- Hardware & Software IT Services

- Global Casino Gaming Equipment Market

Global Casino Gaming Equipment Market Size, Share, and Growth Forecast 2026–2033

Casino Gaming Equipment Market by Product Type (Slot Machines, Video Lottery Terminals (VLTs), Casino Tables & Electronic Table Games, Video Poker Machines, Gaming Chips & Accessories, Others), Mode of Operation (Land-Based Gaming Equipment, Hybrid Connected Gaming Systems, Online-Integrated Casino Equipment), End-user, and Regional Analysis, 2026–2033

Global Casino Gaming Equipment Market Size and Trend Analysis

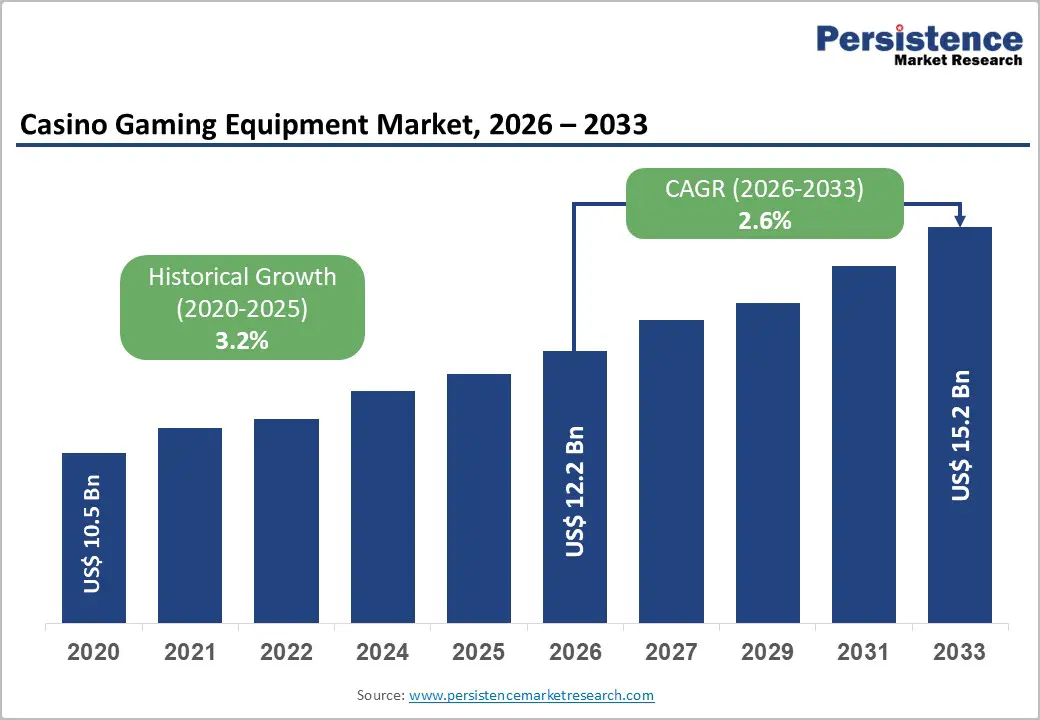

The global casino gaming equipment market is expected to be valued at US$ 12.20 billion in 2026 and is projected to reach US$ 15.21 billion by 2033, at a CAGR of 3.2% between 2026 and 2033.

The global casino gaming equipment market comprises slot machines, electronic gaming terminals, table game equipment, casino management systems, and related technologies used across commercial and tribal casinos. Market growth is driven by casino expansion, rising gaming tourism, digital integration, and increasing demand for advanced, immersive gaming experiences that enhance operational efficiency and player engagement worldwide.

Key Industry Highlights:

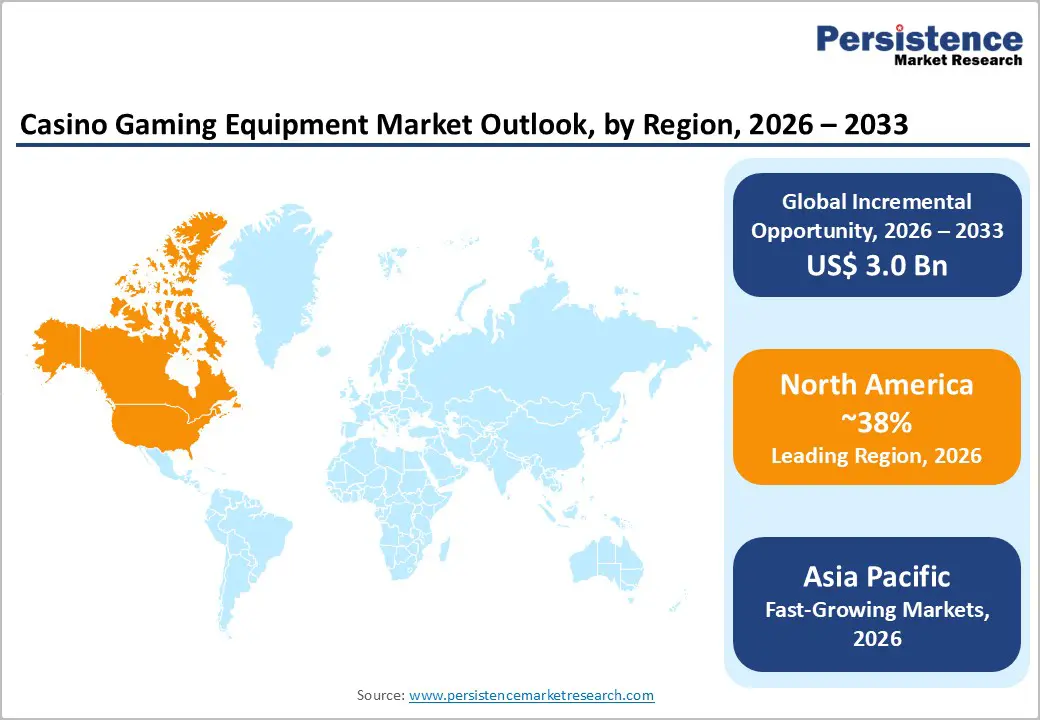

- Leading Region: North America's US$ 4.64 Billion regional market retains the top position in the global casino gaming equipment landscape, backed by pending downstate New York commercial casino licence awards expected to trigger one of the largest single-market equipment procurement cycles since the 2000s Atlantic City expansion era, sustaining the region's leadership through 2033.

- Fastest Growing Region: Asia Pacific's 4.6% CAGR, the fastest of any region, reflects a structural demand shift as post-2022 gaming concession renewals in Macao, new PAGCOR-licensed facilities in the Philippines, and Japan's approaching IR construction phase collectively create a multi-year equipment order book that no other global region can match in aggregate greenfield opportunity size.

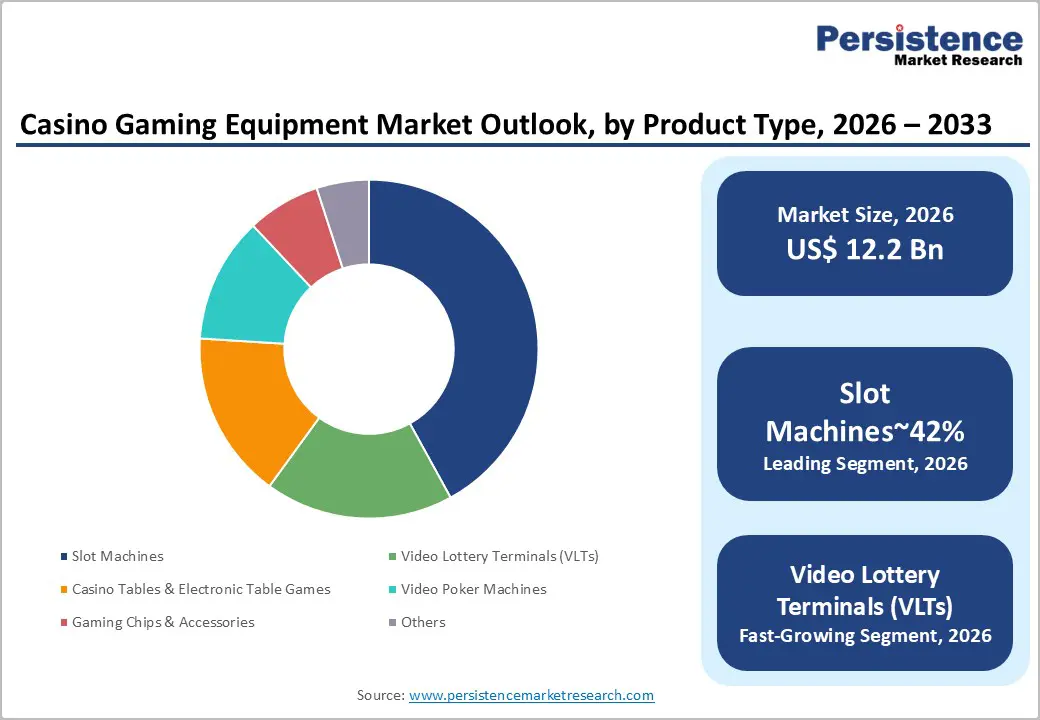

- Leading Product Segment: Slot machines commanding 42.0% product share confirms that physical reel-and-button gaming remains the cornerstone capital investment category for casino operators globally, with U.S. tribal casino replacement cycles and Asian premium slot deployments providing a demand floor that insulates OEM revenues from cyclical demand softness in adjacent product categories.

- Fast-Growing Market: Hybrid connected gaming systems are moving from pilot to mainstream deployment as regulatory approvals in New Jersey, Pennsylvania, and Nevada validate cashless-physical hybrid architectures, positioning OEMs with certified cashless ecosystem products to capture a structurally higher average selling price per unit compared to conventional stand-alone hardware sold in the prior decade.

- Key Opportunity: Integrated resort casinos represent the highest-value per-facility procurement opportunity in the market, with single IR project equipment packages frequently exceeding US$ 100 Million, a scale dynamic that favours OEMs with comprehensive product portfolios spanning slots, electronic tables, and casino management systems, and that will intensify vendor competition for anchor supplier status at upcoming IR developments in Japan, Saudi Arabia, and Thailand.

Market Dynamics

Market Dynamics

Drivers - Accelerating Casino Legalisation and Licensing Pipelines Across Asia-Pacific and North America

Operators and OEMs face an immediate window of procurement-led demand as governments formalise gaming frameworks mandating the sourcing of certified equipment. The implementation of Japan's Casino Regulation Act, with IR Development Act approvals moving forward for Osaka's integrated resort project targeting a 2029 opening, will require purpose-built floor configurations sourced from licensed suppliers, creating a concentrated multi-hundred-million-dollar equipment order cycle. Over the next two to three years, as additional Asian jurisdictions, including Thailand, advance their own casino legalisation debates, OEMs that establish regulatory pre-approval status early will capture disproportionate first-mover contract value.

Floor Technology Modernisation Driven by Player Experience and Yield Optimisation Imperatives

Casino operators are under direct competitive pressure to replace legacy floor assets with networked, analytics-enabled equipment that improves revenue-per-square-foot metrics, a dynamic that directly sustains replacement demand independent of new market openings. Light & Wonder Inc. completed its rebranding and strategic pivot in 2022, dedicating its entire portfolio to systems, content, and cross-platform gaming technology designed to give floor operators real-time yield management capabilities. As cashless gaming is becoming regular, such as those piloted under the Nevada Gaming Control Board cashless wager approvals, the industry is moving toward a broader adoption, enabling the operators to look for hardware upgrades and equipment architectures compatible with digital wallet and TITO-cashless integration.

Restraints - Stringent Regulatory Compliance and Type-Approval Costs Create Meaningful Market Entry Friction

Each jurisdiction requires equipment manufacturers to obtain independent laboratory certification before a single unit can be placed on a casino floor, imposing time-to-market delays of 12 to 24 months and certification costs that can reach into the millions of dollars per product line for new entrants.

The Gaming Laboratories International (GLI) testing regime, which covers more than 480 jurisdictions worldwide, requires hardware and software submissions for each variant, meaning product iteration cycles are structurally slower in gaming than in most adjacent consumer electronics categories. Incumbents with pre-existing multi-jurisdictional approvals hold a durable moat that smaller entrants cannot replicate quickly, effectively rationing competitive pressure at the supply side.

Supply Chain Volatility and Semiconductor Constraints Compress Equipment Margins

Global semiconductor shortages, which the U.S. Department of Commerce estimated caused over $240 billion in lost automotive and electronics revenue in 2021 alone, have left residual lead-time volatility in gaming equipment supply chains that continues to compress gross margins for manufacturers dependent on third-party chip sourcing.

Component lead times for gaming-grade microprocessors and display drivers remain elevated compared to pre-2020 norms, forcing OEMs to either carry higher safety-stock inventory, increasing working capital requirements, or risk delivery delays that breach casino operator procurement contracts.

Opportunities - Server-Based and Cloud-Managed Gaming Systems as a Scalable SaaS-Adjacent Revenue Model

Equipment OEMs that pivot toward recurring software and subscription revenue by deploying server-based gaming (SBG) architectures can structurally de-risk their business models from lumpy hardware replacement cycles and unlock significantly higher lifetime revenue per installed unit.

Konami Gaming Inc. has deployed its SYNKROS casino management system across properties in North America, demonstrating that centralised game content management can reduce floor reconfiguration costs for operators by eliminating per-machine hardware swaps. For this opportunity to fully materialise, operators must standardise on open-architecture hardware platforms, a shift that G2E (Global Gaming Expo) 2023 exhibitor announcements suggested was gaining operator acceptance.

Skill-Based and Hybrid Entertainment Gaming Equipment Targeting Millennial and Gen Z Casino Visitors

Casino operators seeking to broaden demographic appeal beyond traditional slot players represent a compelling addressable market for manufacturers that can deliver equipment blending skill elements with regulated gaming outcomes. The Nevada Legislature's passage of Assembly Bill 162 as early as 2015, with subsequent technical standard updates, created the regulatory template that multiple states have since followed, and manufacturers including Gamblit Gaming validated early commercial interest from operators in non-traditional gaming formats. Equipment suppliers capable of delivering certified hybrid entertainment units with demonstrable floor yield metrics will be best positioned as tribal and commercial operators allocate dedicated floor space to attract under-45 visitor cohorts.

Category-wise Analysis

Product Type Insights

Slot machines are likely to account for 42% of the global casino gaming equipment market in 2026 owing to their position as the single largest product category across all major gaming arenas. The dominance of slot machines traces directly to their unmatched operational economics for casino floors: a single bank of Aristocrat Leisure Limited's MarsX cabinet series, deployed at commercial casinos across Las Vegas and regional U.S. properties, generates higher revenue-per-square-foot than most table game configurations while requiring minimal labour overhead, making them the default capital allocation choice for floor managers.

Video Lottery Terminals (VLTs) are the fast-growing product segment within the casino gaming equipment market, propelled by state and provincial government revenue mandates that are expanding VLT deployment into non-traditional venues. Following the Ontario Lottery and Gaming Corporation's (OLG) expanded VLT program rollout across licensed taverns and charitable gaming facilities in 2023–2024, manufacturers including IGT (International Game Technology) have secured multi-year supply and service contracts that are accelerating unit volumes outside conventional casino floors, a deployment model increasingly being replicated by lottery authorities in European markets including Italy's AAMS-regulated AWP replacement cycle, signalling durable forward demand.

Mode of Operation Insights

Land-based gaming equipment accounts for 78.0% of the global casino gaming equipment market in 2026, equivalent to US$ 9.52 Billion, reflecting the continued primacy of physical casino infrastructure as the primary channel for regulated gaming globally. The category's dominance stems from the capital intensity and regulatory specificity of brick-and-mortar casino operations: operators at properties such as MGM Resorts International's Las Vegas Strip facilities invest hundreds of millions of dollars in floor configurations designed around certified physical hardware, with floor layouts optimised by proprietary analytics systems that track coin-in and time-on-device metrics unavailable in early-generation online environments.

Hybrid connected gaming systems are accelerating as the fast-growing operational mode, driven by operator demand for floor equipment that simultaneously serves in-venue players while feeding real-time data to centralised analytics and remote management platforms. Everi Holdings Inc. commercialised its KIOSK and CashClub Wallet ecosystem from 2022 onward, enabling casino floors to operate physical gaming terminals with full digital cashless connectivity, a configuration that regulators in New Jersey and Pennsylvania approved under updated Division of Gaming Enforcement technical standards, creating a replicable compliance blueprint that other jurisdictions are actively adopting and that will accelerate hybrid system procurement through 2026 and beyond.

End-user Insights

Standalone casinos account for 39.0% of the global casino gaming equipment market in 2026, equivalent to US$ 4.76 Billion, driven by the sheer volume and geographic density of licensed standalone gaming facilities relative to other venue types. Standalone casino operators, particularly tribal gaming enterprises across the United States, which collectively operate over 500 tribal gaming facilities per National Indian Gaming Commission 2023 data, procure equipment in standardised bulk cycles, making them the most consistent and predictable demand cohort for OEM sales teams.

Integrated resort casinos represent the fastest growing end user category as governments across Asia and the Middle East approve large-scale mixed-use entertainment developments that require comprehensive, purpose-built gaming floor equipment packages. Sands China Ltd. completed the renovation of its Londoner Macao integrated resort in 2023, deploying upgraded electronic table games and slot configurations across its expanded floor footprint, a project that exemplified how IR operators commission full-spectrum equipment from multiple vendors simultaneously, generating orders of magnitude greater per-facility procurement value than standalone casino refurbishments.

Regional Insights

North America Casino Gaming Equipment Market Trends and Insights

North America accounts for 38.0% of the global casino gaming equipment market in 2026, representing US$ 4.64 Billion, anchored by the world's highest concentration of licensed gaming facilities and the most mature equipment replacement infrastructure. The Bipartisan Infrastructure Law (2021) indirectly supported tribal economic development funding, reinforcing tribal casino capital expenditure budgets that drive slot and table equipment procurement at scale. Ongoing commercial casino expansions in New York, where Caesars Entertainment, MGM, and others are competing for three downstate commercial gaming licences, will generate a concentrated equipment procurement cycle expected to materialise from 2025 to 2028.

United States Casino Gaming Equipment Market Size

The United States represents an estimated 85% of the North American casino gaming equipment market, or approximately US$ 3.94 Billion in 2026, underpinned by 460-plus commercial casino properties operating across 30 states per American Gaming Association census data. Continued expansion of sports-betting-adjacent electronic gaming terminals in newly regulated states such as Virginia and Massachusetts is the primary near-term demand driver, with equipment refreshes tied to new property openings expected to sustain above-regional-average procurement volumes through 2028.

Europe Casino Gaming Equipment Market Trends and Insights

Europe is likely to account for 27% of the global casino gaming equipment market in 2026, representing US$ 3.29 Billion, with demand shaped by a dual dynamic of regulated market maturation in Western Europe and accelerating liberalisation in Central and Eastern European jurisdictions. The European Gaming and Betting Association (EGBA) has documented progressive national licensing framework updates across EU member states, with countries including Austria and the Netherlands tightening operator compliance requirements that indirectly drive demand for certified, jurisdiction-compliant equipment. Equipment suppliers with established relationships in Eastern European gaming growth corridors, including Poland and the Czech Republic, are positioned to capture above-average regional growth rates through 2030.

Germany Casino Gaming Equipment Market Size

Germany is likely to represent an estimated 18% of the European casino gaming equipment market in 2026, following the State Treaty on Gambling, which reformed the regulatory framework for gaming machines and created new licensed operator pathways. The treaty's revised AWP technical standards are mandating hardware upgrades across thousands of installed machines, generating a near-term replacement-driven procurement wave for certified German-market equipment that is expected to sustain elevated procurement volumes through at least 2027.

United Kingdom Casino Gaming Equipment Market Size

The UK represents an estimated 22% of the European casino gaming equipment market, approximately US$ 724 Million in 2026, supported by the Gambling Act Review process initiated by the UK Gambling Commission and culminating in the Gambling Act White Paper (2023), which is reshaping land-based casino operating conditions. Anticipated regulatory changes around stake limits and gaming machine density per licensed venue are creating near-term equipment reconfiguration demand, with operators proactively modernising floor assets to optimise yield within prospective new density constraints ahead of formal implementation.

France Casino Gaming Equipment Market Size

France is likely to account for an estimated 14% of the European casino gaming equipment market, in 2026, governed by the ANJ, which oversees 200-plus licensed land-based casinos that represent one of Western Europe's densest per-capita casino networks. Groupe Partouche and Groupe Barrière, the two dominant French casino operators, have both signalled ongoing floor modernisation programs targeting electronic table game expansion, providing OEMs with a visible near-term pipeline of upgrade contracts tied to visitor experience investment strategies.

Asia Pacific Casino Gaming Equipment Market Trends and Insights

Asia Pacific is poised for 24% of the global casino gaming equipment market in 2026 and is the fast-growing regional market at a projected CAGR of 4.6% driven by new integrated resort construction pipelines and post-pandemic Macao floor recovery. The Macao Gaming Inspection and Coordination Bureau (DICJ) issued new 10-year gaming concession agreements to all six licensed operators in late 2022, mandating minimum non-gaming investment thresholds that are indirectly stimulating floor technology upgrades as concessionaires compete for premium visitor spend. The Philippines' PAGCOR has approved multiple new Entertainment City and provincial casino licences, adding new procurement demand from Southeast Asia's fastest-growing gaming jurisdiction.

China Casino Gaming Equipment Market Size

Macao, China's only legally licensed casino jurisdiction, represents an estimated 42% of the Asia Pacific casino gaming equipment market, approximately US$ 1.23 Billion in 2026, recovering from a pandemic-driven trough as GGR returned to approximately 70% of 2019 peak levels by mid-2024 per DICJ monthly statistics. Wynn Macau's Encore-branded floor expansion and Galaxy Entertainment Group's Phase 4 Cotai development are both procuring next-generation electronic table game systems and premium slot configurations, supporting a concentrated multi-year procurement uplift across the territory.

India Casino Gaming Equipment Market Size

India accounts for an estimated 8% of the Asia Pacific casino gaming equipment market, approximately US$ 234 Million in 2026, concentrated within Goa, Sikkim, and offshore vessel-based gaming operations permitted under state-level legislation. The Goa, Daman and Diu Public Gambling Act amendments under consideration, alongside the Meghalaya Regulation of Casino Games Act (2021), signal a gradual widening of the licensed gaming geography, with each new state-level licensing event triggering fresh equipment procurement cycles for the small but growing pool of certified Indian gaming operators.

Japan Casino Gaming Equipment Market Size

Japan is likely to account for an estimated 6% of the Asia Pacific casino gaming equipment market, approximately US$ 176 Million in 2026, currently reflecting pachinko-adjacent and pre-IR procurement activity rather than full casino floor demand, as the country's Casino Administration Committee advances technical standards for Osaka's licensed IR. Once the Osaka IR reaches construction stage, industry estimates place the initial equipment procurement package at US$ 1.5 Billion over the project build cycle, making Japan the single largest discrete greenfield equipment opportunity in the global market through the early 2030s.

Competitive Landscape

The global casino gaming equipment market operates as a moderately concentrated oligopoly, with Aristocrat Leisure Limited, Light & Wonder Inc., and International Game Technology (IGT) collectively holding an estimated 50% of global equipment revenue based on public company disclosures and industry analyst estimates.

Competition centres primarily on game content libraries, floor systems integration capability, and multi-jurisdictional regulatory approval breadth rather than on hardware price alone. The dominant strategic theme entering 2026 is platform consolidation, OEMs are acquiring content studios and systems software businesses to build end-to-end floor ecosystems that lock in operator relationships. PlayAGS Inc. represents the most credible disruptive entrant in the mid-tier, aggressively targeting regional and tribal casino operators with competitively priced Class II and Class III certified cabinets that incumbents have historically underserved.

Key Market Developments:

- January 2025: Light & Wonder Inc. announced a multi-year systems and content supply agreement with a major Australian gaming operator, expanding its OpenGaming platform reach across Asia-Pacific regulated markets and reinforcing its cross-platform strategy outside North America.

- September 2024: Everi Holdings Inc. completed its merger with IGT's Gaming & Digital business to form a combined entity under the Everi brand, creating one of the largest diversified gaming technology companies by installed base, with combined revenues exceeding US$ 4 Billion annually and a presence in over 90 jurisdictions worldwide.

- March 2024: NOVOMATIC AG launched its NOVO LINE Interactive multi-game terminal platform at ICE London 2024, targeting European and Latin American casino operators with a modular hardware architecture designed for rapid jurisdiction-specific content updates, directly addressing the compliance-speed challenge identified as a key market restraint.

Companies Covered in Global Casino Gaming Equipment Market

- Aristocrat Leisure Limited

- International Game Technology (IGT)

- Light & Wonder Inc.

- NOVOMATIC AG

- Everi Holdings Inc.

- Konami Gaming Inc.

- Ainsworth Game Technology

- PlayAGS Inc.

- Zitro Games

- Aruze Gaming Global Inc.

- Gaming Partners International Corporation

- Interblock d.d.

- TCS John Huxley

- Euro Games Technology

- AMATIC Industries GmbH

- AGS (PlayAGS) / Elray Resources

- Incredible Technologies

- Multimedia Games

- Jackpot Digital Inc.

- Scientific Industries International

Frequently Asked Questions

The global casino gaming equipment market is valued at US$ 12.20 Billion in 2026 and is projected to reach US$ 15.21 Billion by 2033, growing at a CAGR of 3.2%, driven primarily by new casino licensing activity in Asia-Pacific jurisdictions and sustained equipment replacement cycles in North America's mature commercial and tribal gaming sectors.

Two primary drivers are fuelling market expansion: the proliferation of new integrated resort licensing frameworks, including Japan's Casino Regulation Act and Southeast Asian regulatory liberalisation, which trigger large-scale greenfield equipment procurement cycles, and the accelerating adoption of cashless and server-based gaming mandates under frameworks such as the Pennsylvania Gaming Control Board's approved cashless wagering standards, which compel operators to upgrade existing floor hardware to compatible architectures.

Slot machines hold the largest product segment share at 42.0% of the market in 2026, owing to their superior revenue-per-square-foot economics and minimal labour requirements compared to table games, attributes that make them the default capital expenditure priority for floor managers across commercial and tribal casino operations. The segment's dominance is structurally stable, though sustained by ongoing cabinet design cycles from major OEMs rather than unit volume growth alone.

North America dominates with 38.0% market share in 2026, underpinned by two structural factors: the world's largest installed base of licensed gaming positions, spanning over 460 commercial properties and 500-plus tribal facilities, and an active pipeline of new commercial casino licence awards, particularly the three pending New York State Gaming Commission downstate licences, which will generate a new equipment procurement wave concentrated between 2026 and 2029.

The most actionable opportunity lies in supplying comprehensive equipment packages to integrated resort casino developments across Asia and the Middle East, where single-project procurement values routinely exceed US$ 100 Million, an opportunity best captured by OEMs holding multi-jurisdictional type approvals across slots, electronic table games, and casino management systems. Realisation depends on the timely advancement of Japan's Casino Administration Committee technical standards and the formalisation of regulatory frameworks in prospective Gulf Cooperation Council gaming jurisdictions.

Aristocrat Leisure Limited, Light & Wonder Inc., and Everi Holdings Inc. are the market's dominant forces, collectively controlling the majority of global floor installations across slot, systems, and fintech categories. The competitive landscape is moderately concentrated but intensifying, with competition centred on content library depth, cross-jurisdictional compliance breadth, and the ability to deliver integrated hardware-software-payments ecosystems rather than standalone equipment units.