- Inks, Coatings, Adhesives & Sealants (ICAS)

- U.S. Paints and Coatings Market

U.S. Paints and Coatings Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Paints and Coatings Market by Resin Type (Acrylic, Alkyd, Polyurethane, Epoxy, Polyester, Others), Technology (Waterborne, Solvent-borne, Powder Coating, Others), End-user (Architectural, Automotive, Wood, Protective Coatings, General Industrial, Transportation, Packaging), and Regional Analysis, 2026 - 2033

U.S. Paints and Coatings Market Size and Trend Analysis

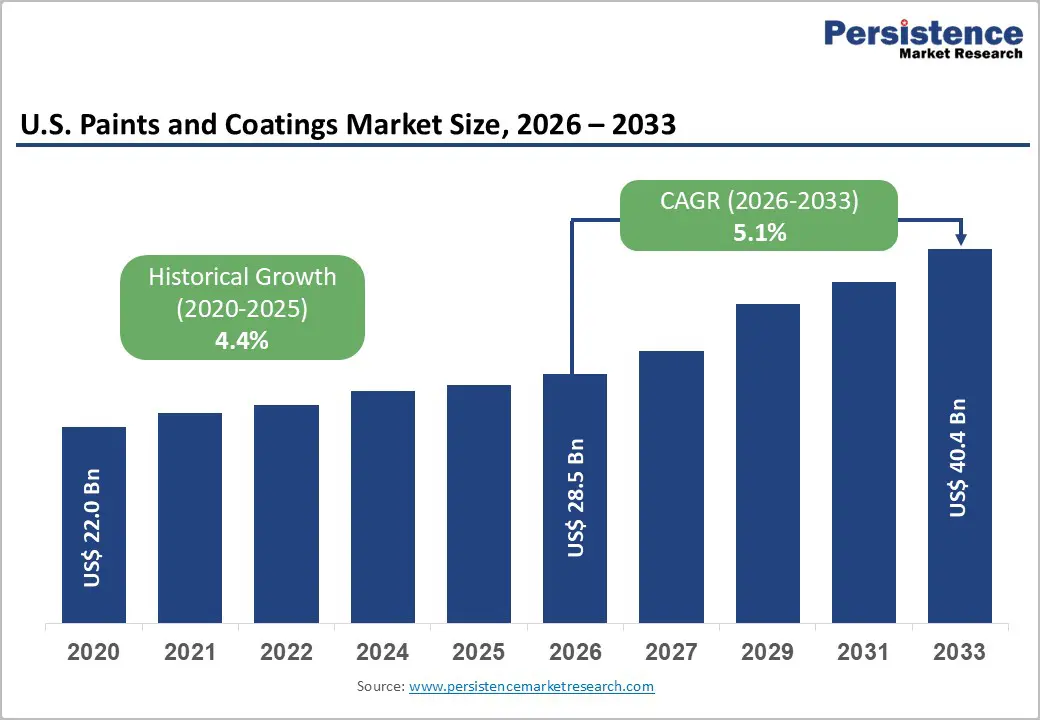

The U.S. paints and coatings market size is expected to be valued at US$ 28.5 billion in 2026 and projected to reach US$ 40.4 billion by 2033, growing at a CAGR of 5.1% between 2026 and 2033. This steady expansion is fundamentally anchored in robust demand from the architectural coatings segment, driven by sustained residential construction activity, renovation spending, and a regulatory push toward low-VOC and waterborne formulations.

The U.S. Census Bureau reported over 1.4 million new residential housing starts in recent periods, directly supporting architectural paint demand. Simultaneously, the resurgence of U.S. manufacturing investment, accelerated by the Infrastructure Investment and Jobs Act (IIJA) and the CHIPS and Science Act, is generating durable demand for industrial, protective, and epoxy coatings across infrastructure, semiconductor fabrication, and transportation asset classes.

Key Industry Highlights:

- Leading Region: The West U.S. leads the paints and coatings market with 31% share in 2026, driven by California's construction activity, CARB-compliant waterborne formulation adoption, and semiconductor facility construction generating specialty epoxy coatings demand.

- Fast-Growing Market: The Southeast U.S. is the fastest-growing region, supported by the nation's highest residential construction rates in Florida, Texas, and Georgia, plus manufacturing reshoring investment generating sustained industrial and protective coatings demand.

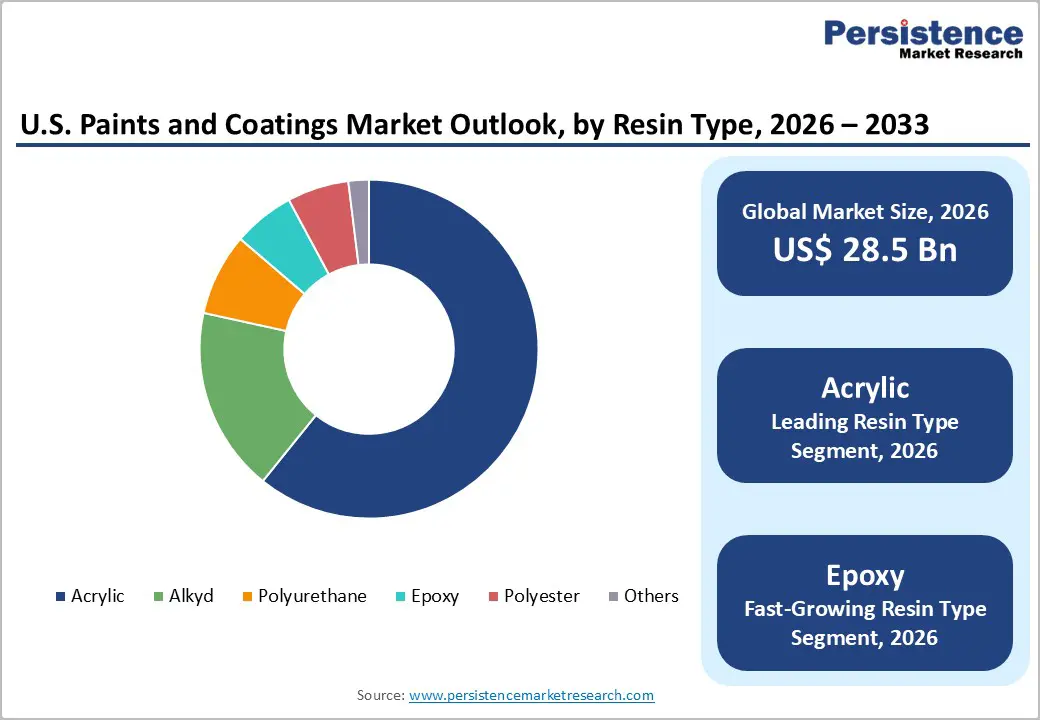

- Dominant Resin Type: Acrylic resins dominate with a 62% market share in 2026, reflecting their versatility, UV stability, VOC-compliance compatibility in waterborne formulations, and central role in premium architectural, automotive, and industrial coating product lines.

- Fast-Growing Resin Type: Epoxy coatings are the fastest-growing resin segment at 7% CAGR (2026 - 2033), driven by EV manufacturing, CHIPS Act semiconductor facility construction, and offshore wind infrastructure requiring high-performance corrosion-resistant coating systems.

- Key Opportunity: Powder coatings offer the highest growth potential as a zero-VOC, high-efficiency alternative, with conversion from solvent-borne systems accelerating across appliance, HVAC, architectural aluminum, and expanding heat-sensitive substrate applications through 2033.

DRO Analysis

Drivers - Infrastructure Investment and Federal Construction Stimulus Generating Protective Coatings Demand

Federal infrastructure investment acts as a demand catalyst for the U.S. paints and coatings market, particularly for protective and industrial coating segments. The Infrastructure Investment and Jobs Act (IIJA) allocated US$ 1.2 trillion over five years starting in 2022, with significant portions directed toward bridges, highways, water infrastructure, and public transit systems, all of which require high-performance protective coatings to extend asset service life.

The American Institute of Steel Construction (AISC) estimates that protective coatings account for up to 15-20% of total steel structure maintenance costs, making coating selection a critical capital expenditure decision. The project pipeline generated by IIJA disbursements is expected to sustain multi-year demand for epoxy, polyurethane, and zinc-rich primer systems across bridge and infrastructure applications through the forecast period.

Residential Renovation and Remodeling Activity Anchoring Architectural Coatings Demand

The U.S. home renovation and remodeling market remains a dominant and countercyclical demand driver for architectural paints and coatings. The Harvard Joint Center for Housing Studies (JCHS) projected U.S. homeowner improvement and repair spending at approximately US$ 450 billion annually, with interior and exterior paint consistently ranking among the top three renovation expenditures.

The aging U.S. housing stock, over 50% of homes were built before 1980, per the U.S. Census Bureau, creates a structural maintenance-driven demand base that is largely insulated from new construction cycles. Premium paint brands such as Sherwin-Williams and Benjamin Moore have benefited from rising per-square-foot spending as homeowners upgrade to higher-quality, durable, and low-VOC formulations in both DIY and professional applicator channels.

Restraints - VOC Regulatory Compliance Costs and Reformulation Burden

Stringent volatile organic compound (VOC) regulations imposed by the U.S. Environmental Protection Agency (EPA) and state-level agencies, particularly the California Air Resources Board (CARB), impose continuous reformulation costs on coatings manufacturers. CARB's Architectural Coatings Suggested Control Measure (SCM) sets increasingly stringent VOC limits requiring investment in low-VOC and zero-VOC binder and solvent systems.

Small and mid-size formulators face disproportionate compliance costs relative to large integrated producers such as PPG Industries and Sherwin-Williams, creating competitive disadvantages and constraining formulation flexibility in solvent-borne product lines.

Raw Material Price Volatility for Titanium Dioxide and Petrochemical-Derived Inputs

Titanium dioxide (TiO2), the primary opacity-providing pigment in paints, and petrochemical-derived monomers and solvents are subject to significant global price volatility. TiO2 pricing is heavily influenced by the supply strategies of dominant global producers, including Chemours and Tronox.

Supply chain disruptions, energy cost spikes in European production hubs, and demand variability from Asia have resulted in periodic TiO2 price surges of 20-35% within single fiscal years. For commodity paint manufacturers operating on thin margins, this input cost volatility directly compresses profitability and limits the ability to maintain retail price competitiveness.

Opportunities - Epoxy Coatings Demand from EV Manufacturing, Semiconductor, and Renewable Energy Infrastructure

The epoxy coatings segment, the fast-growing resin type at a projected 7% CAGR, is propelled by convergent demand from three high-growth U.S. industrial sectors. The electric vehicle manufacturing buildout, anchored by investments from Tesla, GM, and Ford in new U.S. gigafactories, requires epoxy-based coatings for battery enclosures, underbody protection, and thermal management components.

The CHIPS and Science Act's US$ 52 billion commitment to domestic semiconductor fabrication has generated a pipeline of cleanroom and industrial facility construction requiring specialty chemical-resistant epoxy floor and wall coating systems. Offshore wind turbine foundation and tower coatings, supported by the Inflation Reduction Act (IRA) incentives, represent a structurally new, high-value epoxy corrosion protection application for coatings companies, including Hempel A/S and PPG Industries.

Powder Coatings as a Sustainable Technology Solution for Industrial and Architectural Applications

Powder coatings represent one of the most commercially compelling growth opportunities in the U.S. market, combining zero-VOC compliance with superior durability, material utilization efficiency (overspray recapture rates exceeding 95%), and reduced energy consumption relative to liquid coatings. The Powder Coating Institute (PCI) has reported consistent year-on-year conversion from solvent-borne to powder systems in U.S. metal fabrication, appliance, and architectural aluminum extrusion applications.

The penetration of low-cure and ultra-low-cure powder technologies, enabling application to heat-sensitive substrates including wood composite and plastics, is widening the addressable market significantly. Axalta Coating Systems and Akzo Nobel have expanded U.S. powder coating capacity in response to growing OEM and contract coating demand, particularly from the appliance, HVAC, and architectural hardware segments, where sustainability procurement requirements are accelerating technology transition.

Category-wise Analysis

Resin Type Insights

Acrylic resins dominate the U.S. paints and coatings market with an estimated 62% share in 2026, reflecting their unparalleled versatility across architectural, automotive, and industrial coating applications. Acrylic's leadership stems from its superior weathering resistance, UV stability, adhesion performance, and compatibility with waterborne formulation technology.s

The American Coatings Association (ACA) has consistently noted acrylic resins as the backbone of the U.S. architectural paint market, where both interior latex and exterior masonry formulations are predominantly acrylic based. Major producers including The Sherwin-Williams Company, PPG Industries, and Benjamin Moore anchor their premium product lines on advanced acrylic polymer platforms, reinforcing the segment's dominant commercial position through the forecast period.

Technology Insights

Waterborne coatings are the leading technology segment in the U.S. paints and coatings market, accounting for an estimated 55% share in 2026. Their dominance is driven by regulatory compulsion, the EPA's National Emission Standards for Hazardous Air Pollutants (NESHAP) and CARB's increasingly stringent VOC limits have structurally shifted formulation strategy toward water as the primary carrier medium across architectural, wood, and light industrial applications.

Waterborne formulations offer additional commercial advantages including faster dry times, lower odor, and easy soap-and-water cleanup that resonate with both professional contractors and DIY consumers. Wacker Chemie AG's dispersible polymer powder technologies and Sika AG's waterborne admixture systems illustrate the breadth of innovation in this segment. Powder coating is the fastest-growing technology, driven by zero-VOC compliance and expanding substrate applicability.

End-user Insights

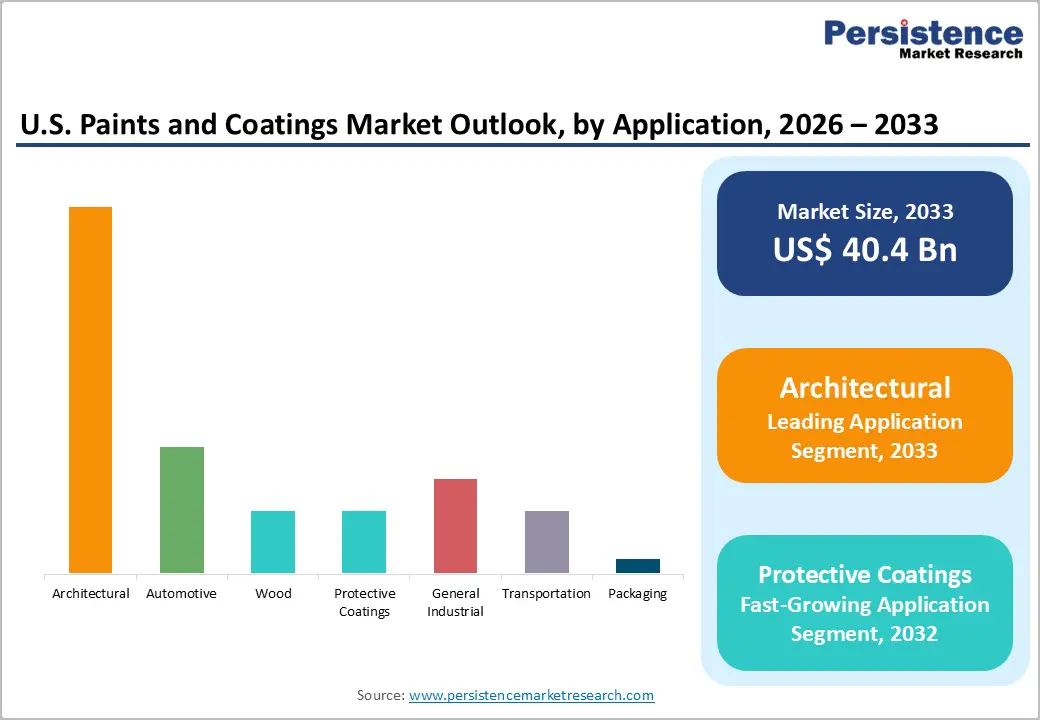

Architectural coatings are the dominant end-use segment in the U.S. market, capturing an estimated 46% share in 2026. This leadership is underpinned by the structural depth of U.S. residential and commercial construction activity, the maintenance-driven demand from a housing stock where the median age exceeds 40 years (per the U.S. Census Bureau), and the broad consumer market for DIY interior and exterior repainting.

The American Coatings Association (ACA) reports that architectural paint and coatings represent the largest single volume category in the U.S., with professional applicators and home improvement retail channels, led by The Home Depot and Lowe's, serving as the primary distribution backbone. Protective coatings is the fastest-growing end-use segment, driven by infrastructure investment and industrial manufacturing expansion.

Regional Analysis

West U.S. Paints and Coatings Market Trends and Insights

The West U.S. region leads the national paints and coatings market with an estimated 31% share in 2026, anchored by California's position as the largest single-state construction and renovation market in the U.S. California's stringent CARB VOC regulations function as a national formulation bellwether, driving waterborne and zero-VOC technology adoption that subsequently propagates across other U.S. regions. The state's sustained residential construction activity in the Bay Area, Los Angeles Basin, and Phoenix metro corridor support consistent architectural coatings demand.

The West's concentration of semiconductor fabrication (Intel, TSMC Arizona), data center construction, and emerging offshore wind development off the Pacific and Gulf Coast creates specialist demand for chemical-resistant epoxy and high-performance protective coating systems. Companies such as Sherwin-Williams and Kelly-Moore Paints maintain strong regional distribution networks serving both trade professional and DIY channels across Western states.

Southeast U.S. Paints and Coatings Market Trends and Insights

The Southeast U.S. is the fast-growing regional market for paints and coatings, supported by the highest rate of new residential construction in the country, states including Florida, Texas, Georgia, and North Carolina consistently rank among the top U.S. states for building permits, per U.S. Census Bureau data. The region's humid subtropical climate drives high demand for mildew-resistant, high-durability exterior architectural coatings with enhanced weathering performance.

The Southeast is also a major beneficiary of U.S. manufacturing reshoring investment, with automotive assembly plants (Toyota, Hyundai, BMW), aerospace facilities, and industrial warehousing generating sustained industrial and protective coatings demand. RPM International Inc. and Sherwin-Williams have expanded distribution and manufacturing presence across the region, recognizing its outsized contribution to U.S. coatings volume growth through 2033.

Midwest U.S. Paints and Coatings Market Trends and Insights

The Midwest U.S. represents U.S. paints and coatings industry, with demand linked to automotive OEM production, heavy equipment manufacturing, metal fabrication, and agricultural equipment finishing, all concentrated in states including Michigan, Ohio, Indiana, and Illinois. The region is home to major automotive finishing operations for General Motors, Ford, and Stellantis, creating consistent demand for electrocoat primers, basecoat-clearcoat systems, and plastic substrate coatings.

Axalta Coating Systems and PPG Industries maintain significant OEM coatings supply relationships across Midwest auto assembly plants. The region's infrastructure renewal under IIJA, focused on bridge rehabilitation and industrial port modernization along the Great Lakes, is generating a new demand vector for anti-corrosion protective coating systems, further diversifying the Midwest coatings demand profile beyond automotive into infrastructure asset management.

Competitive Landscape

The U.S. paints and coatings market is moderately consolidated at the top, with Sherwin-Williams, PPG Industries, and Akzo Nobel collectively commanding significant volume and revenue share. Key competitive differentiators include proprietary resin technology, national retail distribution infrastructure, and OEM supply relationships.

3M and BASF SE compete in specialty segments through materials science innovation. Emerging trends include sustainability-linked product lines (low-VOC, bio-based), digital color-matching services, and DTC e-commerce. Masco Corporation and RPM International leverage brand portfolios across professional and consumer segments to defend market breadth.

Key Developments:

- In 2025, Sherwin-Williams announced capacity expansion at its U.S. manufacturing facilities to meet growing demand for low-VOC architectural and industrial coatings, with investments focused on waterborne formulation lines supporting EPA and CARB compliance requirements across professional trade channels.

- In 2024, PPG Industries launched its next-generation ENVIROCRON™ powder coating line for aerospace and industrial applications, targeting the growing U.S. manufacturing sector with enhanced chemical resistance and zero-VOC performance, reflecting the industry shift toward sustainable coating technologies.

- In 2024, Axalta Coating Systems expanded its U.S. EV coatings portfolio with new battery pack protection and thermal barrier coating systems, positioning itself for growing demand from domestic electric vehicle manufacturing facilities in the Southeast and Midwest regions.

U.S. Paints and Coatings Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 22.0 Billion |

| Current Market Value (2026) | US$ 28.5 Billion |

| Projected Market Value (2033) | US$ 40.4 Billion |

| CAGR (2026 - 2033) | 5.1% |

| Leading Region | West U.S., 31% market share (2026) |

| Dominant Resin Type (Category-1) | Acrylic, 62% market share (2026) |

| Top-ranking Technology (Category-2) | Waterborne, 55% market share (2026) |

| Incremental Opportunity (2026 - 2033) | US$ 11.9 Billion |

Companies Covered in U.S. Paints and Coatings Market

- Akzo Nobel N.V.

- Axalta Coatings Systems

- PPG Industries, Inc.

- Benjamin Moore & Co.

- RPM International Inc.

- Masco Corporation

- The Sherwin-Williams Company

- Parker Hannifin Corp.

- Diamond Vogel

- Kelly-Moore Paints

- Wacker Chemie AG

- Sika AG

- Hempel A/S

Frequently Asked Questions

The U.S. paints and coatings market is expected to be valued at US$ 28.5 billion in 2026 and is projected to reach US$ 40.4 billion by 2033, expanding at a forecast CAGR of 5.1%.

The primary demand drivers are the Infrastructure Investment and Jobs Act (IIJA), which is generating substantial demand for protective and industrial coating across bridges and infrastructure assets, and sustained residential renovation spending.

The West U.S. leads the national paints and coatings market with approximately 31% market share in 2026. California’s stringent CARB VOC regulations sustained residential construction activity, and growing semiconductor facility and renewable energy infrastructure investment collectively drive the region's leadership in both architectural and specialty industrial demand.

The key growth opportunities are epoxy coatings for EV manufacturing, semiconductor facilities (CHIPS Act), and offshore wind infrastructure, growing at 7% CAGR (2026 - 2033), and powder coatings as a zero-VOC technology substitution opportunity across metal fabrication, appliance, HVAC, and architectural aluminum applications, where sustainability procurement mandates are accelerating solvent-borne conversion.

The leading companies in the U.S. paints and coatings market include The Sherwin-Williams Company, PPG Industries Inc., Akzo Nobel N.V., Axalta Coating Systems, Benjamin Moore & Co. (Berkshire Hathaway), RPM International Inc., BASF SE, Hempel A/S, Sika AG, Wacker Chemie AG, Masco Corporation, 3M, Diamond Vogel, and Kelly-Moore Paints, among others.