- Hardware & Software IT Services

- Public Cloud System Infrastructure Services Market

Public Cloud System Infrastructure Services Market Size, Share, and Growth Forecast 2026–2033

Public Cloud System Infrastructure Services Market by Service (Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS)), Enterprise Size (SMEs, Large Enterprises), End-user (BFSI, IT & Telecom, Retail & Consumer Goods, Manufacturing, Energy & Utilities, Healthcare, Media & Entertainment, Government & Public Sector, Others), and Regional Analysis for 2026–2033

Public Cloud System Infrastructure Services Market Size and Trend Analysis

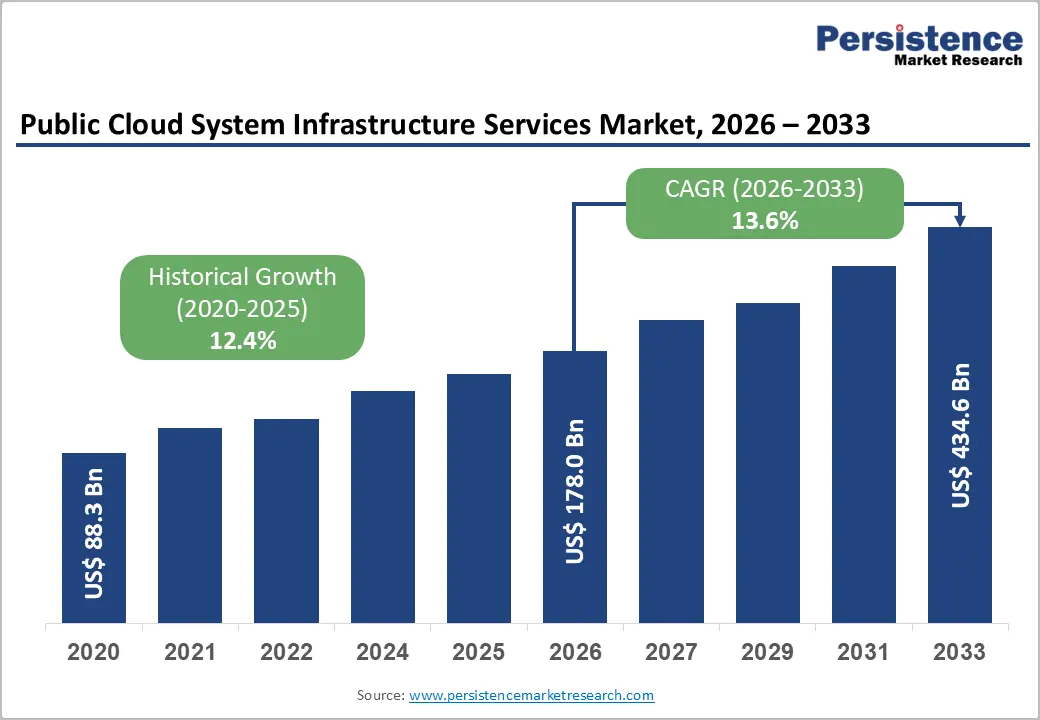

The global public cloud system infrastructure services market size is valued at approximately US$ 172.8 billion in 2026 and is projected to reach US$ 434.6 billion by 2033, growing at a CAGR of 13.6% between 2026 and 2033.

This robust growth is primarily fueled by the accelerating enterprise migration to cloud-native architectures, driven by demand for scalable computing resources and digital transformation imperatives across industries. The proliferation of data-intensive applications, AI/ML workloads, and the global rollout of 5G networks are further intensifying enterprise dependence on cloud infrastructure.

Key Industry Highlights

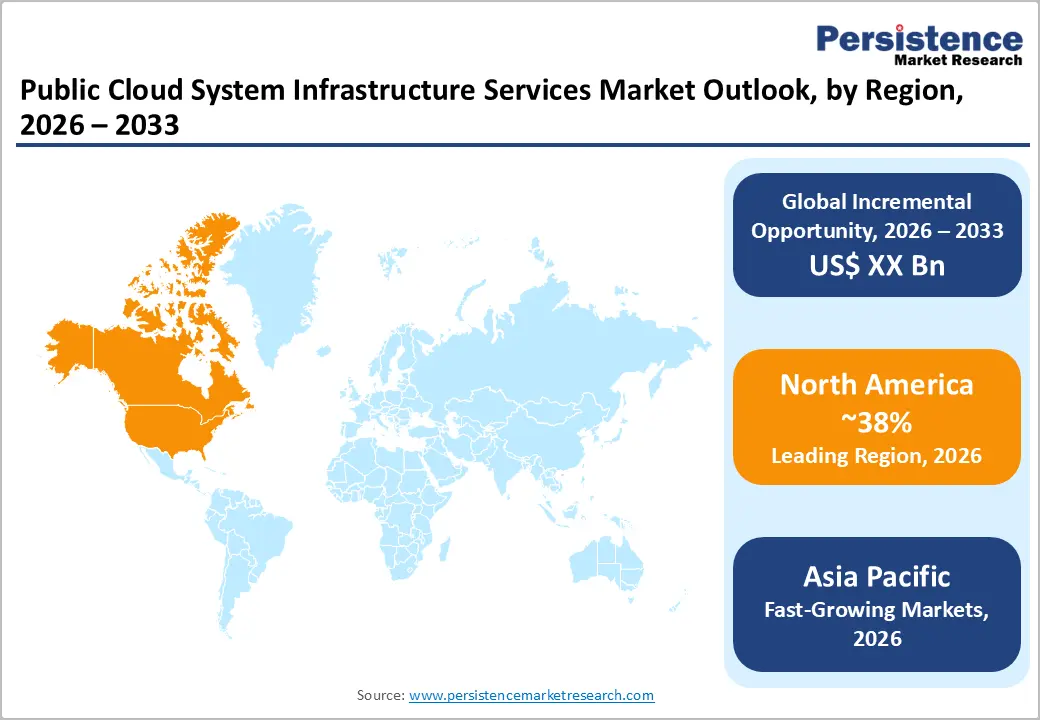

- Leading Region: North America dominates the global Public Cloud System Infrastructure Services market with approximately 38% revenue share in 2026, driven by hyperscaler headquarters, mature enterprise cloud adoption, and significant federal cloud procurement programs.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, projected to expand at a CAGR exceeding 17% through 2033, fueled by digital transformation in China, India, and Southeast Asia, along with hyperscaler data centre expansion.

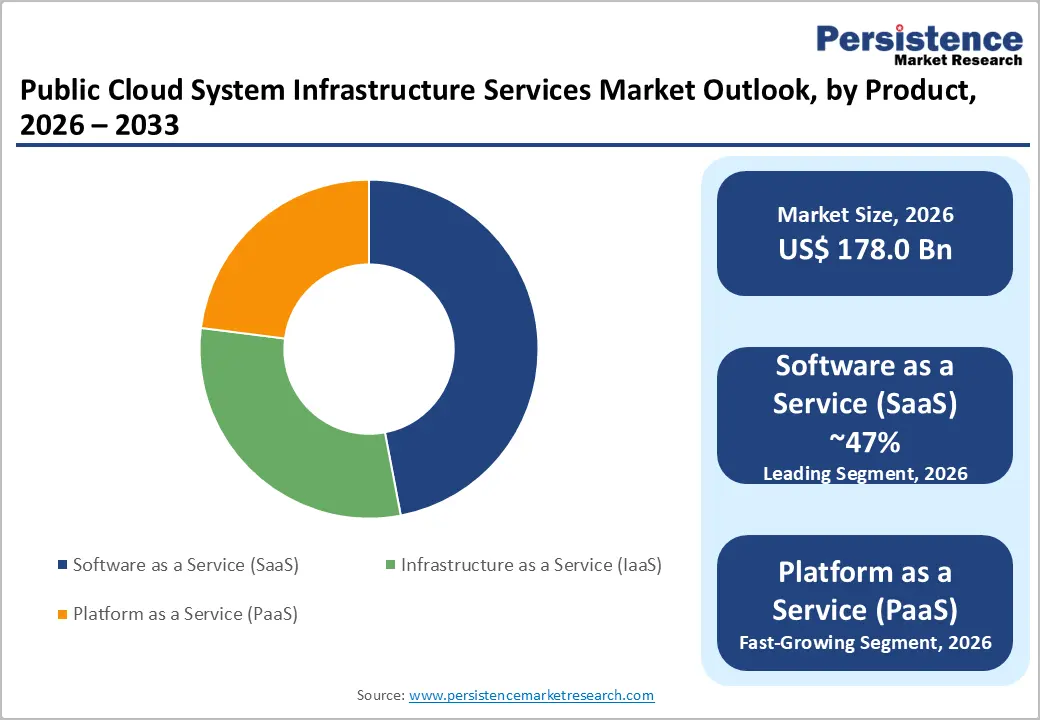

- Dominant Segment: Software as a Service (SaaS) is the leading service segment, accounting for approximately 47% of total market revenue, driven by widespread enterprise adoption of cloud-based productivity and operational applications.

- Fastest Growing Segment: Infrastructure as a Service (IaaS) is the fastest-growing service segment, propelled by surging AI/ML workload deployments, edge computing integration, and hyperscaler GPU infrastructure buildouts globally.

- Key Opportunity: Government digitalization programs and cloud infrastructure expansion in emerging economies, including India’s Digital India and Saudi Arabia’s Vision 2030, represent significant untapped revenue pockets for cloud infrastructure vendors.

DRO Analysis

Drivers - Accelerating Enterprise Digital Transformation and Cloud-First Mandates

The global push toward digital transformation remains the most powerful catalyst for cloud infrastructure adoption. Governments and large enterprises across sectors are implementing cloud-first policies to modernize legacy IT systems. The U.S. Federal Government’s Cloud Smart Strategy, for instance, has directed agencies to prioritize cloud services, unlocking significant demand for public cloud infrastructure.

According to the World Economic Forum, digital transformation is expected to unlock US$ 100 Tn in value for businesses and society by 2025. Cloud infrastructure services underpin this transition by providing elastic compute, storage, and networking capabilities without capital expenditure.

Surge in AI, Big Data, and High-Performance Computing Workloads

The exponential growth of artificial intelligence, machine learning, and big data analytics is driving unprecedented demand for high-performance cloud infrastructure. Training large language models and deploying AI inference engines requires massive parallel computing capabilities that only hyperscale public cloud providers can cost-effectively deliver.

According to Stanford University’s AI Index Report 2024, industry AI training costs have grown over 5x in the past three years, with cloud-based GPU clusters serving as the primary compute substrate. The NVIDIA H100 and next-generation accelerator deployments by all major cloud providers reflect this trend.

Restraints - Data Security, Privacy Regulations, and Compliance Complexity

Despite rapid adoption, stringent data sovereignty and compliance mandates remain a significant brake on public cloud expansion, particularly for regulated industries. The European Union’s General Data Protection Regulation (GDPR) imposes fines of up to 4% of global annual turnover for data breaches.

Similarly, regulations such as HIPAA in healthcare and PCI-DSS in financial services demand rigorous controls that many public cloud deployments struggle to guarantee. The IBM Cost of a Data Breach Report 2023 put the global average cost of a data breach at US$ 4.45 Mn, deterring enterprises from fully committing to public cloud environments.

Vendor Lock-in and Rise in Cloud Costs (Cloud Sprawl)

Vendor lock-in and uncontrolled cloud spending, commonly referred to as “cloud sprawl,” pose meaningful barriers to market expansion. Organizations often encounter significant switching costs and operational disruptions when migrating between cloud providers due to proprietary APIs and data egress fees.

A Flexera 2024 State of the Cloud Report revealed that 82% of enterprises identified cloud cost management as their top challenge, with average cloud waste estimated at 28% of total cloud spend. This financial unpredictability and architectural dependency on a single provider are increasingly motivating enterprises to delay or limit cloud infrastructure investments.

Market Opportunities

Proliferation of Edge Computing and Hybrid Cloud Architectures

The convergence of edge computing with public cloud infrastructure presents a transformative opportunity for market participants. As latency-sensitive applications in autonomous vehicles, smart manufacturing, and real-time analytics demand computing closer to the data source, cloud providers are extending their infrastructure to the network edge.

According to the Linux Foundation’s State of the Edge Report, global edge computing infrastructure investment was anticipated to exceed US$ 274 Bn by 2025. Major providers, including Amazon Web Services (AWS) with AWS Wavelength and Microsoft Azure Edge Zones are already capitalizing on this trend. Hybrid cloud deployments, which blend on-premises infrastructure with public cloud resources, are also gaining momentum, enabling enterprises to balance compliance requirements with cloud-native scalability, presenting a compelling growth avenue for cloud infrastructure vendors.

Cloud Adoption in Emerging Economies and Government Digitalization Programs

Rapid digitalization across emerging economies in Asia Pacific, Latin America, and Africa represents a largely untapped opportunity for cloud infrastructure providers. India’s Digital India Initiative has invested over US$ 20 Bn in digital infrastructure, while Saudi Arabia’s Vision 2030 has prioritized cloud adoption across public services.

The United Nations E-Government Survey 2024 highlighted that 193 member states are actively pursuing e-government transformation, creating substantial demand for cloud IaaS and PaaS solutions. As hyperscalers expand data centre footprints in these geographies with Google, Microsoft, and AWS each announcing multi-billion-dollar regional investments the market is positioned to unlock significant incremental revenue streams.

Category-wise Analysis

Service Insights

The Software as a Service (SaaS) segment dominates the service category, accounting for approximately 47% of total public cloud infrastructure services revenue. SaaS leadership is underpinned by its broad applicability across enterprise functions from Salesforce’s CRM to Microsoft 365’s productivity suite, eliminating on-premises software management overhead.

According to the Research Group, SaaS remained the largest public cloud segment with consistent double-digit growth. The COVID-19 pandemic-driven remote work surge accelerated SaaS penetration, and this adoption has proven structurally sticky. Subscription-based revenue models and continuous feature updates further reinforce enterprise preference for SaaS, consolidating its dominant position within the public cloud service taxonomy.

Enterprise Size Insights

Large enterprises constitute the dominant segment in the enterprise size category, holding approximately 63% of total market revenue. Large enterprises drive disproportionate cloud consumption due to their scale of digital operations, complex multi-cloud strategies, and capacity to negotiate enterprise-grade service agreements with providers.

According to the IBM Institute for Business Value, organizations with over 1,000 employees allocate more than 30% of their IT budgets to cloud services. However, SMEs represent the fastest-growing cohort, as cloud democratization lowers entry barriers and enables smaller businesses to access enterprise-grade infrastructure without significant capital investment.

End-user Insights

The BFSI (Banking, Financial Services, and Insurance) sector leads end-use adoption, commanding approximately 22% of total market share. Financial institutions are among the most aggressive adopters of cloud infrastructure to support real-time transaction processing, fraud detection using AI, and regulatory reporting.

The Financial Stability Board (FSB) noted in its 2023 report that major global banks including JPMorgan Chase and HSBC, have committed to migrating substantial workloads to public cloud platforms. The heightened focus on open banking APIs, digital payment ecosystems, and InsurTech innovation creates persistent demand for scalable, secure cloud infrastructure across the BFSI vertical.

Regional Analysis

North America Public Cloud System Infrastructure Services Market Trends & Analysis

North America remains the undisputed leader in the global Public Cloud System Infrastructure Services market, accounting for approximately 38% of global revenue. The region benefits from the headquarters of all three hyperscale cloud providers, Amazon Web Services, Microsoft Azure, and Google Cloud, alongside a mature enterprise technology ecosystem and a favorable regulatory environment.

The U.S. National Institute of Standards and Technology (NIST) cloud computing framework has standardized adoption practices, while the FedRAMP program has accelerated federal cloud procurement. Continued investment in AI infrastructure, with over US$ 400 Bn committed by hyperscalers for data centre expansion through 2026, will sustain North America’s dominant position.

U.S. Public Cloud System Infrastructure Services Market Size

The United States accounts for over 90% of the North American market and is the world’s single largest national cloud infrastructure market. Estimated at US$ 58.3 Bn in 2026, the U.S. market is propelled by comprehensive enterprise cloud adoption, the world’s highest concentration of technology companies, and federal cloud migration mandates. The Executive Order on Improving the Nation’s Cybersecurity (2021) further accelerated the migration of government systems to cloud infrastructure.

Europe Public Cloud System Infrastructure Services Market Trends, Drivers, & Insights

Europe is the second-largest regional market, representing approximately 27% of global cloud infrastructure revenues. The region’s market is shaped by a dual dynamic: rising enterprise cloud adoption and strict data sovereignty regulations. The European Commission’s GAIA-X Initiative aims to build a federated, sovereign European cloud infrastructure, stimulating local and regional cloud investment.

Sectors such as manufacturing, automotive, and healthcare are significant contributors to cloud infrastructure spend. The European Union Agency for Cybersecurity (ENISA) reported a 43% increase in cloud security incidents in 2023, driving enterprises to invest in more robust cloud infrastructure and security solutions.

Germany Public Cloud System Infrastructure Services Market Size

Germany is the largest cloud market in Europe, estimated at US$ 14.2 Bn in 2026. The country’s strong industrial base, particularly its Mittelstand (mid-sized industrial enterprises) is rapidly adopting IaaS and PaaS for Industry 4.0 applications. Microsoft Azure and SAP’s cloud partnerships have been central to enterprise cloud adoption in Germany.

U.K. Public Cloud System Infrastructure Services Market Size

The United Kingdom market is estimated at approximately US$ 11.6 Bn in 2026. As one of Europe’s most advanced digital economies, the U.K. has seen aggressive cloud adoption in financial services, retail, and the public sector. The UK Government Cloud First Policy mandates that all government departments consider cloud options before any new infrastructure investment, supporting sustained public-sector cloud demand.

France Public Cloud System Infrastructure Services Market Size

France represents a rapidly growing cloud infrastructure market, valued at approximately US$ 8.9 Bn in 2026. The French government’s France 2030 Investment Plan has allocated significant resources toward digital infrastructure and cloud-native technologies. Sovereign cloud initiatives supported by providers such as OVHcloud and Orange Business Services are driving cloud adoption across sensitive sectors.

Asia Pacific Public Cloud System Infrastructure Services Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market, with a projected CAGR exceeding 17% through 2033. The region benefits from burgeoning digital economies, rapidly expanding internet penetration, and massive government investments in smart city and digital infrastructure projects. Rising e-commerce, fintech expansion, and manufacturing digitalization are primary end-use demand drivers.

Hyperscaler have significantly expanded their Asia Pacific data centre footprints: AWS operates regions across Singapore, Japan, India, and Australia, among others. Local champions such as Alibaba Cloud and Tencent Cloud are competing aggressively, creating a dynamic and high-growth competitive environment.

China Public Cloud System Infrastructure Services Market Size

China is the largest cloud market in Asia Pacific, estimated at approximately US$ 24.1 Bn in 2026. Domestic providers Alibaba Cloud and Huawei Cloud dominate, supported by the government’s “New Infrastructure” initiative investing over US$ 1.4 Tn in digital and tech infrastructure through 2025.

India Public Cloud System Infrastructure Services Market Size

India's cloud infrastructure market is estimated at US$ 9.4 Bn in 2026, growing at one of the fastest rates globally. The government’s Digital India initiative and the National Cloud Policy, combined with a booming startup ecosystem and expanding enterprise IT sector, are driving cloud infrastructure demand. Amazon Web Services and Microsoft Azure have each committed over US$ 3 Bn in Indian data centre investments.

Japan Public Cloud System Infrastructure Services Market Size

Japan’s cloud infrastructure market is estimated at approximately US$ 8.7 Bn in 2026. The country is undergoing a significant cloud modernization drive, accelerated by the government’s Society 5.0 Framework and corporate IT modernization mandates. NEC, Fujitsu, and global hyperscaler are expanding their Japanese cloud presence to serve financial institutions, manufacturing firms, and public sector agencies.

Competitive Landscape

The public cloud system infrastructure services market exhibits a highly consolidated oligopolistic structure, with the top three providers Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, collectively commanding over 65% of global IaaS and PaaS revenues.

These hyperscalers compete aggressively on price, global data centre footprint, AI-integrated services, and ecosystem depth. Key differentiators include AI/ML platform maturity, compliance certifications, developer tooling, and strategic managed services portfolios.

Key Developments

- In December 2025, Amazon Web Services (AWS) announced major public cloud advancements at its re: Invent 2025 event, unveiling powerful new technologies such as autonomous Frontier agents, the Trainium3 Ultra Servers AI training infrastructure, expanded Amazon Nova AI models, and AI Factories for hybrid cloud deployments, strengthening its cloud service capabilities for real-time AI and enterprise workloads.

- In November 2025, Google Cloud announced plans to launch a new public cloud region in Türkiye as part of a USD 2 billion investment in collaboration with Turkcell. This hyperscale cloud region is poised for advanced cloud services, supports AI innovation, improves data security, and meets growing local demand with high-performance, low-latency infrastructure for enterprises and public sector organizations.

Global Public Cloud System Infrastructure Services Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 88.3 Bn |

|

Current Market Value (2026) |

US$ 178.0 Bn |

|

Projected Market Value (2033) |

US$ 434.6 Bn |

|

CAGR (2026-2033) |

13.6% |

|

Leading Region |

North America, 38% share |

|

Dominant Application |

Software as a Service (SaaS),47% share |

|

Top-ranking Product |

BFSI, 22% |

|

Incremental Opportunity |

US$ 4.6 Bn |

Companies Covered in Public Cloud System Infrastructure Services Market

- Amazon Web Services, Inc. (AWS)

- Microsoft Corporation (Azure)

- Alphabet Inc. (Google Cloud)

- Alibaba Cloud

- Oracle Cloud

- IBM Cloud

- Huawei Cloud

- Salesforce

- Tencent Cloud

- SAP SE

- OVHcloud

- NTT DATA

Frequently Asked Questions

The global Public Cloud System Infrastructure Services market is valued at approximately US$ 172.8 Bn in 2026 and is projected to reach US$ 434.6 Bn by 2033, expanding at a robust CAGR of 13.6% during the forecast period.

The primary growth drivers include accelerating enterprise digital transformation mandates, the explosive demand for AI/ML and high-performance computing workloads, and government-led cloud adoption initiatives globally.

Software as a Service (SaaS) is the dominant service segment, accounting for approximately 47% of total market revenue. Its dominance is driven by the broad applicability of cloud-delivered software, subscription-based monetization models, and the elimination of enterprise on-premises management overhead, as evidenced by the growth of platforms such as Microsoft 365 and Salesforce.

North America is the leading region, representing approximately 38% of global market revenue in 2026. The region benefits from the headquartering of the world’s three largest cloud providers, a mature enterprise technology ecosystem, and strong federal cloud procurement programs, including FedRAMP and the U.S. Cloud Smart Strategy.

The market is led by a consolidated set of global hyperscaler and enterprise cloud providers. The key companies include Amazon Web Services (AWS), Microsoft Azure, Google Cloud (Alphabet Inc.), Alibaba Cloud, Oracle Cloud Infrastructure, IBM Cloud, Huawei Cloud, and Tencent Cloud, among others.