- Pharmaceuticals

- Acne Treatment Market

Acne Treatment Market Size, Share, and Growth Forecast 2026 - 2033

Acne Treatment Market by Product (Therapeutic Treatment, Devices), Route of Administration (Topical, Oral), Acne Type (Inflammatory Acne, Non-Inflammatory Acne), End-user (Hospitals, Specialty Clinics, Retail Pharmacies, Drug Stores, Online Pharmacies), Regional Analysis, 2026 - 2033

Acne Treatment Market Size and Trend Analysis

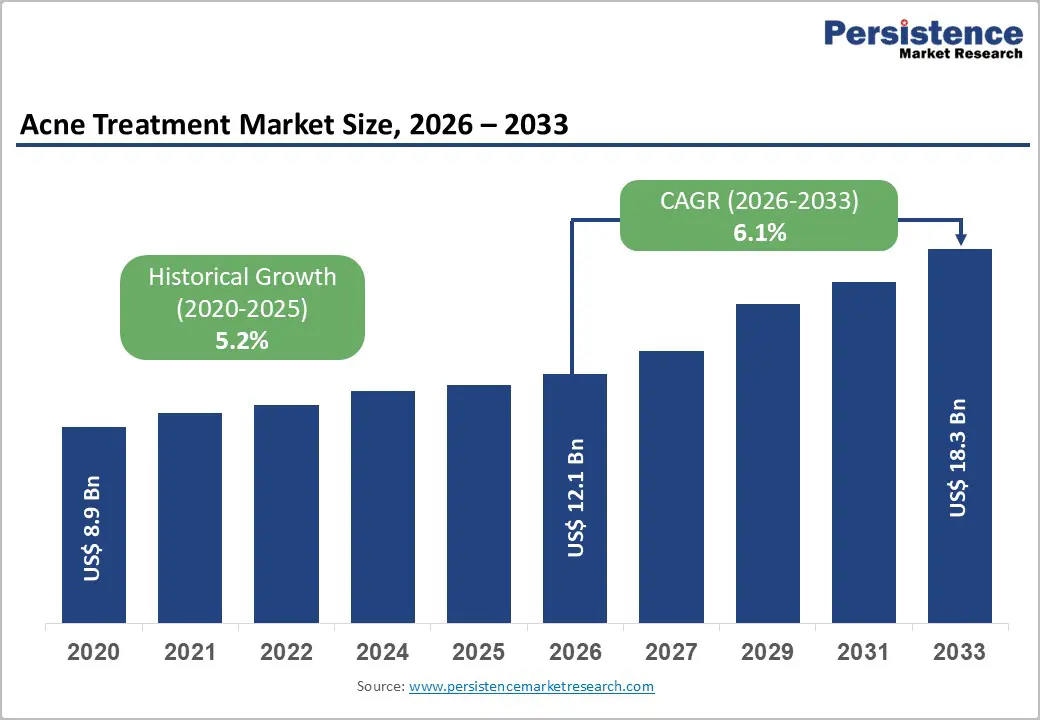

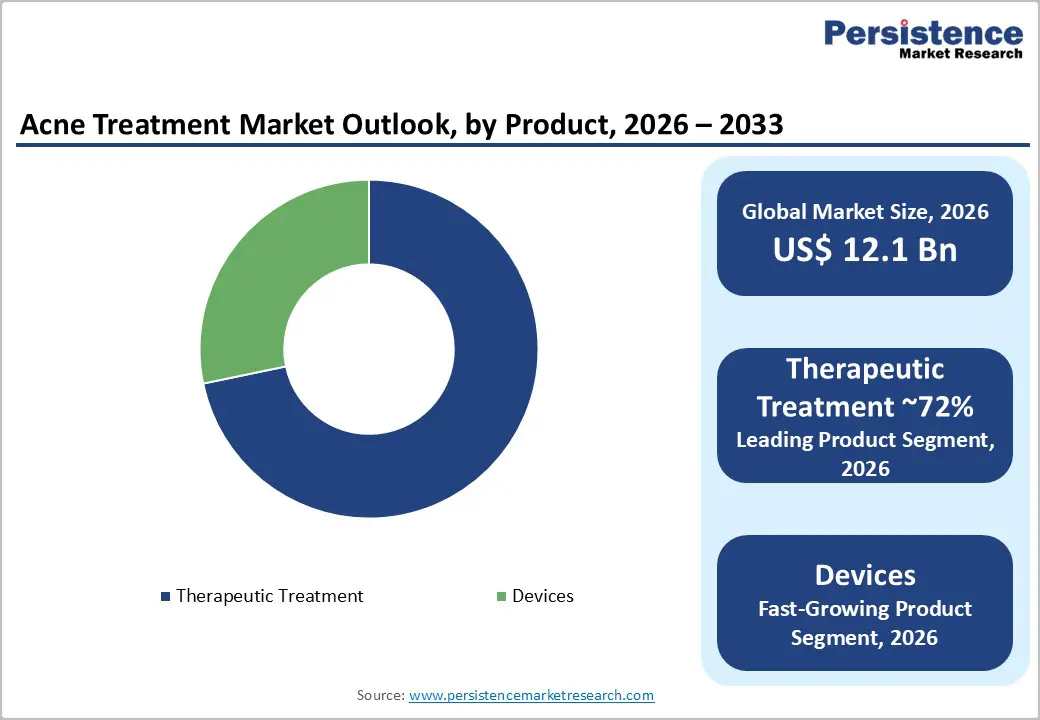

The global acne treatment market size is expected to be valued at US$ 12.1 billion in 2026 and projected to reach US$ 18.3 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033. It is experiencing a strong growth driven by the high global prevalence of acne vulgaris, the world’s most common skin disorder, affecting nearly 9.4% of the global population or around 650 million people. Rising skincare awareness, heavily influenced by social media and beauty-conscious consumers, is increasing demand for effective acne solutions across all age groups.

Growing recognition of adult-onset acne, especially among women, is further expanding the treatment market. Continuous pharmaceutical innovation, including advanced retinoid formulations, targeted biologics for inflammatory acne, and FDA-cleared energy-based laser and light devices, is supporting long-term market expansion. Additionally, improving access to dermatological care and expanding dermatology clinics across the Asia Pacific and Latin America are widening the patient pool and boosting treatment adoption globally.

Key Industry Highlights:

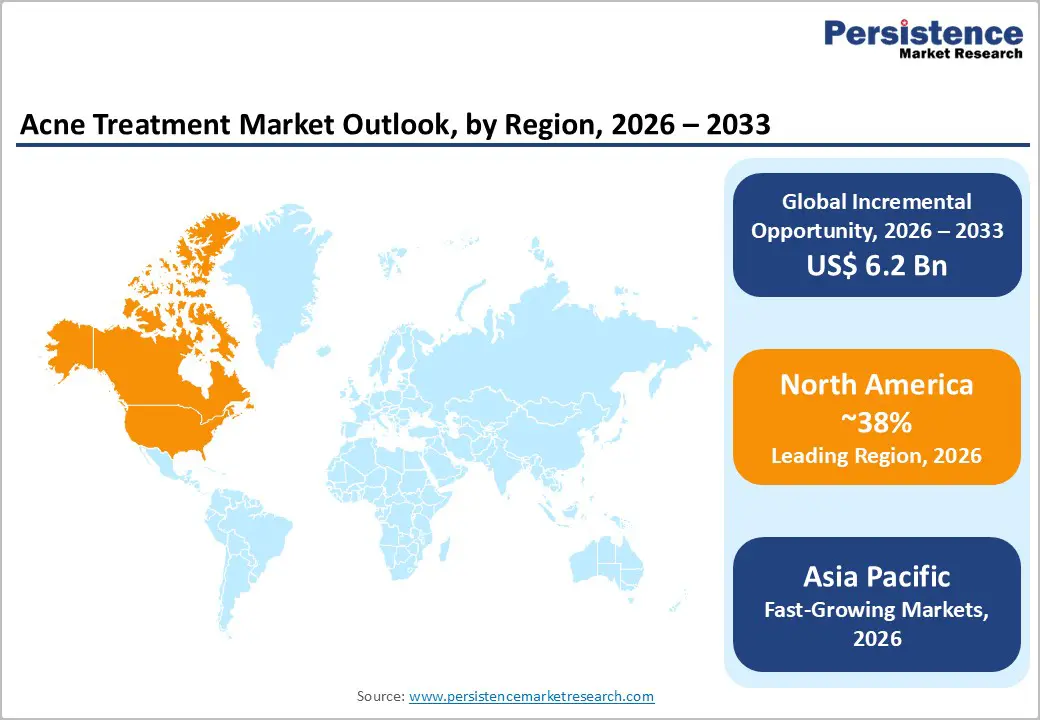

- Leading Region: North America leads the global Acne Treatment market with ~38% revenue share in 2025, underpinned by 50 million+ annual U.S. acne patients (AADA), strong prescription reimbursement, and active FDA approval pipeline for novel retinoids and energy-based devices.

- Fast-Growing Market: Asia Pacific is the fast-growing acne treatment market, driven by China's massive adolescent population, K-beauty-fueled skincare investment, India's young demographic structure, and rapidly expanding dermatology clinic networks across the region.

- Dominant Product Category: Therapeutic Treatment leads the product category with ~72% market share in 2025, anchored by AADA guideline endorsement of topical retinoids as first-line acne therapy and high-volume OTC and prescription sales of adapalene, benzoyl peroxide, and oral antibiotic products globally.

- Fastest Growing Treatment: Devices are the fast-growing acne treatment category, fueled by expanding adoption of FDA-cleared laser and radiofrequency platforms including Cutera's AviClear and Lumenis STELLAR M22 in specialty dermatology clinics globally.

- Key Opportunity: Biologics and novel targeted therapies for inflammatory acne represent the highest-value pipeline opportunity, with Galderma's nemolizumab FDA Breakthrough Therapy designation and multiple anti-IL-17 candidates in Phase 3 trials potentially redefining moderate-to-severe acne treatment through 2033.

Market Dynamics

Drivers - High Global Acne Prevalence and Growing Adult Acne Recognition

Acne vulgaris is the most prevalent dermatological condition globally, and its expanding recognition beyond adolescence is a structural demand driver for the acne treatment market. Historically perceived as a teenage condition, adult acne particularly in women has become a clinically significant and commercially important indication. A study published in the British Journal of Dermatology found that 54% of women over the age of 25 experience some degree of facial acne.

The American Academy of Dermatology Association (AADA) estimates that acne affects more than 50 million Americans annually, making it the most common skin condition in the country. This large, persistent, and cross-demographic patient population spanning adolescents, adults, and post-menopausal women creates diversified demand for topical, oral, and device-based acne treatments across all market segments and distribution channels.

Social Media-Driven Skincare Awareness and Demand for Visible Treatment Outcomes

The rapid growth of social media platforms and the global expansion of the skincare and beauty industry have materially elevated consumer awareness of acne treatments and the expectation of clear, blemish-free skin. Instagram, TikTok, and YouTube have created mass-market awareness of dermatological treatments, including prescription-strength retinoids, blue light therapy, and chemical peels, driving patients to proactively seek dermatologist consultations and OTC treatment products.

The International Society of Dermatology reports a measurable increase in dermatology consultation rates among young adults in high smartphone penetration markets. This digital health literacy trend is particularly pronounced in Asia Pacific, where K-beauty and skincare culture have elevated consumer investment in both prescription and non-prescription acne therapies, expanding the total addressable market significantly.

Restraints - Antibiotic Resistance and Regulatory Restrictions on Long-Term Antibiotic Acne Therapy

The global crisis of antimicrobial resistance (AMR) is directly constraining the long-term use of oral and topical antibiotics, including tetracycline, doxycycline, and erythromycin, which represent a major component of current acne pharmacotherapy.

The World Health Organization (WHO) has designated AMR as one of the top 10 global public health threats, and dermatology professional bodies, including the Global Alliance to Improve Outcomes in Acne (GAIA) now recommend limiting antibiotic courses to 3 months. These restrictions shift prescribing toward combination therapies and non-antibiotic agents, creating formulary disruption and revenue uncertainty for manufacturers of antibiotic-dominant acne portfolios.

Opportunities - Energy-Based Devices: Fastest Growing Segment with Premium Dermatology Clinic Adoption

The devices segment encompassing laser devices, radiofrequency platforms, and photodynamic therapy systems is the fastest growing category in the acne treatment market, driven by growing patient demand for non-pharmacological, non-antibiotic treatment modalities that deliver visible, long-lasting results. FDA-cleared platforms including Lumenis' STELLAR M22, Cutera's enlighten, and Candela Medical's GentleMax Pro are demonstrating strong clinical efficacy for inflammatory acne, acne scarring, and sebaceous gland reduction.

The American Society for Dermatologic Surgery (ASDS) reports that laser and light-based procedures for acne and acne scarring represent one of the fastest growing procedure categories among U.S. board-certified dermatologists. As procedure costs decline and combination protocols become standardized, the devices segment will capture an increasing share from pharmacological-only treatment pathways, particularly within high-value specialty dermatology clinic settings.

Category-wise Analysis

Product Insights

The Therapeutic Treatment segment leads the Acne Treatment market, accounting for ~72% of total product revenue in 2025. This dominance reflects the foundational role of pharmacological treatment, including topical retinoids, benzoyl peroxide, oral antibiotics, hormonal agents, and isotretinoin as the first-line standard of care for acne vulgaris across all severity levels. American Academy of Dermatology Association (AADA) clinical guidelines recommend topical retinoids as the cornerstone of acne pharmacotherapy, with oral treatments added for moderate-to-severe presentations.

The broad availability of generic formulations of key molecules, including adapalene % gel (Differin, Galderma) as OTC in the U.S., drives high prescription and purchase volumes. Branded treatments from Galderma, Bausch Health, Almirall, and Johnson & Johnson command premium pricing in the therapeutic segment, ensuring sustained revenue leadership through the forecast period.

Acne Type Insights

The inflammatory acne segment leads the market, likely to represent ~58% of acne type-based revenue in 2026. Inflammatory acne encompassing papules, pustules, nodules, and cystic lesions is the clinically and commercially dominant indication because it requires active pharmacological or device-based intervention, commands prescription-grade treatment protocols, and is the primary driver of dermatology consultations.

The Global Acne Grading System, widely adopted across clinical practice and FDA clinical trial endpoints, classifies most of the clinically managed acne as predominantly inflammatory, directing significant product volume. Inflammatory acne's association with acne scarring also creates a downstream demand pathway for procedural and device-based interventions, expanding per-patient lifetime treatment revenue and reinforcing this segment's leadership position throughout the forecast period.

End-user Insights

The retail pharmacies segment leads the acne treatment market by end user, likely to represent ~38% of end-user revenue in 2026. Retail pharmacies serve as the primary dispensing and purchase channel for both OTC and prescription acne treatments, including the high-volume topical segment of benzoyl peroxide washes, adapalene gels, and salicylic acid formulations available without prescription across major markets.

The OTC reclassification of Differin (adapalene 0.1%) by Galderma in the U.S. in 2016 significantly shifted volume from specialty clinics to retail pharmacy channels, establishing a large recurring consumer purchase base. Chain pharmacies including CVS, Walgreens, Boots, and dm-drogerie markt (Germany) maintain dedicated skincare sections with strong acne treatment SKU breadth, sustaining retail pharmacy's dominant end-user position.

Regional Insights

North America Acne Treatment Market Trends and Insights

North America leads the global market with ~38% of total revenue in 2025. The region benefits from the highest per-capita dermatology access globally, comprehensive insurance coverage for prescription acne medications under Medicare Part D and commercial plans, strong OTC retail pharmacy infrastructure, and active FDA approval pipelines advancing novel retinoids and energy-based devices. Social media-driven skincare awareness continues to drive dermatology consultation volumes among young adults.

U.S. Acne Treatment Market Size

The U.S. accounts for ~88% of North America's acne treatment revenue. With over 50 million Americans affected annually (AADA), the U.S. has the world's largest single-country acne treatment market. FDA approvals for novel agents including Winlevi (clascoterone) and OTC accessibility of adapalene gel sustain robust retail and prescription demand across specialty clinic and pharmacy channels.

Europe Acne Treatment Market Trends and Insights

Europe is the second-largest acne treatment market, supported by established dermatology reimbursement systems under GKV (Germany), NHS (UK), and national health insurance in France and Italy. The European Dermatology Forum (EDF) guidelines align with international standards, supporting systematic topical retinoid and combination antibiotic prescribing. Growing awareness of adult female acne is expanding the treatment-seeking population across Western Europe, supported by increasing dermatology telehealth consultations.

Germany Acne Treatment Market Size

Germany accounts for ~21% of European acne treatment revenue. The GKV reimburses prescription-grade topical retinoids and oral antibiotics for moderate-to-severe acne, and Germany's robust dermatology specialist network supports high prescription volumes. Galderma, Almirall, and Stiefel (GSK) maintain strong branded market positions alongside expanding generic competition.

UK Acne Treatment Market Size

The UK represents ~17% of European acne treatment revenue. NICE guidance (CG184) standardizes acne management within the NHS, directing prescribing toward topical combination products and discouraging long-term antibiotic monotherapy in alignment with WHO AMR guidelines. Growing NHS dermatology waiting times are driving patients toward private aesthetic clinic and OTC retail pharmacy channels for acne management.

France Acne Treatment Market Size

France contributes ~15% of European acne treatment revenue. Assurance Maladie reimburses prescription retinoids and oral isotretinoin for severe acne, and French dermatology practice follows EDF and ANSM guidelines. France is a strong market for Galderma, headquartered in Lausanne with major French commercial operations, which maintains a significant branded topical and oral acne product share.

Asia Pacific Acne Treatment Market Trends and Insights

Asia Pacific is the fast-growing acne treatment market and is expected to register the highest CAGR during 2026 - 2033. China is the dominant national market, driven by a massive adolescent and young adult population, rapidly expanding dermatology clinic networks in tier-1 and tier-2 cities, and a growing middle class investing in skincare supported by China's Healthy China 2030 initiative's emphasis on skin health. K-beauty and J-beauty cultural influences are elevating treatment demand across South Korea, Japan, and Southeast Asia.

India Acne Treatment Market Size

India accounts for ~13% of Asia Pacific's acne treatment revenue. India's young demographic structure with over 50% of the population under age 30 (Census of India) creates a structurally large adolescent and young adult acne patient population. Domestic manufacturers and international brands including Galderma, Almirall, and Bausch Health are expanding affordable topical retinoid and antibiotic offerings through India's extensive retail pharmacy network.

Japan Acne Treatment Market Size

Japan represents ~19% of Asia Pacific's acne treatment market. PMDA-approved prescription treatments including topical adapalene (Differin, Galderma Japan) and oral antibiotics are widely prescribed through Japan's dermatology clinic network. Japan's premium skincare culture drives high per-capita spending on both prescription and cosmetic acne management products across pharmacy and aesthetic clinic channels.

Competitive Landscape

The global Acne Treatment market is moderately consolidated in the pharmaceutical segment, with Galderma S.A. holding the largest single-company revenue share through its broad acne portfolio including Epiduo, Differin, Benzac, and Oracea. Almirall, Bausch Health, Johnson & Johnson, and Teva Pharmaceutical compete strongly across branded and generic topical and oral segments.

The devices sub-market is more fragmented, with Lumenis, Cutera, Alma Lasers, Candela Medical, and Sisram Medical competing on platform efficacy, clearance breadth, and clinic economics. A key competitive trend is the convergence of pharma-aesthetics, with pharmaceutical companies acquiring or partnering with device manufacturers to offer integrated acne treatment platforms.

Key Developments:

- In January 2026, Almirall, S.A. announced China NMPA approval for Seysara® (sarecycline hydrochloride), the first oral antibiotic specifically developed for moderate-to-severe inflammatory acne vulgaris treatment.

- In November 2025, Cosmo Pharmaceuticals and Glenmark Pharmaceuticals received European Commission marketing authorization for Winlevi® (clascoterone 10 mg/g cream) following a positive CHMP opinion.

- In April 2024, Allergan Aesthetics launched SkinMedica® Acne Clarifying Treatment and Pore Purifying Gel Cleanser, expanding its acne-care portfolio with a complete skincare protocol for acne-prone patients.

Companies Covered in Acne Treatment Market

- Galderma S.A.

- Lumenis Ltd

- Alma Lasers, Sisram Medical Company

- Cutera Inc.

- Almirall, S.A

- Johnson & Johnson Services Inc.

- Bausch Health Companies Inc.

- Teva Pharmaceutical Industries Ltd.

- Stiefel Laboratories, a GSK Company

- Candela Medical

Frequently Asked Questions

The global acne treatment market is estimated to be valued at US$ 12.1 billion in 2026.

Key drivers include rising global acne prevalence, increasing adult acne cases, social media-driven dermatology visits, and innovation in retinoids, biologics, lasers, and radiofrequency devices.

North America leads with around 38% market share, driven by high acne prevalence, strong dermatology access, FDA approvals, OTC availability, and insurance reimbursement support.

Major opportunities include fast-growing energy-based devices like laser therapies and emerging biologics, with targeted treatments creating new growth potential in inflammatory acne management.

Leading players include Galderma, Almirall, Bausch Health, Johnson & Johnson, Teva, Lumenis, Cutera, Alma Lasers, Candela Medical, and Sisram Medical.