- Metals & Minerals

- Seamless Pipes Market

Seamless Pipes Market Size, Share, and Growth Forecast, 2026 - 2033

Seamless Pipes Market By End-use Industry (Oil & Gas, Power Generation, Others), Material Type (Steel & Alloys, Nickel & Alloys, Others), Production Process, and Regional Analysis for 2026 - 2033

Seamless Pipes Market Size and Trends Analysis

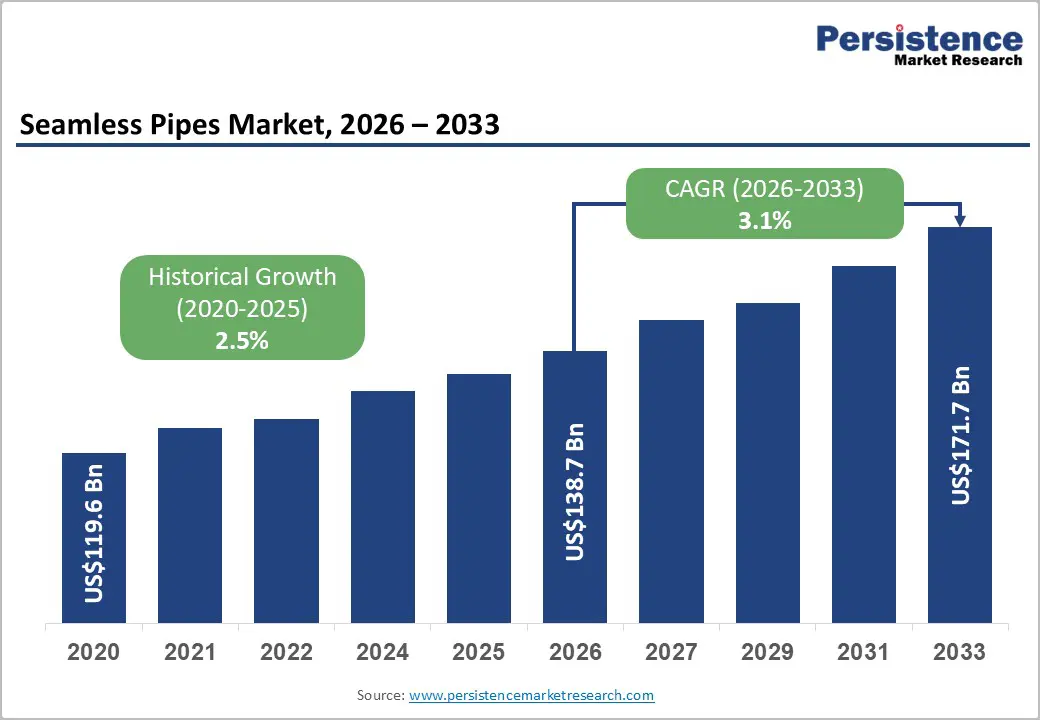

The global seamless pipes market size is likely to be valued at US$108.2 billion in 2026 and is expected to reach US$161.6 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by their superior strength, pressure resistance, and reliability in critical operating environments. The growing adoption of hydrogen infrastructure, carbon capture projects, geothermal energy systems, and advanced industrial facilities is further expanding the application scope of premium seamless pipe products worldwide.

Key Industry Highlights:

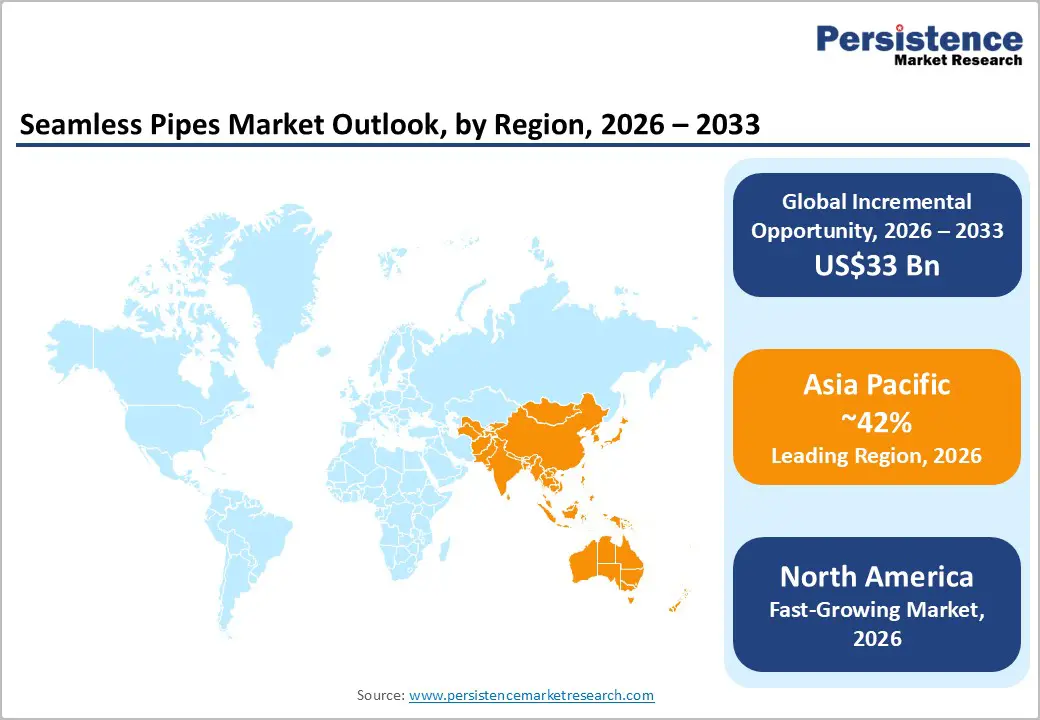

- Leading Region: Asia Pacific is projected to account for 46.6% of market share in 2026, driven by large-scale industrialization, infrastructure development, and strong demand from China and India.

- Fastest-growing Region: Asia Pacific, supported by rapid manufacturing expansion, renewable energy investments, refinery projects, and government-led infrastructure programs across India and Southeast Asia.

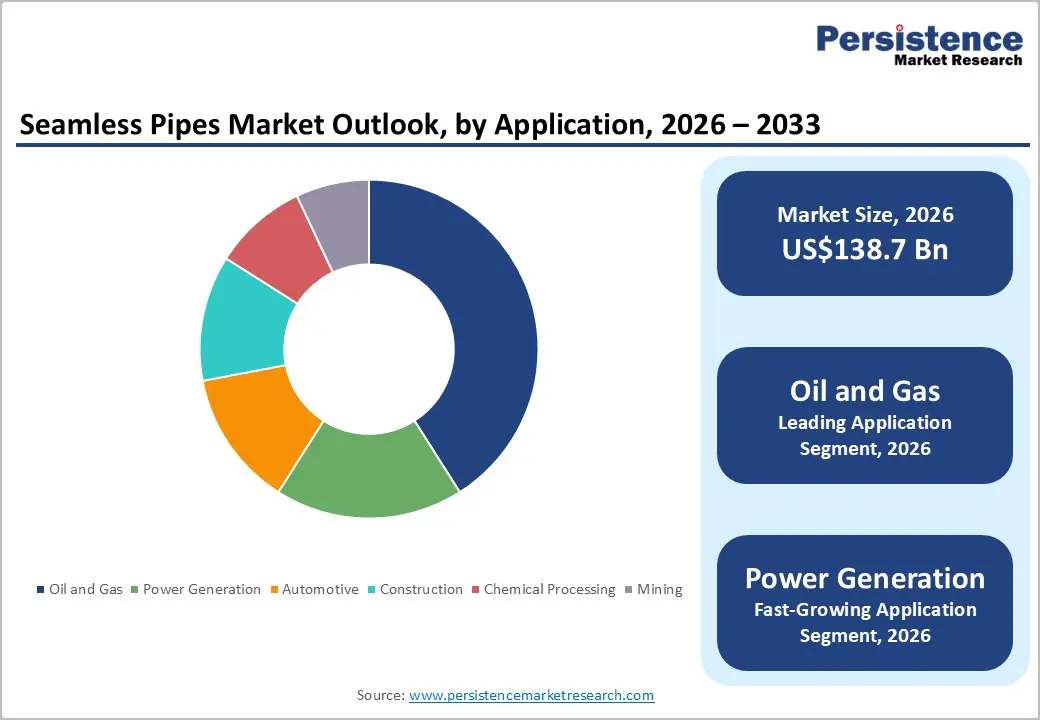

- Dominant End-use Industry: Oil & gas is anticipated to hold 41.2% of market share in 2026, supported by ongoing investments in exploration, production, refining, offshore drilling, and pipeline infrastructure.

- Leading Material Type: Steel & alloys are estimated to account for 67.1% of the market share in 2026, owing to their superior strength, durability, cost-effectiveness, and widespread adoption across energy, industrial, and infrastructure applications.

DRO Analysis

Driver - Sustained Oil & Gas Investments Supporting Seamless Pipe Demand

The oil and gas industry remains the largest consumer of seamless pipes globally, accounting for a significant share of total demand. Seamless pipes are widely utilized in exploration, drilling, well completion, production, refining, and transportation applications due to their ability to withstand extreme pressure, temperature, and corrosive operating conditions. Continued investments in upstream and midstream infrastructure across North America, the Middle East, Latin America, and Asia are creating strong demand for oil country tubular goods (OCTG), line pipes, and premium-grade seamless products.

Large-scale offshore developments, shale exploration projects, and cross-border pipeline construction activities continue to require high-performance tubular solutions. Since seamless pipes offer superior structural integrity compared to welded alternatives, they remain the preferred choice for critical energy applications. This trend is expected to sustain long-term market growth while supporting premium product pricing across major producing regions.

Expansion of Power Infrastructure and Energy Transition Projects

Rapid expansion of power generation capacity and grid modernization initiatives is creating a new growth avenue for seamless pipe manufacturers. Increasing electricity demand, renewable energy integration, and investments in energy transmission infrastructure are driving demand for high-quality pipes used in boilers, heat exchangers, steam systems, and thermal power facilities.

The transition toward low-carbon energy systems is accelerating investments in hydrogen production, carbon capture and storage (CCS), geothermal energy projects, and district heating networks. These applications require seamless pipes capable of operating under demanding thermal and mechanical conditions. Governments and utilities are prioritizing grid resilience, energy security, and infrastructure modernization, resulting in growing demand for durable and corrosion-resistant tubular products. As a result, the seamless pipes market is becoming increasingly diversified beyond traditional oil and gas applications.

Restraint - Raw Material Price Volatility and Project Delays

Despite favorable long-term fundamentals, the seamless pipes market faces challenges associated with steel price fluctuations, project execution risks, and capital expenditure uncertainties. Since steel represents a substantial portion of production costs, changes in raw material pricing directly affect manufacturer margins and procurement decisions.

Project delays caused by financing constraints, regulatory approvals, environmental permitting requirements, and geopolitical uncertainties can postpone purchasing cycles and disrupt order pipelines. In addition, fluctuations in industrial activity and uneven global steel demand create uncertainty regarding future capacity utilization. Smaller manufacturers with limited economies of scale are particularly vulnerable to pricing pressure and margin erosion. These factors can temporarily slow market growth despite strong underlying demand fundamentals.

Opportunity - Growing Demand for Hydrogen, CCS, and Geothermal Infrastructure

The emergence of hydrogen production facilities, carbon capture and storage networks, and geothermal energy developments presents a significant opportunity for seamless pipe manufacturers. These applications require specialized materials capable of resisting hydrogen embrittlement, corrosion, and thermal stress while maintaining long-term operational reliability.

Premium alloy-based seamless pipes are increasingly being specified for hydrogen transportation systems, carbon dioxide pipelines, geothermal wells, and advanced industrial processing facilities. As governments and private investors accelerate decarbonization efforts, demand for high-value tubular solutions is expected to increase substantially. Manufacturers capable of meeting stringent technical requirements and securing qualification approvals from utilities, engineering contractors, and energy operators are positioned to benefit from higher margins and long-term supply agreements.

Asia Pacific Industrialization and Infrastructure Expansion

Asia Pacific continues to represent the largest growth opportunity for the seamless pipes industry. Rapid urbanization, industrial development, manufacturing expansion, and energy infrastructure investments are generating significant demand across multiple end-use sectors.

China remains the world's largest producer and consumer of steel products, while India is emerging as a major manufacturing and infrastructure investment hub. Rising investments in power generation, transportation networks, industrial facilities, refineries, and petrochemical projects are creating favorable conditions for seamless pipe consumption. The expansion of domestic manufacturing capabilities and government initiatives supporting industrial growth further strengthen regional demand prospects. As companies increasingly seek localized supply chains, Asia Pacific is expected to remain the primary engine of global market expansion throughout the forecast period.

Category-wise Analysis

End-use Industry Insights

The oil & gas segment, anticipated to account for approximately 41.2% of the market share in 2026, remains the largest end-use industry. Seamless pipes are extensively used in drilling operations, well casing, tubing, offshore platforms, refineries, and transmission pipelines due to their ability to withstand extreme pressure and temperature conditions. For example, premium OCTG products supplied by companies such as Tenaris and Vallourec are widely deployed in shale developments in the U.S. and offshore projects in the Middle East.

The power generation segment is projected to be the fastest-growing end-use industry through 2033. Demand is being driven by grid modernization, renewable energy integration, and investments in thermal, nuclear, and geothermal power facilities. Seamless pipes are widely used in boilers, steam pipelines, heat recovery systems, and hydrogen production plants. Examples include their application in supercritical coal-fired power plants, geothermal projects in Asia-Pacific, and emerging hydrogen infrastructure developments across Europe, making this segment a key contributor to future market growth.

Material Type Insights

The steel & alloys segment, anticipated to account for approximately 67.1% of the market share in 2026, represents the dominant material category. These pipes are preferred across oil & gas, power generation, construction, and engineering industries due to their high strength, durability, and cost efficiency. For instance, carbon steel and alloy steel seamless pipes are extensively used in refinery operations, natural gas transmission networks, and industrial processing facilities. Their broad availability, established manufacturing base, and compliance with international standards continue to reinforce their market leadership.

The nickel & alloys segment is expected to record the fastest growth during the forecast period. These materials offer exceptional corrosion resistance and high-temperature performance, making them ideal for demanding environments. Examples include their use in offshore oil platforms, chemical processing plants, hydrogen transportation systems, and geothermal facilities. As industries increasingly prioritize operational reliability, longer asset life, and reduced maintenance costs, adoption of nickel-alloy seamless pipes is expected to accelerate significantly.

Regional Insights

North America Seamless Pipes Market Trends

North America remains a strategically important market for seamless pipes due to its strong energy sector, extensive industrial base, and ongoing infrastructure modernization efforts. The region accounts for a significant share of global demand, supported by investments in oil & gas production, power generation facilities, industrial processing plants, and pipeline networks. Growing electricity consumption, data center expansion, and manufacturing reshoring initiatives are increasing demand for high-performance piping systems.

U.S. Seamless Pipes Market Trends

The U.S. is expected to be the largest seamless pipes market in North America, driven by shale oil and gas production, refinery modernization projects, and extensive pipeline infrastructure investments. Demand remains particularly strong in the Permian Basin, Gulf Coast region, and major industrial corridors. Rising investments in power generation, carbon capture projects, hydrogen infrastructure, and data center developments are further supporting seamless pipe consumption. Domestic manufacturing initiatives and supply chain localization strategies continue to strengthen market growth prospects.

Canada Seamless Pipes Market Trends

Canada contributes significantly to regional demand through its oil sands operations, natural gas production, mining activities, and pipeline development projects. Investments in LNG export facilities, energy transportation infrastructure, and industrial processing facilities are creating steady demand for high-strength seamless pipes. The country's focus on energy security and sustainable resource development supports long-term market opportunities.

Europe Seamless Pipes Market Trends

Europe's seamless pipes market is increasingly influenced by energy transition initiatives, industrial modernization programs, and decarbonization objectives. The region is witnessing growing demand for pipes used in hydrogen projects, carbon capture systems, geothermal developments, and renewable energy infrastructure. Strict environmental regulations and sustainability targets are encouraging the adoption of advanced manufacturing technologies and low-carbon steel production processes. While overall volume growth remains moderate compared to Asia Pacific, Europe continues to be a key market for high-value seamless pipe applications.

Germany Seamless Pipes Market Trends

Germany represents the largest seamless pipes market in Europe due to its strong industrial base, advanced manufacturing sector, and ongoing investments in energy infrastructure. Demand is driven by engineering, chemical processing, automotive manufacturing, and hydrogen development projects. The country's focus on industrial decarbonization and energy transition initiatives is increasing demand for premium-grade seamless pipe solutions.

U.K. Seamless Pipes Market Trends

The U.K. remains an important market due to investments in offshore energy projects, carbon capture and storage facilities, hydrogen infrastructure, and industrial modernization programs. Offshore developments in the North Sea continue to support demand for corrosion-resistant seamless pipes, while government-backed net-zero initiatives create additional growth opportunities.

France Seamless Pipes Market Trends

France's market is supported by nuclear energy infrastructure, industrial manufacturing, chemical processing facilities, and renewable energy investments. The country's emphasis on low-carbon energy systems and industrial sustainability is generating demand for high-performance seamless pipe products used in critical applications.

Spain Seamless Pipes Market Trends

Spain is emerging as an attractive market due to increasing investments in renewable energy, hydrogen production facilities, and energy transmission infrastructure. The country's growing role in Europe's energy transition strategy is expected to create long-term opportunities for seamless pipe manufacturers.

Asia Pacific Seamless Pipes Market Trends

Asia Pacific is expected to be the dominant regional market, accounting for approximately 46.6% of global seamless pipe demand. The region benefits from rapid industrialization, infrastructure development, urbanization, and manufacturing expansion. Strong investments in energy, transportation, construction, and industrial projects continue to support demand across multiple end-use sectors. Cost advantages, large-scale manufacturing capabilities, and robust domestic consumption make Asia Pacific the primary growth engine of the global market.

China Seamless Pipes Market Trends

China is expected to be the largest market within Asia Pacific, representing approximately 54% of regional demand in 2026. The country's dominant steel industry, extensive manufacturing ecosystem, and large-scale infrastructure investments drive substantial consumption of seamless pipes. Continued spending on energy projects, transportation networks, industrial facilities, petrochemical plants, and urban development initiatives reinforces China's leadership position in the global market.

India Seamless Pipes Market Trends

India is estimated to account for approximately 26.4% of regional demand in 2026 and is among the fastest-growing seamless pipes markets globally. Government-led infrastructure projects, industrial corridor developments, refinery expansions, renewable energy investments, and manufacturing growth are creating significant opportunities. The country's expanding oil & gas, power generation, and construction sectors are expected to support strong long-term demand.

Japan Seamless Pipes Market Trends

Japan remains a key market for high-quality seamless pipes used in power generation, automotive manufacturing, engineering, and industrial processing applications. Demand is supported by technological innovation, infrastructure maintenance projects, and investments in advanced energy systems, including hydrogen-related initiatives.

Competitive Landscape

The global seamless pipes market exhibits a moderately consolidated structure at the global level, with a limited number of multinational manufacturers controlling a substantial share of premium product segments. Leading companies maintain competitive advantages through technological expertise, extensive distribution networks, product certifications, and long-standing customer relationships. Competition is increasingly centered on product quality, operational efficiency, alloy development, and sustainability performance.

Leading market participants are focusing on premium product development, geographic expansion, sustainability initiatives, and advanced manufacturing technologies. Strategic priorities include capacity modernization, specialty alloy development, digital quality control systems, and long-term customer agreements. Companies are increasingly investing in low-carbon steel production and value-added tubular solutions to differentiate themselves in a competitive market environment.

Key Industry Developments

- In May 2026, Tenaris S.A. announced the acquisition of Artrom Steel Tubes S.A., a Romanian seamless pipe manufacturer, for approximately EUR 86 million.

- In May 2026, Vallourec S.A. secured major line pipe orders from ExxonMobil Guyana Limited for the Hammerhead and Longtail deepwater projects in the Stabroek Block.

Companies Covered in Seamless Pipes Market

- Tenaris S.A.

- Vallourec S.A.

- Nippon Steel Corporation

- JFE Steel Corporation

- TMK (Pipe Metallurgical Company)

- United States Steel Tubular Products, Inc.

- Maharashtra Seamless Limited

- Jindal SAW Ltd.

- ArcelorMittal Tubular Products

- Alleima AB

- Sumitomo Corporation (Sumitomo Steel Pipe Division)

- TPCO (Tianjin Pipe Corporation)

- Hengyang Valin Steel Tube Co., Ltd.

- Baowu Special Metallurgy Co., Ltd.

- ChelPipe Group (Chelyabinsk Pipe Rolling Plant)

- Hyundai Steel Company Limited

Frequently Asked Questions

The global seamless pipes market is estimated to be valued at US$108.2 billion in 2026.

The global seamless pipes market is projected to reach US$161.6 billion by 2033.

Key trends include increasing investments in oil & gas infrastructure, growing demand from power generation projects, expansion of hydrogen and carbon capture infrastructure, adoption of premium alloy pipes, and rising industrialization across Asia Pacific.

The oil & gas segment is the leading end-use industry, accounting for approximately 41.2% of the market share in 2026.

The seamless pipes market is expected to expand at a CAGR of 5.9% between 2026 and 2033.

Major companies include Tenaris, Vallourec, Nippon Steel Corporation, JFE Steel Corporation, and TMK (Pipe Metallurgical Company).