- Metals & Minerals

- Nickel Mining Market

Nickel Mining Market Size, Share, and Growth Forecast, 2026 - 2033

Nickel Mining Market by Mining Technique (Open Cast Mining, Underground Mining, Others), Ore Deposit Type (Laterite Deposit, Sulfide Deposit, Others), Application, and Regional Analysis for 2026 - 2033

Nickel Mining Market Size and Trends Analysis

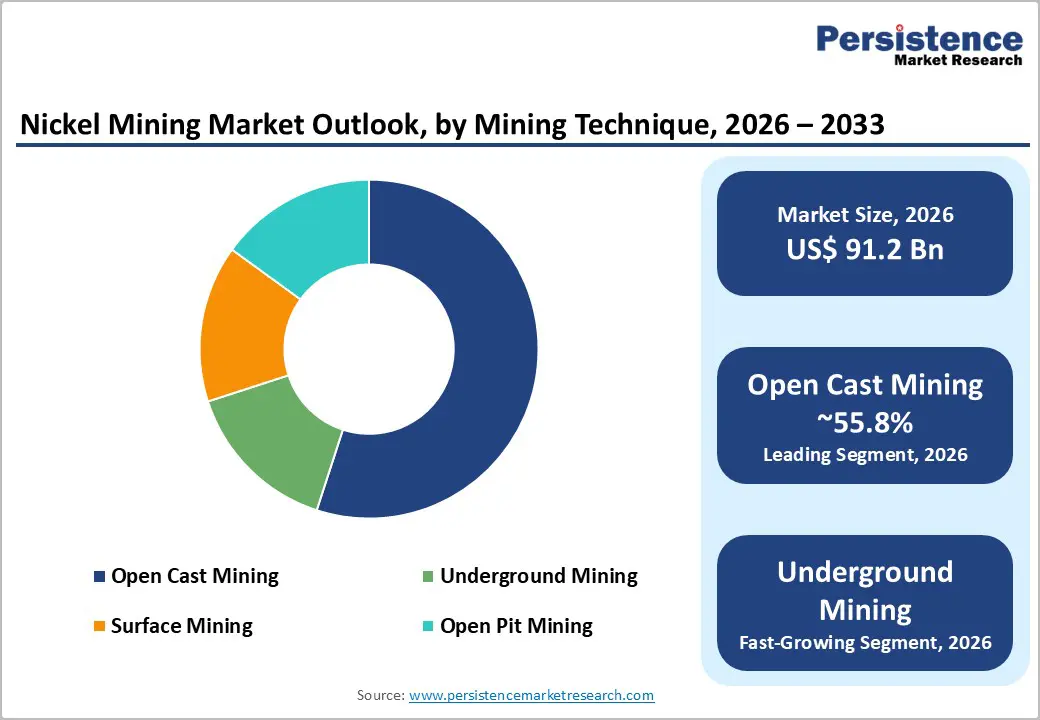

The global nickel mining market size is likely to be valued at US$91.2 billion in 2026 and is expected to reach US$111.4 billion by 2033, growing at a CAGR of 2.9% between 2026 and 2033, driven by sustained stainless steel demand and accelerating adoption in the battery sector.

Rising electrification trends, energy storage deployment, and industrial infrastructure expansion are reinforcing nickel consumption, while supply concentration and pricing pressures continue to influence investment strategies and production decisions.

Key Industry Highlights:

- Leading Region: Asia Pacific is projected to account for 59.7% of market share, driven by Indonesia’s global production and strong integration of mining and processing operations.

- Fastest-growing Region: North America is expected to be the fastest-growing region, supported by policy-driven investments and supply chain localization initiatives.

- Investment Plans: Global investments are increasingly focused on battery-grade nickel and downstream processing, with significant funding initiatives such as US$ 500 million allocated in the United States and large-scale exploration programs in India covering 1,200 projects through 2030-31.

- Dominant Mining Technique: Open-cast mining leads the market with an anticipated 55.8% share, supported by the dominance of laterite deposits and cost-efficient large-scale surface mining operations.

- Leading Application: Stainless steel remains the primary application, accounting for 66.3% of total nickel consumption, ensuring stable baseline demand across industrial sectors.

DRO Analysis

Driver - Stainless Steel Demand Remains the Volume Anchor, While Batteries Add a Faster-Growing Premium Layer

Nickel continues to play a critical role in stainless steel production, which accounts for the majority of global consumption. This segment ensures stable baseline demand due to its widespread use in construction, transportation, heavy machinery, and consumer goods manufacturing. Nickel demand from battery applications is also expanding rapidly, driven by electric vehicle (EV) adoption and grid-scale energy storage systems. Demand growth of 6-8% in 2024 highlights this dual demand structure.

From a business perspective, this creates a two-tier market dynamic. Bulk nickel producers benefit from consistent stainless steel demand, while suppliers capable of producing high-purity Class 1 nickel gain access to premium pricing in battery supply chains. Companies integrating mining with refining and chemical processing are better positioned to secure long-term supply contracts and improve margin stability.

Policy Support for Critical Minerals Is Accelerating Investment in Mining and Processing

Government policies across major economies are actively reshaping the nickel mining landscape by prioritizing supply chain security and domestic production. Regulatory frameworks now emphasize increased extraction, localized processing, and recycling of critical minerals. For instance, policy targets in developed markets aim to achieve 10% domestic extraction, 40% processing capacity, and 25% recycling rates by 2030, while limiting dependence on single-country imports.

In parallel, public funding initiatives, such as US$500 million allocated for critical mineral processing and battery manufacturing in the U.S. and India’s large-scale exploration program covering 1,200 projects through 2030-31, are accelerating project pipelines. These developments are reducing entry barriers, improving financing access, and encouraging vertical integration. The result is increased investment in HPAL (High-Pressure Acid Leach) facilities, refining infrastructure, and recycling technologies, strengthening long-term supply security.

Restraint - Oversupply, Price Volatility, and Geographic Concentration Impact Profitability

Despite strong demand fundamentals, the nickel mining market faces structural challenges from oversupply and price volatility. Indonesia accounts for approximately 60% of global nickel production, creating significant supply concentration. This has contributed to downward price pressure, with nickel prices declining 2% in early 2025 and projected to fall further before a marginal recovery.

Global mine production reached approximately 3.7 million tons in 2024, while several regions, including Australia and New Caledonia, experienced output reductions due to unfavorable economics. These conditions compress margins, delay capital investment, and increase the likelihood of mine closures, particularly for higher-cost producers. The financial risk includes extended project payback periods and constrained access to funding, especially for greenfield developments outside dominant production hubs.

Opportunity - Expansion of Battery-Grade Nickel and Downstream Processing Capabilities

The transition toward electrification is creating significant opportunities in battery-grade nickel production, particularly in nickel sulfate and intermediate products derived from HPAL and matte conversion processes. These materials are essential for lithium-ion battery chemistries used in EVs and energy storage systems.

Companies investing in downstream processing capabilities can capture higher margins compared to raw ore suppliers. Vertical integration, from mining to chemical processing, enhances supply chain control and reduces exposure to commodity price fluctuations. This trend is further supported by increasing demand for low-carbon and traceable nickel, which is becoming a key procurement criterion for automotive and battery manufacturers.

Regional Supply Diversification and Strategic Resource Development

Efforts to diversify global nickel supply chains are creating long-term opportunities in North America and Europe. These regions are investing in domestic mining, refining, and recycling infrastructure to reduce dependence on imports. Canada alone has 56 active mines, 31 processing facilities, and 171 advanced critical mineral projects, indicating a strong pipeline for future nickel supply.

Similarly, Europe’s regulatory push toward resource independence is driving investment in environmentally compliant mining operations. Projects that meet stringent sustainability standards are gaining strategic importance, particularly as industries prioritize responsible sourcing. This shift is expected to support the development of new mining hubs and create opportunities for companies operating in politically stable and resource-rich regions.

Category-wise Analysis

Mining Technique Insights

Open-cast mining is expected to lead, maintaining a dominant share of around 55.8% in 2026, supported by the widespread availability of near-surface laterite deposits. Open-pit mining contributes approximately 80% of the total production, reflecting strong cost efficiency and operational scalability. These techniques are extensively deployed in Indonesia and the Philippines, where integrated industrial parks, such as those developed by Tsingshan Holding Group in Indonesia, combine mining with downstream processing.

In Australia, large-scale laterite operations such as those linked to BHP have historically relied on open-cut methods for bulk extraction. Surface mining enables faster project commissioning, lower stripping ratios in favorable geology, and reduced capital intensity, making it the preferred approach for high-volume production.

Underground mining is likely to be the fastest-growing segment, driven by increasing demand for high-grade sulfide deposits used in premium nickel applications. These deposits, while deeper and more technically complex, produce higher-purity Class 1 nickel, essential for battery-grade materials and superalloys. For example, Vale S.A. operates underground nickel mines in Canada that supply high-grade feedstock for refining, while Nornickel leverages underground mining in Siberia to extract sulfide ores with significant nickel content.

Advances in automation, digital mine planning, and ventilation systems are improving cost efficiency in underground operations. This segment’s growth reflects a strategic shift toward quality over volume, enabling access to higher-margin markets and long-term resource optimization.

Application Insights

Stainless steel is expected to be the largest application segment and is anticipated to account for 66.3% of total nickel consumption in 2026, driven by stable demand across construction, transportation, and industrial manufacturing. Major producers such as Tsingshan Holding Group and Jinchuan Group play a central role in supplying nickel units for stainless steel production, particularly in Asia Pacific. The material’s corrosion resistance, strength, and cost-efficiency ensure consistent demand, making it the backbone of nickel consumption. This segment provides a stable revenue base for mining companies, especially during fluctuations in emerging applications such as batteries.

Batteries are anticipated to be the fastest-growing application, driven by the rapid expansion of electric vehicles and renewable energy storage systems. Companies such as Huayou Cobalt and Sumitomo Metal Mining Co., Ltd. are actively investing in nickel sulfate production and battery material supply chains. Nickel-rich chemistries, such as NMC (nickel-manganese-cobalt), are increasingly preferred for their higher energy density and efficiency. This transition is repositioning nickel as a critical energy-transition material.

Producers that can deliver high-purity, low-carbon nickel are gaining a competitive edge through premium pricing, strategic partnerships, and long-term supply agreements with battery and automotive manufacturers.

Regional Insights

North America Nickel Mining Market Trends

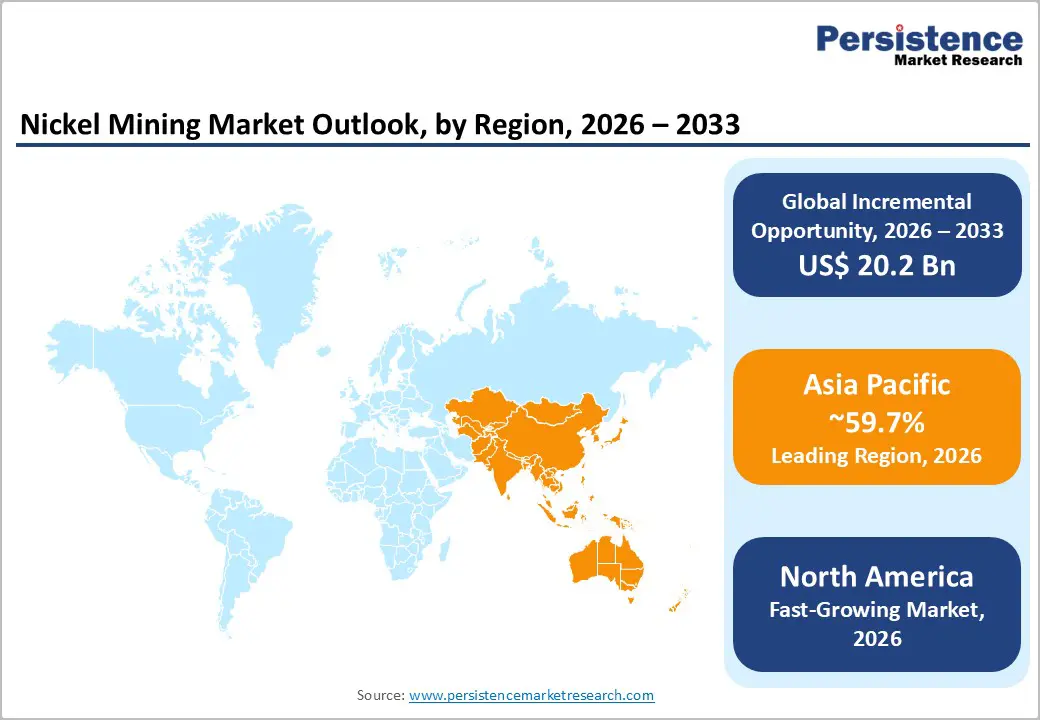

North America is emerging as the fastest-growing region, due to strong policy support and increasing investment in critical mineral supply chains.

U.S. Nickel Mining Market Trends

The U.S. is expected to lead on regulatory momentum. Federal initiatives focused on domestic sourcing and processing are accelerating project development and reducing reliance on imports. For example, Talon Metals Corp., in partnership with Tesla, Inc., is advancing the Tamarack nickel project in Minnesota to supply battery-grade nickel for EV production. This development reflects a broader shift toward localized supply chains and long-term offtake agreements between miners and end-users.

The U.S. is also supporting downstream processing through funding programs, encouraging integrated operations that combine mining, refining, and battery material production. These efforts are strengthening supply chain resilience and positioning the country as a strategic hub for energy-transition minerals.

Canada Nickel Mining Market Trends

Canada is expected to play a central role in regional growth, due to its abundant mineral reserves and advanced project pipeline. The country has a well-established mining ecosystem and is actively expanding its nickel production capacity. For instance, Canada Nickel Company is developing the Crawford Nickel Sulfide Project in Ontario, which is positioned as one of the largest undeveloped nickel resources globally and emphasizes low-carbon production.

Similarly, Vale S.A. continues to invest in its Sudbury and Voisey’s Bay operations, including underground expansions that enhance high-grade nickel output. These developments support the region’s focus on sustainable mining and battery-grade material production. Investment trends indicate a shift toward integrated mining and refining operations, reinforcing North America’s role in the global nickel supply chain.

Europe Nickel Mining Market Trends

Europe’s nickel mining market is shaped by regulatory initiatives aimed at reducing import dependence and strengthening domestic supply chains, with key economies such as Germany, the U.K., France, and Spain driving demand. While primary nickel mining is limited, the region is actively investing in refining, recycling, and downstream processing. For example, Eramet has continued to modernize its nickel operations and processing capabilities, aligning with European sustainability standards and supporting supply diversification.

U.K. Nickel Mining Market Trends

In the U.K., projects led by Anglo American, including its broader critical mineral strategy, are contributing to supply chain resilience through portfolio optimization and strategic asset allocation. Meanwhile, Germany’s automotive sector is driving demand for battery-grade nickel, encouraging partnerships with global suppliers to secure long-term material access.

The region’s focus on circular economy models is evident through increased investment in recycling technologies and secondary nickel production. Regulatory harmonization across the European Union is encouraging environmentally compliant mining and processing projects. Although Europe has limited primary resources compared to Asia Pacific, its strong industrial base, technological expertise, and sustainability-driven policies are creating opportunities for innovation and strategic partnerships.

Asia Pacific Nickel Mining Market Trends

Asia Pacific is expected to lead the global nickel mining market, accounting for 59.7% of market share in 2026 and growing at a CAGR of 4.2%.

Indonesia Nickel Mining Market Trends

Indonesia is the dominant producer, contributing approximately 59% of the global supply. The country’s leadership is reinforced by large-scale integrated industrial parks that combine mining, smelting, and refining. For example, Tsingshan Holding Group has developed major nickel-processing hubs in Indonesia, producing nickel pig iron and battery materials. Similarly, PT Vale Indonesia has expanded operations with new processing facilities such as the Bahodopi project, strengthening downstream capacity. These developments have transformed Indonesia into a global center for nickel production and processing, driving cost efficiencies and supply chain integration.

China Nickel Mining Market Trends

China plays a critical role as both a major consumer and processor of nickel, particularly in stainless steel and battery materials. Companies such as Huayou Cobalt are actively investing in Indonesia-based nickel processing projects to secure raw material supply for battery production. China’s dominance in refining and chemical processing enables it to control a significant portion of the value chain, influencing global pricing and supply dynamics. The country’s continued investment in EV manufacturing and energy storage further strengthens demand for nickel.

Japan Nickel Mining Market Trends

Japan contributes through advanced refining capabilities and technological expertise in high-purity nickel production. Sumitomo Metal Mining Co., Ltd. is a key player, producing electrolytic nickel used in batteries and specialty alloys. The company’s focus on sustainable and efficient refining processes supports Japan’s role in supplying premium-grade nickel to global markets. Japan’s strategic partnerships with Southeast Asian producers ensure stable access to raw materials while maintaining high-quality standards.

The region benefits from cost advantages, abundant resources, and strong government support, making it the central hub for global nickel production and processing. Integrated developments across Indonesia, China, and ASEAN are reshaping the global supply chain by combining raw material extraction with downstream value addition, reinforcing Asia Pacific’s leadership position.

Competitive Landscape

The global nickel mining market exhibits moderate concentration at the country level but fragmentation at the company level. A few countries dominate global production and refining, while numerous companies operate across different stages of the value chain. Integrated players with mining, processing, and refining capabilities hold a competitive advantage due to cost efficiencies and supply chain control.

Leading companies are focusing on vertical integration, cost optimization, and geographic diversification. Investment in downstream processing, low-carbon production technologies, and long-term supply agreements with battery manufacturers are key differentiators. Strategic partnerships and acquisitions are increasingly used to secure resource access and expand global presence.

Key Industry Developments:

- In September 2025, Vale S.A. advanced its nickel production strategy by commissioning Furnace 2 at its Onça Puma operation in Brazil, enhancing processing capacity and supporting downstream integration into higher-value nickel products used in stainless steel and battery applications.

Companies Covered in Nickel Mining Market

- Vale S.A.

- Nornickel

- Tsingshan Holding Group

- Glencore

- BHP

- Eramet

- MMG Limited

- PT Vale Indonesia

- Nickel Industries Limited

- Sumitomo Metal Mining Co., Ltd.

- Sherritt International

- Jinchuan Group

- Huayou Cobalt

- First Quantum Minerals

- South32

- Anglo American

Frequently Asked Questions

The global nickel mining market is valued at US$91.2 billion in 2026.

The nickel mining market is projected to reach US$111.4 billion by 2033.

Key trends include the rapid expansion of battery-grade nickel demand, increasing investment in downstream processing (HPAL and nickel sulfate), growing regional supply chain diversification, and a shift toward low-carbon and sustainable mining practices.

The stainless steel segment leads the market, accounting for 66.3% of market share, driven by consistent demand across industrial and infrastructure sectors.

The nickel mining market is expected to grow at a CAGR of 2.9% between 2026 and 2033.

Major players include Vale S.A., Nornickel, Tsingshan Holding Group, Glencore, and BHP.