- Clothing, Footwear, & Accessories

- Men's Underwear Market

Men's Underwear Market Size, Share, and Growth Forecast 2026 – 2033

Men's Underwear Market by Category (Regular Brief, Boxer Brief, Boxer Shorts, Trunks, Thongs), Fabric Type (Cotton, Polyester, Nylon, Rayon incl. Modal, Spandex), Size (Extra Small, Small, Medium, Large, Extra Large, Double XL, Triple XL), Distribution Channel (Online Retail, Offline Retail), and Regional Analysis, 2026–2033

Global Men's Underwear Market Size and Trend Analysis

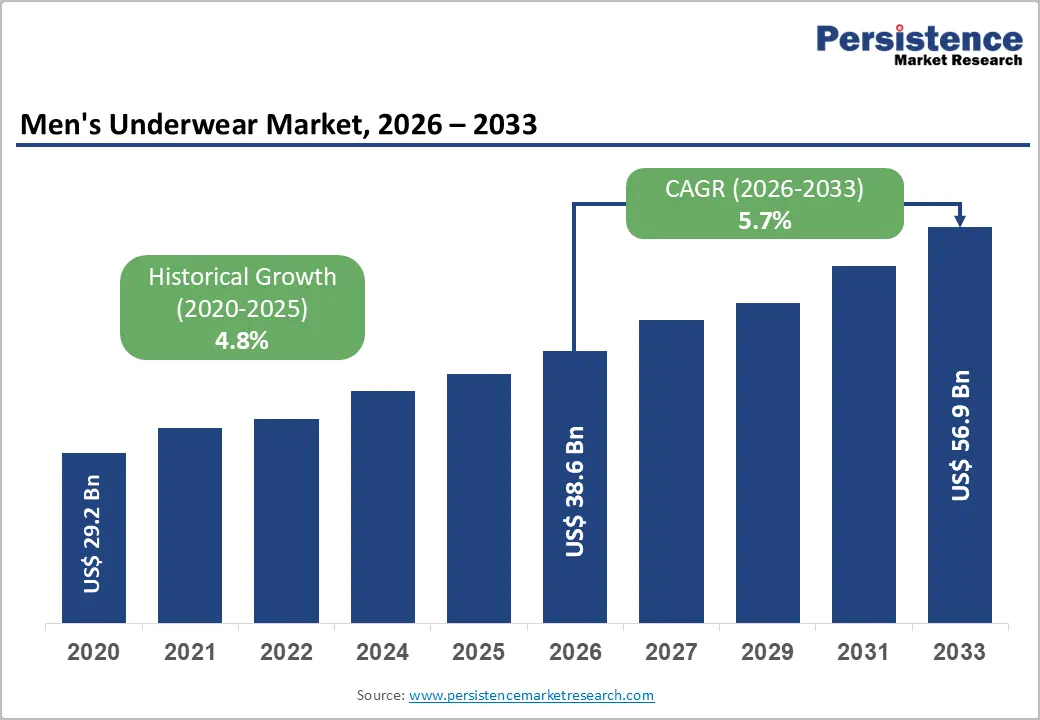

The global men's underwear market size is expected to be valued at US$ 38.7 billion in 2026 and projected to reach US$ 57.0 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033. This sustained growth is propelled by the convergence of evolving male grooming consciousness, premiumization of everyday essentials, and the structural shift toward e-commerce accessibility. The proliferation of performance-oriented fabric technologies such as moisture-wicking polyester blends, anti-microbial treatments, and four-way stretch spandex has elevated consumer expectations beyond basic function.

Additionally, the broadening of size-inclusive product lines, direct-to-consumer brand strategies, and heightened demand from Asia-Pacific's expanding middle-income demographic are collectively reinforcing multi-year demand momentum across the global market.

Key Industry Highlights:

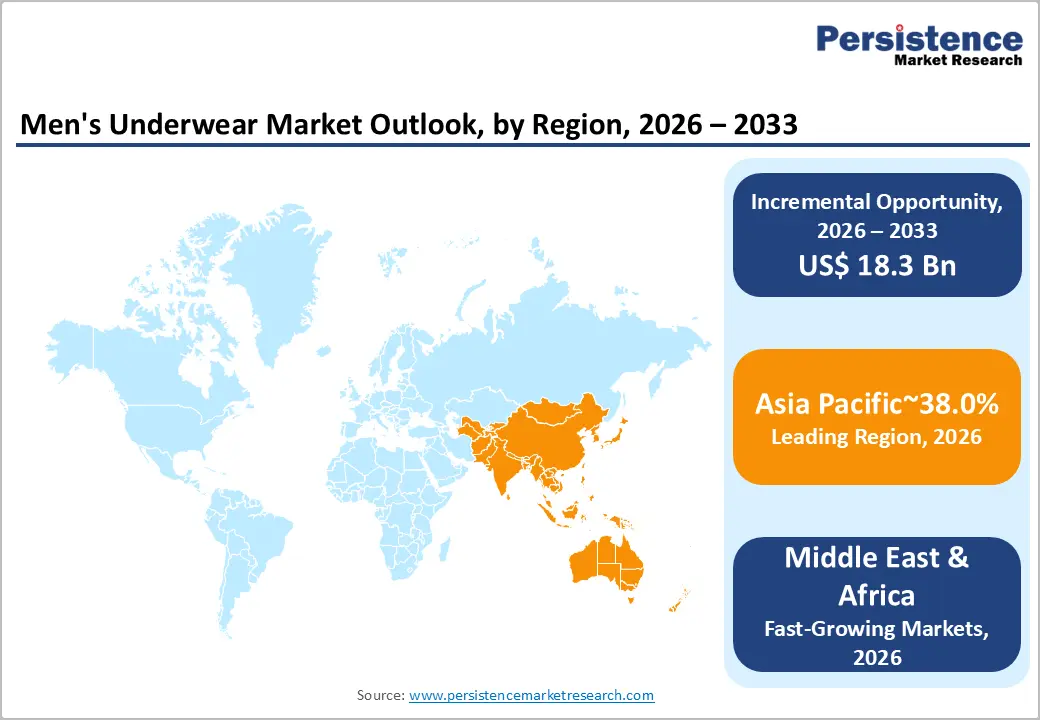

- Leading Region: Asia Pacific dominates the global men's underwear market with a 38% share in 2025, driven by China's US$ 4.4 billion market scale, India's rapid premiumization, and e-commerce-led distribution expansion across tier-2 and tier-3 cities.

- Fast-Growing Market: South Asia/India: India is the fastest-growing major national market in the men's underwear segment, propelled by a demographic dividend of 600 million+ youth consumers, rising organised retail penetration, and domestic brand premiumization.

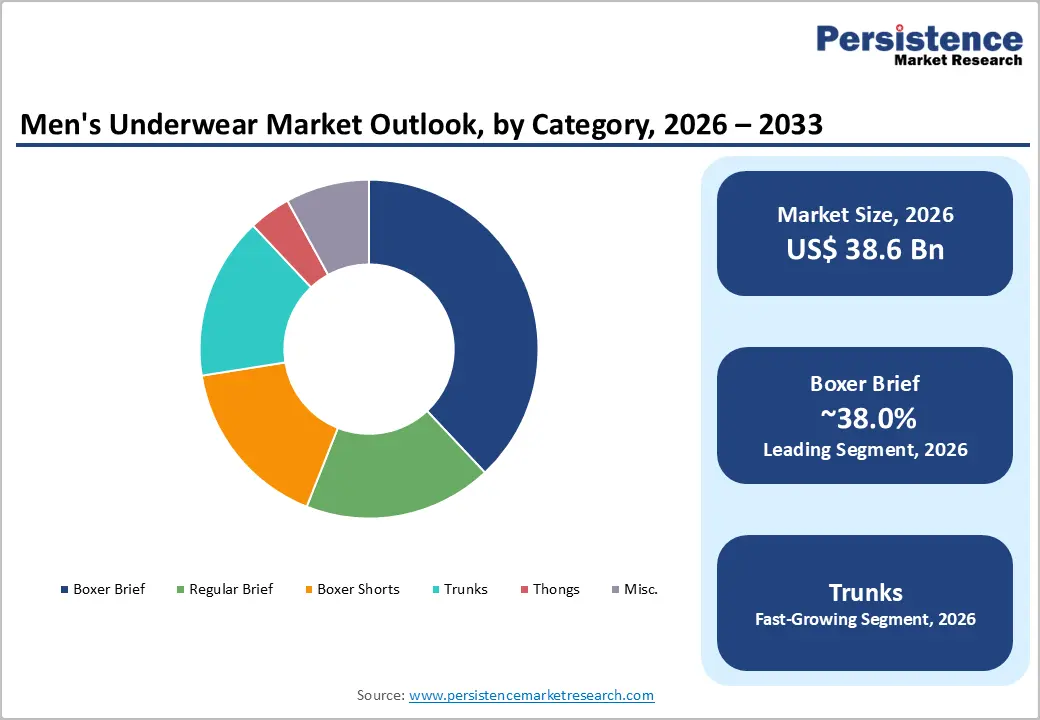

- Leading Category: Boxer briefs lead the global men's underwear market with a 38% product category share in 2025, supported by universal fit appeal, brand-premium positioning by Calvin Klein and SAXX, and proliferation of performance-fabric variants.

- Fast-Growing Category: Trunks are the fast-growing product category (5% CAGR, 2026–2033), driven by fashion-conscious male consumers in Europe and Asia Pacific seeking a streamlined silhouette with everyday comfort performance.

- Key Opportunity: Brands targeting eco-certified fabrics (LENZING™ ECOVERO™, organic cotton) and extended size ranges (XS–6XL) are positioned to capture a disproportionate share of global volume growth through 2033.

DRO Analysis

Drivers - Shift Toward Functional and Performance-Driven Innerwear

A fundamental redefinition of men's innerwear from a commodity to a performance product is reshaping demand globally. According to the Textile Exchange's Preferred Fibre & Materials Market Report, synthetic performance fabrics, particularly polyester and spandex blends, have seen a steady uptick in adoption across activewear and innerwear categories.

Brands such as SAXX with its patented BallPark Pouch™ and Three-D Fit™ technology, and Calvin Klein with micro-stretch and micro-mesh innovation, are commanding premium price points by translating athletic performance standards into daily innerwear. This functional innovation is attracting a new generation of male consumers who treat underwear as a wellness product, not merely a wardrobe basic, directly widening the addressable premium segment.

E-Commerce Penetration and Direct-to-Consumer Channel Expansion

The digital transformation of retail has been particularly impactful in the men's innerwear category, where traditionally low purchase involvement is now being disrupted by subscription models, algorithm-driven personalisation, and influencer-led discovery.

The U.S. Census Bureau reported that e-commerce sales in the apparel and accessories segment grew by over 15% year-on-year in recent periods, with men's basics among the highest repeat-purchase SKUs online. Brands like MeUndies, Tommy John, and MANSCAPED have built scalable DTC operations leveraging digital advertising, influencer partnerships, and loyalty subscription programs. This channel unlocks global reach for niche brands without traditional retail gatekeeping, structurally compressing costs while widening consumer access.

Restraints - Raw Material Price Volatility and Supply Chain Vulnerability

Cotton, the dominant fabric in men's underwear, is subject to significant price fluctuations driven by climatic disruptions, geopolitical supply constraints, and global commodity speculation. The International Cotton Advisory Committee (ICAC) has consistently noted that cotton price volatility creates margin compression for underwear manufacturers, particularly for mid-tier brands with limited hedging capacity.

The COVID-19 pandemic further exposed the fragility of extended supply chains, and post-pandemic reshoring pressures continue to add to production cost burdens. These structural cost pressures inhibit the ability of manufacturers to maintain competitive retail pricing without sacrificing margin.

Tariff Disparities and Trade Policy Uncertainty in Key Markets

Trade policy volatility represents a structural headwind for globally sourced underwear brands. A February 2025 analysis covered by CNN and based on U.S. Government / Progressive Policy Institute data revealed that U.S. tariff policy imposes an average duty of 11.5% on men's underwear imports, adding approximately $0.75 per pair at the retail level. For brands sourcing predominantly from Southeast Asia or China, such tariff structures constrain pricing strategy and erode competitiveness against domestically manufactured alternatives, creating ongoing uncertainty in cross-border supply chain planning.

Opportunities - Sustainable and Eco-Certified Underwear Lines as a Premium Growth Vector

Sustainability has transitioned from a differentiator to a baseline expectation among a growing cohort of male consumers aged 25–44, who increasingly scrutinise supply chain ethics and environmental credentials before purchase. The April 2023 launch by Fruit of the Loom of its Fruitful Threads™ collection featuring LENZING™ ECOVERO™ certified fibres with up to 50% lower CO? emissions illustrates the commercial viability of eco-positioned underwear at accessible retail price points (priced at US$ 19.99 for three-packs through Walmart and Amazon).

In September 2023, Step One's U.S. market entry with bamboo viscose fabric and SA8000-certified ethical manufacturing signalled a viable market for sustainably positioned entrants, particularly within the growing D2C channel.

Size Inclusivity and the Underserved Plus-Size Segment as a Demand Frontier

The men's underwear category has historically underserved plus-size demographics, creating a substantial untapped opportunity for brands willing to invest in extended size ranges. The Centers for Disease Control and Prevention (CDC) reports that over 40% of U.S. adult males are classified as obese, yet fewer than 20% of mass-market underwear SKUs extend beyond XXL. Brands such as Step One (sizes S to 6XL), Skims (sizes XS to 5X), and Neude have deliberately targeted this gap with specialised fits and targeted messaging.

As demographic diversity widens and body-positive retail strategies become mainstream, size-inclusive assortments are projected to command a disproportionate share of volume growth in the Trunks and Boxer Brief segments through 2033.

Category-wise Analysis

Product Category Insights

Boxer briefs dominate the global men's underwear market with an estimated 38% share in 2026, outpacing all other product categories by a significant margin. This leadership stems from the style's functional hybrid design combining the supportive fit of briefs with the leg coverage of boxers, making it the preferred choice across age groups and activity levels.

The widespread adoption by premium brands such as Calvin Klein, Tommy Hilfiger, and Under Armour has elevated boxer briefs to a fashion-forward staple. The proliferation of performance variants, including seamless constructions, moisture-wicking blends, and ergonomic pouch designs, has further cemented its appeal among fitness-conscious and fashion-aware male consumers globally, making it the highest-volume and highest-revenue product segment in the market.

Fabric Type Insights

Cotton retains its position as the leading fabric type in the men's underwear market, commanding an estimated 45% market share in 2026. Its dominance is rooted in its universal consumer trust, breathability, hypoallergenic properties, and price accessibility.

The International Cotton Advisory Committee (ICAC) notes that cotton remains the most widely consumed natural fiber globally, and its stronghold in innerwear reflects deeply entrenched purchase behavior across both developed and emerging markets. Combed and ring-spun cotton variants are commanding premiums in the mid-market, while blended cotton-spandex constructions are gaining traction for providing natural fiber comfort with added stretch. Private-label brands at mass-market retailers continue to anchor cotton as the volume backbone of global men's underwear sales.

Distribution Channel Insights

Offline Retail remains the dominant distribution channel for men's underwear, holding an estimated 62% market share in 2025. Supermarkets, hypermarkets, department stores, and speciality apparel retailers continue to generate the majority of category sales globally, particularly in Asia-Pacific and Latin America, where e-commerce infrastructure is still developing.

The offline channel benefits from tactile trial preferences among male shoppers for fit-sensitive products such as underwear. Retailers such as Walmart, Target, and department store formats continue to benefit from high footfall-to-conversion ratios in the basics category. However, Online Retail is the fastest-growing distribution channel, with digitally native brands and marketplaces rapidly capturing share through subscriptions, bundled multi-pack offers, and seamless returns, signalling a structural channel shift by 2033.

Regional Insights

North America Men's Underwear Market Trends and Insights

North America accounts for approximately 27.0% of the global men's underwear market in 2025, underpinned by high per-capita apparel expenditure, deep penetration of premium and lifestyle underwear brands, and a structurally advanced e-commerce ecosystem.

The region is distinguished by its concentration of innovation-first DTC brands, growing body-inclusivity mandates from major retailers, and a robust pipeline of product launches targeting performance, sustainability, and fashion-forward aesthetics. Regulatory attention to gender-based tariff disparities, with men's underwear attracting an average 11.5% duty versus 15.5% for women's, continues to influence competitive import dynamics across the region.

U.S. Men's Underwear Market Size

The U.S. men's underwear market is valued at approximately US$ 8.7 billion in 2025, making it the single largest national market globally. This scale is driven by the coexistence of mass-market volume leaders Hanesbrands and Fruit of the Loom alongside a thriving premium and DTC ecosystem featuring Calvin Klein, SAXX, Tommy John, and new entrants such as Skims and Knix. The PVH Corp.–Nike licensing agreement, announced in May 2019, further signals institutional confidence in the U.S. market's premium segment scale. Consumer spending resilience in the basics category, combined with subscription commerce penetration, positions the U.S. for continued outperformance against broader apparel category benchmarks.

Europe Men's Underwear Market Trends and Insights

Europe holds a 20% share of the global men's underwear market in 2025, characterised by a strong heritage of premium and designer innerwear brands, high consumer sensitivity to fabric quality and country of origin, and a well-developed omni-channel retail infrastructure.

The region's sustainability regulatory environment, driven by the EU Green Deal and incoming Extended Producer Responsibility (EPR) frameworks for textiles, is accelerating the adoption of eco-certified fabrics and circular product design among European underwear manufacturers, especially in Germany, France, and the Nordics.

Germany Men's Underwear Market Size

Germany's men's underwear market is valued at approximately US$ 1,314.0 million in 2025, making it the largest national market in Europe. Germany's leadership reflects its high consumer spending power on apparel basics, dominant domestic brands such as Schiesser and mey, and strong retail penetration through speciality chains and department stores like Karstadt.

German consumers demonstrate a strong preference for certified organic cotton and Made-in-Europe quality credentials, driving consistent mid-to-premium price tier purchases. The country's regulatory alignment with EU textile sustainability mandates is prompting leading brands to reformulate their fabric sourcing as a competitive differentiator that supports domestic brand premiumization.

U.K. Men's Underwear Market Size

The U.K. men's underwear market is valued at approximately US$ 1,168.0 million in 2025. The market is shaped by a dual-track consumer base: a value-conscious segment serviced by Marks & Spencer and Primark, and a premium-seeking cohort increasingly engaging with DTC brands such as Calvin Klein and Boux Avenue via digital channels.

Post-Brexit import dynamics have modestly shifted sourcing patterns for U.K. retailers, making domestic and nearshore supply chains more attractive. The U.K.'s robust e-commerce penetration, among the highest in Western Europe, is an enabling factor for DTC underwear brand growth, with platforms like ASOS and Next serving as key digital storefronts for premium underwear labels.

Asia Pacific Men's Underwear Market Trends and Insights

Asia Pacific is the dominant regional market with a 38% share of the global men's underwear market in 2026 underpinned by its sheer population scale, a rapidly expanding organised retail footprint, and the structural premiumization of men's fashion in economies such as China, South Korea, and Japan.

China alone commands the largest sub-regional volume, with domestic brands competing aggressively against international players on both price and product innovation. Across the region, e-commerce platforms such as Alibaba's Tmall, JD.com, and Shopee are central to underwear distribution, enabling international and private-label brands to reach previously inaccessible rural and tier-3 city consumers.

China Men's Underwear Market Size

China's men's underwear market is valued at approximately US$ 4.4 billion in 2025, representing the largest single national market in the Asia Pacific. Growth is powered by a structural shift from unbranded commodity products to branded and semi-premium innerwear, driven by younger male consumers who are increasingly brand literate and digitally engaged.

Domestic brands such as Bosideng and Toread compete directly with international brands on Tmall and JD.com. China's National Bureau of Statistics data confirms sustained growth in per-capita apparel expenditure among urban male demographics, with innerwear benefiting from 'self-gifting' and experiential retail trends that are driving premiumization at scale.

India Men's Underwear Market Size

India's men's underwear market is valued at approximately US$ 2.9 billion in 2025 and represents the fastest-growing major national market in the Asia Pacific. This trajectory is driven by a demographic dividend of over 600 million Indians under age 25, combined with the rapid formalisation of retail through Reliance Retail, D-Mart, and e-commerce platforms like Flipkart and Myntra.

Domestic brands such as Lux Industries, Dollar Industries, and Rupa & Company dominate the value segment, while Jockey International has captured a significant share in the premium tier. India's Textiles Ministry has identified innerwear as a strategic export segment under the national textile policy, further validating India's structural role in global men's underwear supply chains.

Competitive Landscape

The global men's underwear market exhibits a moderately consolidated structure at the premium tier, dominated by Hanesbrands Inc., PVH Corp. (Calvin Klein, Tommy Hilfiger), and Fruit of the Loom, while remaining highly fragmented at the value and mid-market tiers, particularly across Asia Pacific and Latin America. Market leaders are investing in sustainability certification, fabric technology IP, and DTC infrastructure to defend margins.

Challenger brands are differentiating through niche positioning, size inclusivity (Skims, Step One), ergonomic engineering (SAXX), and community-led marketing (MANSCAPED). Licensing partnerships such as PVH–Nike signal a trend of brand co-leveraging to access established consumer bases in adjacent market segments.

Key Developments:

- In Nov 2025, Knix launched its first men’s underwear line in North America, expanding beyond women’s lingerie with moisture-blocking “Pristine Pouch” technology, supported by nine-figure U.S. revenues and new U.S. retail/wholesale partnerships (e.g., Bloomingdale’s) to strengthen its position in the U.S. women’s lingerie & men’s underwear market.

- In January 2024, Calvin Klein (U.S.) launched its Spring 2024 men’s underwear collection, featuring refreshed classic designs with new logo treatments and innovative materials such as intense power, micro stretch, and micro mesh. The collection emphasises stylish, everyday comfort while maintaining minimalist essentials, reinforcing Calvin Klein’s position as a leading brand in the U.S. men’s underwear market and appealing to consumers seeking both fashion and functionality.

Global Men's Underwear Market - Key Insights & Details

|

Key Insights |

Details |

|

Historical Market Value (2020) |

US$ 29.2 Billion |

|

Current Market Value (2026) |

US$ 38.7 Billion |

|

Projected Market Value (2033) |

US$ 57.0 Billion |

|

CAGR (2026–2033) |

5.7% |

|

Leading Region |

Asia Pacific, 38% market share (2025) |

|

Dominant Category-1 |

Boxer Brief, ~38% market share (2025) |

|

Top-ranking Category-2 |

Cotton, ~45% market share (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 18.3 Billion |

Companies Covered in Men's Underwear Market

- PVH Corp.

- Hanesbrands Inc.

- Jockey International Inc.

- Berkshire Hathaway Inc.

- Adidas AG

- Nike Inc.

- Puma SE

- H&M Group

- Gildan Activewear Inc.

- Ralph Lauren Corporation

- HUGO BOSS AG

- Under Armour Inc.

- American Eagle Outfitters Inc.

- Delta Galil Industries Ltd.

- Fast Retailing Co., Ltd.

Frequently Asked Questions

The global men's underwear market is expected to be valued at US$ 38.7 billion in 2026, growing from US$ 29.2 billion recorded in 2020. The market is projected to reach US$ 57.0 billion by 2033, expanding at a CAGR of 5.7% during the forecast period.

The primary demand drivers include the shift toward functional and performance-driven innerwear fueled by ergonomic fabric technologies and brand premiumization alongside expanding e-commerce and DTC channel penetration. Sustainability certifications and size-inclusive product ranges are also structurally expanding the addressable consumer base.

Asia Pacific is the leading region, holding approximately 38% of the global men's underwear market share in 2025. China alone accounts for approximately US$ 4.4 billion in market value, driven by premiumization, digital retail expansion, and a young, brand-conscious male consumer base.

The most significant market opportunity lies in the convergence of sustainable material innovation and size-inclusive product design. Brands offering eco-certified fabrics (such as LENZING™ ECOVERO™ and organic cotton) alongside extended size ranges (XS through 6XL) are positioned to capture disproportionate growth through 2033, particularly via DTC and e-commerce channels.

Leading companies in the global men's underwear market include Hanesbrands Inc., PVH Corp. (Calvin Klein, Tommy Hilfiger), Fruit of the Loom, Jockey International, SAXX Underwear, Tommy John, MeUndies, MANSCAPED, Skims, Step One, Knix, Under Armour, Nike (via PVH licensing), Adidas, Lux Industries, Jockey India, Uniqlo (AIRISM), Gunze, Schiesser, and Eminence, among others.