- Technology

- Americas UAV Market

Americas UAV Market Size, Share, and Growth Forecast 2026 - 2033

Americas UAV Market by System Type (Platform, Payload, Ground Control Stations), Operation Mode (Remotely Piloted, Partially Autonomous, Fully Autonomous), Application (Military, Commercial), and Analysis, 2026 - 2033

Americas UAV Market Size and Trends Analysis

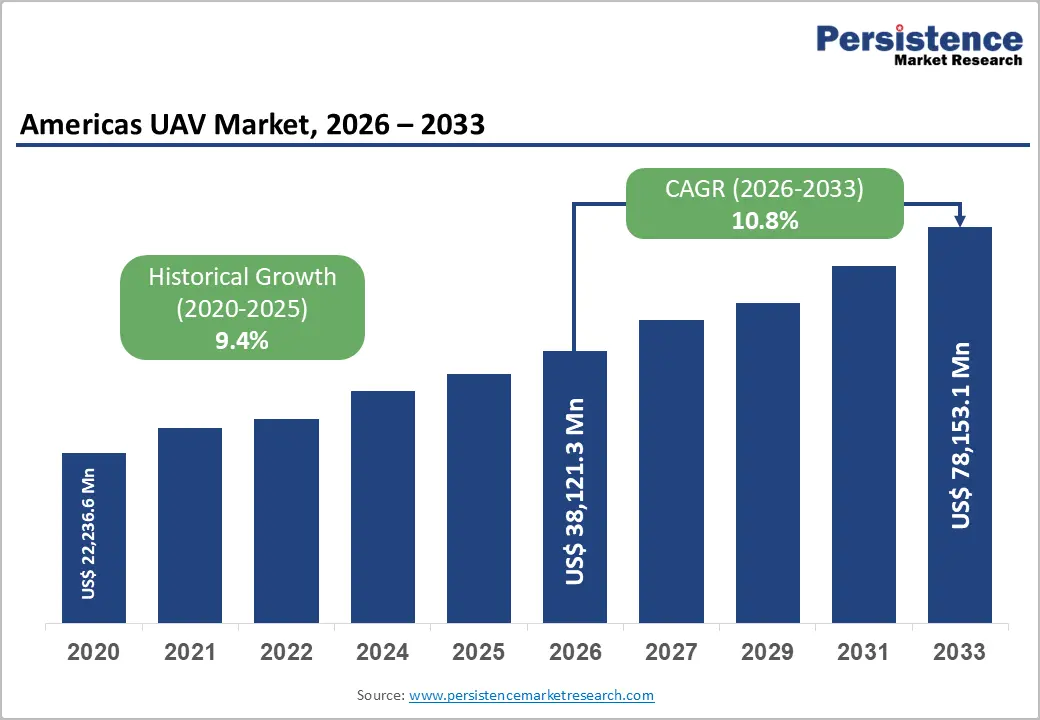

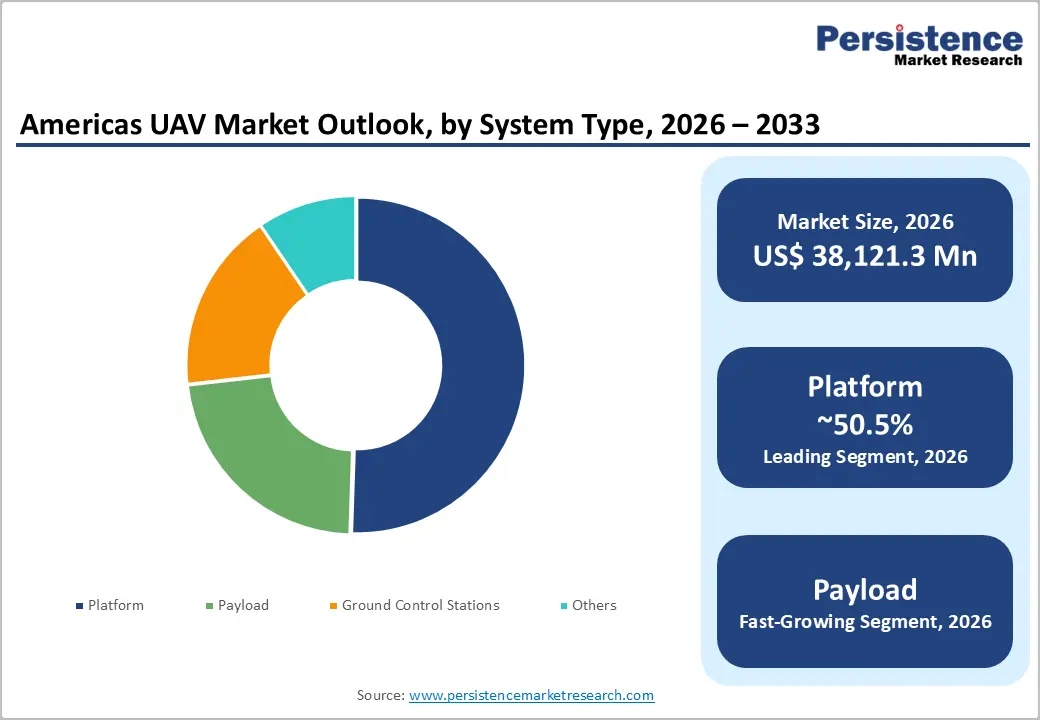

The Americas UAV market size is likely to be valued at US$38,121.3 million in 2026 and is expected to reach US$78,153.1 million by 2033, growing at a CAGR of 10.8% during the forecast period from 2026 to 2033, driven by rising defense investments in autonomous and unmanned systems and increasing use of drones across commercial sectors. Growth is also supported by developments in AI-assisted navigation and sensor technologies.

Key Industry Highlights:

- Leading System Type: Platform, approximately 50.5% share in 2026, as every UAV requires an airframe, propulsion system, and flight control architecture.

- Dominant Application: Military, nearly 43.7% in 2026, as governments prioritize drones for intelligence, surveillance, reconnaissance, and combat missions.

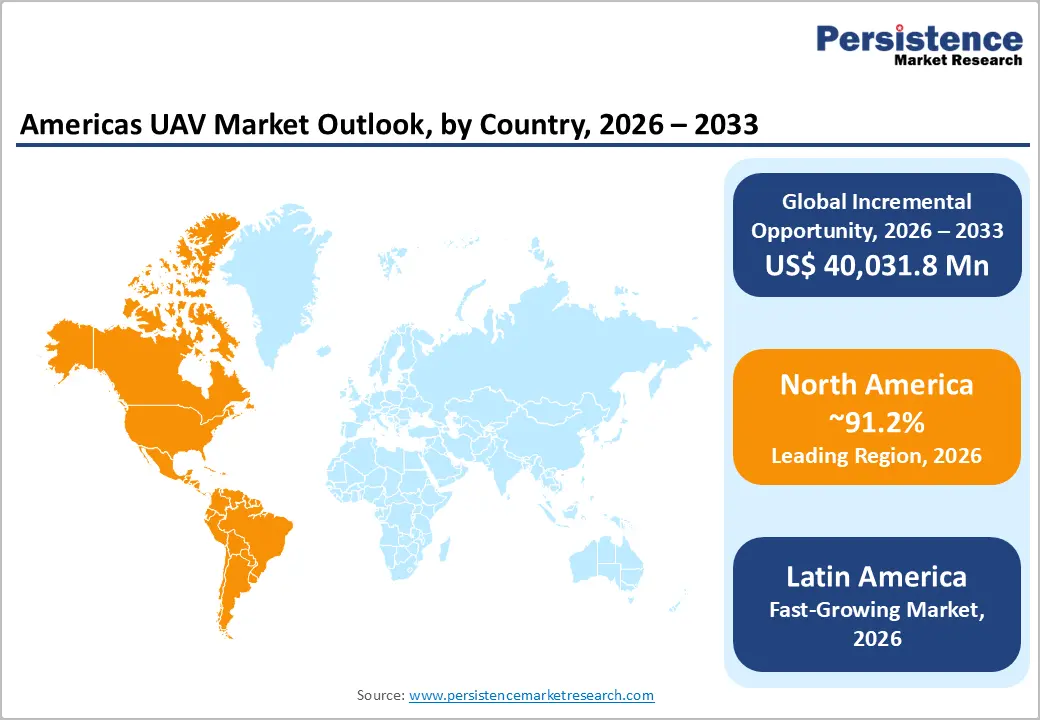

- Leading Region: North America, with about a 91.2% share in 2026, as the U.S. continues to invest heavily in military drones, autonomous systems, and domestic drone manufacturing.

- Fast-growing Region: Latin America, spurred by increasing UAV adoption in precision agriculture, mining, and oil and gas monitoring.

- Recent Deployment: In October 2025, Shield AI deployed its V-BAT unmanned aircraft system during the multinational UNITAS 2025 naval exercise organized by U.S. Naval Forces Southern Command. The UAV provided Intelligence, Surveillance, and Reconnaissance (ISR) support alongside forces from 25 partner nations across the Americas, showcasing rising military adoption of autonomous UAV platforms.

DRO Analysis

Driver - Rising Geopolitical Tensions to Fuel Demand for Improved Security

Increasing geopolitical tension, from the Russia-Ukraine war changing NATO priorities to tensions along the U.S.-Mexico border, has made Unmanned Aerial Vehicles (UAVs) central to modern ISR strategies. The U.S. Department of Defense submitted a FY2025 Military Intelligence Program budget request of USD28.2 billion, a key signal of sustained investment in aerial surveillance.

Canada is following suit. In 2024, L3Harris delivered three ISR-modified King Air 350ER aircraft to the Canadian Armed Forces to strengthen national surveillance capabilities. On the unmanned side, the DoD's Replicator initiative and partnerships between defense contractors and tech firms are actively accelerating research & development in stealth and 5G-enabled real-time communication for UAV platforms. These programs underline how UAVs have moved from being support tools to core battlefield assets across the Americas.

Increasing Demand from Utility and Energy Firms to Inspect Assets

Energy and utility companies across the Americas are turning to UAVs as a smart alternative for inspecting sprawling physical assets. Drones can inspect power lines at speeds of up to 40 mph, far faster than traditional methods, while keeping workers away from high-voltage hazards and expensive bucket trucks. Real-world adoption is already well underway.

New York State Electric & Gas (NYSEG) and Rochester Gas and Electric (RG&E) used drones throughout 2024 to conduct comprehensive visual inspections of thousands of miles of transmission lines. These captured high-resolution images of infrastructure that was difficult or dangerous to access by ground. In pipeline monitoring, Wingcopter in February 2025 launched a BVLOS LiDAR solution capable of surveying up to 37 miles per mission with 10mm accuracy, a benchmark that manual inspection teams simply cannot match.

Restraint - Surging Collision Risk in Low-Altitude Airspace

The swift spread of recreational and commercial drones is putting serious pressure on low-altitude airspace safety. An Associated Press (AP) analysis of an aviation safety database found that drones accounted for nearly two-thirds of reported near midair collisions at the 30 busiest U.S. airports in 2024, the highest such share since 2020. These are not isolated incidents. A jetliner near Miami's international airport had a close encounter with a drone at 4,000 feet, while in August, a drone came within 50 feet of clipping the left wing of a departing jet at Newark International Airport.

A key part of the problem is altitude violations. A Federal Aviation Administration (FAA)-commissioned study by Embry-Riddle researchers found that in 96% of near-miss cases analyzed, the drone was flying above the maximum permissible altitude for its area. With the FAA estimating more than a million drones now operating across the country for recreational and commercial purposes, the absence of mandatory geofencing on consumer drones continues to be a key regulatory gap. It is predicted to trigger strict rules and slow commercial UAV expansion if left unaddressed.

Opportunity - The Race to Replace a Legacy Drone

The U.S. Army's push to retire its aging RQ-7B Shadow UAV has opened one of the most competitive procurement battles in military unmanned aviation. In April 2024, the Army formally awarded contracts to Griffon Aerospace and Textron Systems to enter the flight demonstration phase of the Future Tactical Unmanned Aircraft System (FTUAS) program, narrowing the competition from five original participants.

The requirements showcase next-generation warfare needs. The Army wants the system to be runway-independent, capable of on-the-move command and control, and designed for soldier-led field maintenance. Textron Systems was subsequently selected for FTUAS Options 3 and 4, requiring the company to complete a full flight demonstration and deliver its Aerosonde Mk. 4.8 Hybrid Quad for Army test and evaluation. The program's outcome will likely influence which platforms Brigade Combat Teams across the Army carry into the field. It is projected to make it a defining contract for the tactical UAV segment.

Emergence of Drone-as-a-Service

Industries that once had to buy hardware, hire certified pilots, and manage compliance on their own are now shifting to managed drone services. The Drone-as-a-Service (DaaS) model is evolving from one-time hardware procurement toward subscription-based operations. Autonomous flights are being deployed mainly across infrastructure inspection, agriculture, mining, logistics, and public safety sectors. North America is leading this transition. Platform services are dominating the regional market as enterprises turn to bundled flight and cloud analytics packages to streamline adoption.

Hardware commoditization is further pushing providers toward high-value and recurring-revenue contracts. Businesses can access on-demand drone operations for mapping, LiDAR, volumetric analysis, and real-time site data without the capital costs or operational burdens of ownership. As FAA BVLOS regulations continue to ease, DaaS is positioned to become a standard procurement model rather than a niche workaround.

Category-wise Analysis

System Type Insights

The platform segment is predicted to lead with a share of approximately 50.5% in 2026 in Americas UAV market, as it is the foundation of the entire drone system. It includes the airframe, propulsion system, flight control system, landing gear, and power source. Every UAV requires a platform before payloads, sensors, or communication systems can be integrated. Hence, defense agencies and commercial operators allocate a large share of their budgets to acquiring and upgrading platforms.

The payload segment is estimated to be the fastest-growing segment over the forecast period, as drone users mainly seek actionable data rather than simply flying a drone. Modern UAVs are being equipped with advanced cameras, thermal imagers, LiDAR systems, radar, electronic warfare equipment, and communication modules. These payloads transform drones into intelligence-gathering and decision-making tools. The rise of AI-supported operations is also boosting payload demand.

Application Insights

The military segment is anticipated to dominate with a share of nearly 43.7% in 2026, as drones have become essential assets in modern warfare. They provide ISR, target acquisition, battlefield monitoring, electronic warfare, and precision strike capabilities while reducing risks to personnel. Governments continue to increase investments in drone fleets due to lessons learned from recent conflicts. The widespread use of UAVs in global conflicts has demonstrated that drones can perform missions at a lower cost and with greater operational flexibility than traditional aircraft. Hence, military organizations are extending procurement programs and integrating UAVs into routine operations.

The commercial segment is expected to remain in the second position in 2026, as drones are moving beyond photography into practical business operations. Industries, such as agriculture, construction, energy, logistics, telecommunications, mining, and public safety, increasingly rely on UAVs to improve efficiency and reduce operating costs. One prominent growth driver is drone delivery. The U.S. Federal Aviation Administration (FAA) has continued granting Part 135 certifications to commercial drone operators.

Companies such as Amazon Prime Air, Zipline, DroneUp, and Drone Express are now authorized to conduct commercial package delivery operations in the U.S. This demonstrates the increasing regulatory acceptance of commercial UAV services.

Region Insights

North America UAV Market Trends

In 2026, North America is estimated to dominate with a share of approximately 91.2%, backed by a rare combination of defense depth, regulatory clarity, and commercial maturity. The U.S. leads the regional market on the back of a high defense budget, early adoption of UAV technologies, and proactive regulatory initiatives from the FAA. On the defense side, in 2024, around 65% of U.S. DoD drone operations were dedicated to ISR missions, especially across high-conflict regions and sensitive borders.

On the commercial side, the FAA provides a comprehensive regulatory framework for safe drone integration into national airspace, while academic-industry collaborations strengthen the country's research and development capabilities.

U.S. UAV Market Trends

The U.S. is anticipated to dominate in 2026 with a share of nearly 86.2%. The country is entering one of its most consequential regulatory transitions in a decade. In August 2025, the FAA published its proposed Part 108 rule, a framework designed to incorporate large-scale Beyond Visual Line of Sight (BVLOS) operations with minimal human supervision, replacing the cumbersome Part 107 waiver system with an extensible, routine pathway. Beyond regulation, the U.S. is pushing to reduce reliance on China-made drones.

The DoD's Replicator initiative and the broad executive push showcase a strategic goal, i.e., building a self-sufficient domestic drone industry capable of serving both commercial and defense demands. With BVLOS normalization unlocking industries such as delivery, infrastructure inspection, and emergency response, the U.S. market's growth trajectory is firmly upward.

Canada UAV Market Trends

Canada is estimated to see average growth with a share of approximately 13.8% in 2026. The country is making large and deliberate bets on military drones while its commercial sector steadily builds momentum. The most defining move came in late 2023. Canada announced a CAD 2.49 billion (nearly US$1.7 billion) investment to acquire 11 MQ-9B SkyGuardian drones.

These are fighter jet-sized platforms capable of operating in harsh Arctic climates, representing the first armed drone fleet ever acquired by the Canadian Armed Forces. Two units were in production by the end of 2024, with delivery expected in 2028 and full operational capability by 2033. Arctic sovereignty is the core driver here, as Canada requires persistent surveillance over vast, unmanned northern territories.

Latin America UAV Market Trends

In 2026, Latin America will likely showcase the fastest growth, as drones solve real, pressing problems in the region, right from vast farmlands requiring precision monitoring to difficult terrain and weak infrastructure. The primary drivers are the extensive use of drones in agriculture for crop monitoring and precision farming, rising infrastructure development projects, and government investments in security and surveillance. Agriculture is the anchor use case. The region contains some of the world's largest contiguous agricultural areas, especially in Brazil, where manual inspection is impractical.

At the same time, increasing government operations against narcotics have pushed demand for surveillance drones across the region.

Brazil UAV Market Trends

In 2026, a share of around 37.2% is predicted to be held by Brazil, as it is one of the world's most agriculture-dependent economies. The country's sheer farmland expansion, especially in Mato Grosso and Paraná, makes drone adoption economically unavoidable. Government initiatives to modernize agriculture, led by the Ministry of Agriculture, Livestock, and Supply (MAPA), have actively encouraged the use of precision agriculture technologies, including drones. Data from the government shows that over 8,000 spraying drones were imported into the country in recent years, a figure that shows just how embedded UAVs have become in the country’s farming.

Mexico UAV Market Trends

Mexico will likely account for a substantial share of nearly 17.4% in 2026. On the commercial front, the market is being driven by precision agriculture, infrastructure inspection, and security applications. Farmers are using UAVs for crop health monitoring, variable-rate spraying, and irrigation management, supported by affordable DaaS packages that reduce entry barriers for smaller farms. On the security side, however, Mexico's drone landscape has a darker dimension.

The Department of Homeland Security (DHS) tracked over 27,000 drones within 500 meters of the U.S.-Mexico southwest border in just the last six months of 2024, most linked to cartel surveillance and drug smuggling operations. This dual-use reality is creating indirect demand for counter-drone technology along the border, thereby adding another layer to the market's growth drivers.

Competitive Landscape

The Americas UAV market is moderately fragmented, but swiftly consolidating in the defense and advanced autonomy segments. While hundreds of drone manufacturers, software providers, and component suppliers operate across North and Latin America, a relatively small group of companies is capturing the highest-value military, public safety, and enterprise contracts. Recent acquisitions and strategic partnerships indicate that expansion, autonomous capabilities, and defense certifications are becoming key competitive advantages.

The competitive landscape is mainly divided into two tiers. The first consists of established aerospace and defense giants such as General Atomics, Lockheed Martin, Northrop Grumman, RTX, and Boeing. These dominate large military UAV programs through long-term government contracts and integrated Intelligence, Surveillance, and Reconnaissance (ISR) platforms. Companies such as General Atomics maintain a strong position through platforms such as the MQ-9 series. Lockheed Martin also competes through sensor integration, mission systems, and secure command-and-control networks rather than UAV platforms alone.

Key Industry Developments:

- In June 2026, Motorola Solutions announced a definitive agreement to acquire D-Fend Solutions for US$1.5 billion. The acquisition strengthens Motorola’s presence in counter-drone technologies, with D-Fend’s RF-based drone takeover systems already deployed across more than 30 countries by government, public safety, and enterprise customers.

- In May 2026, Skydio received a follow-on contract expansion from the U.S. Air Force to further equip Explosive Ordnance Disposal (EOD) units with its X10D drone systems. The award more than doubled the scope of the initial order placed in 2025 and supports the Air Force’s broad adoption of autonomous UAVs for high-risk missions.

- In March 2026, the U.S. Army placed an order worth more than US$52 million for over 2,500 Skydio X10D drones, representing the largest single-vendor tactical small-UAS procurement in Army history. The program aims to propel the deployment of autonomous reconnaissance drones at the platoon level.

Companies Covered in Americas UAV Market

- Advanced Aircraft Company

- AgEagle Aerial Systems Inc.

- Aliter Technologies, Inc.

- ARA Robotics

- Aurelia Technologies Inc.

- Draganfly Innovations, Inc.

- Drone Delivery Canada Corp

- Drone Volt SA

- DroneUp, LLC

- Elistair

- Elroy AirMed.

- FlyingBasket SRL

- Freefly Systems

- Guangzhou EHang Intelligent Technology Co. Ltd

- Inova Drone, Inc.

- Inspired Flight Technologies, Inc.

- Optelos

- Parrot Drone SAS

- Quantum-Systems GmbH

- Sentera, Inc.

- Vantage Robotics, Inc.

- Others

Frequently Asked Questions

The Americas UAV market is projected to be valued at US$38,121.3 million in 2026.

The Americas UAV market is expected to reach US$78,153.1 million by 2033.

Key market trends include the integration of AI-supported autonomous navigation and rising investments in domestically manufactured drones.

Platform is expected to be the leading system type with a share of nearly 50.5% in 2026, due to rising demand for long-range surveillance, military reconnaissance, and industrial inspection missions.

The Americas UAV market is expected to grow at a CAGR of 10.8% from 2026 to 2033.

Advanced Aircraft Company, AgEagle Aerial Systems Inc., Aliter Technologies, Inc., and ARA Robotics are a few key market players.