- Technology

- 4D Printing Market

4D Printing Market Size, Share, and Growth Forecast 2026 - 2033

4D Printing Market by Material Type (Programmable Carbon Fiber, Programmable Textiles, Programmable Wood), Printing Technology (Fused Deposition Modeling (FDM), Stereolithography (SLA), Direct Ink Writing/PolyJet, Powder Bed / Inkjet, Others), Application (Self-Assembly Structures, Adaptive Components, Smart Textiles, Medical Implants & Devices, Others), End-user, and Regional Analysis, 2026 - 2033

4D Printing Market Size and Trend Analysis

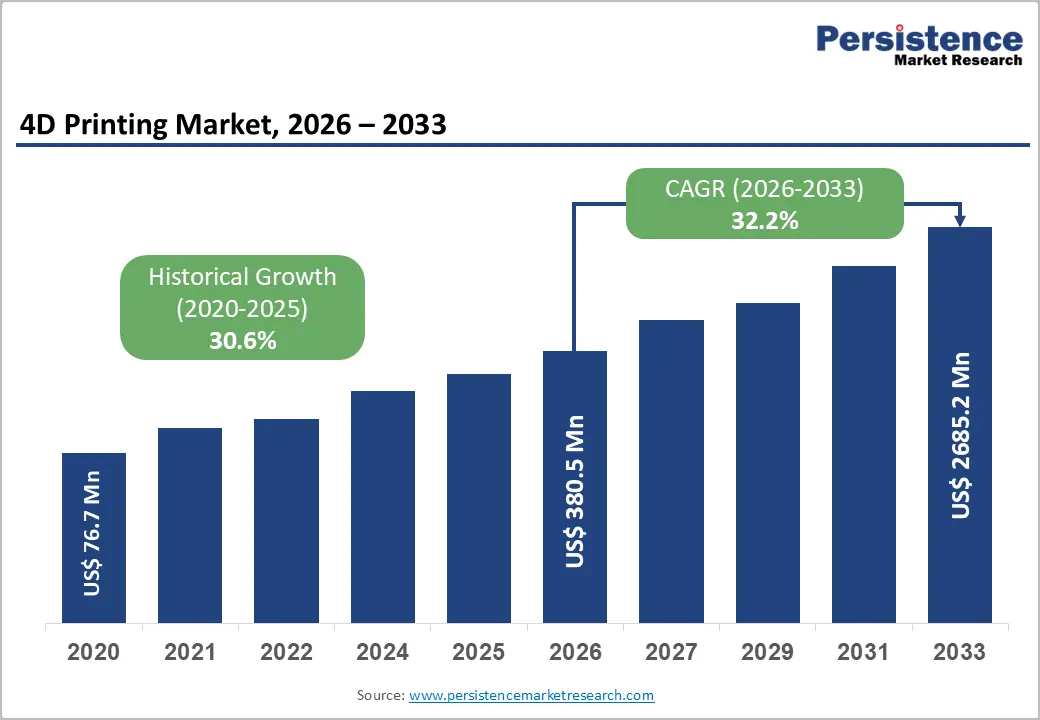

The global 4D printing market size is expected to be valued at US$ 380.50 million in 2026 and is projected to reach US$ 2685.19 million by 2033, growing at a CAGR of 32.2% between 2026 and 2033.

Advances in smart materials science, digital fabrication, and stimuli-responsive systems collectively redefines the techniques involved in the printing outcomes.

Key Industry Highlights:

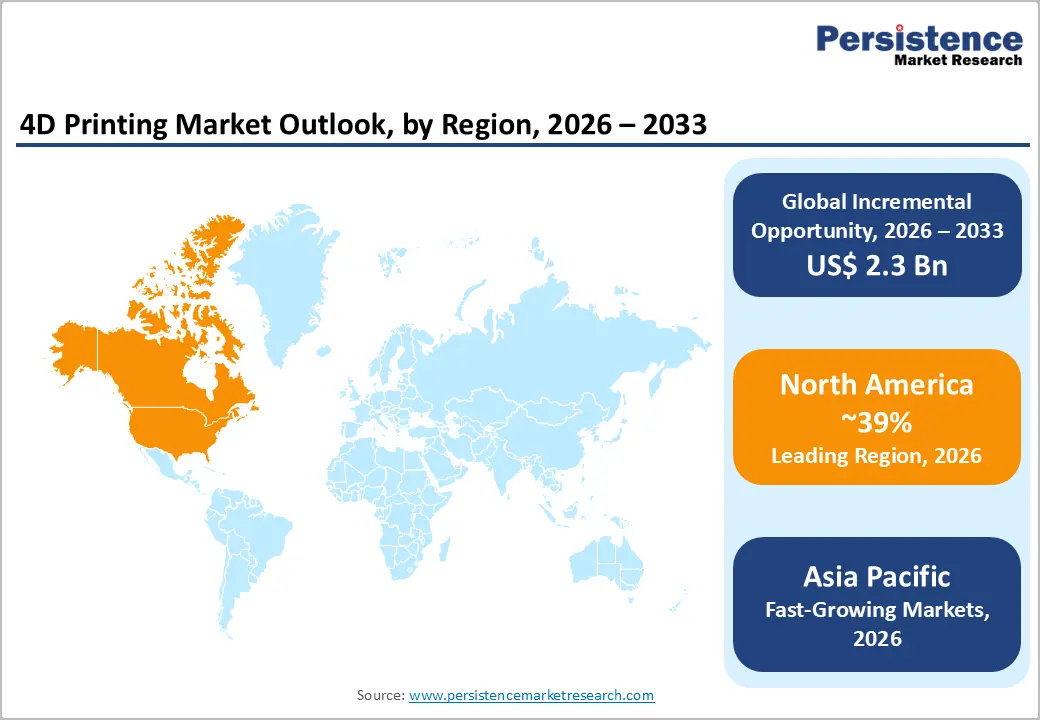

- Leading Region: North America is poised to lead the 4D printing market with a 39.0% share in 2026, underpinned by the world's largest defense R&D budget, a mature aerospace manufacturing base, and an innovation ecosystem that translates university-level smart materials research into commercially deployed programmable matter solutions.

- Fast-Growing Market: Asia Pacific is the fast-growing market projected to reach a CAGR of 35.8%, driven by China's state-directed advanced manufacturing programs, Japan's precision engineering heritage in adaptive materials, and India's defense indigenization drive.

- Leading End-user: Military & defense are dominant end-users with a 41.0% share, justified by defense agencies' unique willingness to pay performance premiums for self-assembly structures and adaptive components that reduce field logistical complexity, a value proposition unmatched in any civilian application at a comparable scale.

- Fastest Growing End-users: The automotive industry is the fast-growing end-user in the 4D printing market, propelled by OEM demand for morphing aerodynamic surfaces, lightweight adaptive components, and thermal management solutions in EV platforms, use cases where time-dependent transformation and stimuli-responsive systems deliver measurable efficiency and performance gains over static alternatives.

- Key Opportunity: The commercialisation of 4D bio-printing for medical implants represents the most actionable near-term opportunity for market participants with regulatory expertise and clinical partnerships, given that an ageing global population, increasing elective surgery volumes, and declining smart material costs converge precisely within the forecast period.

Market Dynamics

Drivers - Rising Adoption of Smart Materials and Shape-Memory Polymers Across Critical End-Uses

The rapid commercial maturation of shape-memory polymers, hydrogels, and adaptive materials capable of executing time-dependent transformation in response to environmental stimuli. Defense agencies across NATO member states have accelerated procurement of self-assembly structures and adaptive components for field-deployable equipment, since these materials eliminate manual reconfiguration under hostile conditions.

Aerospace primes, including those supplying next-generation satellite and UAV platforms, increasingly specify stimuli-responsive systems to reduce mechanical complexity and part count. Industry data indicates that programmable carbon fiber composites now achieve tensile strengths exceeding those of many conventional aerospace-grade alloys at comparable weight, making the performance case for 4D printing compelling across the product engineering cycle.

Expanding Government R&D Investment and Strategic Defense Modernization Programs

A substantial and growing pipeline of government-sponsored research funding directed at advanced manufacturing technologies. The U.S. Department of Defense has allocated multi-year budgets toward bio-inspired adaptive manufacturing as part of broader modernisation initiatives, and analogous programs exist in China, Germany, and the United Kingdom.

Academic-to-industry technology transfer is accelerating: flagship programs at institutions such as MIT's Self-Assembly Lab have produced commercially licensable processes that compress the gap between laboratory proof-of-concept and production-ready digital fabrication.

Restraints - High Material and Process Costs Limiting Broad Commercial Penetration

The primary structural restraint on the 4D printing market is the premium cost associated with engineered smart materials relative to conventional thermoplastics and composites used in standard additive manufacturing. Shape-memory polymers and programmable carbon fiber feedstocks command prices that can be three to five times higher per kilogram than standard FDM filament, restricting adoption primarily to high-value defense, aerospace, and medical applications where per-unit cost sensitivity is lower.

This cost differential directly constrains the addressable market in price-sensitive sectors such as consumer goods and commodity industrial manufacturing. Until economies of scale in smart material synthesis reduce feedstock costs substantially, the 4D printing industry will struggle to penetrate mid-market manufacturing segments at the pace its technology roadmap would otherwise support.

Regulatory Uncertainty and Standardization Gaps in Biomedical and Structural Applications

Regulatory frameworks governing time-dependent, stimuli-responsive components, particularly medical implants produced via bio-printing innovations, remain fragmented across major markets, creating meaningful commercial uncertainty for manufacturers seeking global distribution.

The U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have yet to issue dedicated guidance covering 4D-printed implantable devices; each product typically navigates regulatory review as a novel device requiring de novo classification. This process can extend market entry timelines by two to four years, materially increasing development costs and deterring smaller innovators from committing resources. Without harmonised international standards, the medical implants and devices application segment, one of the highest-value opportunity pockets in the 4D printing space, will remain structurally underserved relative to its technical potential.

Opportunities - Commercialisation of 4D Bio-Printing for Next-Generation Medical Implants

The intersection of bio-printing innovations and 4D printing technology represents one of the most actionable commercial opportunities in the global 4D printing market in the forecast period. Adaptive implants that change shape or stiffness post-implantation in response to physiological stimuli, such as temperature or pH, can dramatically improve patient outcomes in orthopaedics, cardiovascular surgery, and drug delivery, addressing a clinical unmet need that conventional implants cannot meet.

The existing regulatory relationships, biocompatible material libraries, and clinical trial infrastructure are best positioned to capture this opportunity early. Analysts recommend that companies prioritise partnerships with academic medical centres to build the clinical evidence base needed to accelerate regulatory clearance. The convergence of an ageing global population, rising surgical procedure volumes, and declining 4D material costs makes this opportunity increasingly time-sensitive across the 2026 to 2033 forecast window.

Integration of Nanotechnology with 4D Printing for Aerospace and Defense Applications

Nanotechnology integration with programmable matter fabrication opens a high-value frontier that strategically positions the 4D printing industry at the centre of next-generation aerospace and defense supply chains. Nano-reinforced shape-memory composites deliver actuation precision and structural performance at scales impossible with macro-scale smart materials alone, enabling applications from morphing aircraft skins to self-healing structural panels.

Companies that invest now in nano-composite material development and process control capabilities will establish defensible intellectual property moats before the technology reaches peak adoption. Analysts advise incumbents to pursue joint development agreements with nanotechnology specialists and university research programs, which represent cost-effective paths to capability without requiring full vertical integration. With defense modernisation spending across North America and the Asia Pacific sustaining high single-digit annual growth rates, the demand signal for nanotechnology-enhanced 4D-printed components is both durable and near-term.

Category-wise Analysis

Material Type Insights

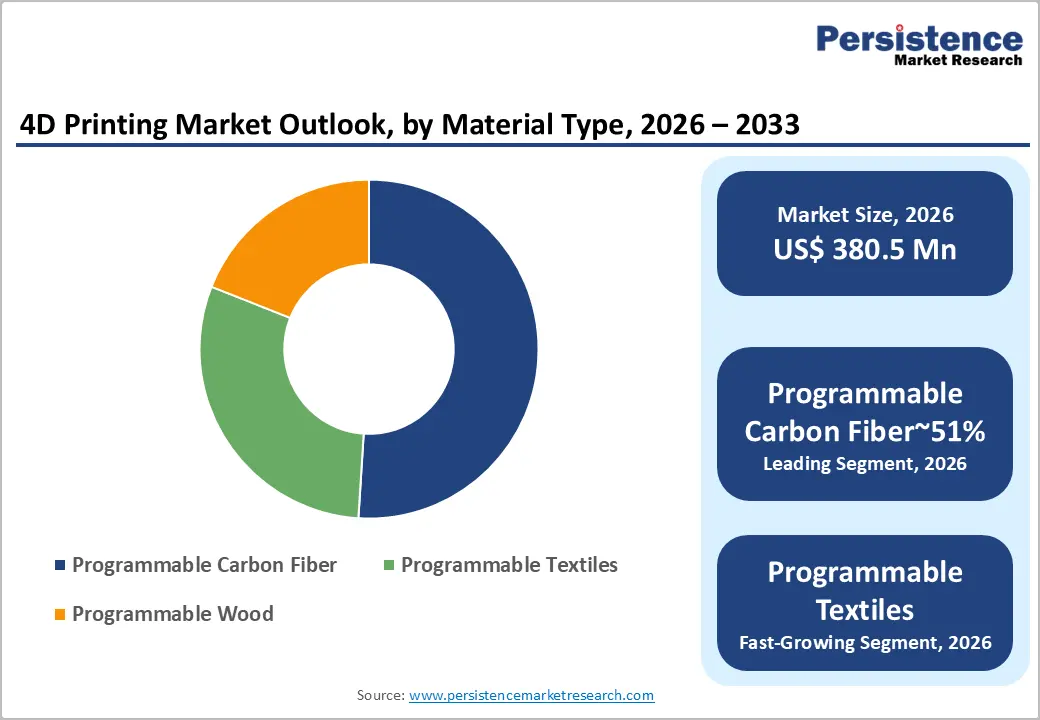

Programmable carbon fiber is likely to account for 51% of the global 4D printing market in 2026, valued at US$ 194.06 million, making it the clear leader in the material segment. This strong position comes from its excellent mechanical strength, lightweight nature, and compatibility with both thermoset and thermoplastic systems, which allow reliable shape transformation under thermal conditions. These properties align well with strict aerospace and defense requirements. Industry data shows that programmable carbon fiber composites used in morphing structures can achieve over 95% strain recovery across repeated cycles, a level of performance that competing smart materials struggle to match at scale.

Programmable textilesare the fast-growing segment, driven by rising demand for smart fabrics in military wearables and performance apparel. Although carbon fiber will remain dominant in the near term due to high qualification barriers, rapid growth in textiles will gradually narrow the gap over time.

Printing Technology Insights

Fused deposition modeling (FDM) is likely to accounts for 36% of the global 4D printing market in 2026, reaching US$ 136.98 million and maintaining its leadership among printing technologies. Its dominance is driven by ease of use, cost-effectiveness, and compatibility with a wide range of thermoplastic smart materials, including shape-memory polymers. This makes FDM suitable for both industrial production and research-based applications without requiring heavy capital investment.

The large installed base of FDM systems worldwide provides a strong infrastructure advantage that newer technologies cannot easily match. At the same time, Direct Ink Writing (DIW) and PolyJet technologies are the fastest growing segments, thanks to their ability to print multiple materials with high precision below 100 micrometers. While FDM will remain widely used, increasing demand for high-precision applications is expected to push manufacturers toward adopting hybrid technology strategies in the coming years.

Application Insights

Self-Assembly structures represent 32% of the global 4D printing market in 2026, valued at US$ 121.76 million, making them the leading application segment. Their leadership is driven by their ability to deliver the core benefit of 4D printing, objects that can assemble or change shape on their own after production. This is especially valuable for aerospace, defense, and infrastructure sectors where reducing assembly time and operational complexity is critical.

Research has shown that such structures can fully transform in under 60 seconds when exposed to specific stimuli, proving their commercial potential. Smart Textiles are the fastest growing application segment, supported by increasing demand from wearable technology companies, apparel brands, and military users. While self-assembly structures will remain dominant due to long-term contracts and projects, the rapid growth of smart textiles will gradually reshape the application landscape over the next decade.

End-user Insights

Military & defense accounts for 41% of the global 4D printing market in 2026, reaching US$ 156.00 million and leading all end-use segments. This dominance is driven by the need for lightweight, adaptable, and easily deployable equipment that reduces logistics and improves operational efficiency. Defense organizations are increasingly investing in advanced manufacturing technologies, including programmable materials, as part of modernization efforts.

Automotive is the fast-growing end-user segment, supported by the industry's focus on lightweighting, improved aerodynamics, and advanced thermal management in electric vehicles. These applications benefit significantly from materials that can adapt over time. While defense will continue to dominate due to long-term contracts and high entry barriers, the rapid growth of automotive applications reflects a broader shift toward innovative manufacturing solutions in commercial industries, which will diversify market demand in the coming years.

Regional Insights

North America 4D Printing Market Trends and Insights

North America holds 39.0% of the global 4D printing market in 2026, leading due to strong defense R&D, advanced manufacturing networks, and venture capital support. Agencies such as the FDA and DARPA accelerate adoption. The region will retain leadership through 2033, driven by defense modernization and programmable materials demand.

- United States 4D Printing Market Size

The United States accounts for 85% of North America’s market, supported by defense contractors, aerospace firms, and research institutions. Growth is driven by Department of Defense programs and aerospace innovation. Continued federal investment will strengthen leadership through 2033, especially in bio-printing and nanotechnology-enabled applications.

Europe 4D Printing Market Trends and Insights

Europe holds 25.0% of the global market, ranking second globally. Growth is supported by Horizon Europe funding and national strategies in Germany, France, and the UK. Strict regulatory frameworks enhance product quality. Expansion will continue through 2033, driven by automotive, aerospace, and medical applications.

- Germany 4D Printing Market Size

Germany captures 30% of Europe’s market, driven by its automotive sector and advanced manufacturing integration. Demand stems from adaptive automotive components and Industrie 4.0 initiatives. Growth will strengthen with EV development, increasing need for lightweight and thermally adaptive materials in batteries and drivetrain systems.

- United Kingdom 4D Printing Market Size

The UK holds 22% of Europe’s market, supported by aerospace and defense industries. Government initiatives like the Advanced Manufacturing Plan boost domestic capabilities. Growth will continue as aerospace applications for programmable materials and self-assembling structures transition from prototypes to large-scale production.

- France 4D Printing Market Size

France accounts for 18% of Europe’s market, driven by aerospace and defense demand via Airbus and DGA. The France 2030 plan supports advanced materials and bio-printing. Growth will be steady, with increasing adoption in medical implants and smart textiles as research transitions to commercialization.

Asia Pacific 4D Printing Market Trends and Insights

Asia Pacific holds 22.0% of the global market and is the fastest-growing region (CAGR 35.8%). Growth is driven by government initiatives, aerospace expansion, and cost-efficient manufacturing. China, Japan, and India lead demand. The region is expected to surpass Europe in market value by 2030.

- China 4D Printing Market Size

China represents 48% of Asia Pacific’s market, driven by state-backed programs like Made in China 2025. Aerospace and defense sectors dominate demand. Strong policy support, manufacturing scale, and improving research capabilities position China to become the largest national 4D printing market before 2033.

- Japan 4D Printing Market Size

Japan holds 28% of Asia Pacific’s market, supported by precision engineering and major industrial players. Growth is driven by automotive lightweighting and medical robotics. Strength in nanotechnology provides an advantage, enabling high-precision 4D printing applications and supporting steady expansion through 2033.

- India 4D Printing Market Size

India accounts for 14% of Asia Pacific’s market, driven by defense indigenization and aerospace manufacturing growth. Research from IISc and IITs is fostering innovation. The market will grow rapidly through 2033, supported by increasing defense procurement and rising demand for advanced manufacturing technologies.

Competitive Landscape

The 4D printing market presents a moderately fragmented competitive landscape in which a small cohort of established additive manufacturing majors, commanding broad technology portfolios and global distribution, compete alongside a larger population of specialist innovators with differentiated smart material or application-specific capabilities. Scale players leverage incumbent customer relationships, certified material libraries, and multi-platform software ecosystems as primary competitive moats.

Differentiation-focused competitors, including university-linked spinouts and material science specialists, compete on the basis of intellectual property in stimuli-responsive systems, nanotechnology integration, and bio-printing innovations. The dominant strategic themes shaping competitive positioning include vertical integration into smart material synthesis, cross-industry partnership formation to accelerate regulatory approval in medical applications, and investment in proprietary process control software that governs time-dependent transformation parameters. Business model innovation is also emerging, with subscription-based digital fabrication platforms and material-as-a-service offerings beginning to challenge the traditional capital equipment sales model.

Key Developments:

- January, 2025: Stratasys Ltd. announced an expanded collaboration with a leading aerospace prime to qualify programmable carbon fiber feedstocks for FDM-based 4D printing applications in structural airframe components, targeting regulatory certification under FAA Part 21 frameworks and expected to enter flight-test evaluation by mid-2026.

- March, 2025: Materialise NV launched a dedicated 4D printing software module within its Magics platform, enabling time-dependent transformation simulation and optimisation for medical implant design workflows, directly addressing the regulatory evidence gap that has slowed FDA de novo submissions for 4D-printed implantable devices.

- November, 2024: EOS GmbH completed a strategic acquisition of a European smart materials startup specialising in shape-memory polymer powder formulations for powder bed fusion processes, significantly expanding its addressable material portfolio and strengthening its competitive position in the medical and aerospace end-use segments of the global 4D printing market.

4D Printing Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 76.68 Million |

| Current Market Value (2026) | US$ 380.50 Million |

| Projected Market Value (2033) | US$ 2685.19 Million |

| CAGR (2026 - 2033) | 32.2% |

| Leading Region | North America (39%) |

| Dominant Material Type | Programmable Carbon Fiber (51.0%) |

| Top-ranking Printing Technology | Fused Deposition Modeling / FDM (36.0%) |

| Top-ranking Application | Self-Assembly Structures (32.0%) |

| Top-ranking End-user | Military & Defense (41.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 2,304.69 Million |

Companies Covered in 4D Printing Market

- Stratasys Ltd.

- 3D Systems Corporation

- Autodesk Inc.

- Materialise NV

- Hewlett-Packard (HP) Inc.

- Dassault Systèmes

- Organovo Holdings Inc.

- ExOne Company

- EOS GmbH

- EnvisionTEC GmbH

- Voxeljet AG

- Nanoscribe GmbH

- CT CoreTechnologie Group

- MIT Self-Assembly Lab

- Siemens AG

- Carbon, Inc.

- Desktop Metal, Inc.

- Renishaw plc

- SLM Solutions Group AG

- Optomec, Inc.

- Prodways Group

- nScrypt, Inc.

- Markforged Holding Corporation

- Arevo, Inc.

Frequently Asked Questions

The global 4D Printing Market is valued at US$ 380.50 million in 2026 and is projected to reach US$ 2,685.19 million by 2033, growing at a CAGR of 32.2%.

Growth is driven by advances in shape-memory materials and strong government R&D funding, enabling commercialization of adaptive components across aerospace, defense, and healthcare industries at scale.

Programmable Carbon Fiber leads with 51.0% share in 2026 due to superior strength, lightweight properties, and reliable performance, meeting strict aerospace and defense requirements and creating high entry barriers.

North America dominates with 39.0% share in 2026, supported by high defense spending, strong R&D ecosystem, and faster commercialization of advanced manufacturing technologies compared to other regions.

Key opportunity lies in 4D bioprinting for adaptive medical implants, driven by rising healthcare demand, aging population, and advancements in biocompatible materials and regulatory support frameworks globally.

The market includes companies like Stratasys, 3D Systems, Materialise, EOS, and Siemens, with moderate competition driven by innovation, proprietary materials, and application-specific expertise rather than pricing pressure.