscription-based digital services represent a growing share of platform procurement decisions.

Application Insights

Precision farming accounts for 36.0% of the global agritech platform market in 2026, reaching over US$6.8 billion, as it directly addresses the most universal and financially material pain point in agriculture input cost management and yield optimization by integrating satellite imagery, soil sensors, variable-rate technology, and predictive analytics into a single operational workflow. Farms deploying precision farming platforms achieve a return on investment within 1–3 growing seasons in high-value crop categories, a payback period that drives rapid commercial adoption.

Financial Services encompassing embedded credit, crop insurance, digital payments, and farm lending analytics is the fastest growing application, driven by the exponential expansion of rural fintech in South Asia and Sub-Saharan Africa, where digital farm data is increasingly accepted as collateral by alternative lenders and microfinance institutions. Platforms that sequence their application roadmap from Precision Farming as the acquisition hook into Financial Services and advisory tools as the retention and monetisation layer will achieve the highest customer lifetime value and lowest churn rates across the forecast period.

Regional Insights

North America Agritech Platform Market Trends and Insights

North America accounts for 39.0% of the global agritech platform market share in 2026, representing US$ 7.4 Billion. The region's structural advantages, large-scale commercial farming operations with high capital intensity, a mature venture and corporate investment ecosystem, and deep integration between university research institutions and agritech commercialisation pipelines create a self-reinforcing demand environment that competitors from other regions find difficult to replicate. Regulatory tailwinds, including the US Farm Bill's sustained investment in agricultural technology programmes and USDA precision agriculture initiatives, add a durable policy subsidy layer to organic market demand.

The United States Agritech Platform market represents 86.0% of the North America regional market in 2026, reaching over to US$ 6.3 billion, driven by the highest concentration of large-scale commercial farms, precision agriculture technology adopters, and agritech venture capital in the world. The US agricultural sector's relentless focus on input cost efficiency, the USDA's Climate-Smart Commodities programme allocating over US$ 3 Billion to technology-enabled sustainable farming, and the rapid integration of AI-powered crop intelligence into existing farm management systems.

Europe Agritech Platform Market Trends and Insights

Europe accounts for 25.0% of the global Agritech Platform market in 2026, representing US$ 4.7 Billion, with the region's growth shaped decisively by the European Union's Farm to Fork Strategy and the Common Agricultural Policy (CAP) 2023–2027, both of which embed digital agriculture adoption as a compliance and incentive condition for subsidy access. Demand is concentrated particularly in Germany, France, and the Netherlands, where large commercial farms and well-capitalised agricultural cooperatives have the financial capacity to invest in enterprise-grade platform solutions. The EU's commitment to reducing chemical pesticide use by 50% by 2030 will structurally drive adoption of precision application platforms across the continent.

Germany Agritech Platform market is reaching over to US$ 1.04 billion value by 2026, underpinned by Germany's position as Europe's largest agricultural economy and its advanced engineering culture that accelerates IoT sensor and smart machinery integration with digital farm management platforms. The France Agritech Platform market is accounting for over US$ 900 million in value by 2026, supported by its position as the France’s leading agricultural producer within the European Union and strong policy backing through the Stratégie nationale pour la transition agroécologique. Growth is concentrated in high-value segments such as viticulture, cereal farming, and dairy livestock, where digital advisory and precision irrigation platforms deliver tangible gains in productivity and cost efficiency.

United Kingdom Agritech Platform market value is expected to exceed over US$ 700 million by 2026, shaped by the post-Brexit transition from EU CAP subsidies to the Environmental Land Management (ELM) scheme, which explicitly rewards technology-enabled environmental stewardship outcomes across UK farms. The UK government's Farming Innovation Programme, directs co-investment into agritech platform development and farmer adoption, combined with a vibrant agritech startup ecosystem concentrated around Cambridge and London.

Asia Pacific Agritech Platform Market Trends and Insights

Asia Pacific accounts for 23.0% of the global agritech platform market in 2026, representing US$ 4.4 Billion, and is the fastest-growing region in the agritech platform market with a projected CAGR of 19.3% through 2033. The structural acceleration forces are uniquely powerful in this region, driven by a combined smallholder farming population exceeding 500 million households, aggressive government digitisation mandates in China, India, and Indonesia, and explosive mobile internet penetration that enables platform access in regions where desktop infrastructure never existed.

The China agritech platform market is expected to surpass US$ 1.7 billion value by 2026, driven by the Chinese government's Digital Village Strategy and sustained state investment in agricultural AI, drone technology, and supply chain digitalisation as strategic priorities within the 14th Five-Year Plan. The demand comes from the rapid modernisation of China's livestock and aquaculture sectors, where platform-based monitoring delivers measurable biosecurity and productivity benefits.

The Japan Agritech Platform market is expected to account for over 12.0% of the Asia Pacific regional market in 2026, shaped by Japan's acute agricultural labour shortage, with the average farmer age exceeding 68 years, which is forcing rapid adoption of autonomous farm management platforms and AI-powered crop monitoring tools to sustain food production with a shrinking workforce. Japan's agritech platform market will serve as a global proving ground for fully autonomous and robotics-integrated farm management systems, with commercial technologies likely to diffuse into other high-labour-cost markets through the forecast period.

India Agritech Platform market represents over US$ 870 million in value by 2026 and is expanding at one of the fastest rates within the Asia Pacific region, driven by the government's Digital Agriculture Mission, the PM-KISAN farmer income support scheme's digital payment infrastructure, and a highly active domestic agritech startup ecosystem headquartered in Bengaluru, Hyderabad, and Mumbai. India's 140 million smallholder farming households represent the largest single addressable market for mobile-first, vernacular-language agritech platforms globally, and domestic entrepreneurs are rapidly building platform businesses calibrated to this user base.

Competitive Landscape

The agritech platform market operates as a moderately fragmented competitive landscape, a structural condition that reflects the market's geographic diversity, the heterogeneity of farming system types, and the early-stage maturity of cross-border platform scaling. The scale-driven players typically well-capitalised Western platforms and technology conglomerates, compete on data breadth, AI capability, and enterprise integrations, while differentiation-driven players, predominantly regional specialists and emerging-market startups, compete on localisation depth, agronomic relevance, and ecosystem partnerships with input suppliers, financial institutions, and government bodies. The dominant strategic themes shaping competitive positioning include platform consolidation through M&A, the embedding of generative AI into agronomic advisory workflows, and the race to capture the embedded financial services revenue layer.

Key Developments:

- In August 2025: Cropin secured a €700K strategic program to deploy its AI-powered agritech platform for scaling regenerative potato farming across Europe. The initiative uses satellite data, AI, and predictive analytics to improve yield, reduce pesticide use, and enhance sustainability. It highlights growing adoption of data-driven agritech platforms in climate-smart agriculture.

- In January 2025: DeHaat acquired AgriCentral to strengthen its digital farming ecosystem. The deal enhances DeHaat’s capabilities in AI-driven crop advisory, farmer engagement, and data analytics. This acquisition supports DeHaat’s strategy to become a full-stack agritech platform serving millions of farmers across India.

Companies Covered in Agritech Platform Market

- Indigo Ag

- CropIn Technology Solutions

- DeHaat

- WayCool Foods

- Ninjacart

- CropX

- Arable

- Gamaya

- Ceres Imaging

- Farmonaut

- AgroStar

- FarmEye

- Intello Labs

- Farmlink

- Others

Frequently Asked Questions

The global Agritech Platform market is valued at US$ 18.90 Billion in 2026 and is projected to reach US$ 47.58 Billion by 2033, growing at a CAGR of 14.1% over the forecast period, driven by the acceleration of government-backed digital agriculture mandates combined with the rapid commercialisation of AI-powered farm management.

The growth is driven by productivity gains and government-backed digital agriculture programs. Public funding and subsidies are reducing adoption risk and accelerating platform penetration.

Platform segment holds the largest share over 63.0% in 2026, due to its ability to integrate multiple value-chain functions into a single unified ecosystem. End-to-end integration reduces fragmentation, improves decision-making through centralized data, and increases user stickiness, making platforms difficult to replace once adopted.

North America leads with more than 39% share & US$ 7.37 Bn value in 2026, due to large-scale commercial farming and a strong innovation ecosystem. Early adoption of AI and advanced technologies strengthens its continued dominance.

The key opportunity lies in embedded financial services like crop insurance, digital credit, and input financing. Companies leveraging farm data and forming early partnerships gain a long-term competitive advantage.

The leading companies in the Agritech Platform market include Indigo Ag, CropIn Technology Solutions, DeHaat, Ninjacart, Ceres Imaging, and CropX, among others.