- Technology

- Rugged Thermal Cameras Market

Rugged Thermal Cameras Market Size, Share, and Growth Forecast 2026 - 2033

Rugged Thermal Cameras Market by Product Type (Handheld Rugged Thermal Cameras, Fixed-Mount Rugged Thermal Cameras, Helmet-Mounted Rugged Thermal Cameras, Drone-Mounted Rugged Thermal Cameras, Vehicle-Mounted Rugged Thermal Cameras, Wearable Thermal Cameras), Technology, Connectivity, Application, End-user, and Regional Analysis, 2026 - 2033

Rugged Thermal Cameras Market Size and Trend Analysis

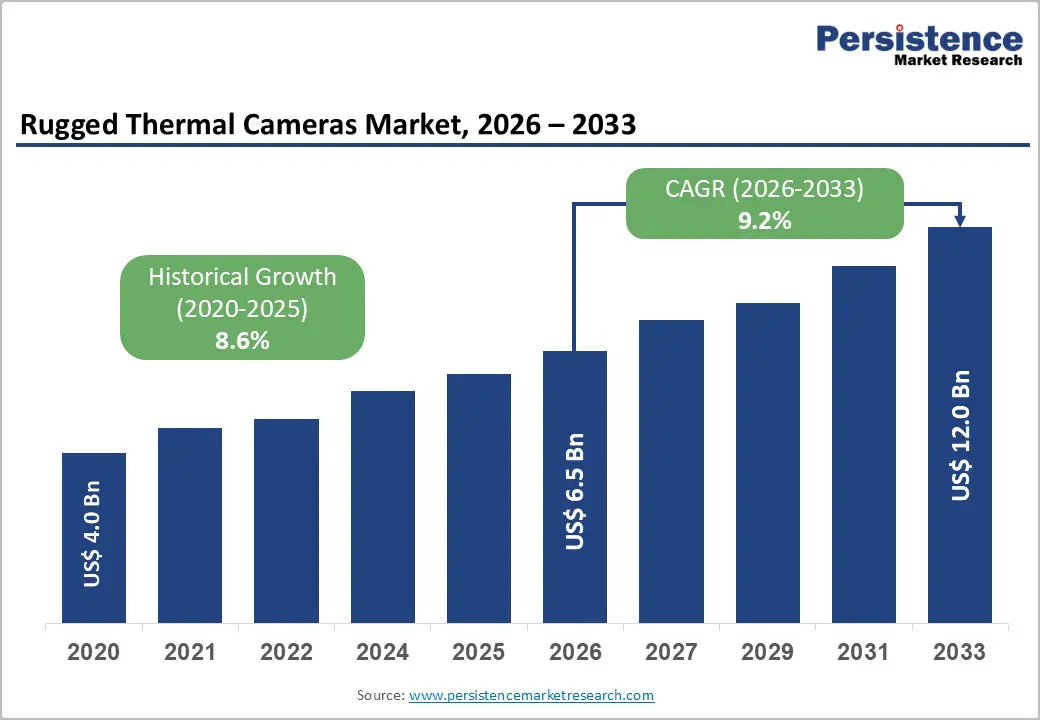

The global rugged thermal cameras market size is likely to be valued at US$ 6.5 billion in 2026 and is expected to reach US$ 12.0 billion by 2033, growing at a CAGR of 9.2% during the forecast period from 2026 to 2033. The market's robust expansion is primarily fueled by escalating global defense spending, rapid proliferation of unmanned aerial vehicles (UAVs), and intensifying demand for advanced situational awareness technologies in both military and civilian domains.

Key Industry Highlights:

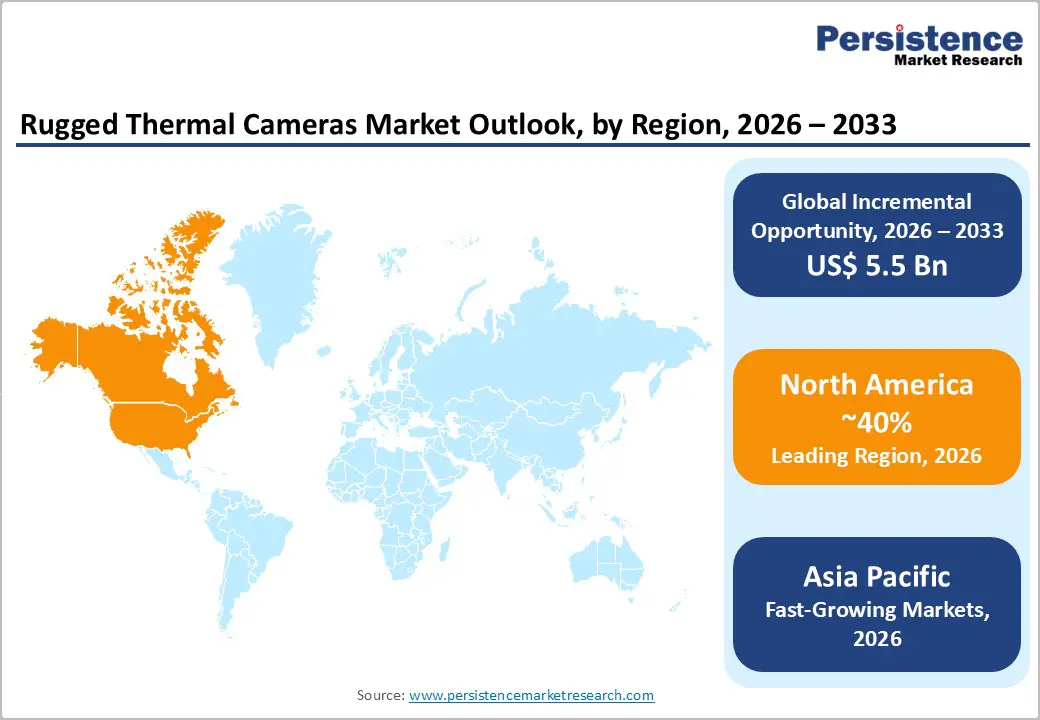

- Leading Region: North America dominates the global rugged thermal cameras market holding 40% share, driven by the U.S. DoD's multi-billion-dollar procurement of advanced EO/IR systems and a robust domestic manufacturing ecosystem anchored by Teledyne FLIR and Raytheon Technologies.

- Fast-Growing Region: Asia Pacific is the fast-growing market, propelled by China, India, and ASEAN defense modernization programs, India's Atmanirbhar Bharat initiative, and rapid expansion of industrial and border surveillance infrastructure across the region.

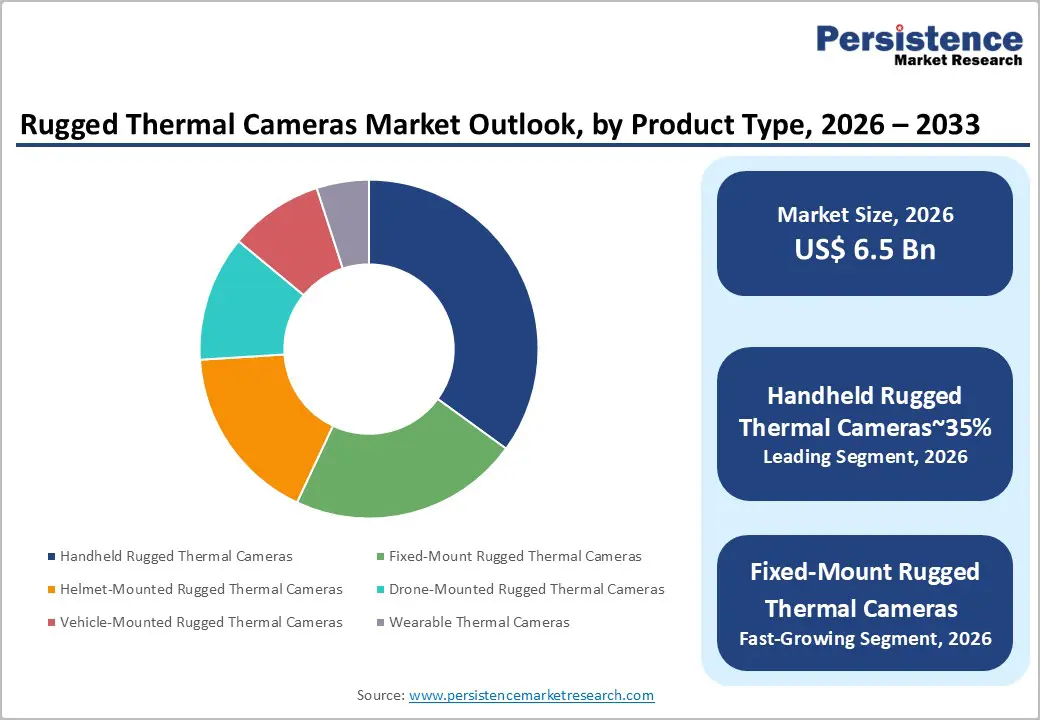

- Dominant Segment: Handheld Rugged Thermal Cameras hold the leading product-type share (~35%), favored for their portability and versatility across military reconnaissance, industrial inspection, and firefighting applications meeting MIL-STD-810 standards.

- Fastest Growing Segment: Drone-Mounted Rugged Thermal Cameras represent the fastest-growing product segment, driven by global UAV adoption across defense, public safety, and infrastructure inspection sectors, integrated with AI-powered real-time thermal analytics capabilities.

- Key Market Opportunity: Healthcare diagnostics and mass fever screening applications present a high-growth opportunity, with WHO-endorsed thermal screening protocols and IEC 80601-2-59 standards creating sustained institutional procurement demand across hospitals, airports, and public facilities.

Market Dynamics

Drivers - Surging Defense Modernization and Border Security Investments

Global defense modernization programs represent the most powerful structural driver for rugged thermal cameras. Nations across North America, Europe, and the Indo-Pacific are substantially upgrading their electro-optical and infrared (EO/IR) sensor portfolios to address asymmetric threats, contested borders, and hybrid warfare scenarios. The U.S. Department of Defense (DoD) has consistently allocated multi-billion-dollar budgets for night vision and thermal imaging modernization under programs such as the Enhanced Night Vision Goggle-Binocular (ENVG-B) and the Family of Weapon Sights-Individual (FWS-I).

The European Defence Agency (EDA) has highlighted thermal imaging systems as a key priority in its Capability Development Plan. These investments are not isolated; they reflect a systemic shift wherein governments recognize thermal cameras as force multipliers for both offensive operations and strategic surveillance, directly sustaining demand for military-grade rugged thermal imaging platforms.

Expanding Industrial and Critical Infrastructure Deployment

Beyond defense, the accelerating adoption of rugged thermal cameras in industrial inspection, energy asset monitoring, and critical infrastructure protection is generating sustained commercial demand. The global shift toward Industry 4.0 and smart manufacturing has elevated predictive maintenance as a strategic operational priority.

According to the International Energy Agency (IEA), investment in energy infrastructure modernization exceeded US$ 1.1 trillion in 2023, with thermal imaging technologies playing a central role in detecting electrical faults, pipeline leaks, and insulation failures. Additionally, the proliferation of offshore wind farms and solar energy installations, requiring continuous, weather-resistant monitoring, has further catalyzed adoption. Rugged thermal cameras, capable of operating in extreme temperatures, high humidity, and corrosive marine environments, are uniquely positioned to serve these demanding applications.

Restraints - High Acquisition and Integration Costs

The elevated cost of advanced rugged thermal cameras, particularly cooled infrared systems, remains a significant barrier to broader adoption, especially in price-sensitive developing markets and small-to-medium enterprise (SME) segments. Cooled thermal cameras, which utilize cryogenic cooling mechanisms to achieve higher sensitivity, can cost between US$ 50,000 and US$ 500,000 per unit for defense-grade systems.

Even uncooled alternatives entail substantial integration costs when deployed in complex industrial or mobile platforms. These financial constraints limit procurement cycles and slow the replacement of legacy systems, thereby dampening overall market velocity in cost-constrained end-user segments.

Stringent Export Controls and Regulatory Barriers

Rugged thermal cameras, particularly those designed for defense applications, are subject to rigorous export control regimes that constrain cross-border trade flows. In the United States, thermal imaging products fall under the jurisdiction of the International Traffic in Arms Regulations (ITAR) and the Export Administration Regulations (EAR), administered by the U.S. Department of State and Department of Commerce respectively.

The European Union's Common Military List imposes strict licensing requirements for the export of thermal imaging systems. These regulatory frameworks significantly increase compliance costs, extend procurement timelines, and restrict market access for manufacturers seeking to penetrate emerging markets.

Opportunities - Drone-Mounted Thermal Cameras: A High-Growth Frontier

The rapid commercialization of unmanned aerial vehicles (UAVs) across defense, public safety, agriculture, and infrastructure inspection sectors is creating an extraordinary growth opportunity for drone-mounted rugged thermal cameras. The Federal Aviation Administration (FAA) reported over 900,000 registered drones in the United States alone as of 2023, with commercial drone deliveries and inspection applications growing at double-digit rates.

Globally, government agencies are investing in UAV-mounted thermal sensors for border patrol, disaster response, and wildlife conservation. The integration of AI-powered analytics with drone-mounted thermal cameras, enabling automated target detection, heat anomaly identification, and real-time situational awareness, is significantly enhancing operational value. Manufacturers who develop lightweight, low-power, high-resolution thermal modules specifically optimized for UAV platforms are well positioned to capture this fast-expanding segment.

Healthcare Diagnostics and Fever Screening: Post-Pandemic Demand Surge

The global pandemic underscored the critical role of thermal imaging in mass fever screening and healthcare diagnostics, creating a durable demand signal that extends well beyond emergency response contexts. The World Health Organization (WHO) and numerous national health authorities have incorporated thermal screening protocols into standard public health preparedness frameworks.

Hospitals, airports, border crossing points, and large public venues are increasingly deploying rugged thermal cameras capable of simultaneous multi-person temperature measurement. The International Electrotechnical Commission (IEC) has published standards (IEC 80601-2-59) specifically for screening thermographs, providing regulatory clarity that encourages institutional procurement. The convergence of healthcare diagnostics with thermal imaging technology represents a significant diversification opportunity for manufacturers targeting civilian and commercial end-user segments.

Category-wise Analysis

By Product Type Insights

Within the product type segmentation, handheld rugged thermal cameras are likely to command the leading share, approximately 35% globally. This is attributed to their unparalleled versatility and portability across a diverse array of operational scenarios, from military reconnaissance and law enforcement to industrial inspection and firefighting.

Handheld units offer tactical flexibility that fixed and vehicle-mounted systems cannot replicate in dynamic field environments. Leading platforms such as the Teledyne FLIR SCION and Fluke TiX Series have set benchmarks for ruggedness, meeting MIL-STD-810 environmental standards. Rapid advancements in detector miniaturization and battery efficiency continue to enhance the operational endurance and imaging performance of handheld units, sustaining their dominant position across both defense and commercial end-user verticals.

By Technology Insights

The uncooled thermal cameras account for a dominant share of approximately 72% of the global market. Uncooled detectors, predominantly based on microbolometer technology, have undergone transformative cost reductions driven by semiconductor fabrication advancements, making them economically accessible for a broad spectrum of commercial and military applications.

Unlike cooled systems, uncooled cameras require no cryogenic cooling mechanisms, resulting in lower manufacturing costs, reduced power consumption, faster startup times, and greater operational reliability in harsh environments. The U.S. Army Research Laboratory and various defense procurement agencies globally have transitioned substantially toward uncooled systems for frontline soldier equipment. Ongoing improvements in noise-equivalent temperature difference (NETD) performance of uncooled detectors are progressively narrowing the sensitivity gap relative to cooled systems.

By Connectivity Insights

The wireless connectivity leads the connectivity category, accounting for approximately 48% market share in 2026. The proliferation of wireless-enabled rugged thermal cameras is driven by the operational necessity for real-time data transmission in dynamic field environments, where wired connections impose mobility constraints.

Technologies such as Wi-Fi 6, 5G, and encrypted tactical radio links have enhanced the bandwidth, range, and cybersecurity posture of wireless thermal imaging networks. In military operations, wireless connectivity enables seamless integration with command-and-control systems and unmanned platforms, while in industrial settings, it supports Industrial IoT (IIoT) architectures for remote monitoring and predictive maintenance. Regulatory bodies such as the IEEE continue to develop standards that further strengthen secure wireless communication for critical sensing infrastructure.

By Application Insights

The security & surveillance application segment dominates the rugged thermal cameras market, commanding approximately 28% of the overall application revenue. The relentless global focus on physical security, encompassing perimeter defense, critical infrastructure protection, and urban surveillance, drives sustained institutional procurement. Fixed-mount and vehicle-mounted thermal cameras are integral to advanced surveillance networks deployed by government agencies, military installations, and commercial facilities.

The U.S. Department of Homeland Security (DHS) has extensively documented the superiority of thermal imaging over conventional visible-light cameras for perimeter intrusion detection under low-visibility conditions. Furthermore, the integration of thermal surveillance systems with AI-powered video analytics platforms, enabling automated intrusion detection, behavioral analysis, and real-time alerting, substantially elevates the operational value proposition of thermal surveillance deployments.

By End-user Insights

The aerospace & defense end-user segment retains the leading position in the rugged thermal cameras market, accounting for approximately 34% of total market revenue. This dominance reflects the sector's non-negotiable requirement for high-performance, environmentally hardened thermal imaging systems capable of withstanding extreme operational conditions. Defense procurement programs, spanning soldier-worn systems, vehicle-mounted sights, naval surveillance platforms, and airborne sensor pods, consistently represent the highest per-unit-value thermal camera acquisitions globally.

The NATO alliance's collective defense spending commitments, particularly the 2% GDP defense expenditure target, have reinforced multi-year procurement pipelines for EO/IR systems across member nations. Companies including Raytheon Technologies, L3Harris Technologies, and BAE Systems continue to secure significant defense contracts for advanced thermal imaging platforms.

Regional Insights

North America Rugged Thermal Cameras Market Trends and Insights

North America accounted for an estimated 36.5% share of the global rugged thermal cameras market in 2026. The region’s dominance is supported by sustained U.S. defense modernization spending, rising deployment of EO/IR surveillance systems, and growing adoption across industrial safety, border security, and critical infrastructure monitoring. Technological leadership from established manufacturers and strong federal procurement programs continue to reinforce market growth across military and commercial sectors.

- United States Rugged Thermal Cameras Market Size

The U.S. represents the largest national market globally, estimated at nearly US$ 2.05 Billion in 2026. Market expansion is driven by extensive Department of Defense procurement programs, integration of thermal imaging into soldier modernization initiatives, and increasing homeland security investments. Industrial applications across oil & gas, utilities, and firefighting also contribute significantly to demand growth, while domestic OEM innovation strengthens technological competitiveness.

Europe Rugged Thermal Cameras Market Trends and Insights

Europe accounted for approximately 28.0% of the global rugged thermal cameras market in 2026, reaching an estimated US$ 1.82 Billion. The regional market is being accelerated by heightened geopolitical tensions, NATO-aligned defense upgrades, and increased investments in border surveillance and battlefield situational awareness systems. Industrial automation, smart manufacturing, and energy infrastructure modernization across Western Europe are further supporting thermal imaging adoption in non-defense sectors.

- Germany Rugged Thermal Cameras Market Size

Germany is Europe’s leading rugged thermal cameras market, valued at approximately US$ 520 Million in 2026. Growth is supported by the Bundeswehr modernization initiative and expanded procurement of advanced surveillance systems under the €100 billion defense investment program. Germany’s strong industrial manufacturing ecosystem also drives substantial adoption of rugged thermal imaging solutions for predictive maintenance, industrial inspection, and energy infrastructure monitoring.

- United Kingdom Rugged Thermal Cameras Market Size

The U.K. rugged thermal cameras market is estimated at around US$ 410 Million in 2026. Demand is fueled by defense modernization programs, naval surveillance upgrades, and increasing deployment of thermal systems in border protection and law enforcement applications. The presence of advanced defense contractors and continued investment in ISR (Intelligence, Surveillance, and Reconnaissance) capabilities are strengthening long-term market expansion.

- France Rugged Thermal Cameras Market Size

France accounted for an estimated US$ 360 Million market size in 2026. The country continues to invest heavily in advanced EO/IR technologies for military vehicles, airborne surveillance, and homeland security applications. Domestic aerospace and defense manufacturers are enhancing indigenous thermal imaging capabilities, while industrial demand from transportation, utilities, and energy sectors is creating additional commercial growth opportunities.

Asia Pacific Rugged Thermal Cameras Market Trends and Insights

Asia Pacific is the fast-growing regional market, accounting for nearly 24.5% of the global market in 2026, equivalent to approximately US$ 1.59 Billion. Rising territorial security concerns, accelerated military modernization, and increasing industrial automation across China, India, Japan, and ASEAN countries are driving rapid adoption. Expanding local manufacturing capabilities and government-backed indigenous technology initiatives are further strengthening regional supply chains and reducing import dependency.

- China Rugged Thermal Cameras Market Size

China is the largest Asia Pacific market, estimated at approximately US$ 710 Million in 2026. Growth is driven by extensive military modernization programs, expansion of domestic thermal imaging manufacturing capabilities, and increasing deployment in smart infrastructure and industrial automation. Chinese manufacturers are rapidly improving sensor quality and production scale, positioning the country as both a major consumer and exporter of rugged thermal imaging technologies.

- India Rugged Thermal Cameras Market Size

India’s rugged thermal cameras market is projected at nearly US$ 290 Million in 2026. The market is benefiting from rising border surveillance requirements, defense procurement initiatives, and the Atmanirbhar Bharat program promoting indigenous manufacturing. Increasing adoption across railways, industrial safety, firefighting, and power infrastructure inspection is also expanding the commercial application base for rugged thermal imaging systems.

- Japan Rugged Thermal Cameras Market Size

Japan’s rugged thermal cameras market reached an estimated US$ 330 Million in 2026. Demand is supported by advanced defense electronics programs, industrial robotics integration, and high adoption of predictive maintenance technologies across manufacturing facilities. Japanese electronics firms continue to invest in compact, high-performance infrared imaging systems, strengthening the country’s role in precision thermal imaging innovation for both defense and industrial sectors.

Competitive Landscape

The global rugged thermal cameras market exhibits a moderately consolidated structure, with the top five manufacturers collectively accounting for an estimated 55% of global revenue. Teledyne FLIR and Raytheon Technologies lead the defense segment, leveraging deep government relationships and extensive technology portfolios.

Key competitive differentiators include detector resolution, NETD performance, MIL-STD certification levels, and software analytics integration. Market leaders are aggressively pursuing AI-integration strategies, embedding deep-learning-based target classification and anomaly detection directly into camera firmware. Emerging business model trends include subscription-based thermal analytics platforms, thermal-as-a-service offerings for industrial clients, and modular sensor architectures enabling rapid platform customization.

Key Market Developments

- January, 2025: Teledyne FLIR launched the FLIR Hadron 640R dual thermal-visible camera module optimized for autonomous drone inspection platforms, featuring a radiometric resolution of 640×512 pixels and integrated AI inferencing capabilities for real-time defect detection.

- March, 2024: L3Harris Technologies was awarded a U.S. Army contract worth approximately US$ 400 million for the supply of next-generation Family of Weapon Sights-Individual (FWS-I) thermal weapon sights, reinforcing its market leadership in soldier-worn thermal systems.

- September, 2023: Thales Group unveiled its enhanced Catherine-XP thermal camera system for armored vehicle platforms at the DSEI defense exhibition in London, incorporating third-generation InSb cooled detector technology with extended detection ranges exceeding 10 km.

Global Rugged Thermal Cameras Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 4.0 Billion |

|

Current Market Value (2026) |

US$ 6.5 Billion |

|

Projected Market Value (2033) |

US$ 12.0 Billion |

|

CAGR (2026–2033) |

9.2% |

|

Leading Region |

North America (40%) |

|

Top-ranking Product Type |

Handheld Rugged Thermal Cameras (35.0%) |

|

Top-ranking Technology |

Uncooled Thermal Cameras (75.0%) |

|

Incremental Opportunity (2026–2033) |

US$ 5.5 Billion |

Companies Covered in Rugged Thermal Cameras Market

- Teledyne FLIR

- L3Harris Technologies

- Leonardo DRS

- BAE Systems

- Axis Communications

- Opgal Optronic Industries

- Seek Thermal

- Fluke Corporation

- Raytheon Technologies

- Thales Group

- Hensoldt

- Xenics

- InfraTec GmbH

- Testo SE & Co. KGaA

- Guide Sensmart

- DRS Technologies (Leonardo DRS)

- Photonis Technologies

- ULIS (Lynred)

- Sierra-Olympic Technologies

- Infrared Cameras Inc.

Frequently Asked Questions

The global rugged thermal cameras market is estimated to be valued at US$ 6.5 billion in 2026 and is projected to reach US$ 12.0 billion by 2033, expanding at a CAGR of 9.2% during the forecast period.

The primary demand drivers include escalating global defense modernization expenditure, exceeding US$ 2.2 trillion globally according to SIPRI, alongside rapid UAV proliferation, stringent border security requirements, growing adoption in industrial predictive maintenance under Industry 4.0 frameworks, and post-pandemic institutional adoption of thermal fever screening protocols.

Handheld Rugged Thermal Cameras represent the dominant product type segment, accounting for approximately 35% of global market revenue. Their leadership is driven by superior portability, versatility across military, law enforcement, and industrial applications, compliance with MIL-STD-810 environmental standards, and ongoing miniaturization of uncooled microbolometer detector technology.

North America holds the largest regional share in the global rugged thermal cameras market, with the United States serving as the primary demand driver through extensive DoD procurement programs. The region benefits from a mature defense industrial base, robust innovation ecosystem, and strong regulatory frameworks administered by bodies such as NIST and the DoD's acquisition agencies.

The most significant growth opportunities lie in drone-mounted thermal cameras, driven by FAA-registered UAV proliferation exceeding 900,000 units in the U.S. and global adoption for border patrol and infrastructure inspection, and in healthcare diagnostics applications, supported by WHO fever screening mandates and IEC 80601-2-59 standards that are driving sustained institutional procurement.