- Display Technologies

- Spatial Light Modulator Market

Spatial Light Modulator Market Size, Share, and Growth Forecast 2026 - 2033

Spatial Light Modulator Market by Device Type (Optically Addressed, Electrically Addressed, Others), Resolution (Below 1024 × 768, 1024 × 768 to 1920 × 1080, Above 1920 × 1080), Application (Consumer Electronics, Healthcare, Telecomm, Automotive, Industrial & Manufacturing, Research & Academia, Defense & Aerospace, Others), and Regional Analysis, 2026 - 2033

Spatial Light Modulator Market Size and Trend Analysis

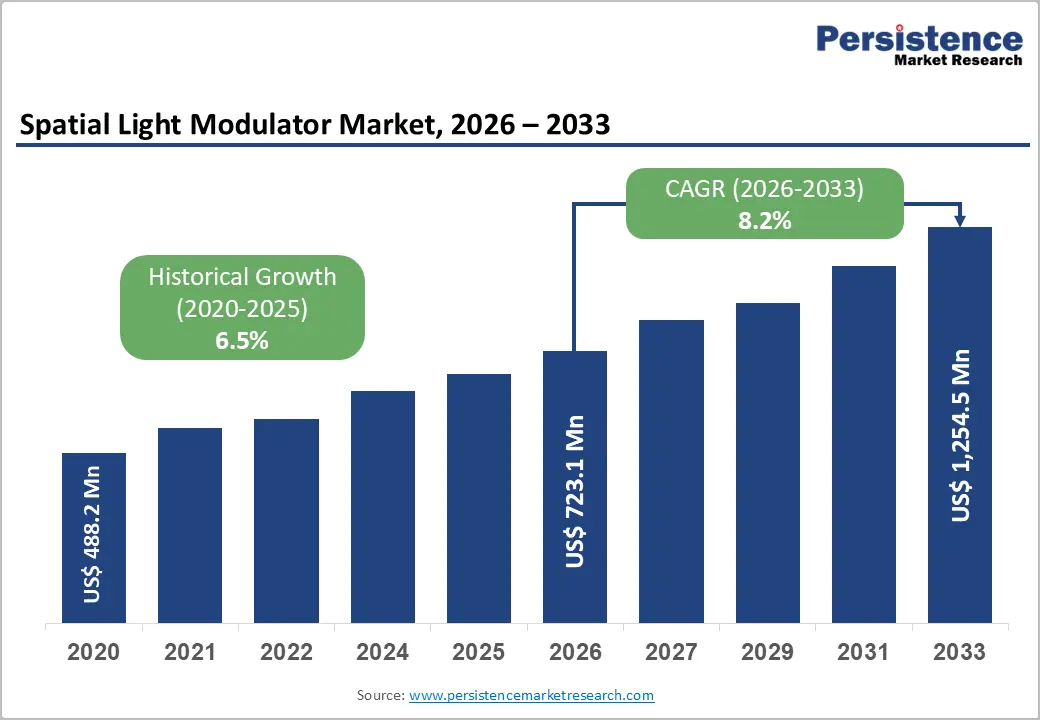

The global spatial light modulator market size is expected to be valued at US$ 723.1 million in 2026 and is projected to reach US$ 1,254.5 million by 2033, growing at a CAGR of 8.2% between 2026 and 2033.

The market is expanding as programmable light control has become essential in high-precision photonics, especially for beam shaping, adaptive optics, holography, microscopy, and advanced laser processing. The demand is also rising as display systems, quantum technologies, and optical instrumentation increasingly require compact, software-driven, and high-resolution modulation solutions. Products such as LCOS-SLMs and DLP-based modulators are gaining traction due to their combination of flexibility, speed, and repeatability in research and industrial environments.

Key Industry Highlights:

- Leading Device Type: Electrically Addressed dominates the market with over 56% share in 2026, valued at more than US$ 405 Mn, driven by their ability to deliver precise, real-time light modulation, high-speed performance, and compatibility with semiconductor fabrication processes.

- Leading Resolution: The 1024 × 768 to 1920 × 1080 segment holds over 35% share in 2026, valued at more than US$ 253.1 Mn, owing to its optimal balance between performance, cost efficiency, and compatibility with existing optical systems.

- Fastest Growing Resolution: Above 1920 × 1080 is the fastest-growing segment, driven by increasing demand for high-definition imaging, LiDAR accuracy, and advanced applications in defense, aerospace, and medical imaging.

- Leading Application: Consumer Electronics leads the market with around 30% share in 2026, valued at over US$ 216.9 Mn, fueled by strong demand for AR/VR devices, high-quality displays, and compact projection systems.

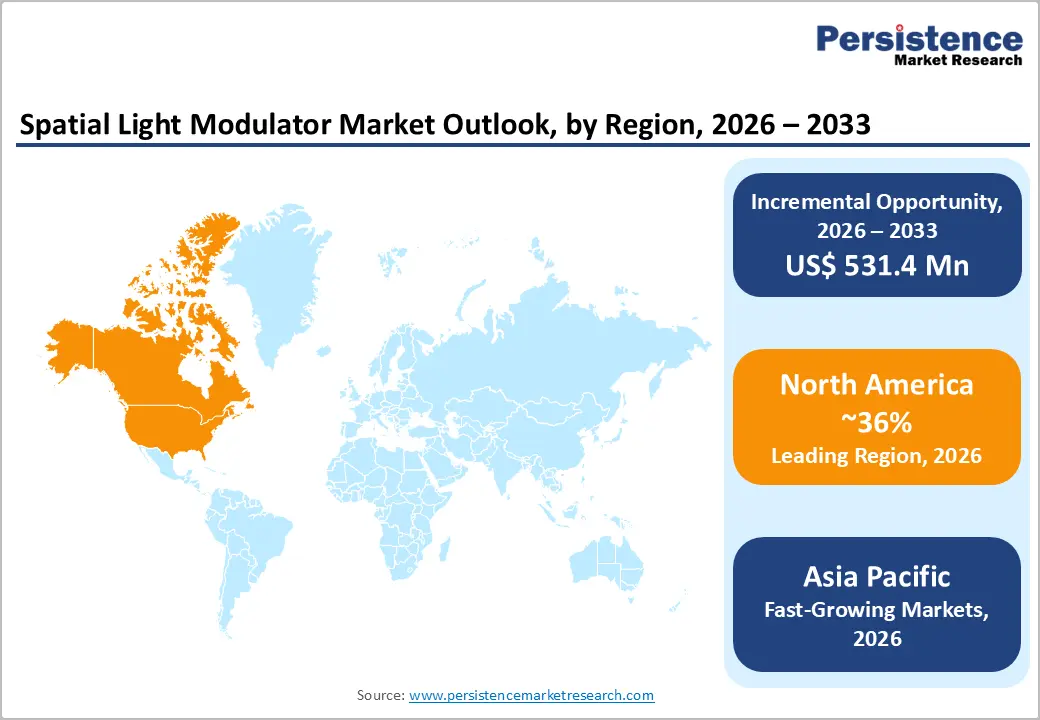

- Leading Region: North America leads the market with around 36% share in 2026, driven by strong defense funding, AR/VR innovation, and photonics R&D investments.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, expanding at a CAGR of 12.7%, supported by semiconductor manufacturing strength, consumer electronics production, and increasing government investments in quantum technologies and photonics infrastructure.

Market Dynamics

Drivers - Surging Demand for Holographic Displays and Augmented Reality Applications

Rising demand for holographic displays and augmented reality (AR) applications is driving demand, fueled by the need for high-precision wavefront control and advanced optical modulation technologies. Consumer electronics manufacturers and enterprise AR platform developers are embedding spatial light modulators into next-generation headsets, heads-up displays, and projection systems to achieve pixel-level light manipulation that conventional optics cannot deliver.

AR headset shipments globally surpassed 20 million units in 2025, driving upstream component demand for high-resolution modulator arrays. As display manufacturers push resolution thresholds above 1920 × 1080, the demand for electrically addressed spatial light modulators with sub-millisecond switching speeds compounds across the value chain.

Increased Defense and Aerospace Investment in Adaptive Optics and Directed-Energy Systems

Defense agencies across North America and Europe are scaling procurement of adaptive optics platforms that rely on spatial light modulators for laser beam steering, wavefront correction, and directed-energy weapon systems. The United States Department of Defense has consistently allocated over US$20 billion annually to advanced photonics and directed-energy research programs, a significant portion of which flows into high-performance modulator technology.

This procurement cycle creates a stable, non-cyclical revenue base for spatial light modulator manufacturers serving the defense and aerospace vertical. The structural reliance on spatial light modulators for real-time phase correction in adaptive telescope systems and satellite communication terminals further reinforces long-cycle purchasing contracts that insulate suppliers from short-term demand volatility.

Restraints - High Manufacturing Complexity and Unit Cost Barriers

The spatial light modulator industry faces a persistent cost ceiling that restricts adoption among cost-sensitive commercial and mid-market buyers. Manufacturing high-resolution liquid crystal on silicon (LCoS) and digital micromirror device (DMD) arrays requires cleanroom fabrication processes, precise alignment tolerances, and specialized optical coatings, which push unit costs substantially above those of commodity display components.

Many industrial automation and consumer-tier applications find spatial light modulators economically prohibitive relative to simpler beam-shaping alternatives. Without meaningful yield improvements or economies of scale from higher-volume programs, this cost barrier will continue to slow adoption penetration in price-elastic end markets throughout the forecast period.

Limited Awareness and Integration Complexity in Emerging Application Verticals

Many potential end-users, including automotive Tier-1 suppliers and medical device integrators, lack in-house optical engineering expertise to specify and integrate modulator systems effectively. This knowledge gap creates elongated sales cycles, increases suppliers' post-sale technical support burdens, and raises the total cost of system integration for buyers.

According to a study, integration-related project delays account for a significant proportion of deferred purchase decisions in the industrial and healthcare segments. Until modulator manufacturers invest more aggressively in reference design kits, application programming interfaces, and turnkey integration partnerships, this restraint will continue to dampen the otherwise robust demand pipeline in emerging verticals.

Opportunities - Commercialization of Optical Computing and Neuromorphic Photonics Architectures

Research institutions and deep-tech startups are actively prototyping all-optical inference engines in which spatial light modulators replace electronic weight matrices, offering orders-of-magnitude improvements in throughput per watt compared with GPU-based architectures. According to a study, venture investment in photonic computing exceeded $1 billion globally, signaling that capital is already being mobilized around this paradigm.

Spatial light modulator manufacturers that establish early partnerships with optical computing platform developers, particularly those targeting data center AI inference workloads, stand to secure long-term volume contracts well ahead of the market's maturation. Established players that prioritize co-development agreements with semiconductor photonics firms are expected to secure early influence over platform-level specifications.

Integration of Spatial Light Modulators into Autonomous Vehicle LiDAR and Sensing Platforms

The automotive sector is presenting a structurally new demand pocket, as solid-state LiDAR developers increasingly evaluate beam-steering spatial light modulators as an alternative to mechanical and MEMS-based scanning approaches. Automotive OEMs and Tier-1 sensor suppliers are under intense pressure to demonstrate reliable, solid-state long-range sensing solutions ahead of the Level 3 and Level 4 autonomy homologation cycles, which are expected to accelerate post-2027. Spatial light modulators capable of high-speed, non-mechanical beam deflection at 905 nm and 1550 nm wavelengths meet these requirements. Modulator suppliers that invest in automotive-grade qualification processes, including AEC-Q100 certification and extended-temperature-range validation, will dramatically expand their addressable market.

Category-wise Analysis

Device Type Insights

The electrically addressed segment is dominant and accounts for approximately 56% share in 2026, as they offer precise, real-time control over light modulation using electronic signals, which is essential for high-speed applications. Industries like telecom, consumer electronics, and advanced imaging require stable, repeatable, and scalable modulation solutions, which EA-SLMs deliver efficiently. Their compatibility with semiconductor manufacturing processes also reduces production complexity and cost.

Optically addressed devices are emerging as the fastest-growing segment, as they enable parallel data processing and high-resolution wavefront control, which are increasingly needed in advanced optical computing and holography. Their ability to handle complex optical patterns without electronic interference makes them ideal for research and scientific applications. They also support emerging needs in quantum optics and optical neural networks. As photonics-based computing evolves, OA-SLMs are becoming critical for next-generation optical architectures.

Resolution Insights

1024 × 768 to 1920 × 1080 dominate, holding over 35% share in the 2026 value of over US$ 253.1 Mn, due to their optimal balance between performance and cost and their ability to meet the needs of most commercial applications. Industries prioritize resolutions that provide sufficient clarity while maintaining affordability and energy efficiency. Their compatibility with existing optical systems reduces the need for redesign or additional investment. The demand is also supported by stable supply chains and mature manufacturing processes.

The 1920 × 1080 segment is growing the fastest, driven by the need for sharper image quality and finer beam shaping in defense, aerospace, and medical imaging, which is driving adoption. Emerging technologies like 3D sensing and LiDAR also require high pixel density for improved accuracy. As digital visualization and immersive technologies expand, higher resolution SLMs become essential. Continuous innovation in microfabrication is also making high-resolution devices more accessible.

Application Insights

Consumer electronics is dominant, capturing around 30% share & value of over US$ 216.9 Mn in 2026, driven by demand for high-quality displays, compact projection systems, and advanced imaging features in devices such as smartphones, AR/VR headsets, and smart TVs. Users increasingly expect enhanced visual experiences, pushing manufacturers to adopt SLMs for better brightness, contrast, and resolution. The trend toward miniaturization and multifunctionality also supports SLM integration. Cost sensitivity in this segment favors scalable and mass-producible technologies like LCoS-based SLMs.

Automotive is the fastest-growing segment, driven by the rising need for advanced driver-assistance systems (ADAS), adaptive headlights, and in-cabin display technologies. SLMs enable dynamic beam shaping for safer night driving and improved visibility. Growth is fueled by increasing integration of LiDAR systems in autonomous vehicles, where precise light modulation is critical. The shift toward smart, connected, and autonomous vehicles is accelerating demand for optical sensing technologies. The need for enhanced safety, real-time data visualization, and intelligent lighting systems is pushing rapid adoption in this segment.

Regional Insights

North America Spatial Light Modulator Market Trends and Insights

North America holds a significant position in the Spatial Light Modulator market, with an estimated share of around 36% in 2026. The region benefits from sustained federal investment in directed-energy weapons, adaptive optics for space surveillance, and quantum computing infrastructure, all of which directly generate demand for high-performance spatial light modulators.

The concentration of AR/VR platform developers and autonomous vehicle technology firms in the United States amplifies near-term adoption momentum. The U.S. Spatial Light Modulator Market accounts for approximately 78% of North America's total revenue, translating to US$ 203.1 million in 2026, based on regional share. Silicon Valley's concentration of LiDAR and autonomous vehicle developers is generating incremental design-win opportunities for beam-steering modulator suppliers.

Europe Spatial Light Modulator Market Trends and Insights

Europe holds a significant share of over 23% in 2026, driven by a combination of precision photonics manufacturing heritage, rigorous regulatory frameworks favoring high-quality optical instrumentation, and sustained public investment in research and academic applications. The European Horizon Europe program has committed substantial funding to photonics and quantum technology research, directly stimulating demand for laboratory-grade spatial light modulators at universities and national research institutes.

Europe's regulatory emphasis on quality and environmental compliance also drives the adoption of energy-efficient electrically addressed modulator architectures.

The German spatial light modulator market is expected to exceed US$40 million in revenue in 2026. The country's advanced industrial manufacturing base, particularly in laser processing, precision optics, and automotive sensing, creates multi-vertical demand for spatial light modulators. The United Kingdom accounts for over 18% of market revenue in 2026. Post-Brexit, the UK has independently reinforced its photonics investment agenda through the UK National Quantum Strategy, which will sustain demand for high-precision modulator hardware in quantum sensing and computing research through the forecast horizon.

Asia Pacific Spatial Light Modulator Market Trends and Insights

Asia Pacific is expected to attain a CAGR of 12.7% in the forecast period. The structural acceleration stems from state-driven investment in semiconductor photonics and quantum communication infrastructure. Consumer electronics manufacturing concentration in the region creates strong pull-through demand for spatial light modulators in AR display and laser processing equipment supply chains.

China's spatial light modulator market, which accounted for over 45% of regional revenue in 2026, was roughly US$104 million. State-backed investment in quantum communication satellite networks, semiconductor lithography equipment, and defense adaptive optics is driving sustained institutional demand.

Japan accounts for over 21% of Asia Pacific's spatial light modulator market revenue in 2026, supported by a tradition of precision optics and photonics manufacturing that includes globally significant players in the instrumentation and semiconductor equipment segments. Japan's display technology leadership, particularly in LCoS and micro-display panel fabrication, reinforces supply-side competitiveness alongside domestic demand. India's growing photonics research base, spurred by the Department of Science and Technology (DST) and the National Mission on Quantum Technologies & Applications (NM-QTA) with an outlay of INR 6003.65 Crore, is creating nascent but accelerating institutional demand for high-resolution SLMs.

Competitive Landscape

The global spatial light modulator market exhibits a moderately fragmented competitive structure, characterised by a handful of scale-capable technology incumbents operating alongside a larger population of specialist niche players focused on specific device architectures, wavelength ranges, or application verticals. Competition centers primarily on technological differentiation, specifically on phase accuracy, pixel count, switching speed, and wavelength compatibility. The spatial light modulator competitive landscape is gradually consolidating at the top tier as R&D costs escalate, while the specialist segment remains dynamic with continued entry from academic spin-offs and deep-tech ventures in optical computing and quantum photonics.

Key Developments:

- In January 2026, Santec AOC announced a special offer for its Spatial Light Modulator (SLM) production units, aimed at accelerating adoption in research and industrial applications. The promotion provides easier access to high-performance SLM devices to support expanding demand in photonics and optical technologies.

- In August 2025, Hamamatsu Photonics announced it had been selected for a Japanese government-backed Post-5G R&D project led by NEDO to accelerate quantum computer development. The company will develop ultra-high-speed and high-sensitivity cameras along with a high-resolution spatial light modulator between 2025 and 2027 to support quantum computing technologies.

Spatial Light Modulator Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 488.2 Mn |

| Current Market Value (2026) | US$ 723.1 Mn |

| Projected Market Value (2033) | US$ 1,254.5 Mn |

| CAGR (2026 - 2033) | 8.2% |

| Leading Region | North America, 36% share |

| Dominant Device Type | Electrically Addressed, 56% share |

| Top-ranking Application | Consumer Electronics, 30% |

| Incremental Opportunity | US$ 531.4 Mn |

Companies Covered in Spatial Light Modulator Market

- Hamamatsu Photonics

- Holoeye Photonics

- Meadowlark Optics

- Texas Instruments

- Santec Corporation

- Jenoptik AG

- Thorlabs Inc.

- Forth Dimension Displays

- LightTrans International

- Laser 2000 GmbH

- Jasper Display Corp.

- Kopin Corporation

- Himax Technologies

- OmniVision Technologies

- Others

Frequently Asked Questions

The Spatial Light Modulator Market is valued at US$ 723.1 Mn in 2026 and projected to reach US$ 1,254.5 Mn by 2033, growing at a CAGR of 8.2%, driven by rising adoption in AR, defense optics, and optical computing.

The rapid commercialization of AR and holographic displays and strong defense photonics investments create sustained demand for high-precision SLMs.

North America leads with ~36% share in 2026, supported by its strong defense and aerospace ecosystem, where continuous funding supports advanced photonics, adaptive optics, and directed-energy programs that heavily rely on spatial light modulators.

Major opportunities lie in automotive LiDAR and adaptive headlighting linked to autonomous driving growth and optical computing/photonic AI. Early partnerships with photonics firms will be critical to capturing future high-volume demand.

Leading players include Hamamatsu Photonics, Holoeye Photonics, Meadowlark Optics, Texas Instruments, Santec Corporation, Jenoptik AG, and Thorlabs Inc.