- Inks, Coatings, Adhesives & Sealants (ICAS)

- Thermal Spray Coatings Market

Thermal Spray Coatings Market Size, Share, and Growth Forecast 2026 – 2033

Thermal Spray Coatings Market by Coating Type (Metals, Ceramics, Intermetallics, Polymers, Carbides, Abradables, Others), Process (Cold Spray, Flame Spray, Plasma Spray, HVOF, Electric Arc Spray, Others), Industry (Aerospace, Industrial Gas Turbine, Automotive, Medical, Printing, Steel, Others), and Regional Analysis, 2026–2033

Thermal Spray Coatings Market Size and Trend Analysis

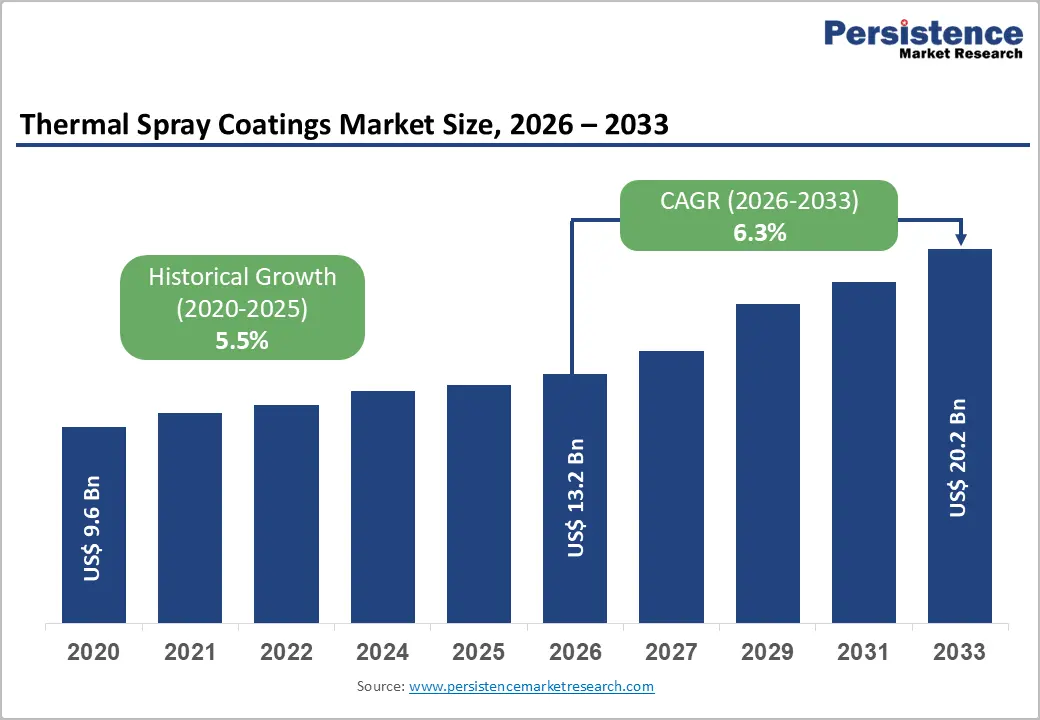

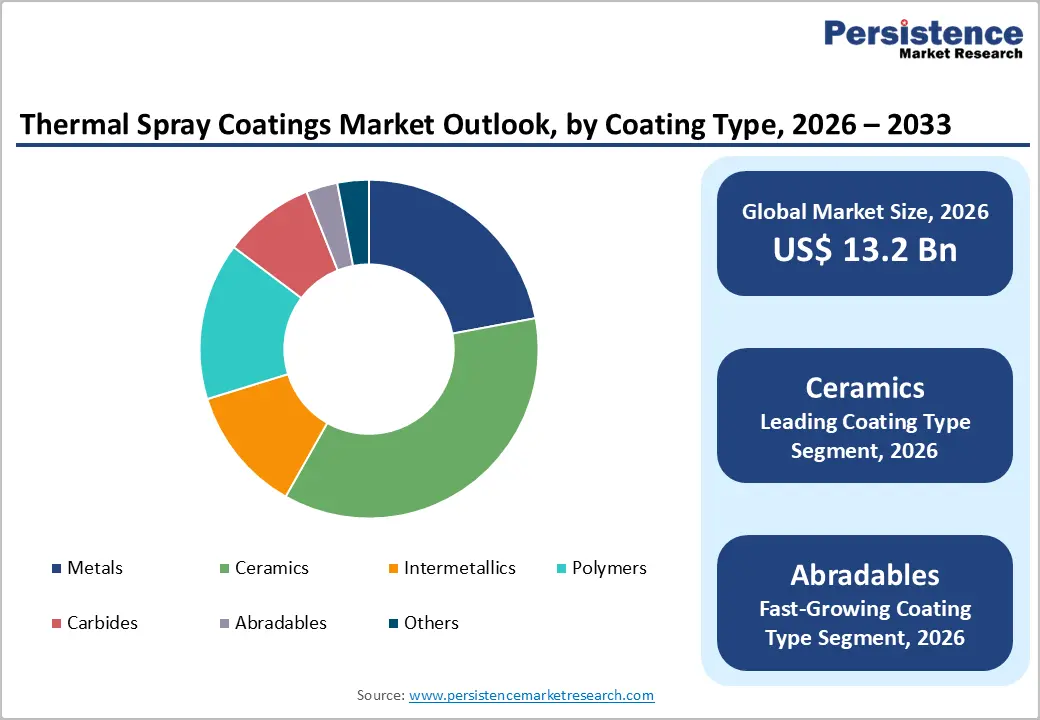

The global thermal spray coatings market size is expected to be valued at US$ 13.2 billion in 2026 and projected to reach US$ 20.2 billion by 2033, growing at a CAGR of 6.3% between 2026 and 2033.

The market is experiencing accelerating growth driven by intensifying demand for high-performance protective coatings in aerospace, industrial gas turbines, and automotive sectors, combined with expanding applications in emerging industries, including medical implants and energy transition technologies.

The global push for extended component lifecycle management, reducing industrial downtime and material costs, coupled with rising investment in MRO services across aviation and power generation, and the rapid industrial capacity expansion in China, India, and Southeast Asia, are the primary forces propelling sustained above-GDP market growth through 2033.

Key Industry Highlights:

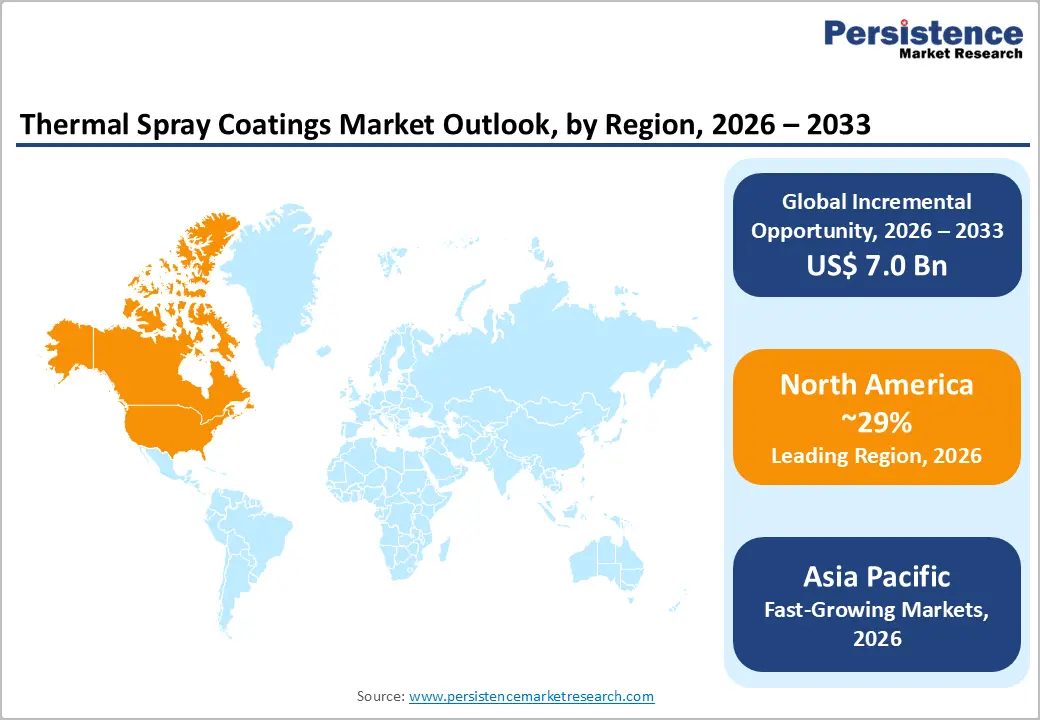

- Leading Region: North America commanded approximately 29% of global thermal spray coatings market share in 2026, anchored by the world's largest aerospace industrial base, DoD's US$ 258 billion+ FY2024 budget, and NADCAP-certified coating infrastructure of Praxair Surface Technologies, Kennametal Stellite, and ASB Industries.

- Fast-Growing Market: Asia Pacific is likely to achieve 7% CAGR driven by China's COMAC C919 aerospace program, India's PLI Defence Scheme, Linde's Asia gas infrastructure expansion, and Singapore's ST Engineering MRO hub driving precision coating demand.

- Dominant Segment: Ceramic coatings are likely to account for approximately 36% market share in 2026, driven by universal gas turbine TBC requirements using YSZ, operating temperatures exceeding 1,600°C enabled by TBCs per NASA Glenn Research Center documentation, and Oerlikon Metco/Saint-Gobain ceramic powder leadership.

- Fast-Growing Segment: Abradables are likely to lead driven by ICAO CORSIA and EASA emissions mandates, next-generation LEAP and GTF engine programs, and Oerlikon Metco's MetcoTough™ and Saint-Gobain's Amdry® abradable coating systems adoption.

- Key Opportunity: China's 14th Five-Year Plan, India's PLI Defence/Aerospace, and IATA's US$ 100 billion+ annual MRO expenditure flowing through Asia Pacific create a US$ 7 billion incremental opportunities for thermal spray suppliers expanding regional coating service capacity.

DRO Analysis

Drivers - Expanding Commercial Aviation Fleet and MRO Activity Driving Aerospace Thermal Spray Demand

The global commercial aviation industry's sustained fleet expansion and intensive maintenance, repair, and overhaul (MRO) activity is the most significant demand driver for thermal spray coatings in the aerospace segment. According to Airbus's Global Market Forecast 2023–2042, the commercial aircraft fleet is expected to nearly double from approximately 22,000 aircraft in 2023 to 46,000 by 2042, generating proportionate demand for thermal barrier coatings (TBCs), abradable seal coatings, and wear-resistant ceramic coatings on turbine blades, vanes, and combustor components.

The International Air Transport Association (IATA) estimates annual global MRO expenditure at over US$ 100 billion, with thermal spray coating services representing a significant and growing component. Praxair Surface Technologies and Oerlikon Metco maintain dedicated aerospace coating certification centers globally to serve this expanding demand base.

Industrial Gas Turbine Fleet Expansion and Energy Transition Investment Sustaining Coating Demand

Global investment in natural gas power generation, as a transition fuel bridging fossil-fuel phase-out and full renewable adoption, is sustaining strong demand for thermal spray coatings in the industrial gas turbine (IGT) segment. The International Energy Agency (IEA) projects that gas-fired power generation capacity will continue to grow through 2030 in Asia, Africa, and Latin America to meet rising electricity demand.

Thermal barrier coatings (TBCs), typically yttria-stabilized zirconia (YSZ) applied by atmospheric plasma spray (APS), enable turbine inlet temperatures exceeding 1,600°C, directly improving fuel efficiency and power output. Each F-class and H-class gas turbine requires extensive thermal spray coating of hot section components, creating significant per-unit coating services revenue for companies including Sulzer, Bodycote, and Curtiss-Wright Surface Technologies.

Restraints - High Equipment Investment and Process Complexity Limiting SME Adoption

Advanced thermal spray systems, particularly High-Velocity Oxygen Fuel (HVOF) and atmospheric plasma spray (APS) equipment, carry capital costs ranging from US$ 200,000 to US$ 1,500,000+ per installation, creating significant entry barriers for small and medium enterprises (SMEs) seeking to establish in-house coating capabilities.

Process qualification requirements under NADCAP (National Aerospace and Defense Contractors Accreditation Program) and AS9100 aerospace quality standards impose rigorous testing and documentation burdens, extending time-to-market for new coating service providers and limiting competitive market entry in precision industrial segments.

Health and Environmental Concerns Around Overspray Particulates and Hazardous Feedstock Materials

Thermal spray processes generate fine particulate overspray, including metallic, ceramic, and carbide particles, that pose respiratory and environmental hazards if inadequately controlled. Regulatory frameworks, including the U.S. EPA's National Emission Standards for Hazardous Air Pollutants (NESHAP) and the EU REACH regulation, impose strict controls on chromium, nickel, and cobalt-containing feedstock materials commonly used in thermal spray, increasing compliance costs.

Restrictions on certain chrome-based coatings under EU RoHS Directive are compelling material reformulation investments that add operational cost and development timeline burdens for coating service providers.

Opportunities - Abradable Coatings: Fastest-Growing Segment Driven by Next-Generation Engine Efficiency Mandates

Abradable thermal spray coatings, applied to compressor and turbine casings to minimize blade-tip clearances and maximize engine efficiency, represent the fastest-growing coating type segment, projected at a 7% CAGR in the forecast period. The critical role of abradables in achieving turbine efficiency targets mandated by the International Civil Aviation Organization (ICAO) Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) and European Aviation Safety Agency (EASA) emissions frameworks is directly driving adoption.

Next-generation engines, including CFM International's LEAP and Pratt & Whitney's GTF (Geared Turbofan), extensively use advanced abradable coating systems. Oerlikon Metco's MetcoTough™ and Saint-Gobain's Amdry® abradable product lines are experiencing increased procurement as engine manufacturers and MRO shops respond to next-generation fleet entry and aggressive fuel efficiency targets across both commercial and military aviation programs.

Asia Pacific Industrial Expansion: Multi-Billion-Dollar Thermal Spray Demand Corridor

Asia Pacific represents a growth geographic opportunity for thermal spray coatings, driven by massive industrial capacity expansion in aerospace manufacturing, power generation, automotive, and steel processing across China, India, Japan, and Southeast Asia. China's 14th Five-Year Plan (2021–2025) and Made in China 2025 initiative allocate significant investment to aerospace and advanced manufacturing, sectors with intensive thermal spray requirements.

India's IISS (Indian Space Research Organisation) and DRDO aerospace programs, combined with the Production-Linked Incentive (PLI) Scheme for Defence worth ?18,924 crore, are expanding the domestic aerospace manufacturing base, requiring NADCAP-compliant thermal spray capabilities. Linde and Höganäs AB are expanding powder manufacturing and gas supply infrastructure in Asia to serve rapidly growing regional coating demand.

Category-wise Analysis

Coating Type Insights

The ceramics segment dominated the thermal spray coatings market, commanding approximately 36% of the total coating type market share in 2026. Ceramic thermal spray coatings, primarily yttria-stabilized zirconia (YSZ) and alumina-titania (Al?O?-TiO?), are indispensable for thermal barrier, wear resistance, and electrical insulation applications across aerospace, industrial gas turbines, and industrial machinery. The fundamental requirement for thermal barrier coatings (TBCs) in every gas turbine hot section component, from first-stage blades to combustor liners, drives enormous and recurring ceramic coating demand.

NASA's Glenn Research Center has documented that TBCs enable turbine operating temperatures exceeding alloy melting points, making ceramic coatings a mission-critical enabling technology. Leading suppliers, including Oerlikon Metco, Praxair Surface Technologies, and Saint-Gobain, maintain extensive ceramic powder and coating service portfolios serving this dominant segment.

Process Insights

Plasma spray, encompassing both atmospheric plasma spray (APS) and vacuum plasma spray (VPS), led the process segment, representing approximately 38% of the total thermal spray process market share in 2026. Plasma spray's unique ability to deposit virtually any ceramic, metallic, or cermet feedstock at temperatures exceeding 15,000°C, sufficient to melt even ultra-refractory materials, makes it the most versatile and widely applicable thermal spray process across aerospace, medical, and industrial gas turbine applications.

NADCAP-qualified plasma spray cells are standard infrastructure requirements for AS9100-certified aerospace component manufacturers. The process's compatibility with yttria-stabilized zirconia (YSZ) TBC deposition, the dominant application in terms of revenue, directly reinforces its market leadership, with Bodycote, Curtiss-Wright, and TWI Ltd maintaining high-capacity plasma spray facilities globally.

Industry Insights

The aerospace end-use segment led the thermal spray coatings market, accounting for approximately 35% of total end-use demand in 2026. Aerospace is the most technically demanding and highest-value thermal spray application segment, with coating requirements spanning turbine blade TBCs, compressor abradable seals, landing gear wear coatings, and fuselage component corrosion protection, each requiring NADCAP-certified process qualification and material traceability.

The Aerospace Industries Association (AIA) reported that U.S. aerospace manufacturing shipments exceeded US$ 900 billion in 2023, with a significant portion of that value embedded in thermally sprayed components. Growing military aviation investment, with the U.S. Department of Defense (DoD) allocating over US$ 258 billion in FY2024 for research, development, test, and procurement, sustains high-specification aerospace thermal spray demand independent of commercial aviation cycles.

Regional Analysis

North America Thermal Spray Coatings Market Trends and Insights

North America led the thermal spray coatings market with approximately 29% global market share in 2026, underpinned by the world's largest aerospace and defense industrial base, NADCAP accreditation infrastructure, high MRO expenditure, and leading R&D investment from institutions including NASA and DoD laboratories in next-generation coating technologies.

U.S. Thermal Spray Coatings Market Size

The U.S. accounts for approximately 88% of North American thermal spray coatings revenue, anchored by a dense aerospace and defense manufacturing ecosystem, the DoD's FY2024 US$ 258 billion+ procurement budget, and headquarters of major suppliers Praxair Surface Technologies, Kennametal Stellite, and ASB Industries, Inc., serving leading OEM and MRO clients.

Europe Thermal Spray Coatings Market Trends and Insights

Europe represents the second-largest market, shaped by leading aerospace OEMs, Airbus, Rolls-Royce, and Safran, and stringent EU REACH and RoHS regulations driving chrome-free coating innovation. Germany, the U.K., and France host world-class thermal spray R&D and service facilities. Oerlikon Metco (Switzerland) and Sulzer (Switzerland) are major European-headquartered coating technology leaders.

Germany Thermal Spray Coatings Market Size

Germany leads European thermal spray adoption, supported by its world-class automotive, aerospace, and energy manufacturing industries. BMW Group, Volkswagen AG, and MTU Aero Engines are major thermal spray consumers. Germany's Fraunhofer-Institut für Werkstoff- und Strahltechnik IWS conducts leading thermal spray R&D, driving domestic innovation and supplier development for high-value coating applications.

U.K. Thermal Spray Coatings Market Size

The U.K. thermal spray market is driven by Rolls-Royce Holdings plc's aero-engine manufacturing and BAE Systems' defense programs. TWI Ltd and Metallisation Ltd, both UK-headquartered, are prominent thermal spray technology suppliers. The UK's Aerospace Technology Institute (ATI) invests in next-generation coating R&D, supporting continued market growth in both aerospace and industrial turbine segments.

France Thermal Spray Coatings Market Size

France benefits from a strong aerospace and defense thermal spray demand base anchored by Safran, Thales Group, and Airbus SAS. France's DGA (Direction Générale de l'Armement) procurement programs drive consistent military aerospace coating demand. Saint-Gobain, headquartered in France, is a global thermal spray powder leader, reinforcing France's position as both a supply and demand market for advanced coating technologies.

Asia Pacific Thermal Spray Coatings Market Trends and Insights

Asia Pacific is the fastest-growing regional thermal spray coatings market at 7% CAGR (2026–2033), driven by rapid aerospace manufacturing growth in China, India, and Japan, massive industrial gas turbine installations for power generation, and expanding automotive and steel processing sectors. China's COMAC C919 commercial aircraft program and AVIC's military aerospace expansion are creating domestic demand for NADCAP-equivalent thermal spray certification infrastructure.

India Thermal Spray Coatings Market Size

India is a rapidly growing thermal spray market, driven by HAL (Hindustan Aeronautics Limited) aircraft manufacturing, DRDO defense programs, and the PLI Scheme for Defence worth ?18,924 crore. India's expanding power generation sector, adding 50+ GW annually per Ministry of Power targets, is driving industrial gas turbine coating demand across BHEL and GE Power India facilities.

Japan Thermal Spray Coatings Market Size

Japan maintains a premium thermal spray coatings market driven by precision engineering demands from Mitsubishi Heavy Industries (MHI), IHI Corporation, and Kawasaki Heavy Industries in aerospace and industrial gas turbines. Japan's advanced automotive sector, led by Toyota, Honda, and Nissan, drives thermal spray demand for engine and powertrain component coatings, reinforcing consistent high-value market demand.

Southeast Asia Thermal Spray Coatings Market Size

Southeast Asia is an emerging thermal spray market, with Singapore's aerospace MRO hub, including ST Engineering and SIA Engineering Company, driving precision coating demand. Vietnam and Thailand's growing automotive and electronics manufacturing sectors are creating new thermal spray applications for wear-resistant and electrical insulation coatings, attracting investment from Linde and Oerlikon Metco in regional service expansion.

Competitive Landscape

The global thermal spray coatings market is moderately consolidated, with Oerlikon Metco, Praxair Surface Technologies (a Linde company), Bodycote, Sulzer, and Saint-Gobain commanding significant global market positions. Key competitive differentiators include NADCAP-certified process capabilities, proprietary powder chemistries (Höganäs AB's metal powder portfolios), global service center networks, and advanced suspension plasma spray (SPS) and solution precursor plasma spray (SPPS) R&D capabilities.

Emerging trends include cold spray additive manufacturing applications, digital coating process monitoring platforms, and sustainability-driven chrome replacement coating programs aligned with EU REACH compliance mandates.

Key Developments:

- In April 2025, Oerlikon Metco announced the commercial launch of its SUME-Arc™ advanced electric arc spray solution optimized for large-structure corrosion protection in offshore energy and bridge infrastructure applications, expanding its addressable market beyond traditional aerospace and industrial gas turbine segments.

- In October 2024, Linde expanded its Asia Pacific thermal spray gas supply infrastructure, commissioning three new HVOF-grade nitrogen and oxygen production facilities in India, Vietnam, and Indonesia to serve rapidly growing regional aerospace and industrial coating service demand.

- In February 2024, Bodycote announced the acquisition of a NADCAP-certified plasma spray coating facility in Monterrey, Mexico, expanding its North American aerospace thermal spray capacity to serve OEM and MRO customers across the U.S., Canada, and Mexico.

Companies Covered in Thermal Spray Coatings Market

- Praxair Surface Technologies

- Bodycote

- Oerlikon Metco

- Curtiss-Wright Surface Technologies

- Sulzer

- Kennametal Stellite

- Metallisation Ltd

- Linde

- Saint-Gobain

- TWI Ltd

- Höganäs AB

- H.C. Starck

- Plasma-Tec, Inc.

- ASB Industries, Inc.

- American Roller Company

Frequently Asked Questions

The global thermal spray coatings market is expected to be valued at US$ 13.2 billion in 2026, growing from US$ 9.6 billion in 2020, and projected to reach US$ 20.2 billion by 2033 at a forecast CAGR of 6.3%, with an absolute dollar opportunity of US$ 7.0 billion through the forecast period.

Key drivers include Airbus's forecast of commercial aircraft fleet doubling to 46,000 aircraft by 2042, IATA's US$ 100 billion+ annual MRO expenditure, IEA-projected gas turbine capacity expansion through 2030, and DoD FY2024 US$ 258 billion+ procurement sustaining defense aerospace thermal spray coating demand.

North America leads with approximately 29% global market share in 2026, driven by the world's largest aerospace and defense manufacturing base, NADCAP certification infrastructure, and headquarters of leading suppliers.

The most significant opportunities include abradable coatings growing at 7% CAGR driven by ICAO CORSIA and EASA engine efficiency mandates, and Asia Pacific industrial expansion through China's 14th Five-Year Plan, India's PLI Defence Scheme, and Linde's Asia gas infrastructure buildout supporting regional coating service growth.

Leading companies include Oerlikon Metco, Praxair Surface Technologies (Linde), Bodycote, Sulzer, Saint-Gobain, Curtiss-Wright Surface Technologies, TWI Ltd, Metallisation Ltd, and Höganäs AB, competing through NADCAP-certified process portfolios, proprietary powder chemistries, global MRO service networks, and next-generation cold spray and suspension plasma spray capabilities.