- Medical Devices

- Mammography Market

Mammography Market Size, Share, and Growth Forecast 2026 - 2033

Mammography Market by Product (Digital Mammography, Analog Mammography, Breast Tomosynthesis (3D), Film-Screen Mammography, Others), Technology (2D Mammography, 3D Mammography, Contrast-Enhanced Mammography, CAD (Computer-Aided Detection), Others), End-user (Hospitals, Diagnostic Imaging Centers, Specialty Clinics, Ambulatory Surgical Centers), and Regional Analysis, 2026 - 2033

Mammography Market Share and Trends Analysis

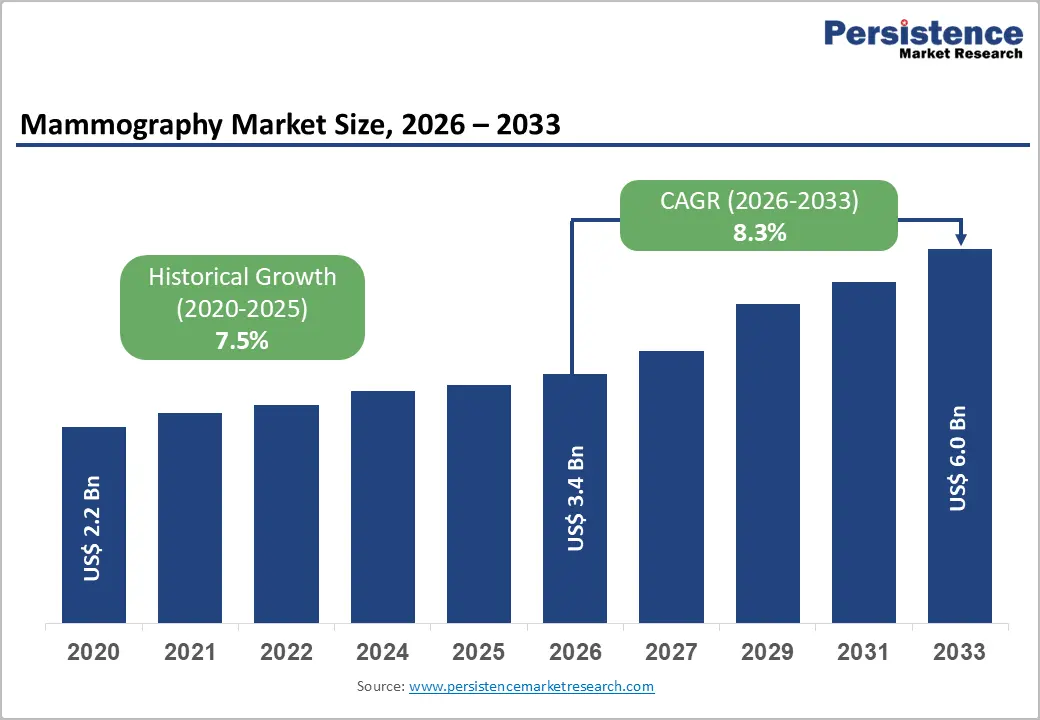

The global Mammography market size is expected to be valued at US$ 3.4 billion in 2026 and projected to reach US$ 6.0 billion by 2033, growing at a CAGR of 8.3% between 2026 and 2033. It is experiencing strong and accelerating growth, driven by the rise in global breast cancer incidence, rapidly expanding national breast cancer screening programs, and the technological shift toward AI-integrated 3D breast tomosynthesis systems that dramatically improve early detection sensitivity. Breast cancer is the world's most commonly diagnosed cancer, with the International Agency for Research on Cancer (IARC) GLOBOCAN 2022 report documenting 2.3 million new breast cancer cases globally, representing 11.6% of all cancer diagnoses.

Expanding government-mandated mammography screening frameworks in North America, Europe, and increasingly Asia Pacific, combined with the transition from analog to digital and 3D mammography platforms, is creating sustained capital equipment and software replacement demand, amplifying market growth well above the broader medical imaging sector average.

Key Industry Highlights:

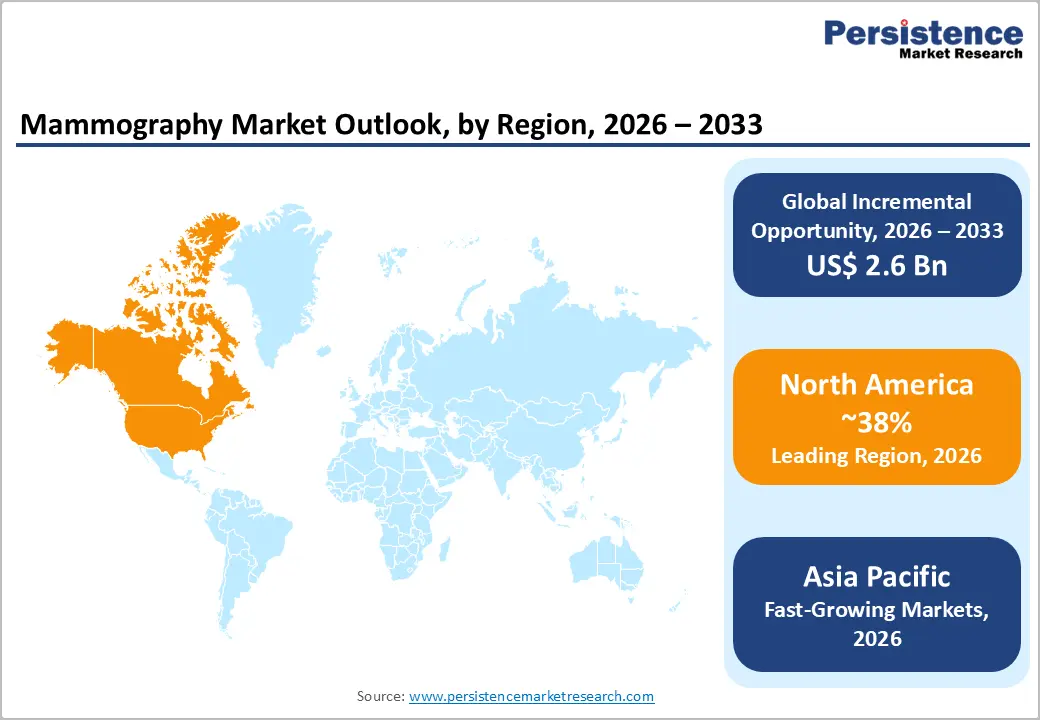

- Regional Leadership: North America leads the global Mammography market with approximately 38% market share in 2026, driven by the USPSTF's 2024 guideline expanding recommended screening age to 40, comprehensive Medicare and commercial insurance reimbursement, and rapid adoption of AI-integrated 3D tomosynthesis platforms from market leaders Hologic, Inc. and GE HealthCare.

- Fast-growing Market: Asia Pacific is one of the fast-growing markets, propelled by rapidly rising breast cancer incidence across China and India, expanding national screening program investments under Healthy China 2030, and growing private hospital adoption of digital and 3D mammography systems driven by increasing healthcare infrastructure capacity and medical tourism.

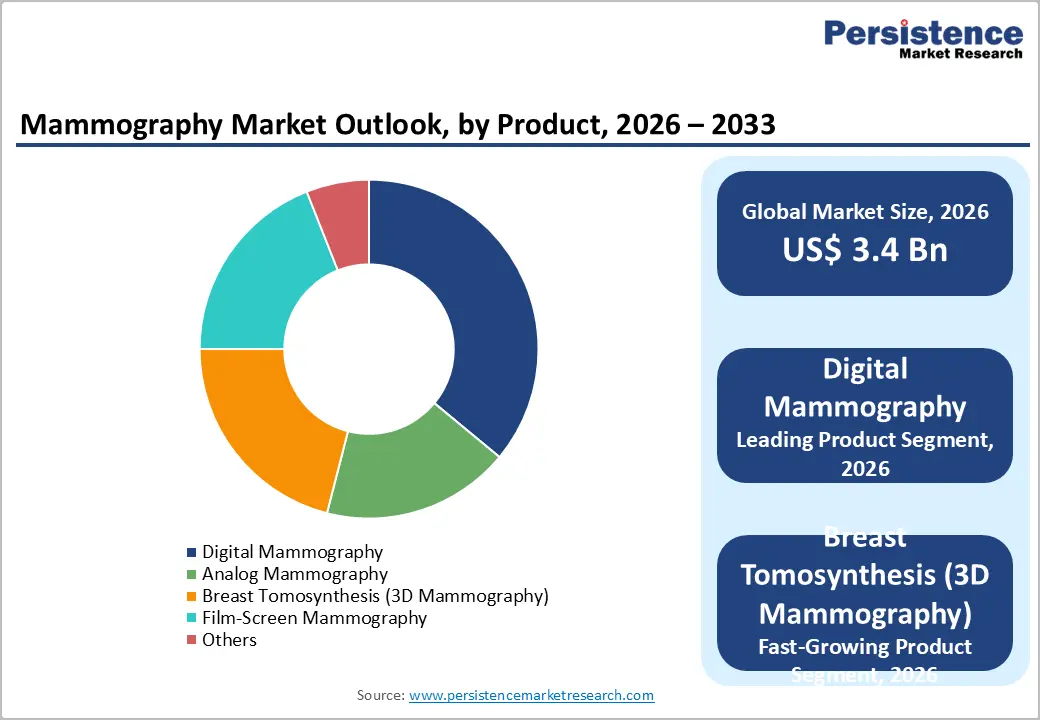

- Leading Product: Digital mammography leads the product category with approximately 36% market share in 2026, reflecting its near-universal adoption as the standard of care in developed markets with approximately 90% of FDA MQSA-certified U.S. mammography facilities utilizing digital systems and its established integration with AI-powered CAD software and hospital PACS networks.

- Fast-growing Product: Breast Tomosynthesis (3D Mammography) is the fastest-growing product segment, driven by ACR, EUSOBI, and SBI guidelines endorsing 3D as the preferred screening modality, clinical evidence of 40% higher invasive cancer detection rates, and active replacement of legacy 2D digital mammography systems across hospitals and imaging centers globally.

- Opportunity: The integration of AI and CAD software into mammography workflows, validated by a landmark Nature Medicine study demonstrating AI performance matching dual radiologist reads, represents the highest-value market opportunity, enabling manufacturers to develop recurring software subscription revenue streams while addressing the global radiologist workforce deficit estimated by the Royal College of Radiologists.

Market Dynamics

Is the Global Rise in Breast Cancer Incidences Scaling Screening Programs?

Breast cancer's position as the world's most prevalent malignancy is the foundational demand driver for the mammography market. The IARC's GLOBOCAN 2022 report identified 2.3 million new breast cancer cases globally in 2022, with the American Cancer Society (ACS) projecting approximately 310,720 new invasive breast cancer diagnoses in U.S. women in 2024 alone. The clinical and public health imperative for early detection—where Stage I breast cancer has a 5-year survival rate exceeding 99% per the ACS, versus significantly lower rates at advanced stages makes regular mammographic screening the most impactful preventive oncology intervention globally.

The U.S. Preventive Services Task Force (USPSTF) updated its 2024 guidelines, recommending that women begin biennial mammography screening at age 40, expanding the eligible screening population significantly. Similar guideline revisions by the European Society of Breast Imaging (EUSOBI) advocating for annual screening in high-risk populations are generating substantial incremental scan volume demand across Europe, directly driving mammography system utilization and procurement.

Accelerating Adoption of AI-Powered 3D Breast Tomosynthesis Driving Technology Upgrade Cycles

The rapid integration of artificial intelligence (AI) and machine learning algorithms into mammography platforms, combined with the shift from 2D to 3D breast tomosynthesis, is creating an active technology upgrade cycle across hospital and imaging center mammography fleets globally. The U.S. Food and Drug Administration (FDA) has cleared over 100 AI-based mammography analysis algorithms as of 2024, enabling AI-assisted lesion detection, risk stratification, and workflow prioritization that demonstrably improve radiologist productivity and diagnostic accuracy.

Clinical evidence published in the Journal of the National Cancer Institute (JNCI) demonstrates that 3D tomosynthesis reduces recall rates by approximately 15–20% while increasing invasive breast cancer detection rates by 40% compared to standard 2D mammography. This compelling clinical evidence is accelerating healthcare institution procurement decisions to upgrade from legacy 2D digital mammography systems to current-generation 3D tomosynthesis and AI-integrated platforms from manufacturers including Hologic, Inc. and GE HealthCare.

How do High Equipment Costs and Reimbursement Constraints Limit Adoption in Emerging Markets?

Advanced digital mammography and 3D tomosynthesis systems carry significant capital costs ranging from approximately US$ 100,000 to US$ 500,000 per unit for full-field digital mammography (FFDM) and tomosynthesis platforms creating substantial adoption barriers in lower-middle-income healthcare markets. In many emerging economies, limited public health budgets and inconsistent insurance reimbursement coverage for mammography screening restrict institutional procurement to basic analog or entry-level digital systems. The World Bank classifies over 80 countries as lower-middle or low-income economies where per-capita health expenditure remains below US$ 300 annually, significantly constraining advanced mammography system penetration in these markets.

Radiation Exposure Concerns and False Positive Rates Generating Patient Hesitancy

Despite significant improvements in digital mammography dose optimization, concerns about cumulative radiation exposure from repeat mammographic screenings continue to generate patient hesitancy, particularly among younger women in the newly expanded USPSTF-recommended screening age bracket of 40–49. Additionally, mammography's documented false positive rate estimated at 10–12% per screening round per American College of Radiology (ACR) data leads to unnecessary recall imaging, patient anxiety, and additional healthcare costs. These clinical performance limitations drive some patients to delay or decline recommended screening, constraining population-level screening utilization rates and limiting achievable mammography system throughput volumes in certain markets.

Does the Rapid Expansion of 3D Breast Tomosynthesis Replace Legacy 2D Digital Systems Globally?

Breast tomosynthesis (3D mammography) is the fastest-growing product segment and represents the most commercially compelling near-term opportunity in the mammography market. The transition from legacy full-field digital mammography (FFDM) to 3D tomosynthesis is accelerating globally following updated clinical guidelines from the American College of Radiology (ACR), EUSOBI, and the Society of Breast Imaging (SBI), all of which now endorse 3D tomosynthesis as the preferred mammographic screening modality. Hologic, Inc., the pioneer of commercial 3D tomosynthesis with its Selenia Dimensions and 3Dimensions platforms, has reported strong and consistent revenue growth in its breast health division, validating the commercial scale of this transition.

With a large installed base of legacy 2D digital mammography systems across hospitals and imaging centers globally, particularly in Europe and Asia Pacific, the replacement opportunity for 3D tomosynthesis platforms represents a multi-year, multi-billion-dollar capital equipment upgrade cycle for mammography manufacturers.

How do Integration of AI and Computer-Aided Detection (CAD) Create High-Value Software Revenue Streams?

The integration of AI-powered Computer-Aided Detection (CAD) and risk stratification software into mammography workflows represents a transformative high-growth opportunity that extends mammography manufacturers' commercial engagement beyond hardware sales into recurring software subscription and AI analytics revenue models.

The FDA's Digital Health Center of Excellence has been progressively expanding clearances for AI-based mammography decision support tools, with companies including Hologic, Inc., iCAD, and Lunit receiving clearances for AI algorithms demonstrating equivalent or superior sensitivity to radiologist-only reads. A landmark study published in Nature Medicine demonstrated that AI-only mammography reading in a UK NHS screening setting matched the performance of two radiologists, highlighting AI's potential to address radiologist workforce shortages estimated at a deficit of tens of thousands of radiologists globally by the Royal College of Radiologists, while improving screening throughput and early detection rates.

Category-wise Analysis

Product Insights

Digital mammography is the leading product segment in the mammography market, accounting for approximately 36% of global market share in 2025. Full-field digital mammography (FFDM) holds this leadership position as the established standard of care for breast cancer screening across major healthcare systems globally, having successfully displaced film-screen mammography over the past two decades.

The FDA's Mammography Quality Standards Act (MQSA) program, which certifies mammography facilities across the United States, reported that approximately 90% of certified U.S. mammography facilities utilize digital mammography systems, reflecting digital's near-complete displacement of analog film-screen technology in developed markets. Digital mammography's proven clinical performance across diverse breast densities, compatibility with AI-powered CAD software overlays, and integration with hospital PACS and radiology information systems secure its continued volume leadership, even as 3D tomosynthesis captures a growing share of new installations at the premium tier.

Technology Insights

2D Mammography holds the leading position within the technology segmentation, representing approximately 48% of the global mammography market share in 2026. Despite the accelerating clinical and commercial transition toward 3D tomosynthesis, 2D mammography encompassing full-field digital mammography (FFDM) systems maintains volume leadership owing to its dominant installed base across global healthcare institutions, well-established reimbursement frameworks in both public and private healthcare systems, and lower acquisition and operational costs compared to 3D platforms.

The Centers for Medicare & Medicaid Services (CMS) provides distinct reimbursement codes for both 2D and 3D mammography, with 2D reimbursement more broadly accessible across a wider range of payer arrangements, supporting continued high-volume utilization. However, technology share is shifting progressively toward 3D mammography, classified as the fastest-growing technology segment, as guideline updates and clinical evidence continue to drive system upgrade procurement.

End-user Insights

Diagnostic imaging centers represent the leading end-user segment for mammography, accounting for approximately 42% of global market share in 2026. Dedicated diagnostic imaging centers, including both independent and hospital-affiliated outpatient imaging facilities, are the primary delivery point for population-level mammography screening programs globally, owing to their specialized imaging infrastructure, radiologist expertise, high patient throughput optimization, and accessibility for ambulatory screening populations.

In the United States, the ACR reports that the majority of mammography screenings are performed in dedicated breast imaging centers and outpatient radiology facilities rather than inpatient hospital settings. The increasing focus on creating dedicated breast health centers offering integrated mammography, ultrasound, MRI, and biopsy services under one roof is further reinforcing diagnostic imaging centers' dominant market position and driving adoption of premium 3D tomosynthesis and AI-integrated platforms.

Regional Insights

North America Mammography Market Trends and Insights

North America leads the global mammography market with approximately 38% market share in 2026 anchored by the United States' dominant position as the world's largest breast cancer screening market, strong national screening program coverage, the USPSTF's 2024 guideline update lowering the recommended screening age to 40, and rapid clinical adoption of AI-integrated 3D tomosynthesis platforms. The region benefits from comprehensive Medicare and commercial insurance reimbursement for both 2D and 3D mammography, supporting high annual screening volumes and active technology upgrade procurement.

U.S. Mammography Market Size

The United States accounts for approximately 88% of North America's mammography market, with the ACS reporting approximately 310,720 new breast cancer diagnoses projected for 2024 and national mammography screening guidelines mandating regular screening for tens of millions of eligible women. The USPSTF's 2024 guideline update, expanding recommended screening age to 40, is expanding the screened population, driving incremental scan volume and system utilization growth across U.S. imaging centers and hospitals equipped with Hologic and GE HealthCare mammography platforms.

Europe Mammography Market Trends and Insights

Europe is the second-largest regional mammography market, characterized by well-established national breast cancer screening programs across the U.K., Germany, France, the Netherlands, and Sweden, and progressive adoption of EUSOBI-endorsed 3D tomosynthesis screening guidelines. The European Commission's updated cancer screening recommendations advocate for organized mammography screening programs across all EU member states, supporting consistent institutional procurement of mammography systems. Growing AI-assisted mammography reading programs to address radiologist workforce shortages are a defining regional technology trend.

Germany Mammography Market Size

Germany accounts for approximately 22% of Europe's mammography market, anchored by its national organized mammography screening program that invites all women aged 50–69 for biennial screening under the Krebsfrüherkennungs-Richtlinie (cancer screening guidelines). Germany's well-funded statutory health insurance system fully covers invited screening mammography, sustaining consistent high-volume imaging center procurement of advanced digital and 3D tomosynthesis systems from manufacturers including Siemens Healthineers, headquartered in Erlangen.

U.K. Mammography Market Size

The U.K. represents approximately 16% of Europe's mammography market. The NHS Breast Screening Programme invites women aged 50–70 for triennial mammographic screening, performing approximately 2 million screening mammograms annually. The NHS has been actively piloting AI-assisted mammography reading programs with landmark studies published in Nature Medicine validating AI performance—and is expanding 3D tomosynthesis deployment across breast screening units, supporting premium technology procurement across the national program.

France Mammography Market Size

France accounts for approximately 14% of Europe's mammography demand. France's national organized breast cancer screening program (Programme National de Dépistage Organisé du Cancer du Sein) invites women aged 50–74 for biennial mammography, funded through Assurance Maladie. France is one of Europe's most active markets for AI mammography integration, with the Institut National du Cancer (INCa) coordinating national pilots of AI-assisted double-reading programs designed to enhance screening sensitivity and address radiologist capacity constraints.

Asia Pacific Mammography Market Trends and Insights

Asia Pacific is the fast-growing regional mammography market, driven by rapidly expanding breast cancer incidence, with China and India together accounting for a significant share of the IARC's projected growth in global breast cancer cases, increasing government investment in organized screening programs, and growing healthcare infrastructure capacity in Japan, South Korea, Australia, and ASEAN nations. China leads regional demand with the National Health Commission of China expanding breast cancer screening initiatives across urban and peri-urban populations as part of Healthy China 2030 cancer prevention targets.

India Mammography Market Size

India represents approximately 7% of the Asia Pacific's mammography market, with demand growing rapidly alongside expanding private hospital networks, increasing breast cancer awareness, and government health scheme investments. India has one of the largest breast cancer burdens in Asia. The Indian Council of Medical Research (ICMR) estimates breast cancer as the most common cancer among Indian women yet population-level screening penetration remains low, creating substantial unmet demand for affordable digital mammography systems across both public and private healthcare facilities.

Japan Mammography Market Size

Japan accounts for approximately 19% of the Asia Pacific's mammography market, reflecting its mature healthcare system and well-organized national breast cancer screening program. Japan's Ministry of Health, Labour and Welfare (MHLW) mandates biennial mammography screening for women aged 40 and above, with Fujifilm Corporation and Canon Medical Systems Corporation both Japanese manufacturers, holding strong domestic market positions in digital mammography system supply.

Competitive Landscape

The global mammography market is highly competitive, driven by continuous advancements in breast imaging technologies and the growing focus on early breast cancer detection. Companies are investing in digital mammography systems, 3D breast tomosynthesis, contrast-enhanced imaging, and AI-powered diagnostic tools to improve screening accuracy and workflow efficiency. Rising demand for minimally invasive and high-precision diagnostic solutions is accelerating product innovation.

Key Developments

- In May 2026, UNC Health Rex launched a new mobile mammography unit named “Hope Esperanza” to expand breast cancer screening access across North Carolina. The unit was introduced to provide 3D breast screenings for patients with and without insurance within a 55-mile radius of Raleigh, covering 21 counties with limited healthcare access.

- In April 2026, GE HealthCare expanded its collaboration with DeepHealth to strengthen AI-powered mammography solutions globally. The partnership introduced enhanced capabilities of DeepHealth’s Breast Suite, including ProFound Pro and Safeguard Review, integrated with GE HealthCare’s Senographe Pristina and Pristina Via mammography systems.

Global Mammography Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.2 Billion |

|

Current Market Value (2026) |

US$ 3.4 Billion |

|

Projected Market Value (2033) |

US$ 6.0 Billion |

|

CAGR (2026–2033) |

8.3% |

|

Leading Region |

North America, 38% market share (2025) |

|

Dominant Product Category |

Digital Mammography, ~36% market share (2025) |

|

Top-Ranking Technology |

2D Mammography, ~48% market share (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 2.6 Billion |

Companies Covered in Mammography Market

- Hologic, Inc.

- GE HealthCare

- Siemens Healthineers

- Koninklijke Philips N.V.

- FUJIFILM Corporation

- Canon Medical Systems Corporation

- Carestream Health

- Planmed Oy

- Metaltronica S.p.A.

- Konica Minolta, Inc.

- Analogic Corporation

- IMS Giotto

- Delphinus Medical Technologies

Frequently Asked Questions

The global mammography market size is estimated to be valued at US$ 3.4 billion in 2026.

The key demand drivers are the escalating global breast cancer burden with approximately 310,720 new U.S. diagnoses projected in 2024 per the ACS expanding screening guidelines including the USPSTF's 2024 recommendation lowering the screening age to 40, and accelerating adoption of AI-powered CAD and 3D tomosynthesis platforms.

North America leads the global Mammography market with approximately 38% market share in 2025, primarily driven by the United States where the ACS projects over 310,000 annual breast cancer diagnoses, and the USPSTF's 2024 guideline update significantly expands the eligible screening population.

The most significant growth opportunity lies in the large-scale integration of AI-powered CAD and Computer-Aided Detection software into mammography workflows, enabling recurring software subscription revenue models that extend manufacturer engagement beyond hardware.

Leading companies in the global Mammography market include Hologic, Inc., GE HealthCare, Siemens Healthineers, Koninklijke Philips N.V., FUJIFILM Corporation, Canon Medical Systems Corporation, Carestream Health, Planmed Oy, IMS Giotto, Metaltronica S.p.A., Konica Minolta, Inc.,