- Technology

- Smart Rings Market

Smart Rings Market Size, Share, and Growth Forecast 2026 - 2033

Smart Rings Market by Operating System (Android, iOS, Cross-Platform), by Technology (Bluetooth-enabled, NFC-enabled, Hybrid Smart Rings), by Application (Health & Wellness Monitoring, Contactless Payments, Notifications & Communication, Security & Access Control, Smart Home Control, Data Transfer), End-user (Fitness Enthusiasts, Healthcare Users, Tech-savvy Consumers, Enterprise Users), and Regional Analysis, 2026 - 2033

Smart Rings Market Size and Trend Analysis

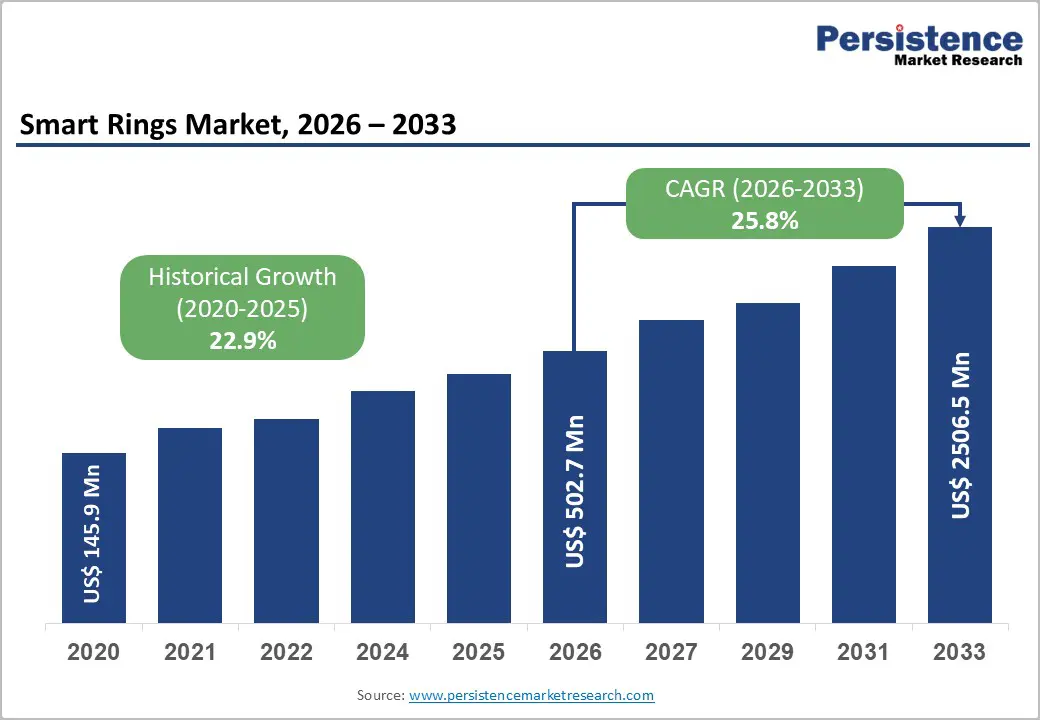

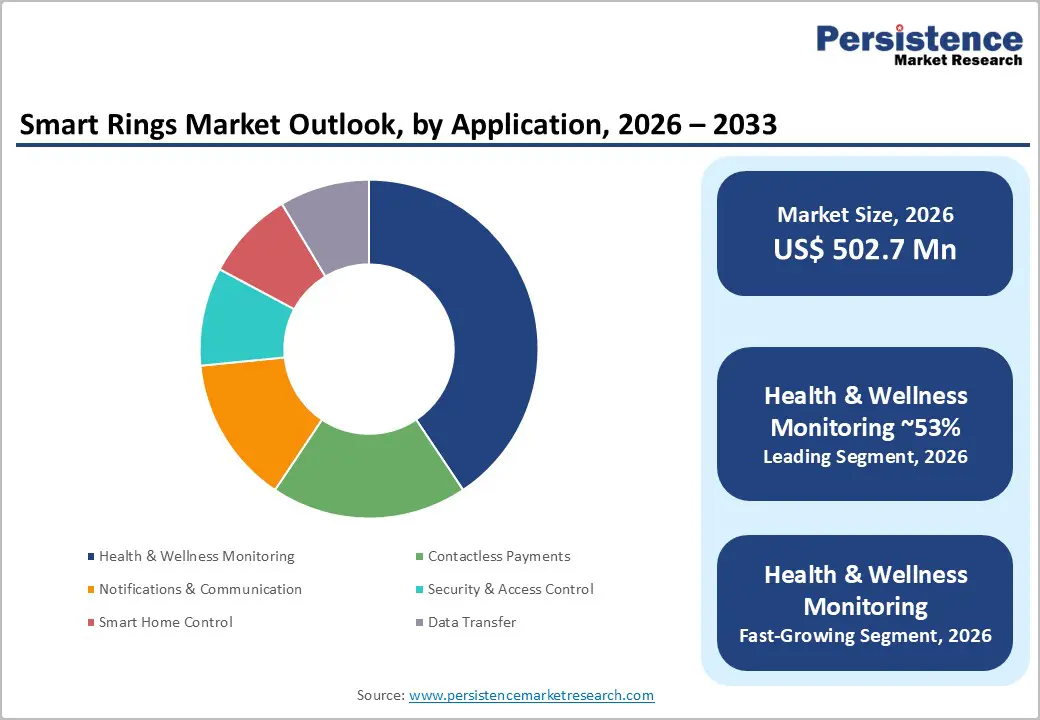

The global smart rings market size is likely to be valued at US$ 502.7 million in 2026 and is expected to reach US$ 2,506.5 million, growing at a CAGR of 25.8% during the forecast period from 2026 to 2033.

It is experiencing exceptional hyper-growth driven by a powerful convergence of consumer health and wellness prioritization, the miniaturization of biometric sensor technology enabling clinical-grade health monitoring in a discreet ring form factor, and the rapid consumer adoption of wearable health devices beyond conventional smartwatches.

Key Industry Highlights:

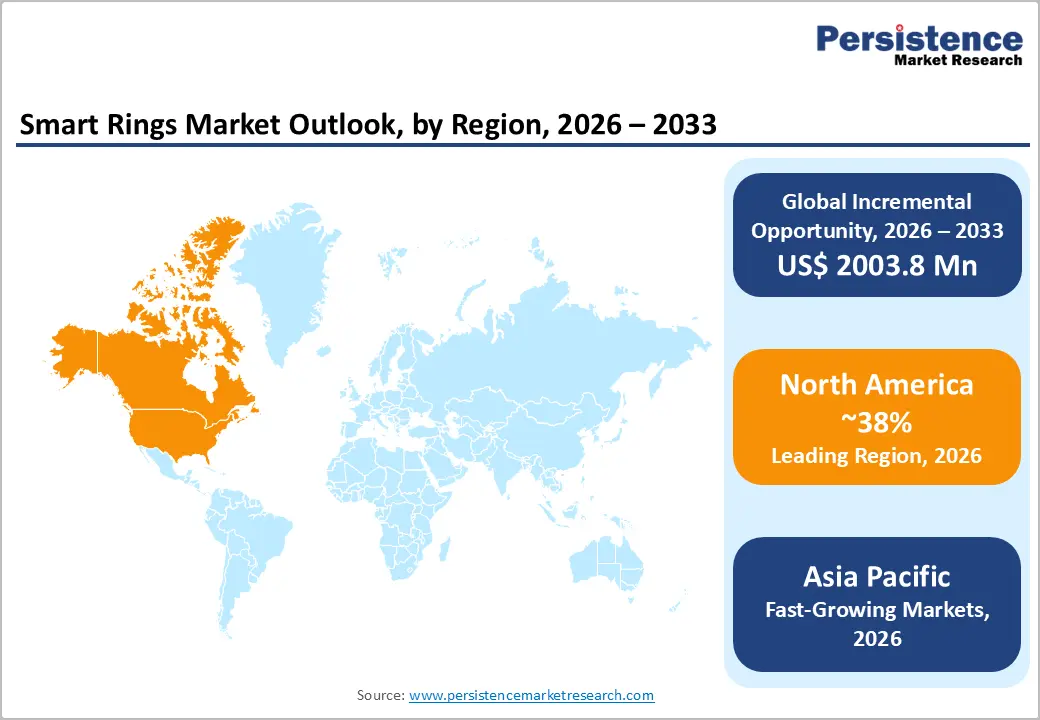

- Leading Region: North America, led by the United States, dominates the global Smart Rings Market holding 38% share, home to pioneer Oura Health with over 2.5 Million active users, the FDA’s Digital Health Center of Excellence enabling medical-grade product development, and the CDC’s documented 6-in-10 U.S. adults with chronic disease creating strong continuous monitoring demand.

- Fast-Growing Market: Asia Pacific is the fastest-growing regional market, driven by Samsung Galaxy Ring’s dominant brand presence in South Korea, Southeast Asia, and India, China’s cost-competitive domestic smart ring brands, and India’s booming digital health ecosystem under the Ayushman Bharat Digital Mission (ABDM).

- Dominant Segment: Health & Wellness Monitoring leads the Application category with approximately 52% market share, anchored by Oura Health’s peer-reviewed clinical studies validating ring-based sleep staging and biometric accuracy, and the WHO’s documented 74% share of global deaths attributable to non-communicable diseases, driving continuous health monitoring demand.

- Fast-Growing End-user Segment: Healthcare Users are the fastest-growing end-user segment, propelled by Movano Health’s FDA 510(k)-cleared Evie Ring establishing a medical device precedent, the CMS multi-billion-dollar remote patient monitoring reimbursement program, and the global aging population’s accelerating demand for continuous passive health surveillance tools.

- Key Opportunity: FDA-cleared clinical-grade smart ring features, targeting the CMS-validated multi-billion-dollar remote patient monitoring reimbursement market and the WHO’s documented 17.9 million annual cardiovascular deaths, driving proactive cardiac monitoring demand, represent the highest-value commercial pathway, transforming smart rings from consumer gadgets into reimbursed medical monitoring devices through 2033.

Market Dynamics

Does the Rise in Consumer Demand for Continuous Passive Biometric Health Monitoring Fuel Growth?

The global surge in consumer health consciousness, accelerated by the COVID-19 pandemic’s elevation of personal health monitoring as a routine practice, is creating structural and growing demand for smart rings as the most discreet, comfortable, and continuous biometric data collection platform available. Smart rings equipped with photoplethysmography (PPG) sensors, accelerometers, and skin temperature sensors can continuously track heart rate, heart rate variability (HRV), blood oxygen saturation (SpO2), sleep stages, and body temperature without the social and physical intrusiveness of smartwatches.

According to the WHO, cardiovascular diseases are the world’s leading cause of death, responsible for approximately 17.9 million deaths annually, creating a massive addressable population for proactive cardiac health monitoring tools. Oura Health’s clinical research partnerships, including research collaborations with the University of California, San Francisco (UCSF), validating the Oura Ring’s menstrual cycle and illness detection accuracy, are establishing medical credibility that differentiates smart rings from lifestyle wearables and elevates their health utility perception among clinically motivated consumer segments.

Samsung Galaxy Ring Launch Catalyzing Mainstream Consumer Awareness and Category Legitimization

The launch of Samsung Electronics’ Galaxy Ring in July 2024 at US$ 399 represents the single most significant commercial catalyst in the Smart Rings Market’s history, validating the product category for mainstream consumers who trust established global consumer electronics brands. Samsung is the world’s largest consumer electronics company by revenue, with annual revenues exceeding US$ 200 Billion, giving it unmatched global retail distribution, marketing investment capability, and ecosystem integration leverage through Samsung Health and Galaxy AI.

The Galaxy Ring’s launch generated widespread media coverage and consumer discovery, dramatically expanding category awareness beyond the tech-enthusiast segment that had previously defined smart ring adoption. According to IDC, global wearable device shipments grew consistently, with smartwatches and wristbands remaining dominant but the ring form factor gaining rapid traction following Samsung’s entry, creating competitive pressure that is driving rapid product and price differentiation across the category.

How is Limited Battery Life Compared to Traditional Jewelry and Smartwatches?

Despite significant advances in power management, smart rings typically require charging every 4-7 days, a recharging frequency that consumers accustomed to traditional rings that never require charging find disruptive. According to user reviews and product specifications published by Oura Health and Samsung Electronics, smart ring battery life ranges from 4-7 days depending on usage intensity, requiring a dedicated charging cradle that adds a friction point to the ownership experience.

This limitation is particularly significant for the ring form factor, where consumer expectations are shaped by traditional jewelry’s perpetual wear, a psychological barrier to adoption that does not apply to smartwatches, where charging expectations are already normalized.

Are Data Privacy Concerns for Continuous Biometric Data Collection Challenging its Adoption?

Smart rings collect highly personal and sensitive biometric data, including heart rate, sleep patterns, menstrual cycle data, and body temperature continuously, raising significant consumer privacy concerns about data storage, sharing, and commercial use.

The U.S. Federal Trade Commission (FTC) has issued guidance on the privacy risks of health-related wearable devices, and the European Data Protection Board (EDPB) has emphasized that biometric data collected by wearables constitutes a special category of sensitive personal data under GDPR Article 9, requiring explicit consent and enhanced security measures. High-profile data breach incidents at health-related companies have amplified consumer concerns about trusting sensitive biometric data to wearable device manufacturers’ cloud platforms.

Does the Availability of Clinical-Grade Health Monitoring Integration and FDA Clearance as a Medical Device Create More Opportunities?

The progression of smart ring health monitoring capabilities toward clinical-grade accuracy, combined with regulatory approval pathways including FDA 510(k) clearance for specific health monitoring features, represents the most transformative commercial opportunity in the Smart Rings Market. Movano Health received FDA 510(k) clearance for its Evie Ring’s blood oxygen monitoring capability in 2023, establishing a regulatory precedent for smart ring medical device classification that could unlock insurance reimbursement, clinical trial deployment, and remote patient monitoring (RPM) program integration.

According to the Centers for Medicare & Medicaid Services (CMS), the U.S. remote patient monitoring reimbursement program represents a multi-billion-dollar addressable market for FDA-cleared health monitoring wearables. Smart ring manufacturers investing in FDA clearance pathways for atrial fibrillation (AFib) detection, blood glucose monitoring, and blood pressure monitoring stand to access institutional healthcare buyer channels that represent a fundamentally different and more durable revenue model than consumer retail.

Enterprise Security and Contactless Payment Application Expansion

The growing adoption of smart rings as enterprise access control and contactless payment devices represents a high-growth opportunity beyond the consumer health monitoring segment. McLear Ltd., which pioneered payment-enabled smart rings through its McLear Ring platform, has demonstrated viable commercial models for rings as contactless payment credentials compatible with Visa and Mastercard payment networks and Apple Pay/Google Pay passthrough systems.

According to the World Economic Forum (WEF), global cashless payment transaction volumes are projected to increase by approximately 80% between 2020 and 2025, with contactless payment channel adoption accelerating across Asia Pacific, Europe, and North America. Enterprise building access control, a market served by NFC-enabled smart rings, including products from Tokenize Inc., is growing as organizations seek to replace traditional key card access systems with wearable-based, frictionless authentication solutions that improve security and convenience for employees.

Category-wise Analysis

Operating System Insights

Cross-Platform compatibility represents the dominant operating system segment, accounting for approximately 48% of total smart rings market revenue. Cross-platform smart rings, which operate with both Android and iOS smartphones through companion applications, provide the broadest addressable consumer market by eliminating operating system lock-in as a purchase barrier.

Oura Health’s Oura Ring, the market’s leading product by installed base with over 2.5 Million active users, is fully cross-platform compatible, enabling seamless data synchronization with both Apple Health on iOS and Google Health Connect on Android.

Android and iOS collectively account for over 99% of global smartphone operating system market share, making cross-platform compatibility essential for maximizing consumer addressability. The Android-dedicated segment is growing fastest, reflecting the dominant global market share of the Android platform and Samsung Galaxy Ring’s initial Android-exclusive ecosystem integration.

Technology Analysis

Bluetooth-enabled smart rings represent the dominant technology segment, accounting for approximately 56% of total Smart Rings Market revenue. Bluetooth Low Energy (BLE) connectivity enables smart rings to continuously sync biometric health data to companion smartphone applications with minimal power consumption, a critical technical requirement given the limited battery capacity of ring-form-factor devices.

All leading health monitoring smart rings, including Oura Ring, Samsung Galaxy Ring, Ultrahuman Ring AIR, and RingConn utilize BLE as their primary data transmission protocol due to its optimal balance of connectivity range, power efficiency, and smartphone ecosystem compatibility. According to the Bluetooth Special Interest Group (Bluetooth SIG), BLE is embedded in virtually all modern smartphones globally, providing a universal connectivity infrastructure for smart ring data synchronization without requiring dedicated hardware infrastructure investment.

Application Insights

Health & wellness monitoring represents the dominant application segment, accounting for approximately 52% of total Smart Rings Market revenue. The health monitoring application’s dominance reflects the primary consumer purchase motivation for smart rings, the desire for continuous, passive, and form-factor-appropriate biometric monitoring that complements or replaces smartwatch-based health tracking for consumers seeking a more natural wearing experience.

Health monitoring is consistently the most cited motivation for wearable device purchase among global consumers. Oura Health’s clinical research program, including published peer-reviewed studies validating ring-based sleep staging accuracy against the polysomnography gold standard, has established health monitoring as the defining application value proposition for the smart ring category, differentiating it from novelty technology and anchoring it in the rapidly growing personal health technology ecosystem.

End-user Insights

Fitness Enthusiasts represent the dominant end-user segment, accounting for approximately 38% of total Smart Rings Market revenue. This segment’s leadership reflects the established consumer behavior of fitness-oriented individuals investing in wearable technology for performance monitoring, recovery optimization, and activity tracking. Oura Health’s marketed readiness score, recovery tracking, and activity monitoring features are specifically positioned to appeal to athletes and fitness enthusiasts seeking actionable training insights from biometric data.

According to the International Health, Racquet & Sportsclub Association (IHRSA), global health club and gym membership has been recovering strongly post-COVID-19, sustaining consumer investment in personal fitness technology. The Healthcare Users sub-segment is growing fastest, driven by FDA-cleared medical monitoring feature development, remote patient monitoring program integration, and the aging global population’s growing demand for continuous health surveillance tools.

Regional Insights

North America Smart Rings Market Trends and Insights

North America accounted for an estimated 38% share of the global Smart Rings Market in 2026, representing approximately US$ 175.0 Million. The region benefits from advanced wearable technology adoption, strong digital healthcare infrastructure, rising chronic disease prevalence, and early integration of AI-driven health monitoring platforms. Regulatory clarity from the U.S. FDA’s Digital Health Center of Excellence is accelerating the commercialization of medical-grade smart ring technologies, while premium consumer demand continues to support strong revenue growth across health, wellness, and fitness applications.

- United States Smart Rings Market Size

The U.S. dominates the North American Smart Rings Market, accounting for nearly 82% of the regional market and valued at approximately US$ 143.5 Million in 2026. Growth is driven by widespread adoption of connected health devices, rising consumer spending on preventive healthcare, and strong presence of wearable technology innovators, including Oura Health and Samsung Electronics. Increasing demand for sleep tracking, cardiovascular monitoring, and women’s health analytics is expanding the medical-grade smart ring ecosystem across the country.

Europe Smart Rings Market Trends and Insights

Europe is likely to represent an estimated 25% of the global smart rings market in 2026, reaching approximately US$ 138.2 Million. The market is shaped by stringent data privacy regulations under GDPR, increasing consumer awareness of digital wellness technologies, and supportive healthcare digitization initiatives across major European economies. Regulatory frameworks, including EU MDR and IVDR, are encouraging clinically validated wearable solutions, while the rising preventive healthcare culture in Northern and Western Europe continues to strengthen smart ring adoption.

- Germany Smart Rings Market Size

Germany accounted for approximately US$ 36 million in 2026, making it Europe’s largest smart ring market. Strong adoption of digital healthcare technologies, high disposable income, and the country’s DiGA reimbursement framework are supporting demand for medically validated wearable devices. German consumers show particularly strong interest in sleep analytics, stress monitoring, and fitness optimization solutions integrated with digital health platforms.

- United Kingdom Smart Rings Market Size

The U.K. Smart Rings Market was valued at approximately US$ 28.5 Million in 2026. Market expansion is supported by the NHS digital transformation strategy, rising acceptance of wearable health monitoring devices, and increasing investment in AI-enabled healthcare technologies. Consumer demand for compact wellness wearables and integration with telehealth ecosystems is contributing significantly to market growth across urban populations.

- France Smart Rings Market Size

France accounted for an estimated US$ 21.4 million in 2026, supported by rising consumer interest in minimalist wearable technologies and expanding digital wellness awareness. Domestic innovation from brands such as Circular is strengthening the regional ecosystem. Increasing adoption of preventive healthcare tools and growing integration of wearable data into fitness and lifestyle applications are driving market momentum.

Asia Pacific Smart Rings Market Trends and Insights

Asia Pacific is the fast-growing smart rings market globally and accounted for approximately 26% of total market revenue in 2026, reaching nearly US$ 148.8 Million. The region benefits from large-scale smartphone penetration, rapid growth of middle-class consumers, expanding digital health ecosystems, and strong electronics manufacturing capabilities. Major consumer electronics companies are accelerating regional adoption through competitively priced products, localized distribution strategies, and AI-powered health monitoring features.

- China Smart Rings Market Size

China led the Asia Pacific smart rings market with an estimated value of US$ 54.3 million in 2026. Growth is driven by the country’s advanced electronics manufacturing ecosystem, rising digital health adoption, and strong domestic wearable technology brands including Zepp Health and RingConn. Increasing demand for affordable health-monitoring wearables among urban consumers continues to accelerate market expansion.

- India Smart Rings Market Size

India’s smart rings market reached approximately US$ 18.6 million in 2026 and is projected to register one of the fastest growth rates globally through 2033. Expansion is supported by rising fitness awareness, rapid growth of the digital health ecosystem under the Ayushman Bharat Digital Mission, and increasing participation from domestic brands, including Noise and boAt. Young urban demographics and growing wearable affordability are key demand drivers.

- Japan Smart Rings Market Size

Japan accounted for an estimated US$ 24.8 million in 2026, supported by high consumer interest in precision healthcare technologies and strong adoption of connected wellness devices. The country’s aging population and emphasis on preventive healthcare are increasing the demand for continuous biometric monitoring solutions. Japanese consumers also demonstrate a strong preference for compact, lightweight, and technologically advanced wearable products.

Competitive Landscape

The global smart rings market is moderately fragmented, transitioning from a niche-brand-dominated landscape toward a more competitive ecosystem following Samsung Electronics’ landmark Galaxy Ring entry in 2024. Oura Health remains the market’s technology and brand leader with its clinically validated health monitoring platform, while Samsung, Ultrahuman Healthcare Pvt Ltd, RingConn, and Movano Health represent the primary competitive challengers.

Key differentiators include clinical evidence quality for health monitoring features, battery life, subscription pricing model transparency, and FDA clearance status. Emerging business model trends include annual subscription health insight platforms, clinician partnership programs for remote patient monitoring integration, and enterprise access control licensing. McLear Ltd. and NFC Ring maintain leadership in the contactless payment and access control niche, while Circular (France) leads the European design-focused premium segment.

Key Developments:

- July 2024: Samsung Electronics launched the Galaxy Ring globally at US$ 399, marking the most significant commercial entry in smart ring history, bringing mainstream consumer brand credibility to the category and integrating ring biometric data into the Samsung Health and Galaxy AI ecosystem.

- February 2025: Oura Health announced the Oura Ring 4 with enhanced AFib detection and expanded women’s health monitoring capabilities, strengthening its clinical positioning and its partnership with Dexcom for continuous glucose monitoring (CGM) data integration.

- January 2025: Ultrahuman Healthcare Pvt Ltd expanded its Ring AIR product availability to 50+ countries through an enhanced direct-to-consumer e-commerce platform, supporting global scaling of its India-headquartered smart ring brand targeting fitness and performance-oriented consumers.

Smart Rings Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 145.9 Million |

| Current Market Value (2026) | US$ 502.7 Million |

| Projected Market Value (2033) | US$ 2506.5 Million |

| CAGR (2026 - 2033) | 25.8% |

| Leading Region | North America (38%) |

| Top-ranking Technology | Bluetooth-enabled (56.0%) |

| Top-ranking End-User | Fitness Enthusiasts (38.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 2003.8 Million |

Companies Covered in Smart Rings Market

- Oura Health

- Samsung Electronics

- Ultrahuman Healthcare Pvt Ltd

- RingConn

- Movano Health

- Circular

- McLear Ltd.

- Noise

- Amazfit

- boAt

- Go2Sleep

- Motiv Inc.

- NFC Ring

- Jakcom Technology Co. Ltd.

- Tokenize Inc.

- Evie Ring

- Iris Ring

- Xenxo S-Ring

Frequently Asked Questions

The global Smart Rings Market is projected to reach US$ 2,506.5 Million by 2033, growing at a CAGR of 25.8% during the forecast period 2026 - 2033, from an estimated US$ 502.7 Million in 2026. The market recorded a historical CAGR of 22.9% between 2020 and 2025, driven by Oura Health’s 2.5+ Million active users validating consumer health ring demand, Samsung’s Galaxy Ring launch in 2024 catalyzing mainstream adoption, and the WHO’s documented chronic disease burden elevating continuous health monitoring demand globally.

The primary drivers are rising consumer demand for continuous passive health monitoring, backed by the WHO’s documentation that NCDs cause 74% of global deaths and cardiovascular diseases account for 17.9 Million annual fatalities, motivating proactive health surveillance, and Samsung Electronics’ Galaxy Ring launch in July 2024 at US$ 399, catalyzing mainstream consumer category awareness through the world’s largest consumer electronics brand’s distribution and marketing infrastructure.

Bluetooth-enabled smart rings dominate the Technology segment with approximately 56% market share. Bluetooth Low Energy (BLE), embedded in virtually all modern smartphones globally per the Bluetooth Special Interest Group (Bluetooth SIG), enables continuous biometric data synchronization with minimal power consumption, the critical technical requirement for battery-constrained ring form factor devices. All leading health monitoring rings including Oura Ring, Galaxy Ring, and Ultrahuman Ring AIR utilize BLE as their primary data transmission technology.

North America, led by the United States, is the dominant regional market, home to pioneer Oura Health with over 2.5 Million active users, Movano Health’s FDA-cleared Evie Ring, and the FDA’s Digital Health Center of Excellence enabling medical-grade product development. The CDC’s report that 6 in 10 U.S. adults have at least one chronic disease creates the largest addressable consumer base for continuous health monitoring rings globally.

FDA-cleared clinical-grade smart ring features for remote patient monitoring represent the defining opportunity, with Movano Health’s 510(k) clearance establishing a medical device regulatory precedent and the Centers for Medicare & Medicaid Services (CMS) remote patient monitoring program providing multi-billion-dollar reimbursement infrastructure. Smart ring manufacturers achieving medical device status can access institutional healthcare buyer channels and insurance reimbursement that fundamentally expand the revenue model beyond consumer retail through 2033.

Key market participants include Oura Health, Samsung Electronics (Galaxy Ring), Ultrahuman Healthcare Pvt Ltd (Ring AIR), RingConn, Movano Health (Evie Ring), Circular, McLear Ltd., Noise, Amazfit (Zepp Health), boAt, Go2Sleep (Sleepon), Motiv Inc., NFC Ring, Jakcom Technology Co. Ltd., and Tokenize Inc., alongside emerging brands Iris Ring and Xenxo S-Ring targeting enterprise and healthcare specialist sub-segments.