- Display Technologies

- Vertical-Cavity Surface-Emitting Lasers Market

Vertical-Cavity Surface-Emitting Lasers Market Size, Share, and Growth Forecast 2026 - 2033

Vertical-Cavity Surface-Emitting Lasers (VCSEL) Market by Mode (Single-mode VCSEL, Multi-mode VCSEL), Wavelength (Short Wavelength, Long Wavelength), Application (Data Communication, Consumer Electronics, Automotive, Healthcare, Industrial Heating & Sensing), and Regional Analysis, 2026 - 2033

Vertical-Cavity Surface-Emitting Lasers Market Size and Trend Analysis

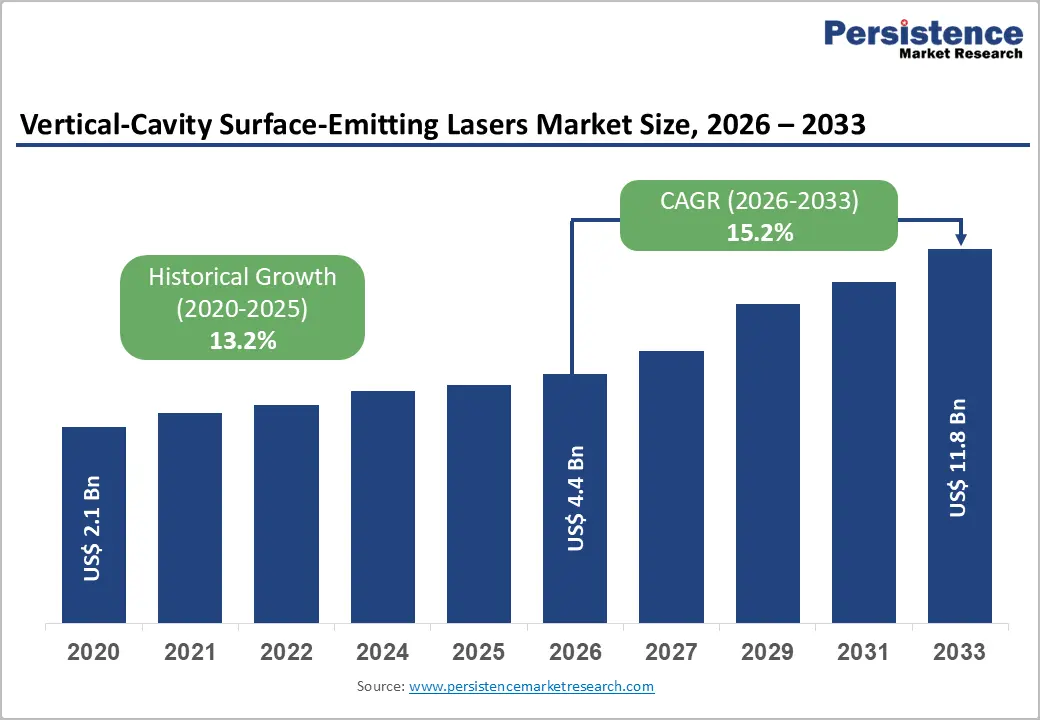

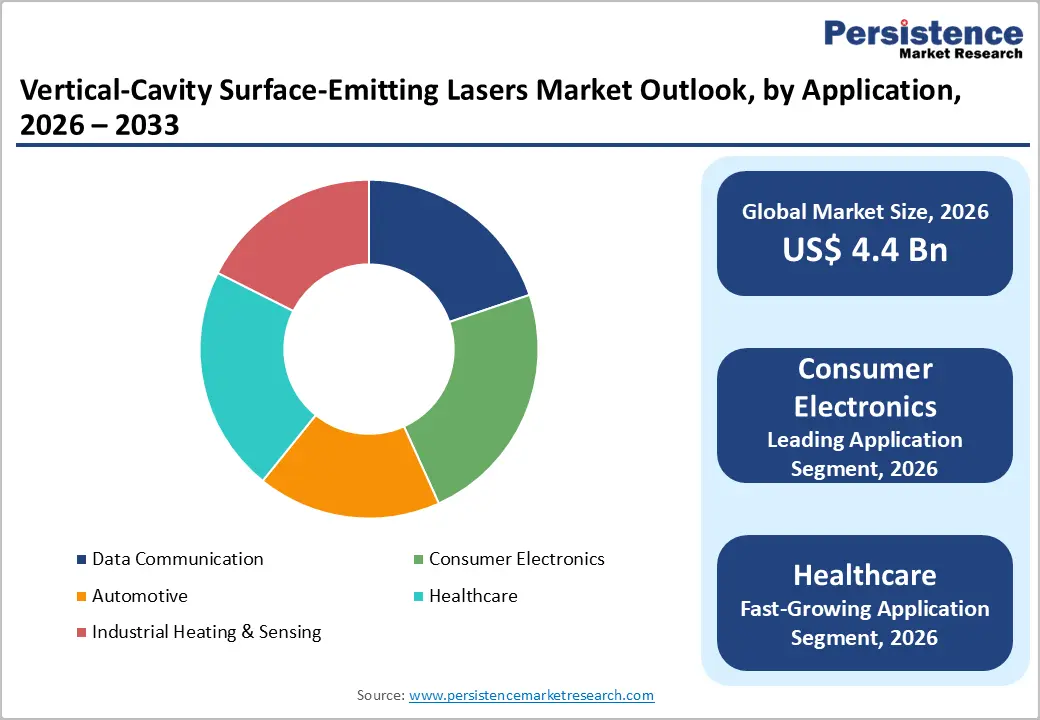

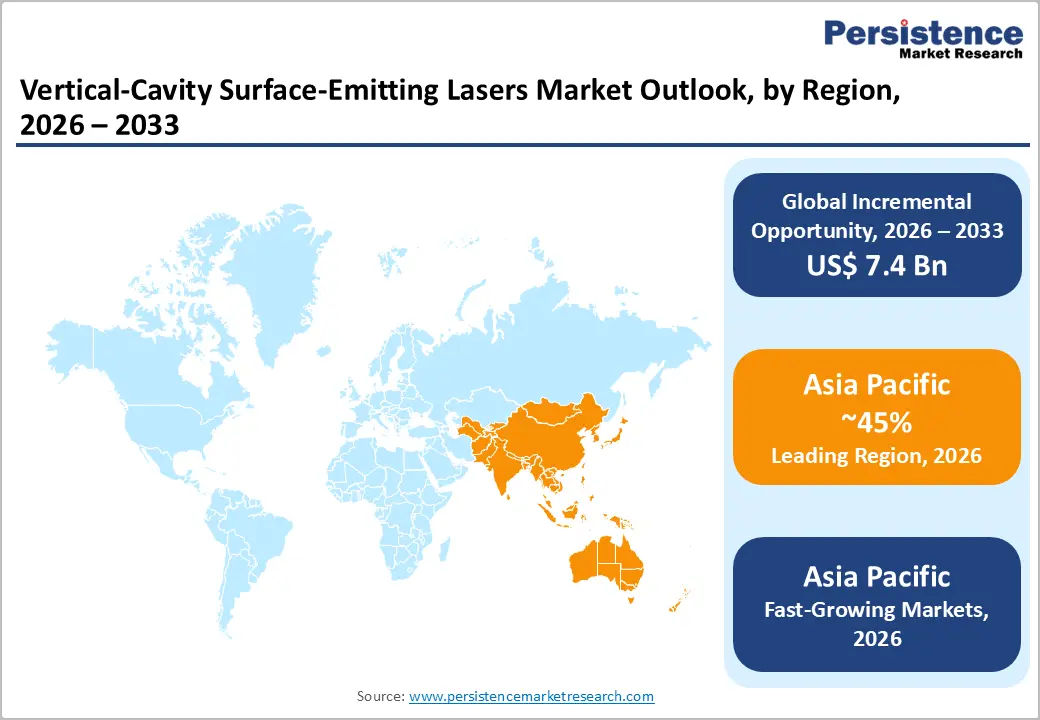

The global vertical-cavity surface-emitting lasers market size is expected to be valued at US$ 4.4 billion in 2026 and projected to reach US$ 11.8 billion by 2033, growing at a CAGR of 15.2% between 2026 and 2033.

The accelerating adoption of three-dimensional sensing modules in smartphones, augmented-reality headsets, and automotive LiDAR systems is the primary engine behind this expansion. Hyperscale data centers transitioning to 400G and 800G optical interconnects are simultaneously absorbing record volumes of 850 nm multi-mode VCSEL arrays, while industrial heating, gas sensing, and medical photonics applications are widening the demand base beyond traditional short-reach communication.

Key Market Highlights

- Leading Region: Asia Pacific dominates the global VCSEL market with a 45% share in 2025, led by China's smartphone manufacturing and Taiwan's epitaxy foundries.

- Fastest Growing Region: Asia Pacific remains the fastest-growing region through 2033, fueled by 5G rollouts and rising healthcare-wearable production across China, India and ASEAN.

- Dominant Segment: Consumer electronics commands a 40% application share in 2026, anchored by 3D facial recognition, AR/VR headsets and proximity sensing.

- Fastest Growing Segment: Healthcare leads growth through 2033, driven by VCSEL integration into smartwatches, pulse-oximetry patches and FDA-cleared photonic biosensors.

- Key Market Opportunity: Automotive LiDAR and in-cabin driver-monitoring sensing offer the most lucrative opportunity, backed by EU safety mandates effective July 2024.

Market Dynamics

Drivers - Rapid 3D Sensing Integration Across Consumer Mobile Devices Worldwide

The proliferation of facial-recognition systems, world-facing depth cameras and proximity sensors in smartphones has positioned VCSEL arrays as the photonic backbone of modern mobile devices. According to the International Telecommunication Union (ITU), global smartphone subscriptions surpassed 8.6 billion in 2024, with more than 70% of premium-tier handsets shipped that year incorporating at least one VCSEL-based optical module.

The structured-light and time-of-flight architectures pioneered for biometric authentication have since expanded into augmented-reality headsets, wireless earbuds and laptops. Mid-range smartphone portfolios are now absorbing emitters that were previously confined to flagship tiers, while indoor-mapping, photography autofocus and gesture-recognition use cases continue to multiply unit content per device, sustaining double-digit volume growth across the consumer ecosystem.

Hyperscale Data Center Buildout Powering AI Optical Interconnects

The exponential growth of generative-AI workloads is forcing cloud operators to upgrade intra-data-center optical fabrics from 100G to 400G and 800G speeds, where 850 nm multi-mode VCSELs paired with OM4/OM5 fiber remain the cost-efficient transceiver choice for sub-100-meter links connecting GPU clusters and switching fabrics.

The U.S. Department of Energy estimates that data centers consumed 176 terawatt-hours of electricity in 2023, with hyperscale facilities accounting for the largest share, and capacity is projected to nearly double by 2028. Multi-year supply commitments placed with VCSEL chip foundries to secure interconnect bandwidth underscore the scale of optical-transceiver consumption expected through the forecast horizon.

Restraints - Thermal Management Hurdles Limiting High-Power Deployment Performance

VCSEL devices operating above 100 mW continuous-wave output suffer from self-heating, wavelength drift, and accelerated degradation, particularly in automotive LiDAR and industrial heating applications where junction temperatures may exceed 85°C. Studies published by the IEEE Photonics Society indicate that every 10°C rise in operating temperature can reduce VCSEL lifetime by roughly half.

This thermal ceiling forces system designers to add costly thermoelectric coolers, active heat-sinking, or derated operating points, all of which inflate bill-of-materials cost and complicate module miniaturization. In harsh outdoor and engine-bay environments, qualification cycles lengthen significantly, slowing time-to-market for sensing modules and limiting addressable applications in extreme-temperature industrial and aerospace settings.

Rising Competition from Alternative Long-Reach Optical Technologies Emerging

For data-center spans beyond 300 meters, distributed-feedback lasers and emerging silicon-photonic transceivers offer superior bandwidth-distance product compared with conventional 850 nm VCSELs. The Optical Internetworking Forum (OIF) has standardized several 400ZR and 800ZR coherent specifications that bypass VCSEL technology entirely for inter-rack and campus interconnects.

As hyperscalers redesign network topologies around longer reaches to support AI training clusters spread across multiple buildings, a portion of the optical-transceiver budget shifts away from VCSEL-based short-reach modules. This architectural pivot caps the upside in pure data-communication applications and pressures average selling prices for short-wavelength multi-mode arrays.

Opportunities - Automotive LiDAR and In-Cabin Sensing Expansion Accelerating Globally

Vehicle manufacturers pursuing Level-2+ and Level-3 autonomy are increasingly specifying 905 nm and 940 nm VCSEL flash-illumination modules for short-range LiDAR, driver-monitoring cameras, and gesture recognition. The European Commission General Safety Regulation mandates driver-drowsiness and attention-detection systems in all new vehicles sold in the EU from July 2024, creating a structural demand pull.

With global new-car sales of roughly 78 million units in 2024 reported by the International Organization of Motor Vehicle Manufacturers (OICA), even modest VCSEL penetration translates into substantial chip volumes. Parallel regulatory momentum from the National Highway Traffic Safety Administration (NHTSA) on advanced driver-assistance features further reinforces the long-term volume trajectory for automotive-grade VCSEL arrays.

Medical Photonics and Wearable Health Monitoring Adoption Surging

Healthcare is the fast-growing application vertical for VCSELs, propelled by photoplethysmography, blood-oxygen monitoring, glucose-sensing research and dermatological phototherapy. The World Health Organization (WHO) estimates that the global population aged 60 years and older will rise from 1.0 billion in 2020 to 1.4 billion by 2030, accelerating uptake of continuous-monitoring wearables across both clinical and consumer settings.

The U.S. Food and Drug Administration (FDA) cleared multiple VCSEL-enabled pulse-oximetry and biosensor modules between 2023 and 2025, validating clinical performance and de-risking integration into smartwatches and patch-based monitors. Photobiomodulation devices for wound healing, pain management, and dermatology further open therapeutic revenue pools beyond traditional vital-signs monitoring.

Category-wise Insights

Mode Analysis

Multi-mode VCSELs command the leading position with an estimated 68% share of the global market in 2025. Their dominance stems from the overwhelming volume of 850 nm devices deployed in short-reach data-center optical interconnects and 3D-sensing arrays for consumer electronics. The IEEE 802.3 Ethernet working group has standardized 400GBASE-SR8 and 800GBASE-SR8 specifications that rely exclusively on multi-mode VCSEL arrays paired with parallel OM4/OM5 ribbon fiber.

Single-mode VCSELs are emerging as the fastest-growing type, propelled by precision sensing, atomic clocks, optical coherence tomography, and high-resolution gas detection that demand narrow spectral linewidth. Advances in oxide-confinement aperture engineering and high-contrast grating mirrors are improving wafer yields, while quantum-technology research programs and next-generation co-packaged optics roadmaps are unlocking fresh design wins for stable single transverse-mode devices.

Wavelength Insights

Short-wavelength VCSELs, spanning the 780 nm to 980 nm band, account for an estimated 82% of the market in 2025. This dominance reflects the deep installed base of 850 nm emitters in data-communication transceivers and the rapid scaling of 940 nm devices used in smartphone face-recognition, world-facing depth cameras, and automotive in-cabin monitoring. Silicon detectors exhibit peak responsivity precisely in this spectral window, enabling low-cost receiver designs.

Long-wavelength VCSELs operating at 1310 nm and 1550 nm are the fastest-growing category, gaining traction in eye-safe automotive LiDAR, passive optical networks, and metro-access links where reach and laser-safety thresholds outweigh cost. Maturing indium-phosphide and wafer-bonding fabrication, combined with rising adoption of eye-safe Class 1 specifications under IEC 60825-1, are progressively narrowing the cost gap with short-wavelength counterparts.

Application Insights

Consumer electronics is likely to lead the application landscape with a commanding 40% share of global VCSEL revenue in 2026. The segment owes its supremacy to universal integration of structured-light and time-of-flight modules in flagship smartphones, the rise of augmented-reality and mixed-reality headsets, and growing proximity sensing in wireless earbuds and laptops. Global smartphone shipments stood at roughly 1.24 billion units in 2024.

Healthcare emerges as the fastest-growing application, driven by VCSEL integration into smartwatches, continuous pulse-oximetry patches, glucose-sensing research devices, and photobiomodulation therapy systems. U.S. Food and Drug Administration (FDA) clearances for VCSEL-enabled biosensors between 2023 and 2025, combined with World Health Organization (WHO) projections of a rapidly ageing global population, are widening adoption across both clinical-grade monitoring and consumer-grade wearable wellness ecosystems.

Regional Insights

North America Vertical-Cavity Surface-Emitting Lasers Market Trends and Insights

North America holds an estimated 28% share of the global VCSEL market in 2026, anchored by hyperscale data-center expansion, defense photonics programs and a robust ecosystem of fabless VCSEL designers. The region benefits from concentrated cloud-infrastructure spending, rising automotive LiDAR pilots and continued leadership in medical-photonics innovation, supported by an unmatched depth of compound-semiconductor design talent.

- U.S. Vertical-Cavity Surface-Emitting Lasers Market Size

The United States is poised for 85% of North American VCSEL revenue in 2026, driven by data-center optics demand and CHIPS and Science Act incentives supporting domestic compound-semiconductor fabrication. Hyperscaler capital expenditure exceeding US$ 200 billion announced for 2025 by leading cloud operators underpins sustained transceiver consumption, while defense and biomedical photonics programs reinforce premium-tier component investment.

Europe Vertical-Cavity Surface-Emitting Lasers Market Trends and Insights

Europe is likely to represent around 22% of the global VCSEL market in 2026, combining automotive-grade photonics leadership with strong industrial-sensing demand. The European Commission Chips Act, targeting 20% global semiconductor production share by 2030, is channelling public funding into compound-semiconductor pilot lines, while regulatory mandates on driver monitoring and pan-European photonics research clusters continue to boost VCSEL adoption.

- Germany Vertical-Cavity Surface-Emitting Lasers Market Size

Germany is anticipated an 30% of European VCSEL revenue in 2026, anchored by automotive Tier-1 suppliers integrating VCSEL emitters into driver-monitoring and short-range LiDAR modules. Industrial heating, laser-welding, and material-processing applications by machine-tool makers further reinforce demand, supported by the country's deep Industrie 4.0 ecosystem and federally backed photonics research clusters across multiple Fraunhofer institutes.

- U.K. Vertical-Cavity Surface-Emitting Lasers Market Size

The United Kingdom is likely to account for nearly 18% of European VCSEL revenue in 2026. Demand is led by quantum-technology research programs funded under the UK National Quantum Strategy with £2.5 billion committed over ten years, alongside data-center optics consumption and medical-device innovation centered in the Oxford-Cambridge corridor, where photonics start-ups and university spin-outs sustain steady design activity.

- France Vertical-Cavity Surface-Emitting Lasers Market Size

France is more likely to account for 15% of European VCSEL revenue in 2026. Aerospace and defense programs, automotive sensing initiatives by domestic Tier-1 suppliers, and the strategic photonics roadmap of the French National Research Agency (ANR) collectively sustain demand for both short and long-wavelength devices, while the France 2030 investment plan further channels public funding into compound-semiconductor capacity.

Asia Pacific Vertical-Cavity Surface-Emitting Lasers Market Trends and Insights

Asia Pacific is likely to dominate with a 45% share of the global VCSEL market in 2026 and is simultaneously the fastest-growing region. China alone manufactures more than half of the world's smartphones, anchoring consumer-electronics VCSEL demand, while Taiwan hosts leading epitaxy foundries supplying global chip houses. South Korea contributes premium handset and memory-fab optical-interconnect demand.

- India Vertical-Cavity Surface-Emitting Lasers Market Size

India is likely to account for nearly 6% of the Asia Pacific VCSEL revenue in 2026. The India Semiconductor Mission, backed by a US$ 10 billion incentive package and the rapid rollout of 5G networks across more than 700 districts, is fueling demand for optical-transceiver components and smartphone-grade 3D-sensing modules, while accelerating data-center buildouts in Mumbai and Hyderabad, which reinforce structural growth.

- Japan Vertical-Cavity Surface-Emitting Lasers Market Size

Japan is poised for roughly 14% of the Asia Pacific VCSEL revenue in 2026. Domestic strength in automotive electronics, precision industrial sensing, and laser printing supports steady demand, with leading image-sensor and lighting companies driving innovation in time-of-flight imaging and high-power VCSEL arrays. Government-backed initiatives under METI further encourage advanced compound-semiconductor research and onshore packaging capacity.

- Southeast Asia Vertical-Cavity Surface-Emitting Lasers Market Size

Southeast Asia represents approximately 12% of Asia Pacific VCSEL revenue in 2026. Vietnam, Malaysia, and Thailand have emerged as critical back-end assembly and optical-module packaging hubs. Foreign direct investment of US$ 230 billion into ASEAN economies in 2023, as reported by UNCTAD, has accelerated capacity additions across electronics value chains, with Malaysia and Singapore hosting growing photonics test and packaging clusters.

Competitive Landscape

The global VCSEL market is moderately consolidated, with a small group of vertically integrated players accounting for the bulk of revenue. Leading firms differentiate through epitaxy-to-module capability, proprietary oxide-confinement processes and automotive-grade qualification under AEC-Q102 standards. Long-term supply agreements with smartphone OEMs and cloud hyperscalers, secured through multi-year wafer commitments, remain the principal moat against new entrants.

Strategic priorities include capacity expansion at 6-inch and 8-inch gallium-arsenide lines, multi-junction VCSEL development to lift wall-plug efficiency, and pure-play foundry partnerships. Emerging business models cover custom-design services for sensing applications and licensing of high-power array architectures to system integrators.

Key Developments:

- In March 2025, II-VI / Coherent Corp. announced expanded 6-inch VCSEL wafer capacity at its Sherman, Texas facility to serve data-communication and automotive sensing customers, supported by U.S. CHIPS Act funding.

- In November 2024: ams OSRAM launched a new generation of high-power multi-junction VCSEL arrays targeting automotive in-cabin sensing and short-range LiDAR, achieving wall-plug efficiencies exceeding 60%.

- In June 2024, Lumentum Holdings disclosed a multi-year supply agreement to provide VCSEL arrays for next-generation 3D-sensing modules in premium smartphones, securing long-term wafer commitments with epitaxy partners.

Companies Covered in Vertical-Cavity Surface-Emitting Lasers Market

- Coherent Corp.

- Lumentum Holdings Inc.

- ams OSRAM AG

- Broadcom Inc.

- TRUMPF GmbH + Co. KG

- IQE plc

- VERTILAS GmbH

- Vixar Inc.

- Sony Semiconductor Solutions Corporation

- Hamamatsu Photonics K.K.

- Inneos LLC

- Finisar Corporation

- Leonardo DRS

- Ushio Inc.

Frequently Asked Questions

The global VCSEL market is valued at US$ 4.4 billion in 2026 and projected to reach US$ 11.8 billion by 2033 at a 15.2% CAGR.

Rising 3D sensing adoption in smartphones, AR headsets, and automotive systems, alongside hyperscale data-center upgrades to 400G and 800G optical interconnects.

Asia Pacific leads with an estimated 45% revenue share in 2025, anchored by China's smartphone scale and Taiwan's epitaxy foundry leadership.

Automotive LiDAR and in-cabin driver-monitoring sensing, reinforced by the European Commission safety mandate effective July 2024 and Level-2+ autonomy growth.

Key players profiled in the report include Coherent Corp., Lumentum Holdings Inc., ams OSRAM AG, Broadcom Inc., TRUMPF GmbH, and IQE plc.