- Inks, Coatings, Adhesives & Sealants (ICAS)

- Blended Cement Market

Blended Cement Market Size, Share, and Growth Forecast, 2026 - 2033

Blended Cement Market by Product Type (Portland Pozzolana Cement (PPC), Portland Slag Cement (PSC), Others), Application (Cast-in-Place Construction, Precast Construction), End-user Industry, and Regional Analysis for 2026 - 2033

Blended Cement Market Size and Trends Analysis

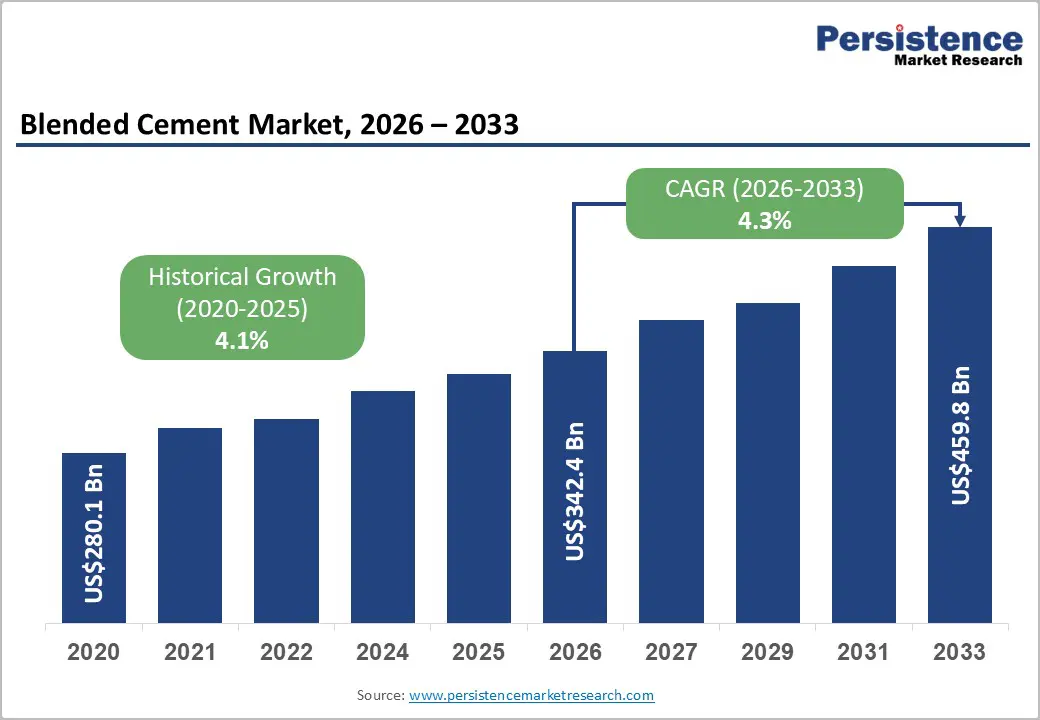

The global blended cement market size is likely to be valued at US$342.4 billion in 2026 and is expected to reach US$459.8 billion by 2033, growing at a CAGR of 4.3% between 2026 and 2033, driven by the increasing adoption of lower-clinker cement formulations, rising use of supplementary cementitious materials (SCMs), and growing regulatory pressure to reduce carbon emissions from the construction sector.

Governments and infrastructure agencies are encouraging the use of low-carbon building materials through procurement standards and sustainability frameworks. Demand growth is also being supported by long-term investments in residential housing, transportation infrastructure, industrial development, and urbanization across emerging economies.

Key Industry Highlights:

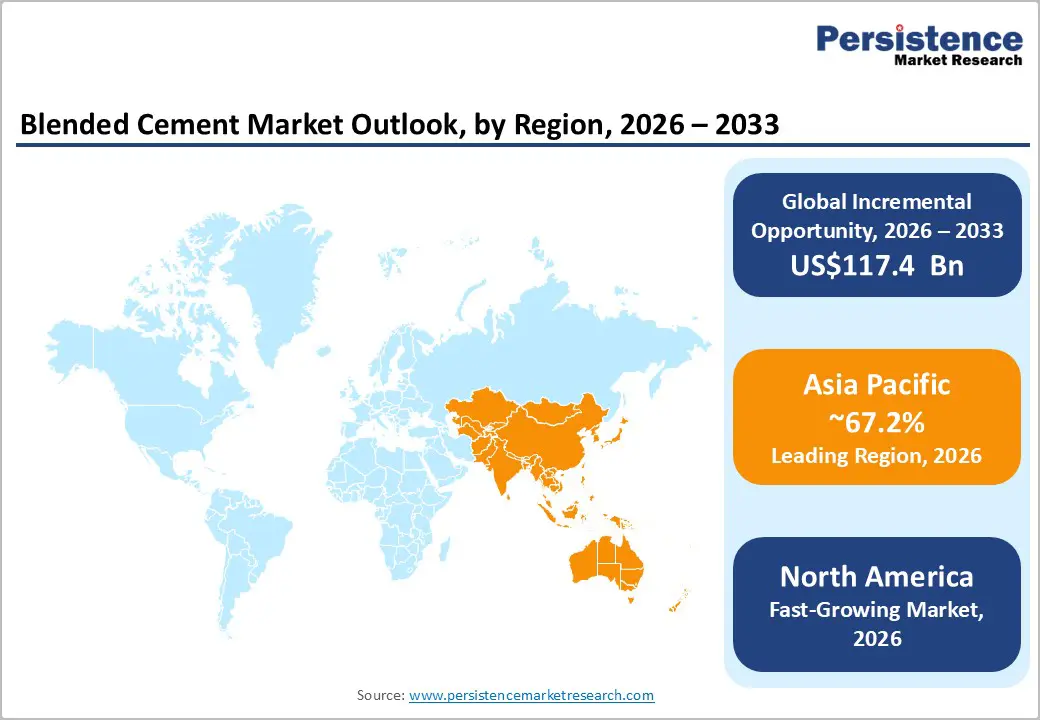

- Leading Region: Asia Pacific is projected to account for approximately 67.2% market share in 2026, supported by large-scale infrastructure development, strong cement manufacturing capacity, and high blended cement penetration across China and India.

- Fastest-growing Region: North America is projected to be the fastest-growing regional market, driven by low-carbon construction policies, rising adoption of Portland Limestone Cement (PLC), and increasing investment in sustainable infrastructure projects.

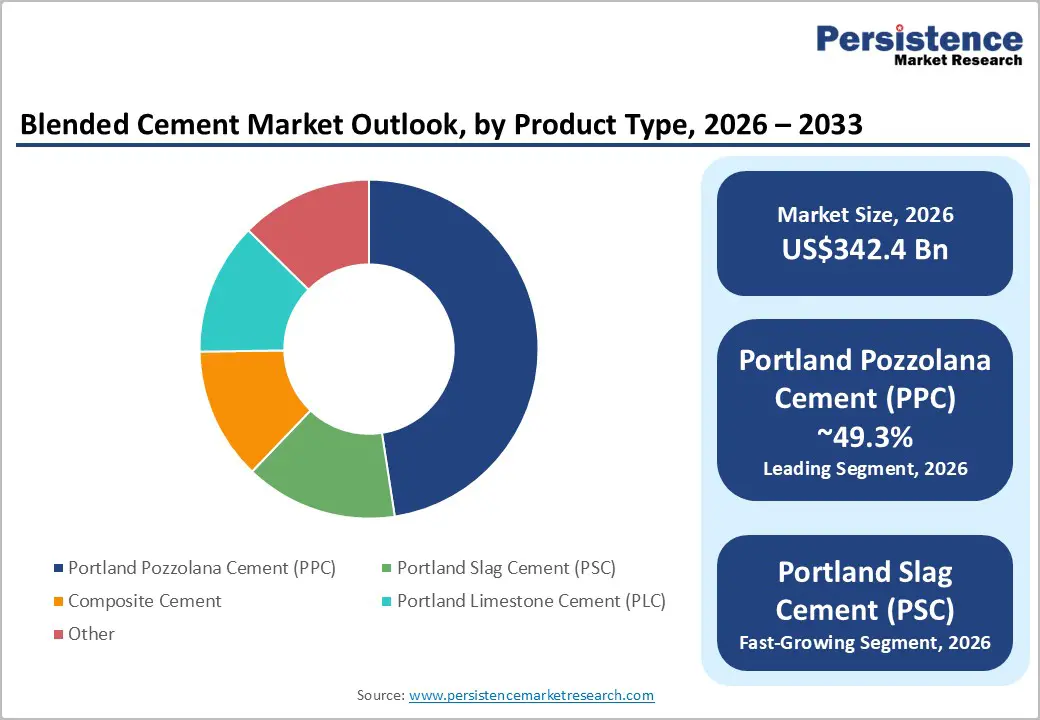

- Dominant Product Type: Portland Pozzolana Cement (PPC) is estimated to lead with approximately 49.3% market share in 2026, driven by lower clinker intensity, cost efficiency, improved durability, and widespread adoption across residential and infrastructure construction.

- Leading Application: Cast-in-place construction is anticipated to account for 60.4% of market share in 2026, supported by extensive use in residential buildings, highways, bridges, commercial structures, and public infrastructure projects.

DRO Analysis

Drivers - Decarbonization Policies Are Accelerating Adoption of Blended Cement

One of the strongest growth drivers for the blended cement market is the global push to reduce carbon emissions from construction materials. Cement manufacturing contributes significantly to industrial CO2 emissions, as clinker production is energy-intensive. As a result, governments and industry regulators are encouraging the use of blended cement formulations that reduce clinker content while maintaining structural performance.

International energy and construction agencies continue to identify clinker substitution through fly ash, slag, limestone, and pozzolanic materials as one of the most practical pathways for lowering emissions from cement manufacturing. Performance-based standards are also gaining importance because they allow broader use of low-clinker products in commercial and infrastructure projects.

In the U.S., federal programs supporting low-carbon construction materials have increased demand for blended cement in roads, bridges, and public infrastructure. Similar sustainability frameworks are emerging across Europe and the Asia Pacific. These regulatory shifts are transforming blended cement from a cost-efficiency product into a compliance-oriented construction material. Producers with lower-carbon product portfolios are expected to gain stronger access to government-funded infrastructure projects and green construction programs.

Infrastructure Expansion and Urbanization Continue to Support Demand

Global demand for blended cement remains closely linked to construction activity, particularly in residential housing, transportation infrastructure, industrial development, and public works projects. Urbanization across developing economies continues to create long-term demand for roads, metros, airports, ports, water systems, and commercial buildings.

In the U.S., construction spending maintained steady growth in 2024, while cement demand remained closely tied to ready-mix concrete applications. Infrastructure modernization programs are increasing the need for durable and cost-efficient cement products suitable for highways, tunnels, bridges, and rail projects.

India remains one of the largest long-term demand centers for blended cement, driven by rapid urban expansion, affordable housing initiatives, and industrial corridor development. Housing still accounts for the majority of cement consumption in the country, while infrastructure spending is steadily increasing its share. Similar trends are evident across Southeast Asia, the Middle East, and parts of Africa, where population growth and urban migration are driving new construction.

Restraint - Limited Availability of SCMs and Regional Logistics Challenges

Despite strong demand growth, the blended cement market faces structural challenges related to the availability and transportation of supplementary cementitious materials. Fly ash, slag, and other SCMs are often concentrated near thermal power plants and steel manufacturing facilities, creating regional supply imbalances.

Portland Slag Cement production depends heavily on access to blast furnace slag generated by steel plants. Similarly, fly ash availability is tied to coal-based power generation. As countries gradually transition toward renewable energy, the long-term availability of certain SCMs may become constrained.

Transportation also remains a major issue because cement and SCMs are low-value bulk materials with high freight sensitivity. Long-distance transportation increases operating costs and reduces profitability. In many regions, outdated standards and prescriptive building codes continue to limit wider adoption of blended cement formulations.

Opportunities - Public Procurement Policies Are Expanding Low-Carbon Cement Demand

Government procurement frameworks supporting sustainable construction materials are creating major growth opportunities for blended cement manufacturers. Public infrastructure agencies are increasingly prioritizing products with lower embodied carbon, particularly for transportation, institutional, and municipal projects. In North America, transportation agencies and environmental programs are supporting procurement of low-carbon concrete and cement through dedicated funding initiatives.

Public works contracts are increasingly incorporating environmental product declarations and carbon reporting requirements. Europe is also strengthening regulations related to carbon accounting, emissions transparency, and sustainable building materials. Carbon border adjustment mechanisms and climate-neutral construction roadmaps are encouraging broader adoption of blended cement across commercial and industrial projects.

These developments are expected to increase demand for cement products containing higher levels of SCMs, particularly Portland Limestone Cement, Portland Pozzolana Cement, and Composite Cement. Companies that can demonstrate measurable carbon reductions and consistent product quality are likely to gain a competitive advantage in government and infrastructure contracts.

Grinding Capacity Expansion and Localization Strategies Are Supporting Growth

The blended cement industry is witnessing increased investment in grinding facilities, regional distribution networks, and composite cement production lines. Grinding-based expansion strategies allow manufacturers to optimize transportation costs while tailoring cement blends according to locally available SCMs.

India has emerged as a major investment destination for expansion projects in the blended cement sector. Several leading manufacturers announced new clinker units, grinding facilities, debottlenecking programs, and regional expansion plans during 2025. These investments are intended to strengthen supply chain efficiency, improve regional market penetration, and support rising infrastructure demand.

Localized grinding infrastructure also allows producers to reduce freight costs, increase operational flexibility, and improve supply reliability for ready-mix and precast concrete customers. Companies with strong logistics capabilities and diversified SCM sourcing strategies are expected to improve profitability while strengthening their regional competitive positions.

Category-wise Analysis

Product Type Analysis

Portland Pozzolana Cement (PPC) is anticipated to lead, accounting for approximately 49.3% market share in 2026. The segment maintains dominance as PPC provides a balance between cost efficiency, durability, and lower carbon intensity compared to ordinary Portland cement. PPC contains pozzolanic materials such as fly ash, typically ranging between 15% and 35%. These materials improve long-term strength, reduce permeability, and enhance resistance against chemical attacks. PPC is widely used in hydraulic structures, marine applications, sewage systems, masonry works, dams, and residential construction.

The growing preference for environmentally sustainable construction materials is further supporting PPC demand. Manufacturers are increasing blending ratios to reduce clinker usage while improving operational efficiency and compliance with carbon reduction targets.

Portland Slag Cement (PSC) is expected to witness the fastest growth during the forecast period. PSC contains high proportions of blast furnace slag, often ranging between 35% and 67.2%, which significantly lowers carbon emissions while improving durability.

PSC performs particularly well in mass concrete applications, coastal infrastructure, bridges, tunnels, ports, and water-retaining structures due to its low heat of hydration and superior sulfate resistance. Rapid infrastructure development across the Asia Pacific and the Middle East is increasing demand for PSC in transportation and industrial projects. Composite cement and Portland Limestone Cement are also gaining traction because they enable higher clinker substitution rates and improved sustainability performance.

Application Insights

Cast-in-place construction is estimated to lead, accounting for approximately 60.4% of the market share. The segment dominates because most residential, commercial, and infrastructure projects continue to rely on on-site concrete mixing and placement.

Blended cement is widely used in foundations, columns, slabs, beams, retaining walls, highways, and industrial structures. Ready-mix concrete producers are among the largest customers of blended cement manufacturers, as cast-in-place construction requires high-volume concrete consumption. Governments across emerging economies continue to invest heavily in roads, rail networks, airports, ports, and smart city initiatives, further supporting demand for blended cement products in on-site applications.

Precast construction is projected to register the fastest growth due to rising demand for shorter construction timelines, improved quality control, and greater labor efficiency. Precast systems are increasingly used in residential buildings, industrial facilities, warehouses, transportation infrastructure, and modular construction projects.

Manufacturers prefer blended cement in precast applications because it offers consistent workability, durability, and long-term structural performance. The growing adoption of industrialized construction methods is expected to accelerate demand for high-performance blended cement formulations. Precast construction also aligns with sustainability objectives by reducing material waste, improving manufacturing precision, and lowering the overall construction time. As urban construction projects become more time-sensitive, demand for precast concrete solutions is expected to rise steadily.

Regional Insights

North America Blended Cement Market Trends

North America is projected to emerge as the fastest-growing regional market for blended cement during the forecast period. The region’s growth is being supported by low-carbon construction policies, infrastructure modernization programs, and rising adoption of Portland Limestone Cement (PLC). Governments and construction agencies across the region are encouraging the use of sustainable cement formulations to reduce embodied carbon emissions from buildings and infrastructure projects.

The region also benefits from a mature construction ecosystem, strong technical standards, advanced transportation infrastructure, and increasing collaboration between cement producers and environmental agencies. Demand for blended cement is expected to rise steadily as infrastructure replacement cycles accelerate across highways, bridges, transit systems, airports, and public utilities.

U.S. Blended Cement Market Trends

The U.S. remains the largest blended cement market in North America, driven by large-scale infrastructure spending and rising demand for sustainable construction materials. Blended cement adoption has expanded significantly across highways, bridges, institutional buildings, industrial projects, and transportation systems. Federal infrastructure programs and climate-focused procurement policies are encouraging broader use of low-carbon cement products. Government agencies are increasingly integrating environmental performance requirements into public construction contracts, particularly for transportation and public works projects.

Ready-mix concrete producers remain the dominant customer group for cement manufacturers, as cast-in-place construction remains highly prevalent across the U.S. market. Manufacturers are also increasing investments in slag grinding facilities, cement terminals, and regional logistics infrastructure to improve supply reliability and reduce freight costs. Demand for Portland Limestone Cement is growing rapidly because it offers lower carbon emissions while remaining compatible with existing construction methods and engineering standards.

Europe Blended Cement Market Trends

Europe represents a highly regulated and sustainability-focused blended cement market characterized by strict climate policies, carbon pricing mechanisms, and advanced construction standards. The region is prioritizing lower-carbon construction materials as part of broader decarbonization and circular economy strategies. Cement manufacturers across Europe are investing heavily in carbon capture technologies, alternative fuels, and the use of SCM to comply with long-term climate targets.

Readymix concrete remains the dominant application channel, while precast construction continues to expand steadily due to labor shortages, modular construction demand, and efficiency requirements.

Germany Blended Cement Market Trends

Germany remains one of the largest cement markets in Europe, driven by its strong industrial base and large-scale infrastructure modernization initiatives. Demand for blended cement is being driven by transportation upgrades, energy-efficient building renovations, and public infrastructure redevelopment.

The country’s aggressive climate policies are accelerating the adoption of lower-clinker cement products. German cement manufacturers are actively investing in carbon capture technologies, alternative fuel systems, and sustainable cement formulations to meet national and EU emissions targets.

U.K. Blended Cement Market Trends

The U.K. continues to see rising demand for blended cement driven by infrastructure expansion, transportation investments, and stricter environmental regulations. Sustainable construction practices are becoming increasingly important across residential, commercial, and institutional projects.

The U.K. government’s net-zero targets are encouraging the adoption of low-carbon cement products in highways, rail projects, public buildings, and urban redevelopment programs. Cement producers are also focusing on recycled materials, circular construction systems, and lower-emission manufacturing technologies.

Precast and modular construction applications are expanding rapidly across the U.K. market due to labor shortages and the need for faster project execution.

Long-term growth opportunities are expected to emerge from rail modernization, logistics infrastructure expansion, and energy transition projects.

Asia Pacific Blended Cement Market Trends

Asia Pacific continues to dominate the market, accounting for nearly 67.2% of the market share in 2026. The region benefits from massive infrastructure investment, rapid urbanization, industrial expansion, and large-scale cement manufacturing capacity. The market is supported by rising demand for residential housing, transportation infrastructure, industrial corridors, energy facilities, ports, airports, and smart city developments. Asia Pacific also benefits from proximity to key supplementary cementitious material sources such as fly ash and slag, which support large-scale blended cement production.

China Blended Cement Market Trends

China remains the world’s largest cement producer and consumer, accounting for nearly half of global cement production. The country maintains substantial cement demand across transportation systems, industrial facilities, ports, railways, and urban infrastructure projects. Although China’s real estate sector has moderated compared to earlier growth cycles, public infrastructure spending continues to support cement demand. Chinese manufacturers are increasingly focusing on lower-carbon cement production, energy-efficiency improvements, and emissions-reduction technologies.

India Blended Cement Market Trends

India represents the fastest-growing major blended cement market in Asia Pacific due to rapid urbanization, affordable housing demand, and expanding infrastructure investment. Government initiatives supporting highways, railways, metros, airports, industrial corridors, and smart cities are significantly increasing cement consumption.

Portland Pozzolana Cement and Portland Slag Cement remain widely used across residential and infrastructure applications because of their cost efficiency and lower carbon intensity. Indian cement manufacturers are aggressively expanding grinding capacity, regional distribution networks, and blended cement production capabilities.

Japan Blended Cement Market Trends

Japan’s blended cement market is primarily driven by infrastructure maintenance, earthquake-resistant construction, and sustainable building initiatives. The country continues to invest in transportation infrastructure upgrades, coastal protection systems, and resilient urban construction.

Japanese cement producers are focusing on energy efficiency, carbon reduction technologies, and advanced cement formulations. Demand for blended cement is also supported by redevelopment projects in major metropolitan regions and the ongoing modernization of aging infrastructure assets.

Competitive Landscape

The global blended cement market is moderately fragmented at the global level but highly competitive within regional markets. Large multinational cement producers compete alongside domestic manufacturers, regional grinding companies, and integrated construction material suppliers.

Leading manufacturers are focusing on capacity expansion, regional grinding infrastructure, clinker reduction, and sustainable product development. Companies are also increasing investments in logistics optimization, SCM sourcing partnerships, and carbon-efficient manufacturing technologies. The industry is gradually transitioning toward region-specific blended cement portfolios designed around local raw material availability and sustainability requirements.

Key Industry Developments:

- In April 2025, Ambuja Cements announced that it had crossed 100 MTPA cement production capacity following the commissioning of a 2.4 MTPA brownfield grinding expansion at Farakka, West Bengal, along with debottlenecking initiatives across multiple plants.

- In March 2025, UltraTech Cement completed the acquisition of Kesoram Industries' cement business, adding 10.75 MTPA of cement capacity across Karnataka and Telangana.

Companies Covered in Blended Cement Market

- Holcim

- Heidelberg Materials

- CNBM (China National Building Material Company)

- Anhui Conch Cement

- UltraTech Cement

- Cemex

- CRH

- Ambuja Cements

- Shree Cement

- Dalmia Bharat

- Buzzi

- Taiheiyo Cement

- Taiwan Cement Corporation

- Votorantim Cimentos

- Titan Cement Group

- Siam Cement Group (SCG)

Frequently Asked Questions

The global blended cement market is estimated to be valued at US$342.4 billion in 2026.

The global blended cement market is projected to reach approximately US$459.8 billion by 2033.

Key trends shaping the blended cement market include rising adoption of low-clinker and low-carbon cement formulations, increasing use of Portland Limestone Cement (PLC), and Portland Slag Cement (PSC).

Portland Pozzolana Cement (PPC) is the leading product segment, accounting for approximately 49.3% of the market share due to its cost-efficiency, durability, and lower carbon intensity compared to conventional cement products.

The blended cement market is projected to grow at a CAGR of 4.3% between 2026 and 2033.

Major companies include Holcim, Heidelberg Materials, UltraTech Cement, Ambuja Cements, and Cemex.