- Metals & Minerals

- Lanthanum Market

Lanthanum Market Size, Share, and Growth Forecast, 2026 - 2033

Lanthanum Market by Application (Catalysts, Batteries & Energy Storage, Others), Product Form (Lanthanum Oxide, Others), End-use Industry (Oil & Gas, Automotive, Electronics, Water Treatment), and Regional Analysis for 2026 - 2033

Lanthanum Market Share and Trends Analysis

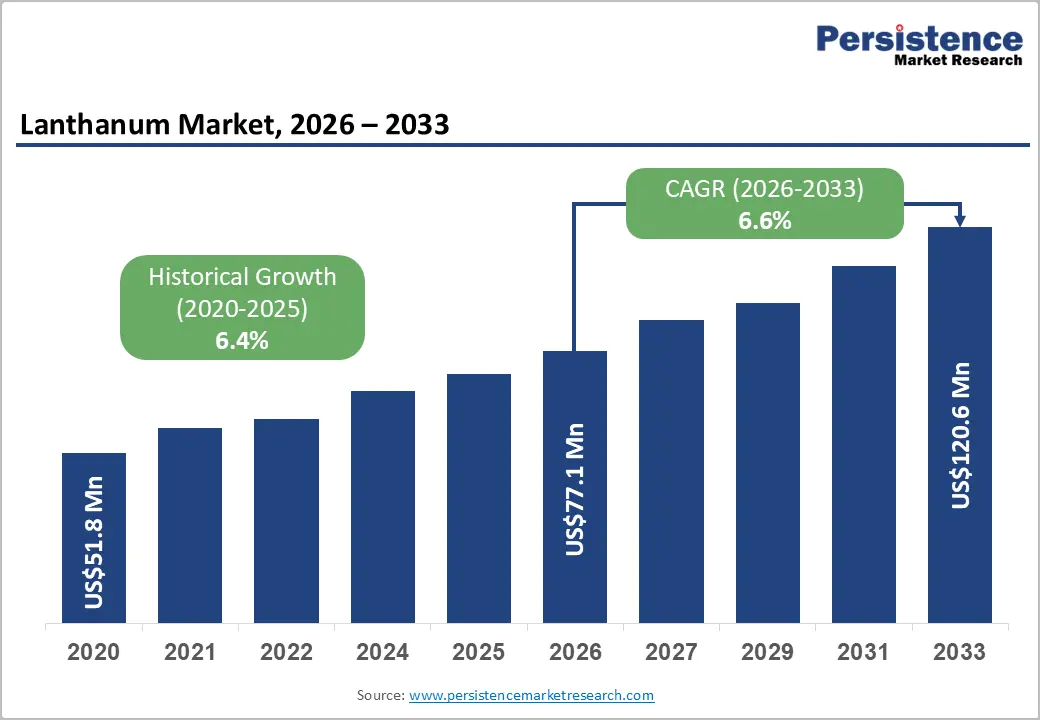

The global lanthanum market size is likely to be valued at US$77.1 million in 2026 and is projected to reach US$120.6 million by 2033, growing at a CAGR of 6.6% during the forecast period 2026 - 2033, driven by rising demand for petroleum refining catalysts, expanding electric vehicle (EV) battery applications, and increasing use in optical glass manufacturing.

Regulatory emphasis on cleaner fuels and water purification is further supporting adoption. Supply concentration in Asia and evolving recycling technologies continue to shape pricing dynamics and long-term availability.

Key Industry Highlights:

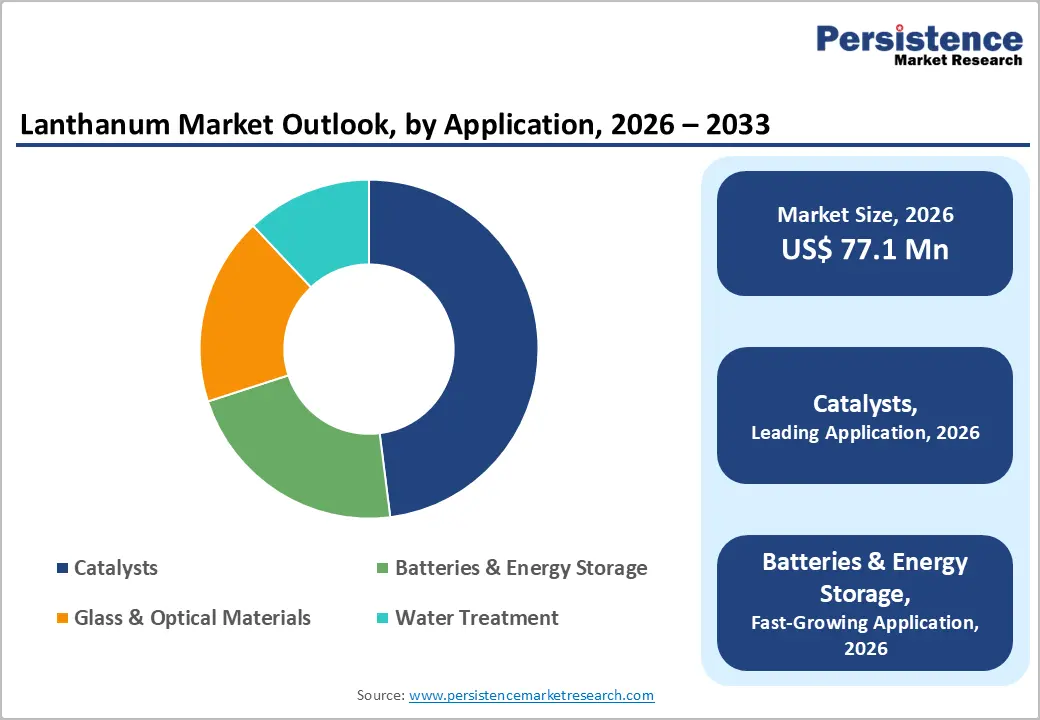

- Dominant Application Segment: Catalysts are set to command around 48% of the lanthanum market revenue share in 2026, while batteries & energy storage are likely to register the fastest growth through 2033, driven by EV adoption and renewable energy integration.

- Leading Product Forms: Lanthanum oxide is expected to dominate with approximately 52% share in 2026, while lanthanum carbonate is projected to be the fastest-growing segment through 2033, supported by increasing demand in environmental and water treatment applications.

- Key End-Use Trends: The oil & gas sector is anticipated to lead with nearly 44% share in 2026, while the automotive segment is likely to witness the fastest growth, reflecting rising EV and hybrid vehicle production.

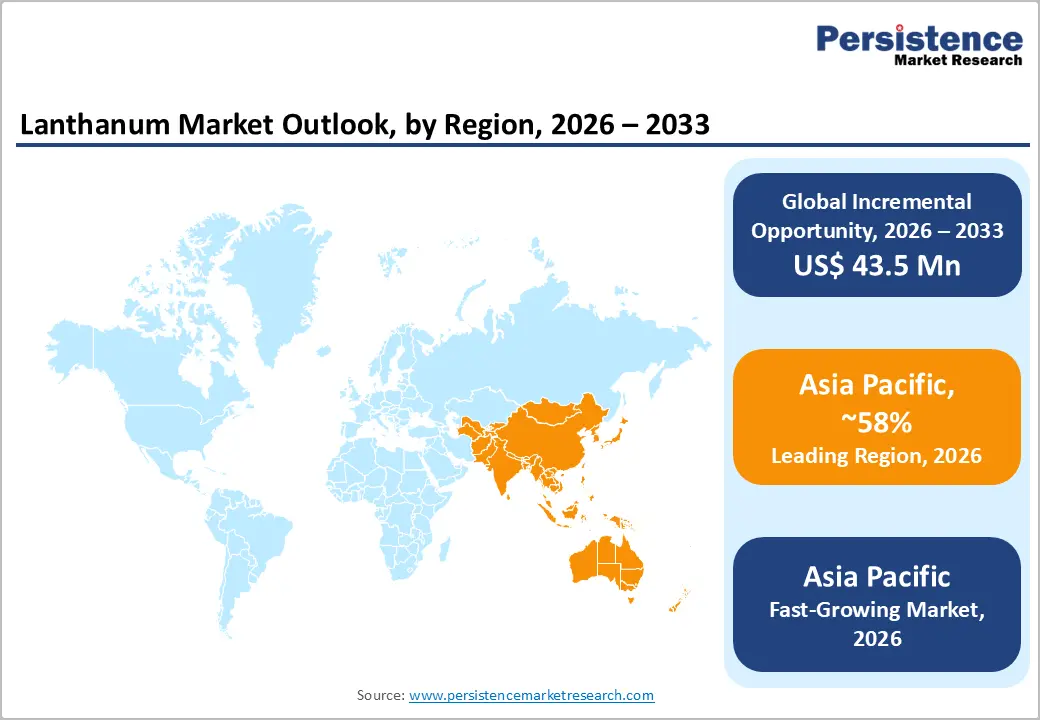

- Regional Leadership: Asia Pacific is poised to dominate with an estimated 58% share in 2026 and maintain the fastest growth trajectory through 2033, supported by China’s supply leadership and integrated manufacturing ecosystem.

- Future Market Direction: Industry focus on sustainability, rare-earth recycling, and supply diversification is expected to define long-term growth, as regulatory emphasis on environmental compliance and circular-economy practices increases.

DRO Analysis

Driver - Rising Demand for Catalytic Applications in Oil Refining

The primary growth driver for the lanthanum market is its critical role in fluid catalytic cracking (FCC) catalysts used in petroleum refining. According to the U.S. Energy Information Administration (EIA), global petroleum consumption exceeded 100 million barrels per day in 2024, directly driving catalyst demand. Lanthanum improves catalyst stability and enhances yield efficiency, making it indispensable for refineries aiming to meet stringent fuel standards such as Euro VI and EPA Tier 3 regulations.

The International Energy Agency (IEA) highlights continued investments in refining capacity across Asia and the Middle East. This sustained demand ensures steady consumption of lanthanum-based catalysts. As refineries optimize output and reduce sulfur emissions, lanthanum’s performance-enhancing properties will remain central, reinforcing its market growth trajectory.

Restraint - Supply Chain Concentration and Price Volatility Creating Structural Risk

The lanthanum market operates within a highly concentrated supply chain, with China accounting for over 60% of global rare earth production (U.S. Geological Survey). Export controls, environmental policies, and geopolitical tensions are increasing price volatility and disrupting the supply predictability. This concentration limits sourcing flexibility and exposes manufacturers to sudden cost escalations, thereby weakening procurement stability across industries that depend on lanthanum.

These fluctuations directly impact the automotive and electronics sectors, where cost sensitivity is critical. Limited recycling infrastructure further restricts alternative supply avenues, intensifying dependency risks. As a result, companies face higher inventory costs and constrained long-term planning. This structural imbalance ultimately slows investment momentum and reduces operational agility in lanthanum-driven applications.

Electric Mobility and Energy Storage Driving New Demand Frontiers

The accelerating adoption of electric vehicles (EVs) presents a strong growth opportunity for the lanthanum market, particularly in nickel-metal hydride (NiMH) batteries. According to the International Energy Agency (IEA), global EV sales surpassed 14 million units in 2024, with continued expansion expected across emerging markets. Policy momentum, including the U.S. Inflation Reduction Act and India’s FAME scheme, is accelerating battery manufacturing and localization of the supply chain. This shift is expanding lanthanum's role in cost-efficient battery chemistries, strengthening its strategic importance.

Lanthanum-based alloys are critical in battery performance, offering durability and cost advantages. Grid-scale energy storage systems are expanding, driven by the integration of renewable energy. Government-backed investments across the U.S., EU, and India are scaling battery ecosystems, unlocking multi-million-dollar demand potential. This convergence of EV growth and energy storage expansion creates a clear, long-term opportunity for lanthanum suppliers to scale and diversify.

Category-wise Analysis

Application Insights

Catalysts are expected to lead the lanthanum market, accounting for approximately 48% of the market share in 2026, driven by their critical role in petroleum refining. Lanthanum is expected to enhance catalyst efficiency, reduce coke formation, and improve fuel yield, aligning with tightening fuel standards such as Euro VI. Refinery upgrades across China and the Middle East are likely to reinforce this demand trend. This positions catalysts as a stable, high-volume segment with consistent consumption visibility over the forecast period.

Batteries & energy storage are projected to be the fastest-growing segment, expanding at an estimated CAGR of 6.6% through 2033, supported by accelerating EV adoption and renewable energy integration. Policy frameworks such as the U.S. Inflation Reduction Act and India’s FAME scheme are expected to scale battery production. Lanthanum-based NiMH batteries are likely to remain relevant in hybrid vehicles due to cost advantages. This shift is anticipated to diversify demand beyond traditional refining applications.

Product Form Insights

Lanthanum oxide is estimated to dominate with around 52% share in 2026, supported by its extensive use across catalysts, optical glass, and ceramics. Its ability to enhance refractive index and thermal stability is expected to sustain demand in precision optics and electronics. Growth in advanced display technologies and imaging applications, particularly in Asia, is likely to reinforce their adoption. This versatility positions lanthanum oxide as the most commercially stable product form.

Lanthanum carbonate is projected to be the fastest-growing segment, registering an estimated CAGR of 6.8% through 2033, driven by expanding environmental and healthcare applications. Increasing regulatory focus on wastewater treatment and phosphate removal is expected to boost demand. Additionally, its use in managing chronic kidney disease is likely to gain traction globally. This convergence of environmental compliance and healthcare needs is anticipated to unlock new growth opportunities.

End-Use Industry Insights

The oil & gas sector is estimated to lead with nearly 44% share in 2026, reflecting its reliance on lanthanum-based refining catalysts. Rising global fuel demand and refinery modernization projects, particularly in Asia and the Middle East, are expected to sustain consumption. Lanthanum’s role in improving refining efficiency and meeting emission standards is likely to remain critical. This ensures the segment’s continued dominance despite gradual energy transition trends.

The automotive industry is projected to be the fastest-growing segment, expanding at an estimated CAGR of over 6.9% through 2033, driven by increasing EV and hybrid vehicle production. Growth in electrification across China, the U.S., and Europe is expected to boost demand for lanthanum in battery systems. Continued use of NiMH batteries in hybrid vehicles is likely to support steady adoption. This shift is anticipated to position automotive as a key future growth driver.

Regional Analysis

North America Lanthanum Market Trends

North America is estimated to account for approximately 18.0% of the global lanthanum market in 2026, supported by advanced refining infrastructure and a strong regulatory environment. The region is witnessing a strategic shift toward domestic rare earth supply chains, driven by energy security concerns and clean energy investments. Increasing funding in EV manufacturing and battery ecosystems is expected to strengthen long-term demand. Recycling technologies and policy-backed initiatives are further shaping a more resilient supply framework.

U.S. Lanthanum Market Trends

The U.S. is estimated to contribute nearly 65% of the regional market, driven by strict environmental regulations and refinery modernization. Policies under the Defense Production Act are accelerating domestic rare earth processing capabilities. The country is also expanding EV and battery manufacturing capacity, reinforcing lanthanum demand. Strategic partnerships between mining and technology firms are strengthening supply chain independence.

Canada Lanthanum Market Trends

Canada accounts for an estimated 10% share of the region, supported by its growing role in rare-earth exploration and sustainable mining practices. Government-backed projects are advancing processing capabilities to reduce reliance on imports. Increasing focus on clean energy and battery materials is driving incremental demand. Canada’s resource base positions it as a strategic supplier within North America’s evolving ecosystem.

Europe Lanthanum Market Trends

Europe is projected to hold around 22% of the global lanthanum market in 2026, driven by strong regulatory alignment under the European Green Deal. The region is transitioning toward sustainable material use and circular economy models, with increasing investments in recycling and emission-reduction technologies. Growth is supported by expanding EV production and by integrating renewable energy. Regulatory frameworks such as REACH continue to shape production standards and material usage.

Germany Lanthanum Market Trends

Germany is estimated to account for approximately 30% of the regional market, driven by its leadership in automotive manufacturing and industrial innovation. The country is scaling EV production and investing in battery supply chains to reduce import dependency. Advanced manufacturing capabilities and strong policy support are accelerating lanthanum adoption. Germany remains a central hub for high-value applications across Europe.

U.K. Lanthanum Market Trends

The U.K. is expected to hold an estimated 18% share in 2026, supported by increasing investments in clean energy and EV infrastructure. Government initiatives promoting net-zero targets are driving demand for advanced materials, including lanthanum. The country is also focusing on recycling and sustainable sourcing strategies. This positions the U.K. as a key contributor to Europe’s evolving rare earth ecosystem.

Asia Pacific Lanthanum Market Trends

Asia Pacific is estimated to dominate with nearly 58% share of the global lanthanum market in 2026, supported by integrated supply chains and cost-efficient manufacturing. The region benefits from abundant rare earth resources and strong government support for industrial expansion. Increasing investments in battery manufacturing, refining capacity, and renewable energy projects are driving sustained demand. Asia Pacific remains the primary hub for both production and consumption.

China Lanthanum Market Trends

China is estimated to account for over 65% of the regional market in 2026, driven by its control over rare earth mining and processing. Government policies and export controls significantly influence global supply and pricing dynamics. The country continues to expand refining capacity and battery material production. Its dominance ensures a strong position across the entire lanthanum value chain.

Japan Lanthanum Market Trends

Japan holds an estimated 12% share within the region in 2026, supported by its leadership in electronics and battery technologies. The country is investing in advanced material innovation and recycling capabilities to reduce supply risks. Strong demand from the automotive and consumer electronics sectors is driving lanthanum usage. Japan’s focus on high-performance applications positions it as a key value-driven market.

Competitive Landscape

The global lanthanum market is moderately consolidated, with key players such as China Northern Rare Earth Group, Lynas Rare Earths Ltd., MP Materials Corp., and Iluka Resources controlling a significant share of supply. These companies leverage vertically integrated operations across mining and processing to ensure cost efficiency and supply stability. Their focus remains on capacity expansion and advanced refining technologies. Long-term supply agreements further strengthen their market position.

Regional players are targeting niche applications and recycling technologies to capture additional value. High entry barriers, including capital intensity and regulatory constraints, limit new competition. However, supply diversification efforts are enabling new projects in North America and Europe. Consolidation is expected to rise as firms pursue partnerships and acquisitions to expand reach.

Key Industry Developments:

- In April 2026, USA Rare Earth announced a US$2.8 billion acquisition of Serra Verde, securing Brazil’s Pela Ema mine and advancing a fully integrated “mine-to-magnet” supply chain. This move is expected to strengthen Western supply independence and directly challenge China’s dominance in critical rare earth materials.

- In March 2026, Lynas entered a US$6 million agreement with the U.S. Department of Defense to supply rare earth oxides for defense applications. The deal reinforces non-China supply chains and highlights growing government focus on securing critical materials for national security.

Companies Covered in Lanthanum Market

- Lynas Rare Earths Ltd.

- MP Materials Corp.

- Iluka Resources Limited

- Arafura Rare Earths Limited

- Avalon Advanced Materials Inc.

- Neo Performance Materials Inc.

- Indian Rare Earths Limited

- Shin-Etsu Chemical Co., Ltd.

- Solvay S.A.

- Alkane Resources Ltd.

- Great Western Minerals Group

- Jiangxi Tungsten Industry Group

- China Northern Rare Earth Group

Frequently Asked Questions

The global lanthanum market is projected to reach US$77.1 million in 2026.

Rising demand from petroleum refining catalysts, EV battery expansion, and water treatment applications drives the market.

The market is expected to grow at a CAGR of 6.6% from 2026 to 2033.

Growth opportunities stem from EV adoption, energy storage expansion, and increasing investments in rare earth supply chains.

China Northern Rare Earth Group, Lynas Rare Earths Ltd., MP Materials Corp., and Iluka Resources are key players.