Industry: Chemicals and Materials

Published Date: February-2025

Format: PPT*, PDF, EXCEL

Delivery Timelines: Contact Sales

Number of Pages: 182

Report ID: PMRREP34892

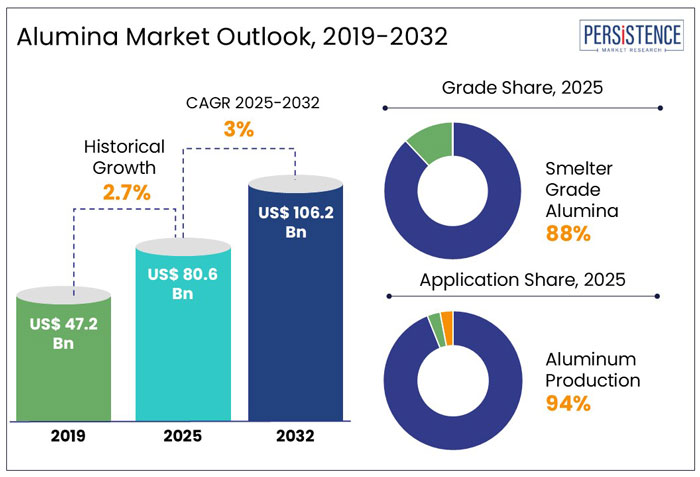

The global alumina market is likely to be valued at US$ 80 Bn in 2025 and is projected to jump to US$ 106 Bn by the end of 2032. The market is poised to witness remarkable revenue growth, and in the next seven years, it is projected to exhibit a stellar 1.3x expansion, maintaining a consistent CAGR of 3.0% between 2025 and 2032.

There is currently a lot of demand within the automotive industry for lightweight, high-performance materials and even weight efficiencies that can be considered necessary for improving fuel efficiencies, further augmenting battery ranges, especially in electric vehicles. This trend is expected to lead to burgeoning demand for advanced aluminum materials.

Aluminum parts are expected to replace iron and steel components in vehicles as early as the next ten years, greatly enhancing alumina demand. Various nations are thus directed towards improving their production capacities to meet this demand.

Key Industry Highlights

|

Global Market Attributes |

Key Insights |

|

Alumina Market Size (2025E) |

US$ 80 Bn |

|

Market Value Forecast (2032F) |

US$ 106 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.7% |

Driving Forces

Skyrocketing Demand for Aluminum from the Construction and Automotive Sector to Boost Sales of Smelter Grade Alumina

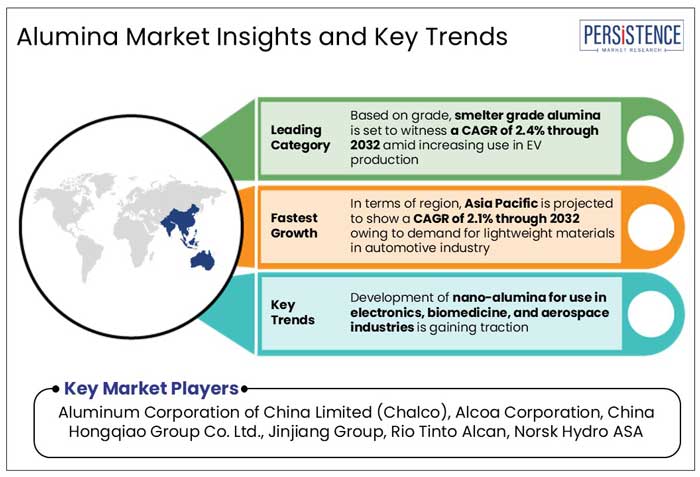

Alumina is widely classified into two primary grades, namely, Smelter Grade Alumina (SGA) and Chemical Grade Alumina (CGA). The smelter-grade alumina is produced only by calcination of aluminum hydroxide in refineries and is mainly accounted for in the market. In 2022, SGA constituted roughly 90% of total alumina demand and is anticipated to grow with a relatively strong Compound Annual Growth Rate (CAGR) of 2.8% from 2024 to 2031.

This grade of alumina is the one necessary to produce aluminum for derived value-added products such as flat, extruded, and forged. Aluminum as a construction material is critical for numerous industries, particularly automotive, aerospace, packaging, and consumer goods.

Fluctuating Price Levels are Poised to Have Big Knocks on Profitability Metrics

COVID-19 had a major influence on aluminum supply chains mainly through three attributes: factory shutdowns, port closures, and container ship shortages. Lockdowns were imposed worldwide to control the pandemic since early 2020, and it resulted in significant interruptions to overland transportation.

Recovery of alumina prices began in 2021 and reached levels equal to pre-pandemic by the beginning of 2022, even though some alumina-producing nations experienced restrictions due to movement and lockdowns. Such restraining energy costs in 2022 and continued supply disruptions from Australia kept the price of alumina high.

The average alumina price in 2023 surged to US$ 450 per ton, a substantial increase of about 35% from its value in 2020. Maintaining high alumina prices is dependent on energy cost concerns across the value chain posing a challenge in the future. This scenario creates an opportunity for market shareholders to look directly at solutions for improving market resilience and stability.

Asia Pacific Alumina Market

Increasing Investment across the Aluminum Value Chain (India and Indonesia Leading)

Investment in the aluminum value chain has grown enormously over the last few years.

For Southeast Asia, this comes as a huge window of opportunity, with aluminum and integrated investments. Southeast Asia is on the map mainly due to China executing overseas alumina projects to take advantage of bauxite deposits.

In bauxite processing, which is the essential raw material for aluminum smelters, Indonesia is making a good contribution and is seen to become the fastest-growing alumina market in the world in coming years. This is making it a key market where China is likely to implement its alumina projects.

The global alumina industry is dominated by China, closely followed by Australia- the duo that shapes the industry and infuses life into different global supply chains. In China, alumina production grew steadily owing to new project launches and restarting of idle capacities.

Australia is the second-largest producer of alumina, producing about 21 million tons per year. Australia is strongly maintaining its position as a top exporter, with six refineries producing smelter-grade alumina-based primarily fed.

North America Alumina Market

North America accounted for approximately more than 8% of the global alumina demand in 2024, with very slow growth expected in the coming years. Canada has the major alumina demand in the region primarily due to its lower carbon footprint production. The existence of hydropower sources empowers Canada to make its products competitive in pricing against other areas. It is also considered the fourth-largest primary aluminum producer in the world after China, India, and Russia.

U.S. was the largest export destination for Canada's aluminum products, with the U.S. accounting for around 90% of the total aluminum imports. This trend will likely continue for the next few years, as the country is over-reliant upon imports to fulfill its demands for aluminum and aluminum products. However, in February 2025, the U.S. government announced a 25% tariff on all aluminum imports into the country, including from Canada. The U.S., on the other hand, is also counted among the major producers of chemical-grade alumina in the world, a grade mostly used for calcined alumina and alumina hydrate.

Latin America Alumina Market

In Latin America, Brazil is predominant in alumina production, having produced over 10 million tons in 2022. Jamaica is a significant producer in the region with rich bauxite reserves and is placed among the top five producers worldwide. Jamaica improved earnings from the bauxite and alumina sector in 2023.

Europe Alumina Market

Alumina Production Costs Have Skyrocketed due to the Ongoing Geopolitical Confrontation between Russia and Ukraine.

Russia has been an important contributor to the alumina and aluminum industry in Europe, with over 35% of alumina production in Europe in 2023. The ongoing geopolitical tension with Ukraine is what ultimately caused the metallurgical alumina prices in Europe to fluctuate negatively.

The production potential for alumina in Ukraine has been disturbed by the conflict. At the same time, Australia has banned exporting bauxite and alumina to Russia, which has further affected the supply chain of these raw materials.

Meanwhile, it has also meant that there are higher alumina imports from China into Russia, filling some of the gaps in supply. While sanctions have turned the dynamics of global alumina trade, this could probably allow some market realignment.

Although high energy prices have caused some disruptions to aluminum smelters across Europe, this may act as a spur for innovation and investment into sustainable energy solutions. The industry then would be able to navigate these obstacles in a much more efficient way towards achieving its goals of green transition.

Middle East & Africa Alumina Market

Guinea's Suspension of Bauxite Will Stir the World Alumina and Aluminum Production

Due to the suspension of bauxite in Guinea, a major source of bauxite for China, exports have negatively impacted global alumina market growth while spot prices have been hitting all-time highs. This was followed by spiking alumina prices in China to an all-time high on October 15 due to these supply delays and high demand from aluminum producers. For example,

China imports 70% of its bauxite from Guinea for alumina production. This reliance has increased as Guinea's output has received considerable Chinese investment during the last 10 years.

Supply issues worsened when customs officials halted Guinée Alumina Corporation (GAC) exports. Bauxite supply constraints from China and unfavorable import conditions, such as rising alumina costs in Australia, weigh heavily on aluminum producers. Given a few arbitrage possibilities, production can be expected to continue. The profit margins of aluminum smelters in China are anticipated to be sustained in the future.

Manufacturers are Driving Their Commitment Toward Sustainability and The Circular Economy

Several leading companies like Aluminium Corporation of China Limited (CHALCO), China Hongqiao Group Ltd, Shandong Xinfa Group, Alcoa, Rio Tinto Alcan, and Rusal have successfully integrated their alumina businesses. These manufacturers are pursuing capacity expansion and resolving bottlenecks present in their facilities that would have positive implications on general performance.

Sustainability and carbon reduction are now top priorities, constituting the technological drivers for advancement within the alumina sector. In a radical rethink, this would set out to address every aspect of the value chain, right from bauxite and alumina to finished aluminum products.

Recent Developments

|

Report Attributes |

Details |

|

Historical Data/Actuals |

2019 - 2024 |

|

Forecast Period |

2025 - 2032 |

|

Market Analysis Units |

Value: US$ Bn/Mn, Volume: As applicable |

|

Geographical Coverage |

|

|

Segmental Coverage |

|

|

Competitive Analysis |

|

|

Report Highlights |

|

By Grade

By Application

By Region

To know more about delivery timeline for this report Contact Sales

The market is set to reach US$ 80 Bn in 2025.

In 2023, Australia was the largest exporter of alumina, followed by Brazil, India, Indonesia, and the European Union (EU).

Aluminum Corporation of China Limited (Chalco), Alcoa Corporation, and China Hongqiao Group Co. Ltd. are a few leading players.

The industry is estimated to rise at a CAGR of 3% through 2032.

The alumina industry is likely to reach US$ 106 Bn in 2032.