- Metals & Minerals

- Hollow Concrete Block Market

Hollow Concrete Block Market Size, Share, and Growth Forecast, 2026 - 2033

Hollow Concrete Block Market by Product Type (Split-Faced Concrete Blocks, Others), Application (Non-Residential/Commercial, Residential, Others), Production Technique, and Regional Analysis for 2026 - 2033

Hollow Concrete Block Market Size and Trends Analysis

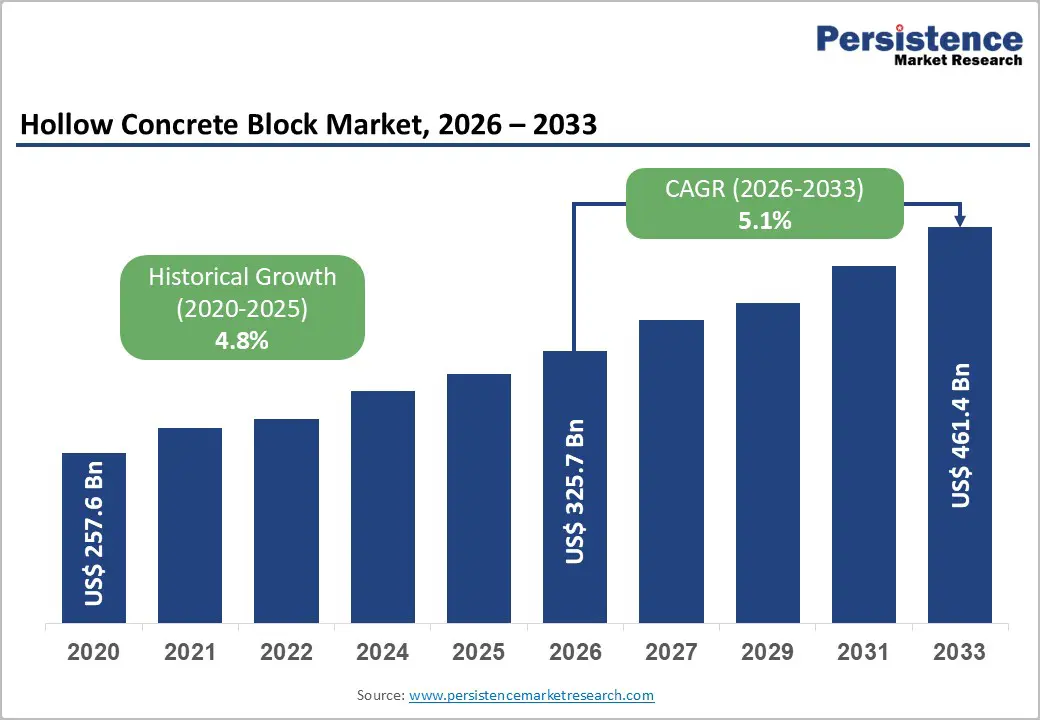

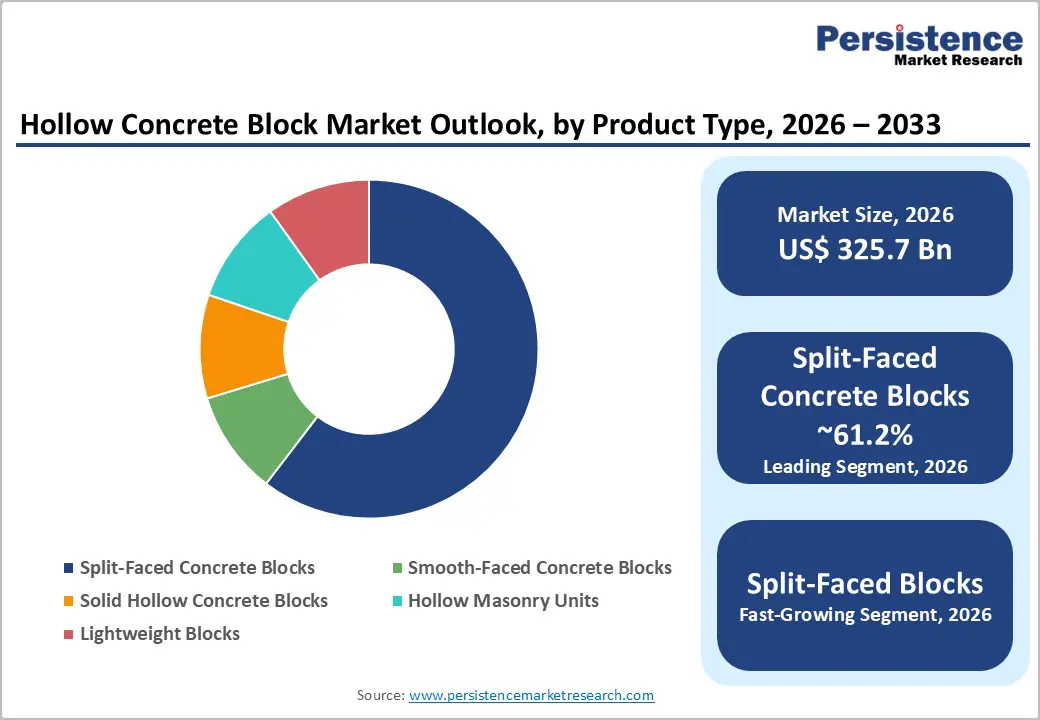

The global hollow concrete block market size is likely to be valued at US$325.7 billion in 2026 and is expected to reach US$461.4 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033, driven by increasing urbanization, the adoption of sustainable construction practices, and growing industrial demand. This growth reflects the strong recovery of the global construction sector alongside increasing investments in infrastructure development.

Overall, the hollow concrete block industry exhibits resilience and strategic significance, with particularly strong momentum in emerging economies undergoing rapid urbanization and infrastructure advancement.

Key Industry Highlights:

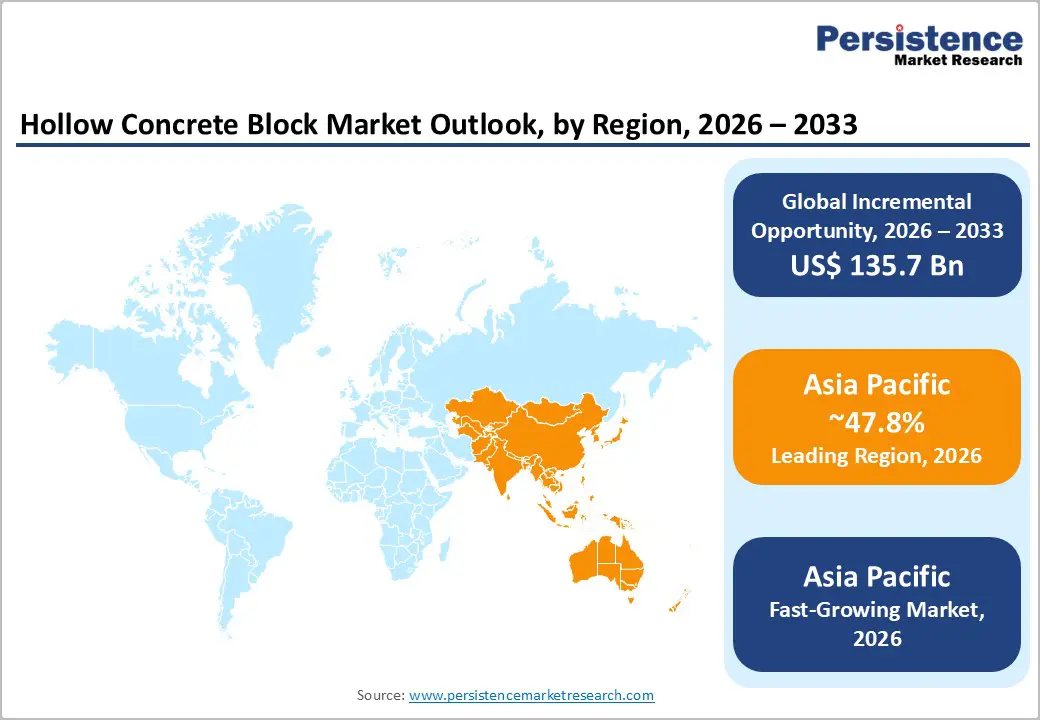

- Leading Region: Asia Pacific is projected to account for 47.8% of market share, driven by large-scale urbanization, infrastructure investments, and strong manufacturing capacity across China and India.

- Fastest-growing Region: Asia Pacific, supported by rapid urban migration, government housing initiatives, and expanding industrial construction activity.

- Investment Plans: Strong focus on production automation and low-carbon technologies, with increasing capital allocation toward advanced manufacturing systems and cement-free concrete solutions to enhance efficiency and sustainability.

- Dominant Product Type: Split-faced concrete blocks are anticipated to account for 61.2% revenue share in 2026, supported by high demand in architectural and non-residential applications due to durability and aesthetic appeal.

- Leading Application: The non-residential/commercial segment is estimated to hold 62.3% market share, driven by extensive use in commercial buildings, institutional infrastructure, and large-scale construction projects.

DRO Analysis

Driver Analysis - Accelerating Global Urbanization and Infrastructure Development

Global urbanization continues to accelerate, with the UN estimating that 68% of the world's population will live in urban areas by 2050, up from 56% in 2020. This demographic shift creates unprecedented demand for residential, commercial, and institutional infrastructure. Hollow concrete blocks represent a cost-effective, efficient solution for rapid construction in developing markets.

Major infrastructure initiatives, including India's Smart Cities Mission, China's New Urbanization Plan, and ASEAN connectivity projects, specifically incorporate concrete masonry components. Quantitative analysis indicates construction spending is projected to reach US$15.7 trillion annually by 2030, with masonry materials capturing an estimated 18-22% market share. Construction output in the Asia Pacific region alone is expected to grow at a 6.2% CAGR through 2033, directly translating into proportional increases in hollow concrete block demand.

Technological Advancement and Sustainable Manufacturing Practices

Manufacturing innovation substantially improves the efficiency and sustainability of the hollow concrete block sector. Modern production techniques, including automated mixing systems, vibration-induced compaction, and accelerated steam curing, increase production capacity by 30-40% while reducing material waste by 15-20%. Industry adoption of waste incorporation, recycled aggregates, industrial byproducts, and post-consumer materials aligns with circular economy imperatives.

Regulatory frameworks in Europe, North America, and progressive Asian markets mandate ESG compliance, incentivizing manufacturers to adopt low-carbon production methods. Studies indicate that sustainable hollow concrete blocks capture a 12-15% market premium, translating to revenue growth exceeding volume expansion. Advanced material formulations achieving 28-day compressive strengths of 7-8 MPa with 25% recycled content demonstrate commercial viability and competitive advantage in developed markets.

Restraint - Raw Material Cost Volatility and Supply Chain Disruptions

Hollow concrete block manufacturing depends critically on cement, aggregates, and energy inputs. Cement price volatility, fluctuating 15-28% annually depending on regional capacity and logistics costs, directly impacts production margins. Global supply chain disruptions, evidenced by freight cost inflation (60-80% above pre-pandemic baselines) and raw material scarcity, are creating production bottlenecks.

Energy costs constitute 8-12% of manufacturing expenses; electricity price increases in manufacturing-heavy regions reduce competitiveness. Labor cost escalation, particularly in high-growth markets such as India and Vietnam, increases production costs by 5-8% annually. These combined constraints compress margins, particularly for manufacturers lacking vertical integration or long-term supply agreements.

Opportunity - Emerging Market Infrastructure Investment and Affordable Housing Programs

Developing economies prioritize mass affordable housing construction, representing a substantial opportunity for hollow concrete block manufacturers. India's Pradhan Mantri Awas Yojana targets 20 million homes by 2030, while similar initiatives in Indonesia, the Philippines, and Nigeria are accelerating demand. Hollow concrete block's cost advantage, 50-70% cheaper than alternative load-bearing solutions, makes it the preferred material.

Public-private partnership infrastructure projects across Southeast Asia and Africa require 2-3 billion units in total. Manufacturers developing localized production capabilities in high-growth regions capture premium pricing and market share. Technology transfer partnerships enabling local production in developing nations create sustainable competitive advantages and resilient supply chains.

Green Building Standards and Regulatory Mandates

Global regulatory evolution mandates sustainable construction practices. LEED certification requirements, European Green Building Council standards, and national decarbonization targets increasingly specify the use of recyclable, low-embodied-carbon materials. Hollow concrete blocks with 40%+ recycled content and verified carbon footprints of <150 kg CO2-equivalent per cubic meter command premium positioning.

The EU Carbon Border Adjustment Mechanism's implementation creates a competitive advantage for manufacturers that meet stringent sustainability standards. Market expansion in green building sectors projects 12-18% premium pricing for certified sustainable products, with regulatory compliance becoming a market entry requirement by 2028-2030.

Category-wise Analysis

Product Type Insights

Split-faced concrete blocks are anticipated to dominate the product landscape, accounting for 61.2% of revenue share in 2026. Their leadership is driven by architectural appeal, durability, and versatility, making them a preferred choice for commercial façades, boundary walls, and landscaping applications. These blocks combine structural functionality with aesthetic value, reducing the need for additional finishing materials. Their widespread use in non-residential construction further reinforces their market dominance.

Split-faced blocks are also the fastest-growing segment, supported by increasing demand for visually appealing and low-maintenance construction materials. Growth is particularly strong in urban commercial developments where design aesthetics play a critical role. The shift toward integrated architectural solutions is expected to sustain the growth momentum of split-faced variants.

Application Insights

The non-residential segment is estimated to hold the largest share, accounting for approximately 62.3% of the market in 2026. This dominance is attributed to the extensive use of hollow concrete blocks in offices, educational institutions, warehouses, retail spaces, and infrastructure projects. Commercial projects typically require durable, fire-resistant, and cost-effective materials, making hollow blocks a preferred choice. Larger project sizes and repeat specifications further contribute to higher consumption volumes in this segment.

The residential segment is emerging as the fastest-growing application area, driven by housing demand, urban migration, and government-led housing initiatives. Rapid urban expansion in developing economies is increasing the need for affordable and scalable construction materials. Hollow concrete blocks are widely used in mid-rise housing, partition walls, and boundary structures, offering cost efficiency and ease of installation. This segment is expected to maintain strong growth due to ongoing housing shortages and infrastructure development.

Production Technique Insights

Machine-made production is estimated to dominate the market, accounting for 70-80% of market share in 2026. This method ensures high precision, consistent quality, and large-scale production capability, making it suitable for commercial and infrastructure projects. Automated manufacturing processes reduce material wastage and improve operational efficiency, enabling manufacturers to meet stringent construction standards and project timelines.

Advanced production methods, including lightweight and automated technologies, represent the fastest-growing segment. These techniques focus on reducing material weight, improving thermal performance, and lowering carbon emissions. Innovation in this segment is driven by sustainability goals and evolving construction practices, making it a key area of investment for forward-looking manufacturers.

Regional Insights

North America Hollow Concrete Block Market Trends

North America represents a mature, established market with stable growth dynamics.

U.S. Hollow Concrete Block Market Trends

North America represents a mature, established market with stable growth dynamics. The U.S. market is projected to account for approximately 37.1% of regional market value in 2026, demonstrating 3.9% CAGR through 2033. Market maturity, evidenced by established manufacturing capacity, distribution networks, and standardized specifications, provides baseline growth tied to construction sector expansion.

Commercial real estate development, driven by post-pandemic normalization and workplace modernization investment, sustains primary demand. Regulatory frameworks, including building codes emphasizing structural efficiency and fire resistance, favor hollow concrete block specifications. The U.S. Green Building Council LEED standards increasingly mandate sustainable material sourcing, incentivizing manufacturers to obtain third-party certifications and recycled content verification.

Competitive landscape concentration features major manufacturers, including Oldcastle Materials, Concrete Masonry Association members, and regional specialists. Innovation emphasis includes lightweight block development, specialized insulation systems, and integrated moisture management technologies. Investment trends focus on production automation upgrades and quality assurance systems. Strategic opportunities emerge in institutional construction (education, healthcare), infrastructure rehabilitation, and green building segments.

Recent developments include facility expansions by leading manufacturers and industry consolidation, pursuing economies of scale and geographic coverage optimization.

Canada Hollow Concrete Block Market Trends

Canadian market dynamics parallel U.S. trends with additional emphasis on regional supply chain resilience. The market benefits from stable construction demand and increasing focus on sustainable building materials and localized production capabilities.

Mexico Hollow Concrete Block Market Trends

Mexican markets demonstrate higher growth rates, reflecting infrastructure investment acceleration and housing demand. The country’s expanding construction sector supports increased adoption of hollow concrete blocks across residential and infrastructure applications.

Europe Hollow Concrete Block Market Trends

European markets, led by Germany, the U.K., France, and Spain, display differentiated growth dynamics reflecting regulatory harmonization and mature market characteristics.

Germany Hollow Concrete Block Market Trends

Germany is expected to command approximately 29.8% of the European market value in 2026, demonstrating a steady 3.8% CAGR driven by infrastructure restoration, energy efficiency retrofit projects, and sustained commercial construction. German manufacturing excellence and engineering standards establish competitive benchmarks across European markets.

France Hollow Concrete Block Market Trends

France is expected to represent 19% of the market value in 2026, emphasizing affordable housing development and urban regeneration projects. Demand is supported by government-backed housing initiatives and the modernization of the urban infrastructure.

Spain Hollow Concrete Block Market Trends

Spanish markets, accounting for 13% of regional value, benefit from EU infrastructure funding and construction sector recovery. Growth is supported by renewed investments in both public and private construction projects.

The EU regulatory environment, including Circular Economy Action Plan requirements and Construction Products Regulation compliance, mandates sustainable material sourcing and verified performance characteristics. Regulatory harmonization through the European Committee for Standardization establishes unified performance standards, facilitating cross-border competition and supply chain optimization.

Investment trends concentrate on waste incorporation technology, carbon footprint reduction, and advanced quality assurance systems. Environmental Product Declarations (EPD) certification increasingly determines market access and premium positioning. Strategic opportunities emerge in building renovation programs targeting 3% annual renovations and green building standard adoption.

Recent developments include manufacturer collaborations on sustainability initiatives, joint ventures pursuing market share expansion, and technology partnerships advancing lightweight composite innovations.

Asia Pacific Hollow Concrete Block Market Trends

Asia Pacific is expected to dominate the global hollow concrete block market, commanding 47.8% market share in 2026 and demonstrating an accelerating 5.8% CAGR, substantially exceeding global averages. Regional growth reflects unprecedented urbanization, industrial expansion, and infrastructure investment concentration.

China Hollow Concrete Block Market Trends

China is expected to contribute approximately 56.5% of the regional market value in 2026, leveraging massive manufacturing scale, construction output, and global supply chain integration. Chinese manufacturers collectively produce approximately 4.8-5.2 billion units annually, establishing global production leadership.

India Hollow Concrete Block Market Trends

India is expected to represent 19% of the regional market value in 2026, demonstrating the fastest growth (7.2% CAGR), driven by the Pradhan Mantri Awas Yojana housing initiative, smart cities development, and industrial construction acceleration.

Japan Hollow Concrete Block Market Trends

Japan is expected to maintain a mature market characteristic with steady 3.1% growth, focusing on quality premium positioning and advanced technology integration.

Regulatory environment evolution emphasizes seismic resilience, thermal efficiency, and moisture management, particularly in earthquake-prone regions. Investment trends concentrate on capacity expansion, advanced technology adoption, and supply chain localization. Strategic opportunities include market entry through joint ventures, technology partnerships with established domestic manufacturers, and specialized product development for regional requirements.

Recent developments include mega-facility investments by leading manufacturers, the acquisition of regional players by global corporations, and technology transfer partnerships advancing sustainable production capabilities.

Competitive Landscape

The global hollow concrete block market exhibits moderate fragmentation with significant regional variations. Global top-10 manufacturers control approximately 28-32% market share, with the remainder distributed among regional and local specialists. This structure reflects capital intensity, creating competitive advantages for large-scale operators, offset by geographic specificity, enabling local manufacturers to maintain competitive positions.

Mega-manufacturers, including Oldcastle Materials, Cemex, Bekaert, and regional leaders, maintain dominant positions through production scale, distribution networks, brand recognition, and technological capabilities. Mid-tier manufacturers differentiate through specialized product development, regional market expertise, and customer service excellence.

Market leaders employ differentiated strategic approaches. Cost leadership through production scale dominates mega-manufacturers, optimizing efficiency and competing on pricing. Innovation and product differentiation characterize technology-forward manufacturers developing lightweight variants, advanced insulation systems, and sustainable formulations commanding premium pricing. Geographic expansion pursues emerging market entry through joint ventures, capacity investments, and local partnership development.

Supply chain integration reduces cost and creates competitive advantages through vertical integration or long-term supplier agreements. Customer intimacy and technical support enable regional specialists to maintain competitive positions despite scale disadvantages. Emerging business model trends emphasize sustainability certification, circular economy participation, and integrated construction solutions addressing customer total cost of ownership.

Key Industry Developments:

- In February 2026, Sumitomo Osaka Cement developed high-durability concrete blocks designed for earthquake-resistant construction, strengthening its portfolio in infrastructure and seismic-resilient building solutions.

- In March 2026, Kennametal Inc. introduced advanced polycrystalline diamond (PCD) cutting tools designed for high-precision machining in aerospace and automotive applications, improving durability and performance.

Companies Covered in Hollow Concrete Block Market

- CRH plc

- Holcim Group

- CEMEX

- Heidelberg Materials

- Wienerberger AG

- Boral Limited

- Adbri Limited

- Oldcastle APG

- QUIKRETE Companies

- UltraTech Cement Limited

- Lafarge Canada Inc.

- Nitterhouse Masonry Products

- Taylor Concrete Products

- Thomas Armstrong (Concrete Blocks) Ltd

- Forterra plc

- BigBloc Construction Limited

Frequently Asked Questions

The global hollow concrete block market is valued at US$325.7 billion in 2026.

The hollow concrete block market is projected to reach US$461.4 billion by 2033.

Key trends include rising adoption of low-carbon and cement-free concrete blocks, increasing automation in manufacturing processes, growing demand for lightweight and energy-efficient materials, and strong infrastructure and housing development across emerging economies.

Split-faced concrete blocks lead the market, accounting for 61.2% revenue share, driven by their architectural appeal and durability in commercial applications.

The hollow concrete block market is expected to grow at a CAGR of 5.1% between 2026 and 2033.

Major companies include CRH plc, Holcim Group, CEMEX, Heidelberg Materials, and Wienerberger AG.