- Executive Summary

- Global Adrenogenital Syndrome Treatment Market Snapshot, 2025 and 2033

- Market Opportunity Assessment, 2025 - 2033, US$ Mn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-economic Factors

- Global Sectoral Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Tool Adoption Analysis

- Regulatory Landscape

- Value Chain Analysis

- PESTLE Analysis

- Porter’s Five Force Analysis

- Price Analysis, 2025A

- Key Highlights

- Key Factors Impacting Deployment Costs

- Pricing Analysis, By Drug Class

- Global Adrenogenital Syndrome Treatment Market Outlook

- Key Highlights

- Market Volume (Units) Projections

- Market Size (US$ Mn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast

- Historical Market Size (US$ Mn) Analysis, 2025-2025

- Market Size (US$ Mn) Analysis and Forecast, 2025 - 2033

- Global Adrenogenital Syndrome Treatment Market Outlook: Drug Class

- Introduction / Key Findings

- Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Drug Class, 2025 - 2025

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Drug Class, 2025 - 2033

- Glucocorticoids

- Mineralocorticoids

- Hormone Modulators

- Steroidogenesis Inhibitors

- Market Attractiveness Analysis: Drug Class

- Global Adrenogenital Syndrome Treatment Market Outlook: Disease Type

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Disease Type, 2025 - 2025

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2025 - 2033

- Classic Congenital Adrenal Hyperplasia (CAH) - Salt-Wasting

- Classic CAH - Simple Virilizing

- Non-Classic CAH

- Market Attractiveness Analysis: Disease Type

- Global Adrenogenital Syndrome Treatment Market Outlook: Route of Administration

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Route of Administration, 2025 - 2025

- Market Size (US$ Mn) Analysis and Forecast, By Route of Administration, 2025 - 2033

- Oral

- Intravenous

- Intramuscular

- Subcutaneous

- Long-Acting

- Market Attractiveness Analysis: Route of Administration

- Key Highlights

- Global Adrenogenital Syndrome Treatment Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) and Volume (Units) Analysis, By Region, 2025 - 2025

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Region, 2025 - 2033

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Adrenogenital Syndrome Treatment Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Route of Administration

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- U.S.

- Canada

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Drug Class, 2025 - 2033

- Glucocorticoids

- Mineralocorticoids

- Hormone Modulators

- Steroidogenesis Inhibitors

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2025 - 2033

- Classic Congenital Adrenal Hyperplasia (CAH) - Salt-Wasting

- Classic CAH - Simple Virilizing

- Non-Classic CAH

- Market Size (US$ Mn) Analysis and Forecast, By Route of Administration, 2025-2033

- Oral

- Intravenous

- Intramuscular

- Subcutaneous

- Long-Acting

- Market Attractiveness Analysis

- Europe Adrenogenital Syndrome Treatment Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Drug Class

- By Disease Type

- Route of Administration

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Drug Class, 2025 - 2033

- Glucocorticoids

- Mineralocorticoids

- Hormone Modulators

- Steroidogenesis Inhibitors

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2025 - 2033

- Classic Congenital Adrenal Hyperplasia (CAH) - Salt-Wasting

- Classic CAH - Simple Virilizing

- Non-Classic CAH

- Market Size (US$ Mn) Analysis and Forecast, By Route of Administration, 2025-2033

- Oral

- Intravenous

- Intramuscular

- Subcutaneous

- Long-Acting

- Market Attractiveness Analysis

- East Asia Adrenogenital Syndrome Treatment Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Route of Administration

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- China

- Japan

- South Korea

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Drug Class, 2025 - 2033

- Glucocorticoids

- Mineralocorticoids

- Hormone Modulators

- Steroidogenesis Inhibitors

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2025 - 2033

- Classic Congenital Adrenal Hyperplasia (CAH) - Salt-Wasting

- Classic CAH - Simple Virilizing

- Non-Classic CAH

- Market Size (US$ Mn) Analysis and Forecast, By Route of Administration, 2025-2033

- Oral

- Intravenous

- Intramuscular

- Subcutaneous

- Long-Acting

- Market Attractiveness Analysis

- South Asia & Oceania Adrenogenital Syndrome Treatment Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Route of Administration

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Drug Class, 2025 - 2033

- Glucocorticoids

- Mineralocorticoids

- Hormone Modulators

- Steroidogenesis Inhibitors

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2025 - 2033

- Classic Congenital Adrenal Hyperplasia (CAH) - Salt-Wasting

- Classic CAH - Simple Virilizing

- Non-Classic CAH

- Market Size (US$ Mn) Analysis and Forecast, By Route of Administration, 2025-2033

- Oral

- Intravenous

- Intramuscular

- Subcutaneous

- Long-Acting

- Market Attractiveness Analysis

- Latin America Adrenogenital Syndrome Treatment Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Route of Administration

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Drug Class, 2025 - 2033

- Glucocorticoids

- Mineralocorticoids

- Hormone Modulators

- Steroidogenesis Inhibitors

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2025 - 2033

- Classic Congenital Adrenal Hyperplasia (CAH) - Salt-Wasting

- Classic CAH - Simple Virilizing

- Non-Classic CAH

- Market Size (US$ Mn) Analysis and Forecast, By Route of Administration, 2025-2033

- Oral

- Intravenous

- Intramuscular

- Subcutaneous

- Long-Acting

- Market Attractiveness Analysis

- Middle East & Africa Adrenogenital Syndrome Treatment Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2025 - 2025

- By Country

- By Drug Class

- By Disease Type

- By Route of Administration

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025 - 2033

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Mn) and Volume (Units) Analysis and Forecast, By Drug Class, 2025 - 2033

- Glucocorticoids

- Mineralocorticoids

- Hormone Modulators

- Steroidogenesis Inhibitors

- Market Size (US$ Mn) Analysis and Forecast, By Disease Type, 2025 - 2033

- Classic Congenital Adrenal Hyperplasia (CAH) - Salt-Wasting

- Classic CAH - Simple Virilizing

- Non-Classic CAH

- Market Size (US$ Mn) Analysis and Forecast, By Route of Administration, 2025-2033

- Oral

- Intravenous

- Intramuscular

- Subcutaneous

- Long-Acting

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Pfizer Inc.

- Overview

- Segments and Deployments

- Key Financials

- Market Developments

- Market Strategy

- Merck & Co., Inc.

- Novartis AG

- F. Hoffmann-La Roche Ltd.

- Recordati Rare Diseases

- Neurocrine Biosciences

- Sanofi S.A.

- Bayer AG

- Takeda Pharmaceutical Company

- AbbVie Inc.

- Endo International plc

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

- Ipsen S.A.

- Crinetics Pharmaceuticals

- Pfizer Inc.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Pharmaceuticals

- Adrenogenital Syndrome Treatment Market

Adrenogenital Syndrome Treatment Market Size, Share, and Growth Forecast, 2026 - 2033

Adrenogenital Syndrome Treatment Market by Drug Class (Glucocorticoids, Mineralocorticoids, Hormone Modulators, Steroidogenesis Inhibitors), Disease Type (Classic CAH – Salt-Wasting, Classic CAH – Simple Virilizing, Non-Classic CAH), Route of Administration (Oral, Intravenous, Intramuscular, Subcutaneous, Long-Acting), and Regional Analysis for 2026 - 2033

Key Industry Developments

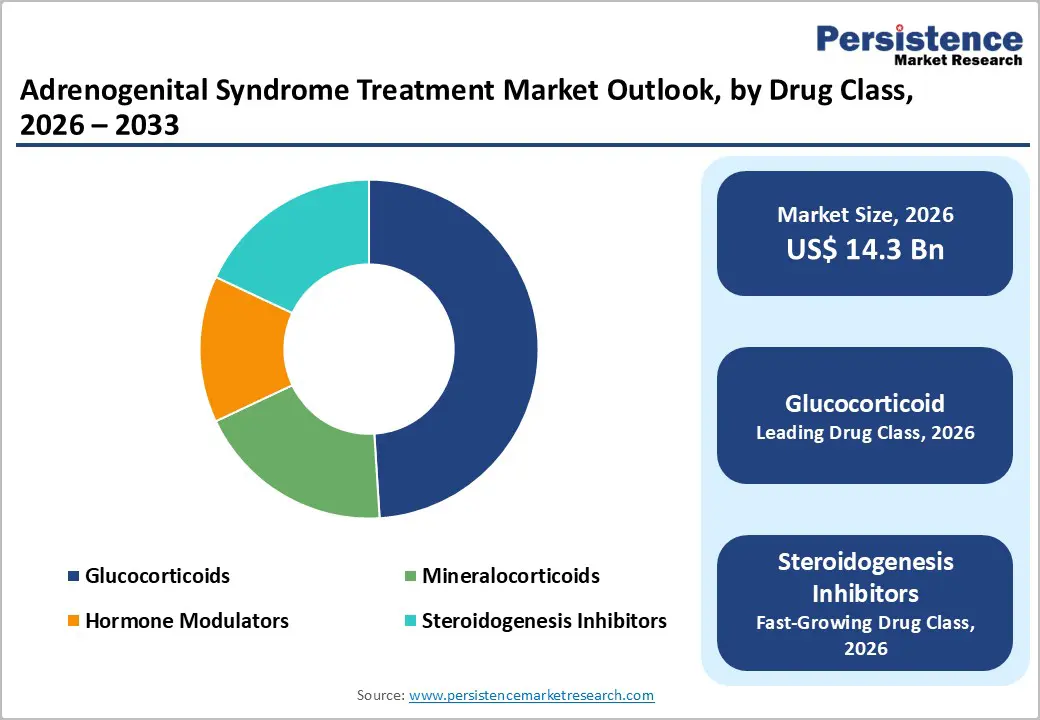

- Leading Drug Class: Glucocorticoids are expected to lead with about 49% revenue share in 2026, while steroidogenesis inhibitors are projected to grow the fastest at nearly 7.4% CAGR through 2033, supported by advances in targeted endocrine therapies.

- Dominant Disease Type: Classic CAH – salt-wasting is projected to dominate with roughly 52% share in 2026, while non-classic CAH is anticipated to grow the fastest during 2026–2033, driven by improved diagnostic screening.

- Route of Administration Trends: Oral administration is expected to lead with approximately 60% share in 2026, with long-acting formulations recording the fastest growth through 2033, reflecting demand for improved treatment adherence.

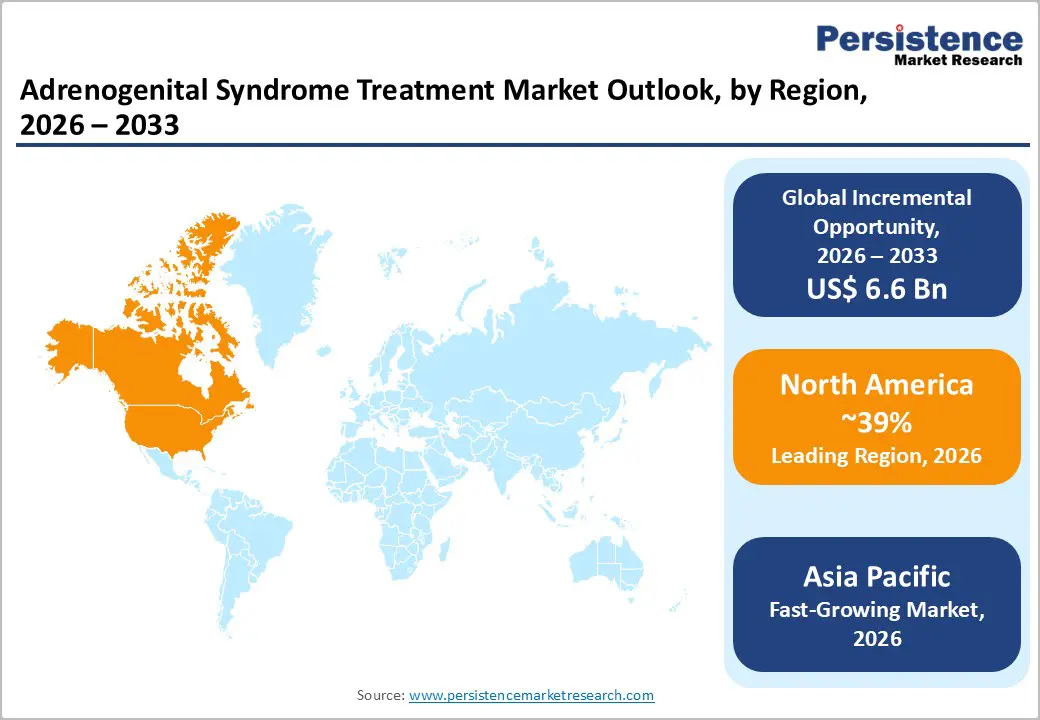

- Regional Leadership: North America is projected to dominate with nearly 39% share in 2026, while Asia Pacific is expected to grow the fastest at approximately 6.7% CAGR through 2033, on account of expanding healthcare infrastructure and screening programs.

- Expanding Diagnosis Base: Rising newborn screening programs and improved diagnostic capabilities are expanding the global CAH patient population, increasing early diagnosis rates and strengthening long-term demand for hormone replacement therapies and specialized endocrine care.

| Key Insights | Details |

|---|---|

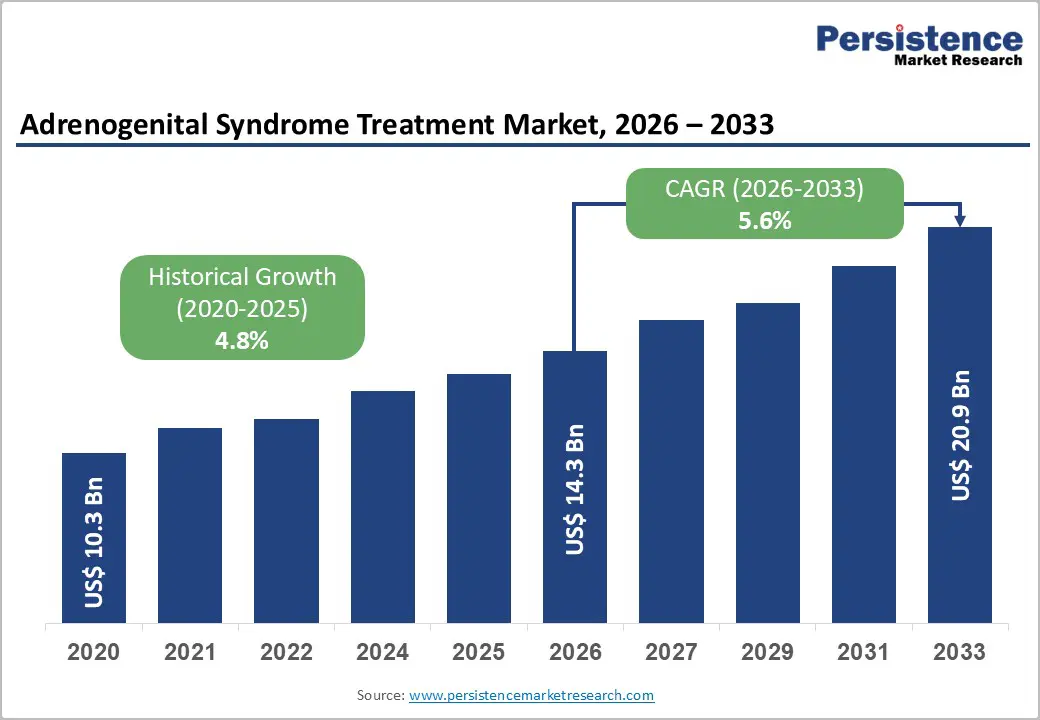

|

Adrenogenital Syndrome Treatment Market Size (2026E) |

US$ 14.3 Bn |

|

Market Value Forecast (2033F) |

US$ 20.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growing Global Prevalence of Congenital Adrenal Hyperplasia

Adrenogenital syndrome, primarily caused by CAH, affects approximately 1 in 10,000–15,000 live births globally, according to data from the World Health Organization (WHO) and the National Institutes of Health (NIH). Increasing newborn screening programs have significantly improved detection rates. The U.S. Centers for Disease Control and Prevention (CDC) reports that all U.S. states include CAH in mandatory newborn screening panels, leading to earlier diagnosis and treatment initiation. Newborn screening has now been adopted in more than 49 countries worldwide, enabling earlier identification of adrenal hormone deficiencies and improving survival outcomes for infants with severe forms of CAH.

Early detection increases demand for lifelong hormone replacement therapies including glucocorticoids and mineralocorticoids. Moreover, healthcare systems in Europe and Asia are expanding neonatal screening coverage, further increasing patient identification rates. Public health agencies continue to strengthen screening infrastructure and follow-up care systems. For example, the U.S. Health Resources and Services Administration (HRSA) maintains CAH as part of the national newborn screening panel to ensure early identification and clinical intervention. As diagnostic technologies become more accessible in developing economies, the patient pool is expected to expand steadily, directly supporting pharmaceutical demand in the adrenogenital syndrome treatment market.

Advancements in Hormone Replacement Therapies and Rising Investment in Rare Disease Research

Technological advancements in endocrinology treatment are improving the effectiveness of CAH management. According to European Society for Paediatric Endocrinology (ESPE) clinical guidelines, optimized dosing regimens and new steroid formulations have improved patient outcomes by reducing adrenal crises and hormonal imbalance. Pharmaceutical companies are developing modified-release glucocorticoids and long-acting steroid delivery mechanisms designed to mimic natural circadian cortisol rhythms. These therapeutic improvements are helping physicians maintain better hormonal balance and reduce complications associated with conventional treatment protocols.

Recent regulatory approvals are also accelerating treatment innovation. In December 2024, the U.S. Food and Drug Administration (FDA) approved crinecerfont (Crenessity) as a treatment to help control androgen levels in patients with classic CAH when used alongside glucocorticoid therapy, marking an important advancement in targeted endocrine treatment strategies. Additionally, in 2025 the FDA approved a hydrocortisone oral solution for pediatric adrenal insufficiency, improving dosing precision and treatment accessibility for younger patients. These developments reflect increasing global investment in rare disease therapeutics. According to Organisation for Economic Co-operation and Development (OECD) health expenditure statistics, global healthcare spending surpassed US$ 9 trillion in 2024, with a growing share directed toward rare disease research and orphan drug development, strengthening the long-term innovation pipeline for CAH therapies.

Long-Term Steroid Therapy Side Effects and Treatment Compliance Challenges

One of the most significant challenges in CAH management is the long-term adverse effects of chronic steroid therapy. Continuous glucocorticoid administration can lead to complications including weight gain, hypertension, reduced bone density, and metabolic disorders. According to the Endocrine Society clinical guidelines, approximately 30–40% of CAH patients experience metabolic complications during long-term treatment. These complications require frequent dose adjustments and continuous monitoring by endocrinologists. Physicians often face difficulty balancing adequate androgen suppression with minimizing steroid exposure. This treatment complexity increases the burden on both patients and healthcare providers managing lifelong endocrine disorders.

These side effects often result in poor patient compliance, particularly among adolescents transitioning from pediatric to adult endocrine care. Long-term therapy requires strict adherence to dosing schedules and continuous medical supervision. In 2025, clinical endocrinology studies highlighted treatment discontinuation rates exceeding 20% in some patient groups, indicating persistent adherence challenges. Medical experts also emphasize that optimizing steroid dosing remains difficult because biochemical markers do not always correlate with clinical outcomes. Consequently, inconsistent treatment adherence can increase the risk of adrenal crises and hormonal imbalance. This challenge highlights the need for safer long-acting therapies and improved treatment monitoring systems.

Limited Disease Awareness and Underdiagnosis in Emerging Healthcare Systems

Although CAH screening is common in developed countries, diagnosis rates remain significantly lower in many developing healthcare systems due to limited newborn screening infrastructure. According to UNICEF maternal and child health reports, several low-income regions still lack nationwide neonatal metabolic screening programs. Without systematic screening, infants with adrenal enzyme deficiencies may remain undiagnosed during early childhood. In many healthcare settings, symptoms of CAH can initially resemble other endocrine or metabolic disorders. This diagnostic uncertainty delays treatment initiation and increases the risk of severe complications.

In 2025, clinical research conducted in Southeast Asia highlighted that delayed CAH diagnosis remains common where newborn screening programs are absent or limited. Studies examining patient experiences reported that families often struggle to access specialized endocrine testing and treatment services due to gaps in diagnostic infrastructure. In several regions, access to hormone testing laboratories and trained endocrinologists remains limited. These systemic healthcare gaps contribute to underreported cases and delayed disease management. Consequently, despite increasing awareness of endocrine disorders, limited diagnostic capacity continues to restrict market penetration for CAH therapies across developing healthcare systems.

Advancements in Long-Acting Hormone Therapies and Precision Medicine Approaches

One of the most promising opportunities lies in circadian rhythm-based hormone replacement therapies. These treatments replicate the body's natural cortisol secretion cycle, improving metabolic stability. Clinical trials conducted in Europe and North America demonstrate that modified-release hydrocortisone therapies reduce cortisol fluctuations and improve patient quality of life. Researchers are also investigating therapies targeting CYP21A2 gene mutations, which account for the majority of CAH cases. These innovations are expanding treatment options beyond conventional steroid therapy. Advances in precision endocrinology are enabling more targeted approaches to hormone regulation and long-term disease control.

Recent regulatory developments further strengthen this opportunity. In December 2024, the U.S. FDA approved crinecerfont (Crenessity) as a treatment used alongside glucocorticoids to control androgen levels in patients aged four years and older with classic CAH. This therapy helps reduce excess adrenal androgen production and allows physicians to lower glucocorticoid doses while maintaining hormonal balance. In parallel, clinical studies are evaluating gene therapy approaches such as adreno-associated virus (AAV)-based treatments designed to correct adrenal enzyme deficiencies, reflecting growing scientific interest in long-term disease-modifying therapies. Together, these advancements are expected to accelerate innovation and create significant opportunities for pharmaceutical companies developing next-generation CAH treatments.

Expansion of Newborn Screening Programs in Emerging Healthcare Markets

Governments in Asia and Latin America are expanding national newborn screening initiatives to detect metabolic and endocrine disorders earlier. For example, healthcare authorities in India and China initiated pilot neonatal screening programs in several states and provinces, covering disorders such as congenital hypothyroidism and CAH. These initiatives aim to strengthen early disease detection and improve clinical outcomes for infants born with endocrine disorders. Expanding screening coverage also enables healthcare systems to identify adrenal hormone deficiencies before symptoms become severe. This trend is expected to significantly increase the number of patients entering long-term hormone therapy programs.

Recent public health research highlights the scale of these screening initiatives. A neonatal screening study in Guangzhou, China screened more than 818,000 newborns for CAH using biochemical testing of 17-hydroxyprogesterone, demonstrating how large-scale screening programs can detect endocrine disorders early and enable prompt treatment. Similar screening expansion initiatives are being evaluated across several Asian healthcare systems. As these programs expand nationally, the number of diagnosed CAH patients is expected to increase substantially, improving treatment access and strengthening demand for hormonal therapies. Improved newborn screening coverage therefore represents a major opportunity for pharmaceutical companies and healthcare providers involved in endocrine disorder management.

Category-wise Analysis

Drug Class Insights

Glucocorticoids are expected to represent the leading drug class, accounting for approximately 49% of the adrenogenital syndrome treatment market revenue share in 2026. These medications replace deficient cortisol and suppress excessive adrenal androgen production, making them the primary therapy for CAH. Widely used drugs such as hydrocortisone, prednisone, and dexamethasone remain central to long-term disease management in both pediatric and adult patients. Clinical guidelines continue to recommend glucocorticoids as first-line therapy due to their ability to stabilize hormone levels and prevent adrenal crises. A 2025 update from the UK Medicines and Healthcare products Regulatory Agency (MHRA) also reaffirmed the importance of optimized hydrocortisone dosing for adrenal insufficiency and CAH management. This regulatory guidance highlights the continued reliance on glucocorticoid therapy in endocrine care worldwide.

Steroidogenesis inhibitors are projected to be the fastest-growing drug class, expanding at an estimated CAGR of around 7.4% during 2026–2033. These therapies regulate adrenal hormone production by targeting enzymes involved in steroid synthesis, helping control androgen overproduction associated with CAH. Pharmaceutical research increasingly focuses on enzyme-targeted treatments that can improve hormonal balance while reducing dependence on high-dose glucocorticoids. In 2025, clinical research published in the Journal of Clinical Endocrinology & Metabolism reported continued evaluation of enzyme-targeted therapies designed to regulate adrenal steroid production in CAH patients, highlighting their potential to improve biochemical hormone control. As clinical evidence expands and regulatory approvals progress, steroidogenesis inhibitors are expected to become an important complementary treatment option in endocrine care.

Route of Administration Insights

Oral administration is likely to dominate with an estimated 60% of the adrenogenital syndrome treatment market share in 2026. This leadership position is primarily driven by convenience, accessibility, and well-established clinical protocols for hormone replacement therapy. Most glucocorticoids and mineralocorticoids used in CAH treatment are available in oral formulations, allowing physicians to adjust dosing based on patient age, disease severity, and metabolic response. In 2025, the U.S. NIH reaffirmed oral hydrocortisone therapy as a standard treatment approach for adrenal insufficiency and CAH management, emphasizing individualized dosing strategies. The simplicity of oral dosing, combined with strong physician familiarity and outpatient suitability, continues to support its dominance in long-term endocrine therapy.

Long-acting administration methods are expected to be the fastest-growing segment, projected to expand at a CAGR of about 7.1% through 2033. These delivery systems provide sustained hormone release, helping maintain stable cortisol levels and reducing the need for frequent dosing. Long-acting therapies are particularly valuable for patients requiring lifelong hormone replacement, as they can significantly improve treatment adherence. In 2025, researchers at the University of Birmingham’s Institute of Metabolism and Systems Research reported ongoing development of modified-release steroid therapies designed to mimic natural cortisol cycles, demonstrating promising clinical potential. As endocrine drug delivery technologies advance and regulatory approvals increase, long-acting hormone therapies are expected to gain wider adoption in specialized endocrine treatment centers.

Regional Analysis

North America Adrenogenital Syndrome Treatment Market Trends

North America is expected to represent approximately 39% of the adrenogenital syndrome treatment market value in 2026, supported by highly developed healthcare systems, strong rare-disease research funding, and advanced endocrinology treatment centers. The United States drives most regional demand due to comprehensive newborn screening programs that allow early detection of congenital adrenal hyperplasia shortly after birth. Early diagnosis significantly improves treatment outcomes and increases long-term therapy adoption. In addition, specialized pediatric endocrine clinics and university medical centers actively participate in clinical research related to hormone replacement therapies and precision endocrine medicine. Canada further supports regional growth through publicly funded healthcare systems that provide access to endocrine disorder treatment and national metabolic screening programs.

Recent industry developments continue to reinforce North America's leadership in the CAH treatment landscape. In December 2025, Crinetics Pharmaceuticals initiated the Phase III CALM-CAH clinical trial evaluating atumelnant, a once-daily oral adrencorticotropic hormone receptor (ACTHR) antagonist designed to normalize adrenal androgen levels while reducing glucocorticoid exposure in patients with classic CAH. Additionally, new clinical evidence presented at the ENDO 2025 endocrine conference highlighted ongoing research focused on improving hormone control and reducing long-term glucocorticoid complications in CAH patients. These developments reflect the region’s strong pharmaceutical pipeline, continuous clinical innovation, and high level of investment in rare endocrine disease therapies.

Europe Adrenogenital Syndrome Treatment Market Trends

The Europe market is supported by universal healthcare coverage, strong rare-disease regulatory frameworks, and established endocrinology research networks. Countries including Germany, the United Kingdom, France, and Spain maintain advanced neonatal screening programs that enable early diagnosis and long-term clinical management of CAH. Regional healthcare systems provide extensive coverage for hormone replacement therapies, ensuring consistent treatment access for patients. Academic medical institutions across Europe also collaborate extensively with pharmaceutical developers to improve treatment protocols and evaluate new endocrine therapies. These collaborative research initiatives strengthen Europe’s role as a major hub for clinical development in rare hormonal disorders.

Several medical and research developments supported continued market growth across the region. A 2025 European clinical study evaluating modified-release hydrocortisone therapy demonstrated improved biochemical control of key CAH markers such as androstenedione and 17-hydroxyprogesterone, indicating improved disease management outcomes with advanced hormone formulations. Meanwhile, ongoing European endocrine research programs continue to investigate optimized steroid dosing strategies and circadian hormone replacement approaches to improve long-term patient outcomes. These clinical advancements, combined with strong regulatory support for orphan diseases and well-established specialist treatment centers, are expected to sustain Europe’s stable market expansion.

Asia Pacific Adrenogenital Syndrome Treatment Market Trends

Asia Pacific is projected to be the fastest-growing market for adrenogenital syndrome treatment with an estimated CAGR of around 6.7% during the 2026-2033 forecast period. Market growth in the region is primarily driven by expanding healthcare infrastructure, rising awareness of rare endocrine disorders, and improving access to diagnostic technologies. Countries such as China, Japan, India, and South Korea are investing heavily in pediatric healthcare systems and endocrine disease management programs. Increasing government initiatives aimed at improving newborn screening and genetic diagnostics are also contributing to earlier identification of congenital metabolic disorders, including CAH. As awareness grows, treatment adoption rates for hormone replacement therapies are gradually increasing across emerging Asian healthcare markets.

The region has also witnessed significant clinical and pharmaceutical developments during 2025–2026 that support market expansion. Clinical research programs across Asia have increasingly focused on evaluating newer endocrine therapies that aim to reduce long-term steroid exposure while maintaining hormonal balance in CAH patients. In addition, multinational pharmaceutical companies have continued expanding regional production and distribution networks for hormone replacement therapies, improving medication accessibility and reducing treatment costs in developing healthcare systems. Expanding endocrine research collaborations between Asian medical universities and global pharmaceutical developers are further accelerating innovation. These advancements position Asia Pacific as the fastest-growing regional market, driven by improved diagnosis rates, expanding healthcare access, and increasing rare-disease treatment investments.

Competitive Landscape

The global adrenogenital syndrome treatment market is moderately concentrated, with a small number of pharmaceutical companies accounting for a significant portion of the market. Key players such as Novo Nordisk, Neurocrine Biosciences, Spruce Biosciences, and Crinetics Pharmaceuticals are actively involved in developing advanced therapies for CAH. These companies focus on innovative hormone replacement treatments, modified-release glucocorticoids, and non-steroidal therapies to improve hormonal balance and reduce long-term steroid complications. Continuous investment in clinical trials and rare-disease drug development supports their competitive positioning.

Emerging biotechnology firms and specialized endocrine therapy developers are entering the market with targeted treatment approaches. Companies are increasingly researching ACTHR antagonists and precision endocrine therapies aimed at improving treatment outcomes. Strategic collaborations between pharmaceutical companies, academic research institutions, and pediatric endocrinology centers are also accelerating innovation. While strict regulatory requirements and high R&D costs limit new entrants, ongoing clinical advancements and partnerships are expected to gradually increase competition in the market.

Key Industry Developments

- In January 2026, Crinetics Pharmaceuticals raised US$ 350 million through a public stock offering to support commercialization and accelerate development of its endocrine therapy pipeline. The funding will help advance innovative treatments targeting congenital adrenal hyperplasia.

- In September 2025, Renata PLC launched Fludrocortisone 0.1 mg tablets in the U.K., targeting Addison’s disease and salt-losing adrenogenital syndrome, with supply from its MHRA-approved facility. The product offers a competitive advantage by remaining stable below 25°C, eliminating refrigeration needs and improving storage and distribution efficiency.

- In June 2025, Lundbeck received Orphan Drug Designation from the U.S. FDA and the European Medicines Agency (EMA) for Lu AG13909, an investigational anti-ACTH monoclonal antibody for congenital adrenal hyperplasia. The therapy is currently being evaluated in a Phase I/II clinical trial to improve treatment outcomes for CAH patients.

Companies Covered in Adrenogenital Syndrome Treatment Market

- Pfizer Inc.

- Merck & Co., Inc.

- Novartis AG

- F. Hoffmann-La Roche Ltd.

- Recordati Rare Diseases

- Neurocrine Biosciences

- Sanofi S.A.

- Bayer AG

- Takeda Pharmaceutical Company

- AbbVie Inc.

- Endo International plc

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

- Ipsen S.A.

- Crinetics Pharmaceuticals

Frequently Asked Questions

The global adrenogenital syndrome treatment market is projected to reach approximately US$ 14.3 billion in 2026.

Increasing newborn screening programs, rising awareness of rare endocrine disorders, and growing investment in rare disease drug development are key market drivers.

The market is poised to witness a CAGR of 5.6% from 2026 to 2033.

Development of non-steroidal therapies, improved hormone replacement formulations, and expanding rare disease research initiatives present major growth opportunities.

Key companies operating in the market include Novo Nordisk, Neurocrine Biosciences, Spruce Biosciences, and Crinetics Pharmaceuticals.