- Metals & Minerals

- Steel Rebar Market

Steel Rebar Market Size, Share, and Growth Forecast, 2026 - 2033

Steel Rebar Market by Product Type (Deformed, Mild), Process (Basic Oxygen Steelmaking, Electric Arc Furnace), Application (Residential Building, Public Infrastructure, Industrial), and Regional Analysis for 2026 - 2033

Steel Rebar Market Size and Trends Analysis

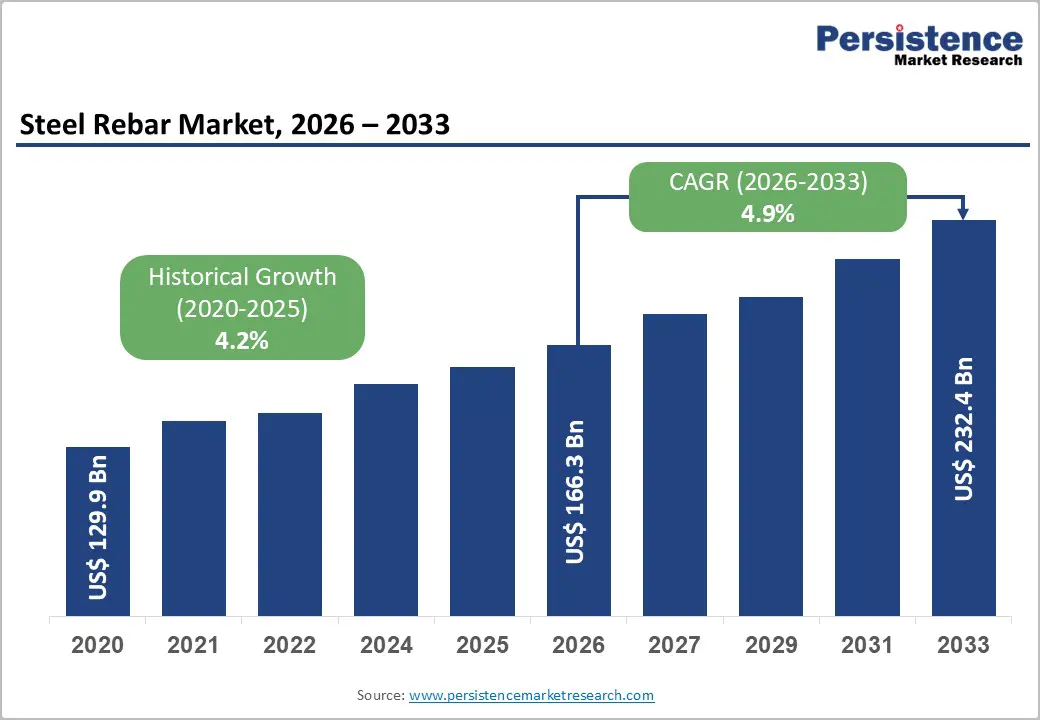

The global steel rebar market size is likely to be valued at US$166.3 billion in 2026, and is expected to reach US$232.4 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by accelerating urbanization in emerging economies, surging public infrastructure investment, and the global transition toward green steel production through Electric Arc Furnace (EAF) technology that supports the circular economy and lower carbon-intensity construction supply chains.

Key Industry Highlights

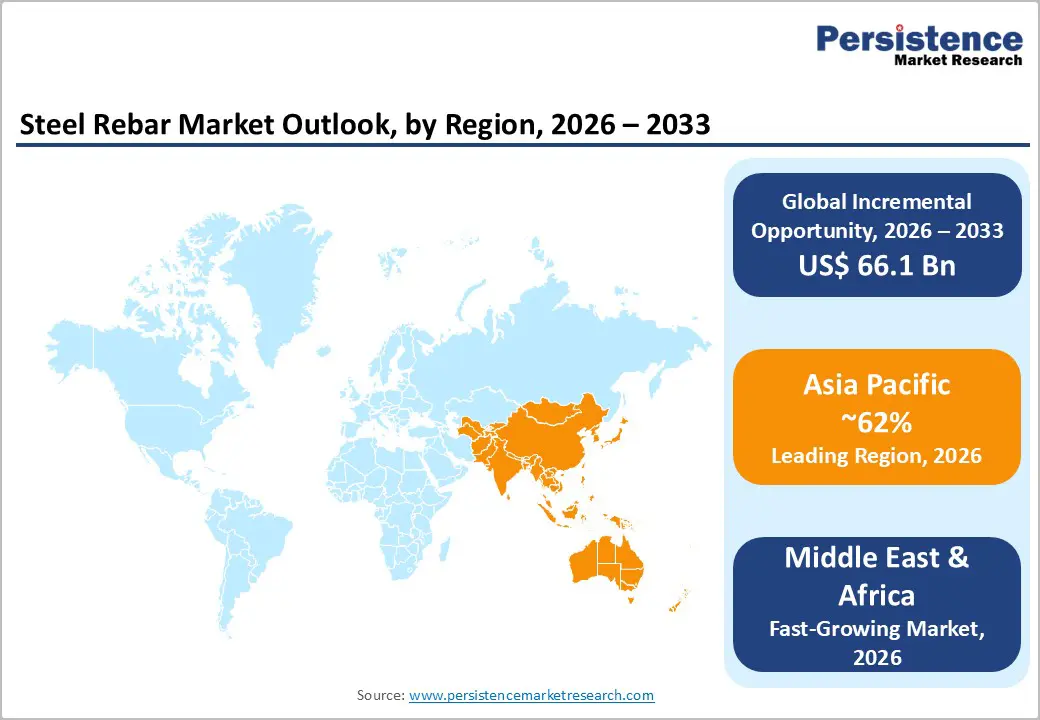

- Dominant Region: Asia Pacific is set to command approximately 62% of the global steel rebar market revenue in 2026, anchored by China's colossal construction activity, India's infrastructure push under the National Infrastructure Pipeline, and Southeast Asia's rapid urbanization trajectory.

- Fastest-growing Region: The Middle East & Africa is projected to be the fastest-growing regional market for steel rebar, driven by Gulf Cooperation Council (GCC) mega-project pipelines, including NEOM in Saudi Arabia and large-scale affordable housing programs across Sub-Saharan Africa.

- Leading Product Type: Deformed rebar accounts for approximately 72% of the total steel rebar market share, preferred universally for its superior mechanical bond strength with concrete in reinforced concrete (RC) structural applications.

- Leading Process: Electric arc furnace (EAF) steelmaking is expected to represent approximately 58% of the global steel rebar production process mix, driven by its lower carbon footprint, scrap metal feedstock flexibility, and regulatory alignment with green steel mandates.

DRO Analysis

Driver - Green Steel Transition and EAF Technology Expansion Reshaping Production Economics

The accelerating shift from basic oxygen steelmaking to electric arc furnace production technology is a defining supply-side driver that is simultaneously expanding the competitiveness of steel rebar and aligning the industry with increasingly stringent environmental regulations. EAF-produced steel generates approximately 0.4–0.6 tonnes of CO2 per tonne of steel produced, compared to 1.8–2.2 tonnes for the BOS route, a carbon intensity reduction of approximately 75% that carries significant commercial implications as carbon pricing mechanisms expand globally.

The European Union's Carbon Border Adjustment Mechanism (CBAM), which began phasing in from October 2023 and will be fully operational by 2026, imposes carbon costs on imported steel products entering the EU market, directly benefiting EAF-based rebar producers with lower embedded carbon footprints. The EU Emissions Trading System (ETS) carbon price, which has traded in the €50–€100 per tonne CO2 range since 2021, adds direct cost pressure on BOS-route producers within Europe, accelerating investment in EAF conversion.

Restraint - Volatility in Iron Ore and Scrap Steel Feedstock Prices Compressing Margins

The steel rebar market is highly sensitive to feedstock price volatility, as raw materials, iron ore for BOS producers, and scrap steel for EAF operators account for a major share of production costs. Fluctuations in iron ore prices significantly impact manufacturer margins, particularly for producers lacking integrated mining assets or long-term supply agreements to cushion against spot market exposure.

Scrap steel price volatility creates challenges for EAF-based rebar producers. Scrap availability is uneven globally. Developed economies generate abundant scrap, while rapidly industrializing regions in South and Southeast Asia often face supply constraints relative to growing EAF capacity, adding cost pressure and supply risk.

Opportunity - Affordable Housing Deficits in Emerging Economies Creating Sustained Long-Cycle Demand

The global affordable housing deficit represents one of the most durable and large-scale demand opportunities for the steel rebar market across the forecast period. The World Bank estimates that over 1 billion people globally live in inadequate housing, with the largest concentrations in Sub-Saharan Africa, South Asia, and Southeast Asia. Closing this deficit through government-sponsored and private sector affordable housing programs requires construction of hundreds of millions of new residential units over the next decade, each consuming substantial quantities of reinforcing bar in reinforced concrete structural systems that dominate construction practice in these markets.

Government-funded affordable housing programs are already generating measurable rebar demand uplift. India's PMAY scheme, Indonesia's One Million Houses program, Egypt's National Housing Project targeting 1.5 million social housing units, and Ethiopia's Integrated Housing Development Program collectively represent construction pipelines that will consume tens of millions of tonnes of reinforcing bar through 2033.

Category-wise Analysis

Product Type Insights

Deformed rebar is expected to dominate, commanding approximately 72% of the total market revenue in 2026. Its leadership is rooted in the superior mechanical interlock it provides with concrete through its ribbed or twisted surface profile, which dramatically enhances the tensile load transfer efficiency of reinforced concrete structures compared to smooth mild steel bars. Steel Authority of India Limited (SAIL) uses ribbed TMT rebars in infrastructure and seismic projects, where the deformed surface ensures stronger concrete bonding and better load transfer than smooth bars.

Mild rebar is likely to be the fastest-growing segment, characterized by its smooth surface and lower yield strength, due to its cost advantage and widespread use in low-specification construction applications across price-sensitive emerging markets. Tata Nexarc, which highlights that mild steel (plain) rebars are widely used in small residential buildings, repair works, and low-rise structures due to their lower cost and ease of fabrication.

Process Insights

Electric arc furnace steelmaking is projected to dominate approximately 58% of the total share in 2026. EAF's leadership position has been established through the structural advantages it offers in terms of capital efficiency, environmental compliance, and feedstock flexibility relative to the integrated BOS route. Nucor Corporation operates entirely on EAF-based mini-mills, leveraging lower capital costs and high flexibility to scale efficiently and rank among North America’s largest steel producers.

Basic oxygen steelmaking is likely to be the fastest-growing, retaining significant capacity in Asia Pacific, particularly in China, Japan, and South Korea, where integrated steelmakers with large BOS complexes continue to produce substantial rebar volumes as part of multi-product steel output portfolios. POSCO HOLDINGS INC., which operates large integrated steel complexes at Pohang and Gwangyang using the blast furnace–basic oxygen steelmaking (BOS) route.

Application Insights

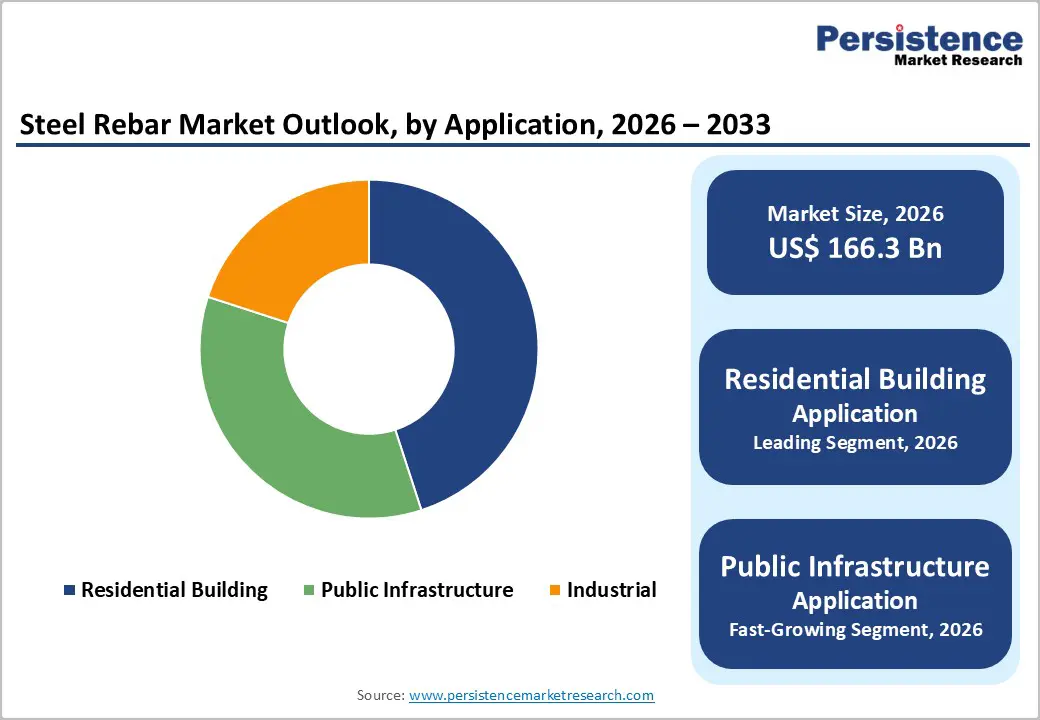

The residential building application is expected to dominate, approximately 45% of total market revenue in 2026. Residential construction's leadership position is driven by the persistent urban housing deficit across the world's fastest-growing economies, where multi-story reinforced concrete apartment construction dominates the housing delivery model. Edgemere Commons, an affordable housing project developed by S. Falco Construction in New York, used over 1,200 tons of rebar in a multi-family residential building with 237 apartments.

Public infrastructure is expected to be the fastest-growing application, propelled by coordinated government investment in transportation, water, energy, and urban-mobility infrastructure across both developed and developing economies. Steel Authority of India Limited (SAIL), which supplied large volumes of rebar for the Lucknow Metro Rail project part of India’s expanding urban transport infrastructure. The company supplied rebar for metro corridors and bridge projects nationwide, reflecting strong demand driven by public infrastructure investment.

Regional Insights

North America Steel Rebar Market Trends

The North America steel rebar market is growing steadily, propelled by large-scale infrastructure rehabilitation, urban construction, and government programs such as the U.S. Infrastructure Investment and Jobs Act and Canada’s federal-provincial infrastructure and transit projects. Key trends include rising demand for higher-strength and recycled steel rebars, a shift toward sustainable and LEED-aligned construction, and infrastructure (transport, utilities, and energy) outpacing residential growth as the main source of rebar consumption across the region.

U.S. Steel Rebar Market Insights

The U.S. is North America’s largest market and one of the most structurally important in the developed world, underpinned by a deep infrastructure-renewal cycle and a mature EAF-based domestic production base. The Infrastructure Investment and Jobs Act (IIJA), allocating about US$1.2 trillion through 2030, is the key demand driver for U.S. rebar consumption, funding highway reconstruction.

Canada Steel Rebar Market Insights

Canada’s market is supported by consistent public-sector demand fueled by federal and provincial infrastructure investments, including the Investing in Canada program and major transit developments such as Ontario’s subway expansion and British Columbia’s Broadway Corridor SkyTrain extension. These large-scale projects help offset potential slowdowns in the residential construction sector by maintaining steady infrastructure-related activity.

Europe Steel Rebar Market Trends

The Europe market is growing steadily, driven by large-scale infrastructure programs, urbanization, and ongoing residential and non-residential construction across the region. Key trends include rising demand for low-carbon “green” rebar under the EU Green Deal, stricter sustainability and emissions regulations, and growing use of corrosion-resistant and higher-grade rebars in transport and coastal infrastructure.

Germany Steel Rebar Market Trends

Germany is Europe’s largest market, underpinned by robust construction demand, ongoing rail and road infrastructure programs, and a strong need for domestic rebar supply to support both new builds and refurbishment. Major drivers include the Deutschlandtakt rail expansion, extensive Autobahn rehabilitation and modernization projects, and ambitious social-housing targets that collectively sustain high-volume rebar consumption across the country.

U.K. Steel Rebar Market Trends

The U.K. market is driven by urban residential development, particularly the government's target of 300,000 new homes per year, alongside substantial infrastructure programs including HS2 high-speed rail (which, despite scope revisions, remains a major civil engineering rebar consumer), the Thames Tideway Tunnel, and various National Highways improvement schemes.

Asia Pacific Steel Rebar Market Trends

Asia Pacific market is projected to dominate, capturing the 62% of share in 2026, driven by rapid urbanization, large-scale infrastructure investments, and government-led construction programs, particularly in China and India. Demand is shifting toward high-strength, earthquake-resistant rebar as building codes tighten, while EAF-based production is expanding to support decarbonization and cost-efficiency.

China Steel Rebar Market Trends

China dominates the global steel rebar market, accounting for ~50% of consumption and production at peak, driven by cyclical property and infrastructure activity. The 14th Five-Year Plan, with over RMB 45 trillion (US$6.2 trillion) in infrastructure investment, fuels demand across high-speed rail expansion (~35,000 km planned), urban metro development (>9,000 km), and large-scale water conservancy projects.

Japan Steel Rebar Market Trends

Japan’s market is defined by stringent quality standards and strong demand for seismic reinforcement, urban redevelopment, and aging infrastructure upgrades. Key projects include Expo 2025 Osaka, the Linear Chuo Shinkansen, and nationwide resiliency programs for earthquake-prone structures. NIPPON STEEL CORPORATION and Daido Steel lead the market, offering high-strength SD490 and SD590 earthquake-resistant rebar that commands premium pricing.

Middle East & Africa Steel Rebar Market Trends

The Middle East & Africa steel rebar market is likely to be the fastest-growing region globally, propelled by rapid urbanization, large-scale infrastructure projects, and rising residential and commercial construction across GCC, North Africa, and sub-Saharan economies. Demand is led by transport, energy, and industrial zone developments, with governments prioritizing airports, highways, power plants, and social housing schemes that all require substantial volumes of reinforcing bars.

UAE Steel Rebar Market Trends

The UAE market is expanding rapidly, driven by a construction and infrastructure boom in Dubai, Abu Dhabi, and surrounding emirates, including large-scale real estate, transport, and tourism projects. Infrastructure is the largest and fastest-growing rebar-using segment, supported by government-led programs in transport, utilities, and industrial-zone development that sustain high-volume demand.

Saudi Arabia Steel Rebar Market Trends

Saudi Arabia is a growing market, supported by the country’s massive construction and infrastructure build-out under Vision 2030 and related megaprojects such as NEOM and the Qiddiya entertainment city. Demand is being driven by large-scale transport networks, urban-scale housing schemes, and industrial-zone developments that require high-volume rebar consumption for both high-rise and heavy-civil structures.

Competitive Landscape

The global steel rebar market features a tiered competitive landscape with global steel giants, regional leaders, and EAF-based mini-mill operators. ArcelorMittal leads with a highly diversified production footprint across Europe, North America, and Brazil. In Asia-Pacific, POSCO HOLDINGS INC. and NIPPON STEEL CORPORATION specialize in high-strength, earthquake-resistant rebar for premium markets.

The mid-tier competitive space includes JSW Steel (India), SAIL (India), NLMK (Russia), Acerinox S.A. (Spain), Commercial Metals Company (U.S.), and Daido Steel (Japan), each with strong domestic market positions and selective export capabilities. Competitive differentiation in the global steel rebar market increasingly centers on documented carbon intensity credentials, rebar product traceability and sustainability certification, high-strength product portfolios (Grade 500 and Grade 600 rebar), and supply reliability in the context of construction project critical-path procurement requirements.

Key Industry Developments:

- In April 2026, Jindal Stainless Ltd launched its ‘Jindal Infinity’ stainless steel rebars in the retail segment, beginning in Amritsar, Punjab. The company aimed to directly capture the construction value chain by offering products with enhanced durability and corrosion resistance, and it planned a pan-India rollout over the following 6–12 months.

- In October 2024, Shyam Metalics and Energy Ltd. launched stainless steel rebar production to target coastal infrastructure demand, aligning with the ‘Make in India’ initiative. The move followed policy support from the Ministry of Road Transport and Highways, with Nitin Gadkari emphasizing the use of corrosion-resistant rebars in coastal regions, strengthening market adoption.

Companies Covered in Steel Rebar Market

- Acerinox S.A

- ArcelorMittal

- Commercial Metals Company

- Daido Steel Co Ltd

- Gerdau S/A

- HBIS Group

- Jiangsu Shagang Group

- JSW

- NIPPON STEEL CORPORATION

- NLMK

- Nucor

- POSCO HOLDINGS INC.

- SAIL

- Steel Dynamics, Inc.

Frequently Asked Questions

The global steel rebar market is projected to reach US$166.3 billion in 2026.

The steel rebar market is driven primarily by urbanization-led residential construction demand in emerging economies, coordinated government infrastructure investment programs, including the U.S. IIJA, India's National Infrastructure Pipeline, and Saudi Arabia's Vision 2030, and the accelerating green steel transition toward EAF production that is lowering the carbon intensity of rebar supply chains and aligning them with sustainable construction procurement requirements.

The steel rebar market is poised to witness a CAGR of 4.9% from 2026 to 2033.

Key opportunities include the global affordable housing deficit requiring hundreds of millions of new residential units in emerging economies through 2033, and the renewable energy infrastructure construction boom encompassing wind turbine foundations, solar farm civil works, and grid modernization projects, which is creating a structurally new and rapidly growing industrial demand vertical for reinforcing bar beyond traditional construction application categories.

Key players include ArcelorMittal, Nucor Corporation, POSCO HOLDINGS INC., Gerdau S/A, JSW Steel, NIPPON STEEL CORPORATION, HBIS Group, Jiangsu Shagang Group, NLMK, Acerinox S.A., Commercial Metals Company, Steel Dynamics Inc., Daido Steel Co. Ltd., and SAIL.