- Metals & Minerals

- Laminated Steel Market

Laminated Steel Market Size, Share, and Growth Forecast, 2026 – 2033

Laminated Steel Market by Product Type (Carbon Steel, Low-alloy Steel, Electrical Steel, Others), Manufacturing Process (Cold-rolled Laminated Steel, Others), End-user (Automotive & Transportation, Construction & Infrastructure, Others), and Regional Analysis for 2026-2033

Laminated Steel Market Share and Trends Analysis

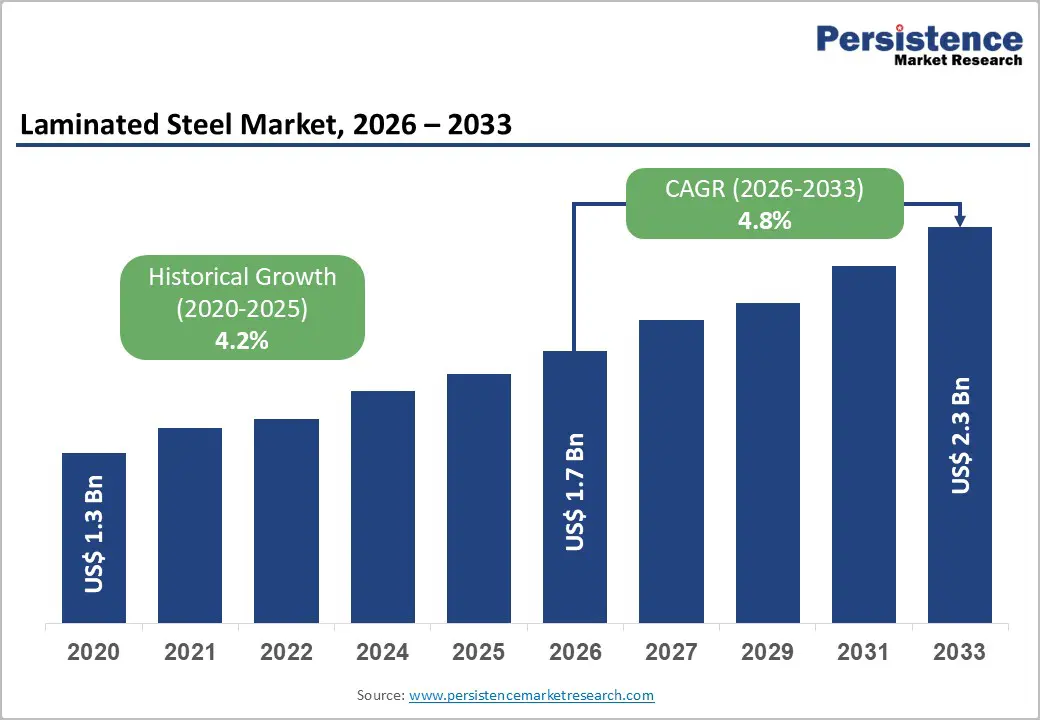

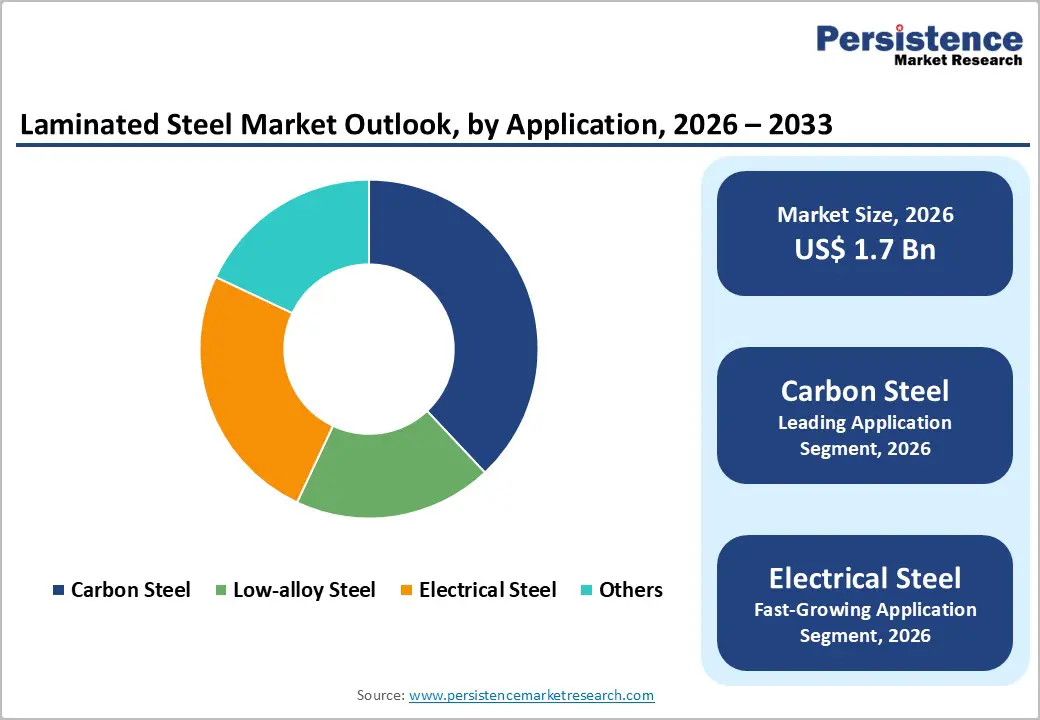

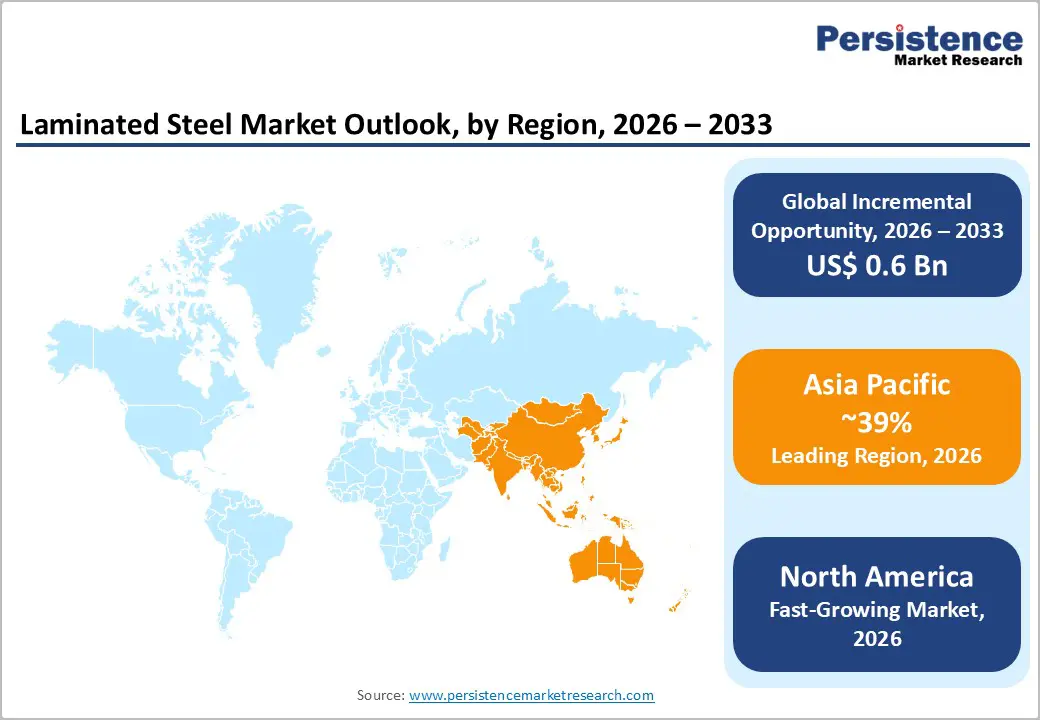

The global laminated steel market size is likely to be valued at US$1.7 billion in 2026 and is estimated to reach US$2.3 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by rising demand for high-efficiency electrical systems, lightweight structural materials, and corrosion-resistant steel solutions across industrial applications.

Growth in electrification programs within transportation and power infrastructure is increasing the adoption of laminated steel due to improved magnetic performance and reduced energy losses. Industrial modernization initiatives and government infrastructure investments strengthen demand across the construction and manufacturing sectors.

Key Industry Highlights:

- Leading Product Type: Carbon steel is set to hold around 38% revenue share in 2026 due to versatility and cost-effectiveness across structural applications.

- Fastest-Growing Product Type: Electrical steel is projected to be the fastest-growing, supported by high efficiency in transformers and motors across power infrastructure.

- Leading End-user: Automotive & transportation is likely to lead with a 35% share in 2026, driven by lightweight crash-resistant components improving fuel efficiency and safety.

- Fastest-Growing End-User: Electrical & power generation is anticipated to be the fastest-growing segment, fueled by demand for efficient magnetic cores in transformers and generators.

- Regional Leadership: Asia Pacific is projected to capture roughly 39% of the market share by 2026, while North America is forecast to record the fastest growth due to electrification and automation.

- Competitive Environment: Moderately consolidated with strong global steel producers focusing on innovation and low-carbon production.

- Innovation Trends: Advancements in electrical efficiency, coating technologies, and smart manufacturing integration are shaping material evolution.

DRO Analysis

Driver - Growth in Industrial Automation and Mobility Electrification

Industrial automation and mobility electrification act as structural demand accelerators for laminated steel through rising deployment in high-efficiency motors, transformers, and precision drive systems. Automation in manufacturing elevates the adoption of low-loss electrical cores in robotics, Computer Numerical Control (CNC) systems, and servo motors, improving energy efficiency and operational stability. Integration of smart factory systems increases reliance on compact magnetic components, supporting higher torque density and reduced thermal losses across continuous production environments.

Mobility electrification expands usage in electric drivetrains, hybrid systems, and charging infrastructure, where magnetic performance directly influences efficiency. Expansion of rail electrification and electric vehicle ecosystems reinforces demand for lightweight laminated cores in traction motors and power electronics. India's steel consumption rose 7% in FY26 to 164 million tonnes, supported by industrial and infrastructure expansion. This reflects strong downstream material pull from electrified transport and automated industrial systems.

Restraint - High Production Complexity and Cost Sensitivity

Manufacturing laminated steel requires multiple precision steps, such as rolling, annealing, insulation coating, and segment stacking, which raise capital and operational intensity. Each stage needs tight process control to limit core losses and maintain magnetic performance, increasing equipment cost and maintenance burden. This complexity limits the number of qualified producers and constrains capacity scalability, especially in regions with weaker manufacturing infrastructure.

Raw-material and energy costs amplify sensitivity to price fluctuations and compress margins for both producers and end-users. Cost-driven segments often prioritize upfront equipment cost over incremental efficiency gains, favoring lower-grade materials or alternative designs. This price-conscious behavior caps demand growth in price-sensitive regions and reduces Original Equipment Manufacturer (OEM) willingness to invest in premium laminated steel, even where efficiency benefits are evident.

Opportunity - Expansion of Renewable Energy Infrastructure

Rising deployment of renewable energy systems drives sustained demand for high-efficiency electrical cores within the laminated steel market. Solar and wind installations require transformers and generators that minimize energy losses during conversion and transmission. Government of India, Ministry of New and Renewable Energy, 2025, indicates installed renewable energy capacity above 253.96 GW, supporting grid integration expansion. This trend strengthens procurement of electrical grade materials across utility and industrial segments, networks upgrade.

Grid modernization linked to renewable integration strengthens the demand for advanced laminated steel used in power conversion and distribution equipment. Variable output from wind and solar resources increases reliance on efficient transformers and motor cores designed for reduced thermal and core losses. Electric mobility charging networks and distributed energy systems expand utilization across urban infrastructure. Industrial operators prioritize energy-efficient materials supporting higher replacement cycles and capacity upgrades across electrical networks.

Category-wise Analysis

Product Type Insights

Carbon steel is likely to be the leading segment with 38% revenue share in 2026, due to its balance of strength, affordability, and widespread use in structural and general fabrication. Industry acceptance stems from proven performance in bridges, industrial framing, and columns, supported by mature supply chains and standard tolerances. Alloy refinements boost fatigue resistance without major cost hikes. Examples include beams, columns, and rebar in municipal and industrial projects.

Electrical steel is expected to witness the fastest growth as electrification boosts demand for low-loss magnetic properties in motors and transformers. Treatment effectiveness reduces energy dissipation, favoring high-frequency-optimized grades. Examples include EV traction motors, wind-turbine generators, and distribution transformers. Scaled production for renewables, standardized testing, and innovation in grain-oriented variants shorten development cycles for next-generation drivetrains and grid-linked equipment.

Manufacturing Process

Fusion method laminated steel is poised to lead with a forecasted over 60% market share in 2026, due to monolithic bonds that eliminate delamination under thermal cycling. Consumer trust stems from long-term field data and structural integrity in demanding environments. Cultural acceptance in heavy industry favors adhesive-free processes, supported by standardized output and regulatory simplicity. Industrial adoption rises through compatibility with existing fabrication infrastructure. Preventive maintenance and digital configurators enhance adoption.

Coated and composite lamination methods are anticipated to be the fastest-growing segment, driven by advanced surface treatments that improve corrosion resistance and aesthetics. Consumer trust builds on accelerated weathering data. Designers favor multifunctional materials for visible applications and e-commerce-driven customization. Industrial safety protocols prefer coatings that reduce particulate release, while virtual prototyping shortens quotation cycles.

End-user Insights

The automotive & transportation segment is likely to be the leading segment with a projected 35% of the laminated steel market share in 2026, due to its requirement for lightweight, crash-resistant components that improve fuel efficiency and safety ratings. Engineering validation comes from crash-test data confirming structural strength. Examples include body panels and battery enclosures, where reduced weight extends electric-vehicle range. OEM integration and digital design tools support precision use across high-volume vehicle production systems.

The electrical & power generation segment is anticipated to be the fastest-growing segment, fueled by global electrification initiatives that demand efficient magnetic cores for transformers and generators. Efficiency ratings verified under international standards strengthen adoption confidence. Examples include distribution transformers and wind generators, where lamination improves energy transfer efficiency. Government renewable capacity expansion data support demand growth. Predictive maintenance systems and modular designs enhance operational reliability across grid infrastructure and renewable energy installations.

Regional Insights

North America Laminated Steel Market Trends

North America is forecast to be the fastest-growing market for laminated steel, stimulated by rapid grid modernization and heavy capital deployment in transformer and electrical infrastructure manufacturing. Large-scale investments from companies such as Hitachi Energy and Siemens Energy exceed $1 billion each in 2025–2026, targeting transformer shortages linked to data center expansion and electric vehicle charging networks. The United States Department of Energy reports rising backlog in transformer manufacturing capacity and extended delivery cycles for grid equipment, reinforcing the urgency for domestic sourcing and high-efficiency electrical steel adoption.

Growth acceleration is further supported by renewable integration policies and industrial reshoring programs across the U.S. and Canada. General Electric, ABB, and Schneider Electric expand digital transformer production aligned with grid resilience targets and AI-driven electricity demand growth. Hitachi Energy’s Ontario facility expansion strengthens regional capacity for large transformer refurbishment and lifecycle services. Electric vehicle platforms from Ford and General Motors integrate laminated steel motor cores to improve efficiency, while utility upgrades prioritize low-loss materials for wind and solar grid connectivity.

Europe Laminated Steel Market Trends

Europe demonstrates strong momentum driven by advanced electrification systems, strict energy-efficiency mandates, and deep integration of renewable power infrastructure. Germany strengthens demand through Siemens Energy and thyssenkrupp Electrical Steel initiatives focused on high-grade motor cores for industrial automation and grid stabilization. France expands transformer modernization through Electricité de France (EDF) network upgrades and Alstom rail electrification programs supporting high-capacity power conversion systems. The U.K. advances adoption through National Grid reinforcement projects and offshore wind expansion requiring efficient electrical steel for transmission and storage infrastructure.

Italy supports consumption through precision engineering clusters in Lombardy and Emilia-Romagna, producing electrical motors and industrial drives. Spain accelerates deployment through Iberdrola renewable integration projects linked to wind and solar farms requiring high-efficiency transformers. Sweden and Finland reinforce growth through ABB Ltd electrification systems and Outokumpu Oyj steel innovations targeting low-loss magnetic performance. Strong decarbonization policies and industrial efficiency targets drive the continuous replacement of legacy electrical equipment across the manufacturing and utility sectors.

Asia Pacific Laminated Steel Market Trends

Asia Pacific is expected to lead with an estimated 39% of the laminated steel market share in 2026, supported by large-scale industrial expansion, integrated supply chains, and aggressive electrification programs. China strengthens its dominance through State Grid Corporation investments in ultra-high voltage transmission expansion and domestic steel output scaling by Baowu Steel Group. India advances demand through the National Electricity Plan 2025, which targets grid expansion and transformer capacity upgrades across renewable corridors.

Japan supports growth through Toshiba Energy Systems and Mitsubishi Electric initiatives focused on high-efficiency motor cores for industrial automation. South Korea drives adoption through Hyundai Motor Group's electrification programs and LS Electric investments in smart transformer systems aligned with digital grid upgrades. Manufacturing density across electrical equipment, automotive platforms, and renewable infrastructure accelerates laminated steel consumption. Continuous upgrades in precision rolling mills and automated lamination lines enhance production efficiency and material consistency across export-oriented supply chains.

Competitive Landscape

The global laminated steel market demonstrates a moderately consolidated structure with the presence of global steel manufacturers and specialized electrical steel producers. Leading players include ArcelorMittal, Nippon Steel, POSCO, and Tata Steel. Competition is driven by technological innovation, production efficiency, and material performance optimization. Market positioning is shaped by vertical integration, supply chain control, and advanced metallurgy capabilities across industrial applications.

ThyssenKrupp and JFE Steel Corporation strengthen competitive intensity through investments in high-efficiency electrical steel and precision lamination technologies. Strategic focus remains on energy-efficient product development and expansion into renewable energy and automotive electrification applications. Firms prioritize research and development in low-loss magnetic materials and thermal stability. Collaboration with automotive and power equipment manufacturers supports integration into electric motors, transformers, and grid infrastructure systems across global industrial value chains.

Key Industry Developments:

- In May 2025, Tata Steel announced an INR 15,000 crore (US$1.8 billion) capital expenditure plan for FY26, with major allocation toward India-based capacity expansion, electric arc furnace projects, and green steel initiatives aimed at strengthening laminated steel supply for automotive and electrical applications, supporting energy-efficient industrial growth.

- In May 2024, JSW Steel launched zinc-magnesium-aluminum-coated steel to improve corrosion resistance and support renewable energy and infrastructure applications, strengthening domestic advanced steel production for durable industrial use.

Companies Covered in Laminated Steel Market

- ArcelorMittal

- Nippon Steel

- POSCO

- Tata Steel

- ThyssenKrupp

- JFE Steel Corporation

- Voestalpine AG

- Baosteel Group

- AK Steel

- Cleveland-Cliffs Inc.

- Nippon Kokan K.K.

- JSW Steel

- Hyundai Steel

- SSAB

Frequently Asked Questions

The global laminated steel market is projected to reach US$1.7 billion in 2026.

Rising demand for energy-efficient electrical systems, electric vehicle adoption, and grid modernization drive the laminated steel market through improved magnetic performance and reduced energy losses.

The laminated steel market is poised to witness a CAGR of 4.8% from 2026 to 2033.

Expansion of renewable energy infrastructure, electrification of transportation systems, and modernization of power grids create strong opportunities for high-efficiency laminated steel adoption.

Some of the key market players include ArcelorMittal, JFE Steel Corporation, ThyssenKrupp, Nippon Steel, POSCO, and Tata Steel