- Medical Devices

- Anti-Embolism Stockings Market

Anti-Embolism Stockings Market Size, Share, and Growth Forecast, 2026 - 2033

Anti-Embolism Stockings Market by Product Type (Knee-High, Thigh-High, Waist-High), Material (Nylon, Spandex, Cotton), and Regional Analysis for 2026 - 2033

Anti-Embolism Stockings Market Size and Trends Analysis

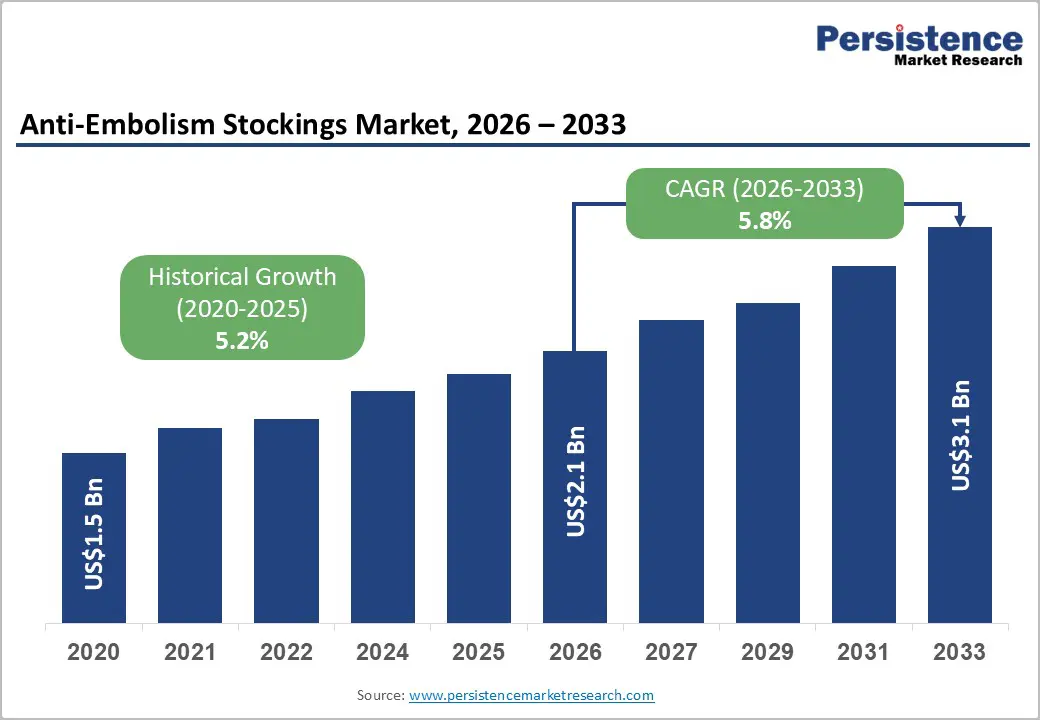

The global anti-embolism stockings market size is likely to be valued at US$2.1 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 5.8% during the forecast period from 2026 to 2033, driven by rising prevalence of venous disorders, increasing surgical procedures, and growing awareness regarding thrombosis prevention in hospitalized and immobile patients.

Anti-embolism stockings are widely used to improve blood circulation and reduce the risk of deep vein thrombosis (DVT) and pulmonary embolism (PE) during post-operative recovery and long-term care. The market is supported by the expanding geriatric population, increasing adoption of preventive healthcare practices, and advancements in compression fabric technologies that enhance patient comfort and compliance. Growing demand from hospitals, specialty clinics, and home healthcare settings is also contributing to overall market expansion.

Key Industry Highlights:

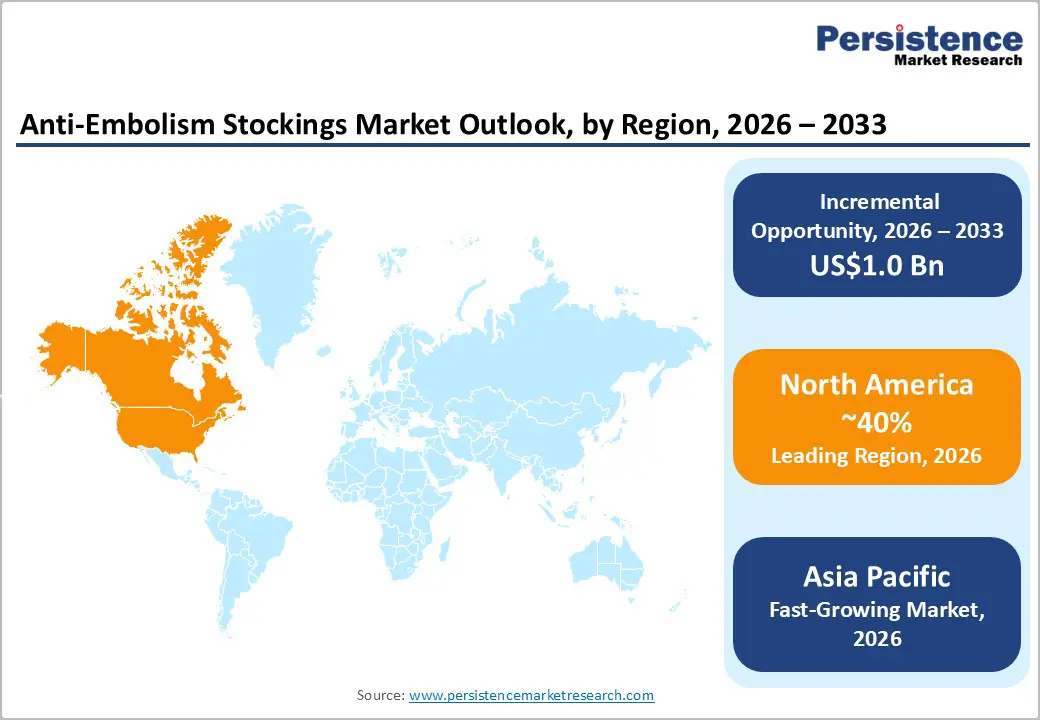

- Leading Region: North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong healthcare infrastructure, high surgical volumes, and increasing awareness regarding VTE prevention.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by expanding healthcare infrastructure, rising surgical procedures, and strong manufacturing capabilities.

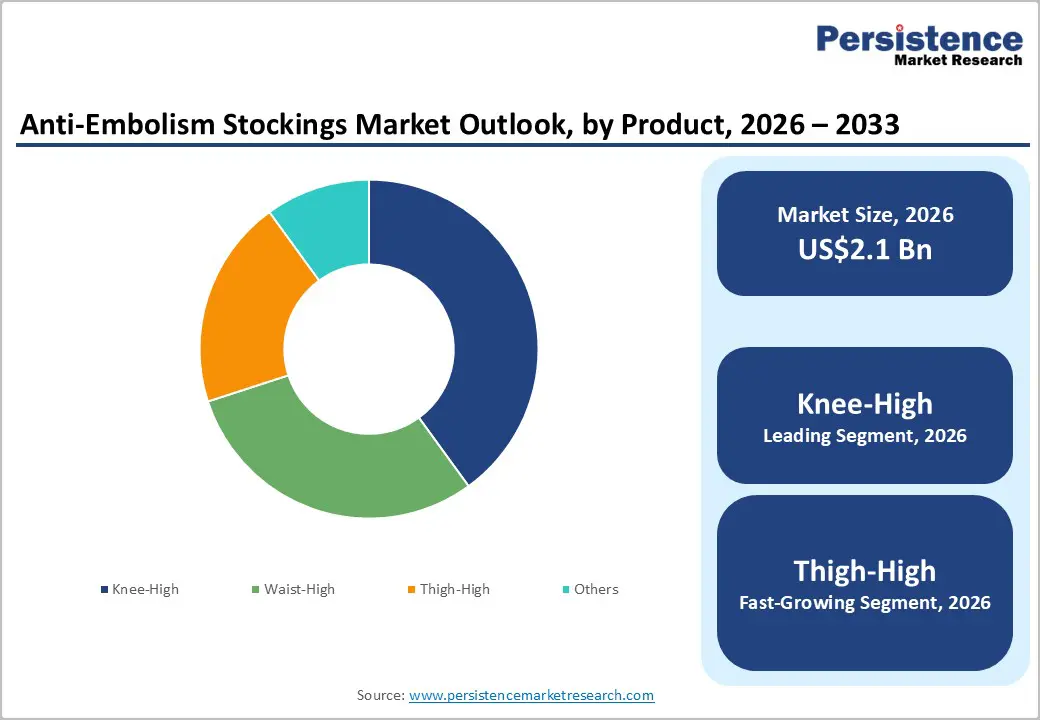

- Leading Product Type: Knee-high is projected to represent the leading product type in 2026, accounting for 55% of the revenue share, due to high patient compliance and widespread hospital usage.

- Leading Material Type: Nylon is anticipated to be the leading material type, accounting for over 50% of the revenue share in 2026, supported by its durability, elasticity, and cost-effectiveness.

- Key Opportunity: The key opportunity in the anti-embolism stockings market lies in the development of technologically advanced, comfortable, and cost-effective compression solutions for expanding home healthcare, post-operative care, and aging patient populations.

DRO Analysis

Driver - Rising Incidence of Venous Thromboembolism (VTE) and Surgical Procedures

Growing numbers of orthopedic, cardiovascular, bariatric, and general surgical procedures have increased the need for preventive compression therapy during hospitalization and post-operative recovery. Hospitals and healthcare providers are increasingly adopting anti-embolism stockings as part of standard thromboprophylaxis protocols to reduce complications associated with prolonged immobility.

Rising awareness among clinicians regarding preventive patient care and improved recovery outcomes has strengthened product adoption. Expanding healthcare infrastructure and higher hospital admission rates are supporting consistent market growth. The rapidly growing elderly population is another major factor accelerating the adoption of anti-embolism stockings across healthcare settings. Older adults are more susceptible to circulatory disorders, reduced mobility, and chronic diseases that increase the risk of venous thromboembolism.

Long-duration hospital stays, intensive care admissions, and rehabilitation treatments contribute to the requirement for compression-based preventive therapies. Increasing obesity rates and sedentary lifestyles are contributing to higher incidences of vascular complications among adults. Healthcare institutions are also emphasizing preventive measures to reduce readmission rates and improve patient outcomes.

Restraint - Patient Comfort and Adherence Challenges

Many patients experience issues such as excessive tightness, heat retention, skin irritation, itching, and difficulty wearing stockings for extended periods. Elderly individuals and patients with limited mobility often struggle with proper application and removal, reducing consistent product usage. Improper sizing and inadequate fitting also decrease therapeutic effectiveness and discourage patient compliance. In long-term care and homecare settings, discomfort-related concerns frequently result in irregular use of compression garments.

Limited patient awareness regarding the importance of compression therapy also affects adherence rates in several regions. Many patients discontinue usage after surgery or hospitalization due to inconvenience, discomfort, or insufficient understanding of long-term preventive benefits. Healthcare providers also face challenges in ensuring proper education about correct wearing duration, maintenance, and replacement schedules.

Opportunity - Technological Convergence and Product Innovation

Manufacturers are increasingly developing advanced compression garments using breathable fabrics, moisture-wicking materials, antimicrobial coatings, and ergonomic designs to improve patient comfort and usability. Innovations in textile engineering are enabling better pressure distribution and enhanced durability, supporting improved therapeutic outcomes.

Companies are also focusing on lightweight and skin-friendly materials to address long-standing comfort concerns among patients. Rising investments in healthcare innovation and increasing demand for personalized medical products are encouraging the development of next-generation compression solutions. The growing integration of smart healthcare technologies is expanding future opportunities within the anti-embolism stockings market.

Emerging developments include smart compression stockings equipped with sensors capable of monitoring blood circulation, pressure levels, and patient mobility in real time. Such technologies can support remote patient monitoring and improve adherence management in homecare environments. Increasing digitalization in healthcare systems and rising telehealth adoption are encouraging demand for connected medical wearables.

Category-wise Analysis

Product Type Insights

Knee-high is expected to lead, accounting for 55% of the revenue share in 2026, due to its ease of use, strong patient compliance, and widespread adoption in hospitals for post-operative thrombosis prevention. These stockings are commonly preferred for moderate-risk patients because they provide effective graduated compression while remaining more comfortable and convenient than longer alternatives. A notable example includes the TED Knee Length Anti-Embolism Stockings offered by Cardinal Health, which are widely utilized across hospitals and clinical care settings for effective compression therapy and patient recovery support.

Thigh-high is likely to represent the fastest-growing segment, supported by increasing demand for enhanced venous coverage among high-risk and immobile patients. These stockings are increasingly used after major orthopedic, cardiovascular, and abdominal surgeries, where broader compression support is clinically recommended. For example, Mediven Thrombexin Thigh-High Stockings developed by Medi GmbH, is designed to provide reliable graduated compression and improved patient comfort during recovery and immobilization treatment.

Material Type Insights

Nylon is projected to lead the market, capturing around 50% of the revenue share in 2026, supported by its superior durability, elasticity, and cost-efficiency in compression garment manufacturing. Nylon-based stockings are widely preferred because they provide consistent graduated compression while maintaining structural strength during prolonged usage. For instance, anti-embolism compression products manufactured by Sigvaris Group, which utilize advanced nylon-based textile technologies for medical-grade compression therapy applications.

Spandex is expected to be the fastest-growing material segment, driven by its superior elasticity, flexibility, and shape-retention properties that enhance both patient comfort and compression effectiveness. Its ability to provide a secure fit while maintaining consistent pressure makes it a preferred material in anti-embolism stockings. For instance, JOBST Anti-Embolism Stockings from BSN Medical incorporate spandex-blended fabrics to offer improved stretchability, reliable graduated compression, and greater comfort during thrombosis prevention and post-operative care.

Regional Insights

North America Anti-Embolism Stockings Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, supported by advanced healthcare infrastructure, increasing surgical procedures, and strong awareness regarding venous thromboembolism prevention. Hospitals and long-term care facilities across the region continue to adopt compression therapy products as part of standard post-operative and immobility care protocols. A notable example includes anti-embolism compression solutions offered by Stryker, which support post-surgical patient care and hospital thromboprophylaxis programs through advanced compression therapy products and integrated healthcare solutions.

U.S. Anti-Embolism Stockings Market Trends

The U.S. is expected to dominate the regional market, accounting for approximately 80% of the market share in 2026, driven by rising surgical admissions and strong clinical emphasis on thrombosis prevention. Hospitals increasingly implement preventive compression therapy protocols for orthopedic and cardiovascular procedures. Growth in outpatient surgeries is expanding demand for easy-to-use compression garments. Rising obesity rates and sedentary lifestyles are increasing venous disorder risks among adults. Healthcare providers are also emphasizing early mobility and recovery management after surgeries.

Canada Anti-Embolism Stockings Market Trends

Canada is likely to be a significant market for anti-embolism stockings, holding approximately 20% of the market share in 2026, supported by increasing elderly populations and rising hospitalization rates. Public healthcare institutions are emphasizing preventive care measures for reducing venous thromboembolism risks among surgical patients. Demand for compression therapy products is increasing in rehabilitation centers and long-term care facilities. Hospitals are adopting patient-centered recovery programs that support the use of anti-embolism stockings during post-operative care.

Europe Anti-Embolism Stockings Market Trends

Europe is likely to be a significant market for anti-embolism stockings in 2026, due to strong healthcare systems, rising aging populations, and increasing prevalence of vascular disorders. The region continues to witness substantial demand for compression therapy products in hospitals, specialty clinics, and rehabilitation centers. For example, compression therapy products developed by Sigvaris Group, which offers advanced medical compression solutions.

U.K. Anti-Embolism Stockings Market Trends

The U.K. is likely to be a significant market for anti-embolism stockings, estimates for 17% of Europe market share in 2026, supported by increasing surgical procedures and expanding elderly demographics. Hospitals and healthcare facilities continue implementing thrombosis prevention programs for immobile and post-operative patients. Demand for compression therapy products is increasing across both acute care and homecare environments. Healthcare authorities are focusing on reducing venous thromboembolism-related complications through preventive treatment strategies.

Germany Anti-Embolism Stockings Market Trends

Germany is anticipated to dominate the regional market, accounting for around 35% of the Europe market share in 2026, due to its advanced healthcare infrastructure and strong medical device industry. The country experiences high demand for compression therapy products in surgical and rehabilitation settings. Increasing orthopedic and cardiovascular procedures are driving product adoption across hospitals. German healthcare providers emphasize preventive thrombosis management and patient recovery optimization. The aging population is also contributing to higher demand for vascular support products.

Asia Pacific Anti-Embolism Stockings Market Trends

The Asia Pacific region is likely to be the fastest-growing region in anti-embolism stockings in 2026, driven by its expanding healthcare infrastructure, increasing surgical procedures, and rising awareness regarding venous thromboembolism prevention. For example, the TED Anti-Embolism Stockings distributed by Cardinal Health across several Asia Pacific healthcare markets support post-operative thrombosis prevention and patient recovery management in hospitals and rehabilitation centers.

China Anti-Embolism Stockings Market Trends

China is projected to dominate the regional market, holding around a 30% share of the market in 2026, due to large patient populations and expanding healthcare infrastructure. Increasing surgical procedures and rising hospitalization rates are strengthening demand for thrombosis prevention products. Domestic manufacturers are expanding production capabilities to meet growing hospital demand. Rising awareness regarding circulatory disorders and post-operative care is encouraging greater adoption of anti-embolism stockings.

India Anti-Embolism Stockings Market Trends

India is expected to emerge as a significant market for anti-embolism stockings, accounting for approximately a 22% share in 2026, due to increasing healthcare awareness and rising surgical volumes. Expanding hospital networks and improving healthcare accessibility are supporting wider adoption of compression therapy products. The growing prevalence of diabetes, obesity, and cardiovascular conditions is increasing the risk of venous complications among patients. Healthcare providers are increasingly focusing on preventive thrombosis management during post-operative care.

Competitive Landscape

The global anti-embolism stockings market exhibits a moderately fragmented structure, driven by the presence of multinational medical compression manufacturers, regional healthcare suppliers, and specialized vascular care companies competing across hospital and homecare segments. Market growth is supported by rising demand for thrombosis prevention products, increasing surgical procedures, and expanding awareness regarding venous health management.

With key leaders, including Sigvaris Group, Medi GmbH, BSN Medical, Cardinal Health, Paul Hartmann, and Stryker, the market remains highly innovation-focused and quality-driven. These players compete through product innovation, strategic partnerships, healthcare distribution expansion, and development of patient-centric compression technologies.

Key Industry Developments:

- In October 2025, Cardinal Health launched the Kendall SCD SmartFlow Compression System in Europe, designed to enhance venous thromboembolism prevention through advanced intermittent pneumatic compression technology and improved patient monitoring features.

- In June 2025, Cardinal Health highlighted strategic investments in advanced medical products and long-term healthcare innovation initiatives during its Investor Day presentation, strengthening its position in vascular care and compression therapy solutions.

Companies Covered in Anti-Embolism Stockings Market

- Sigvaris Group

- Medi GmbH

- BSN Medical

- 3M Health Care

- Cardinal Health

- Paul Hartmann

- Stryker

Frequently Asked Questions

The global anti-embolism stockings market is projected to reach US$2.1 billion in 2026.

The market is driven by rising surgical procedures, increasing prevalence of venous thromboembolism (VTE), and growing demand for preventive compression therapy in hospitals and homecare settings.

The anti-embolism stockings market is expected to grow at a CAGR of 5.8% from 2026 to 2033.

Key opportunities lie in advanced compression fabric innovations, expanding home healthcare adoption, and growing demand for patient-friendly anti-embolism stockings in emerging healthcare markets.

Sigvaris Group, Medi GmbH, BSN Medical, 3M Health Care, and Medtronic are the leading players.