- Hardware & Software IT Services

- Data Broker Market

Data Broker Market Size, Share, and Growth Forecast 2026 - 2033

Data Broker Market by Data Category (Consumer Data, Business Data), Data Type (Structured Data, Unstructured Data), Pricing (Subscription, Pay-per-Use), End-user (BFSI, Retail and E-commerce), and Regional Analysis, 2026 - 2033

Data Broker Market Size and Trends Analysis

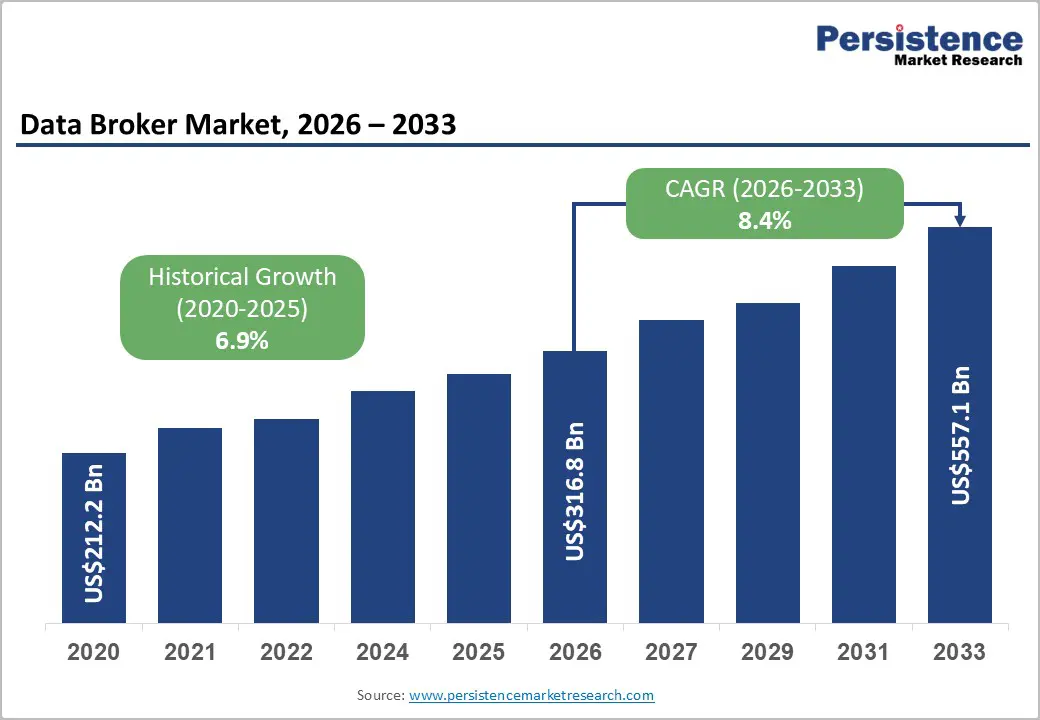

The global data broker market size is likely to be valued at US$316.8 billion in 2026 and is expected to reach US$557.1 billion by 2033, growing at a CAGR of 8.4% during the forecast period from 2026 to 2033, driven by the ongoing expansion of digital platforms that continuously generate consumer data across e-commerce, social media, and mobile applications.

Growth is further supported by the increasing adoption of AI and machine learning tools that improve data analytics, profiling, and predictive capabilities for businesses.

Key Industry Highlights:

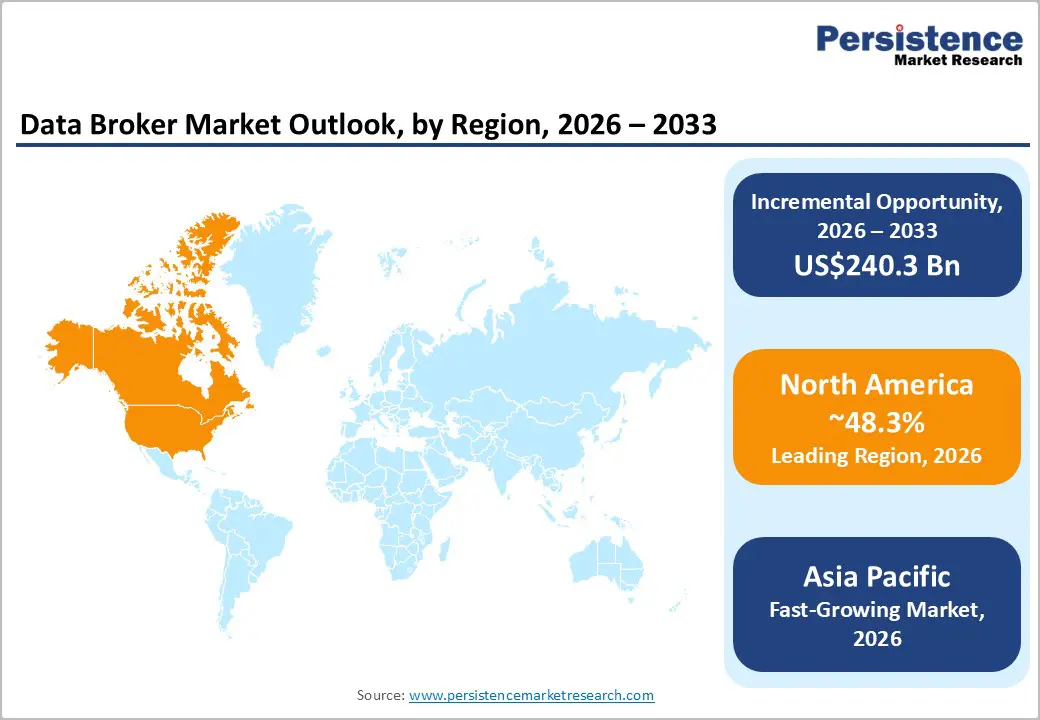

- Leading Region: North America, with about a 48.3% share in 2026, owing to the presence of leading data brokers such as Experian and Equifax.

- Fast-growing Region: Asia Pacific, backed by large-scale digital adoption and rising e-commerce activity.

- Latest Report: In February 2026, a congressional investigation in the U.S. reported that identity-theft losses associated with key data broker breaches exceeded US$20.9 billion. The findings intensified regulatory pressure on data brokers and increased industry focus on consumer data protection, opt-out mechanisms, and transparency practices.

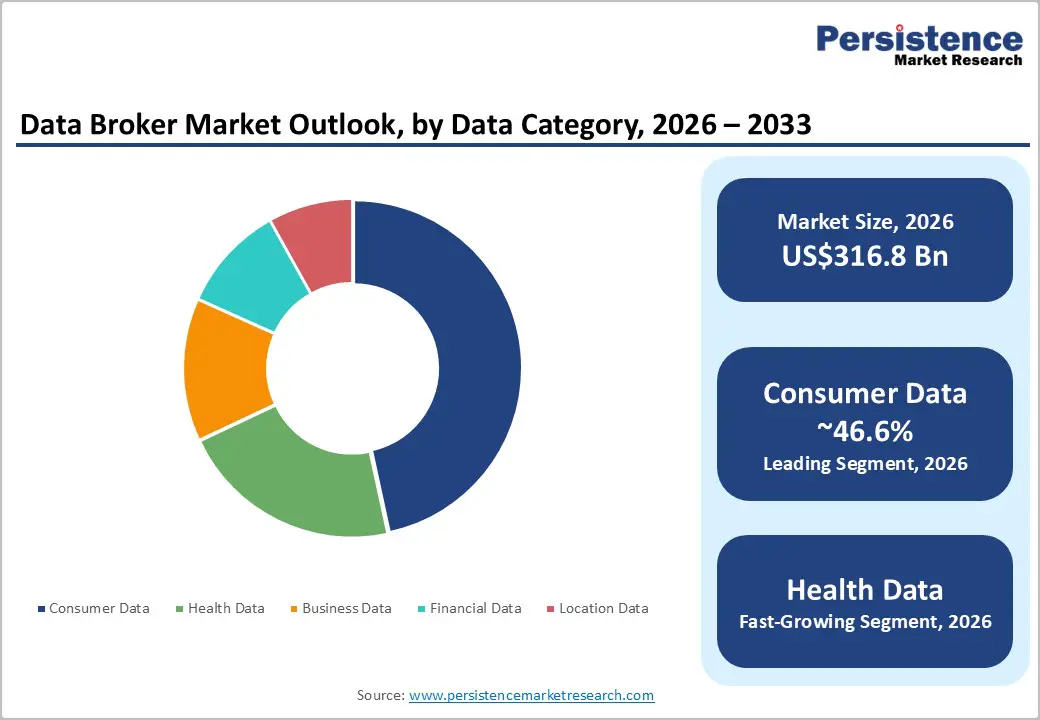

- Leading Data Category: Consumer data, approximately 46.6% share in 2026, as it supports high-value applications such as targeted advertising.

- Dominant Pricing: Subscription, nearly 44.2% in 2026, as enterprises demand continuous and real-time data access and analytics integration.

DRO Analysis

Driver - Brands Demand Consumer Data to Create Personalized Advertising

Brands today don't just want to reach audiences; they want to reach the right audience at the right moment. This has made consumer data the backbone of modern advertising. Agencies and in-house marketing teams are shifting budgets toward outcome-based buying models that reward accurate audience segmentation, prompting data brokers to improve unified-ID, probabilistic-matching, and contextual-signals pipelines.

The pressure intensified after Google began phasing out third-party browser cookies in 2024, creating a structural gap in digital advertising targeting, one that data brokers are well positioned to fill with alternative identity solutions. According to Salesforce, personalized ads now yield three times the return on investment compared to traditional ads. Meanwhile, Meta's ad revenues climbed from nearly US$134.90 billion in 2023 to US$164.50 billion in 2024, validating how deeply consumer profiling pushes advertising value.

Rise of E-Commerce to Generate Rich Data Trails

Every online transaction leaves behind a data footprint such as browsing habits, purchase history, payment behavior, and location signals. E-commerce sales in 2024 soared to US$1.19 trillion, marking an 8.1% rise from 2023, according to the U.S. Census Bureau. This surge is expanding the volume and richness of behavioral data available to brokers. Experian's third-party data marketplace, launched in January 2025, enables marketers to smoothly blend third-party and first-party data.

It helps in improving audience segmentation and campaign personalization, which is a direct response to rising e-commerce data demand. Data brokers are also benefiting from fraud prevention needs. As digital transactions broaden, retailers increasingly rely on third-party behavioral data to detect anomalies in real time. This is creating a dual-use case that sustains demand well beyond basic marketing applications.

Restraint- Surging Consumer Shift toward Privacy Tools and Ad-Blocking Technologies

More consumers are actively shielding themselves from data collection, and the numbers are difficult to ignore. Over 763 million active ad-blocking users were reported globally as of 2024, a number expected to exceed 1 billion by 2026. Ad blocking is estimated to have cost publishers around US$54 billion in lost advertising revenue worldwide in 2024. Privacy-first browsers such as Brave and DuckDuckGo are gaining mainstream traction, while more users are choosing browsers with built-in ad blocking instead of relying on extensions.

This shift disrupts data brokers as less trackable web activity means thin behavioral profiles. About 39% of internet users now use ad blockers, and 86% of people in the U.S. say data privacy is a surging concern. As consumers opt out of tracking ecosystems, the quality and completeness of third-party data assets degrade. It is reducing their commercial value and putting pressure on brokers to find alternative, consent-based data sourcing models.

Opportunity - Blockchain to Enable Individuals to Monetize Their Own Data

Web3 infrastructure is changing who controls data and who profits from it. Platforms such as Ocean Protocol have introduced a model where data providers create ERC-20 tokens called datatokens that provide access to their data, which consumers can purchase using OCEAN tokens. This removes the intermediary layer that traditional data brokers occupy. Pricing can be set dynamically using bonding curves, and providers can limit how often their data is accessed or restrict it to certain types of users or applications.

For data brokers, this is both a challenge and an opportunity. Those who integrate tokenized data pipelines can tap into a new class of verified and consent-based datasets, especially valuable as regulatory scrutiny over data sourcing intensifies. In 2024 alone, venture capital firms poured US$11.5 billion into blockchain and Web3 startups across more than 2,150 deals, signaling sustained investor confidence in decentralized data infrastructure.

Cloud-Based Data Marketplaces to Lower Barriers to Data Access

Cloud infrastructure is transforming how data is bought, sold, and integrated without requiring complex Extract, Transform, and Load (ETL) pipelines or custom integrations. Snowflake's Data Marketplace connects business leaders to over 360 data providers, delivering more than 1,700 live and ready-to-query datasets as well as applications. In December 2025, Snowflake announced it had doubled its transaction growth year-over-year on the AWS Marketplace, eclipsing US$2 billion in sales within a single calendar year.

For data brokers, these platforms reduce the friction of data distribution. A broker can list a dataset once and reach enterprise buyers across industries without custom integrations. This has paved the way for new business models such as data providers delivering datasets for sale or subscription via the Snowflake Marketplace. It is enabling organizations to enrich their internal data with third-party sources and fostering a powerful network effect. As cloud adoption rises globally, these marketplaces are becoming the default distribution channel for structured data assets.

Category-wise Analysis

Data Category Insights

Consumer data is predicted to lead with a share of approximately 46.6% in 2026, as it propels revenue-linked use cases such as advertising, credit scoring, and personalization. Consumer data is the most monetizable form of data. It connects directly to spending behavior, identity, and intent. Companies in advertising and retail rely on it to target users with high precision. For example, firms such as Experian and Equifax build detailed consumer profiles for lenders, insurers, and marketers.

According to the Federal Trade Commission, data brokers collect data from retail purchases, public records, and online activity to create comprehensive dossiers on individuals, which are then sold for marketing and risk assessment. This wide applicability across industries makes consumer data the most traded category.

Health data is estimated to be the fastest-growing segment in the forecast period, spurred by digital health adoption and regulatory-backed data sharing frameworks. Healthcare systems are constantly digitizing patient records, diagnostics, and monitoring systems. This has created a surge in structured and real-time health data. Governments are also pushing interoperability. For instance, the Centers for Medicare & Medicaid Services mandated APIs for patient data access under its interoperability rule.

India’s Ayushman Bharat Digital Mission is also building a national digital health ecosystem. Wearables and remote monitoring devices are adding another layer of continuous data generation.

Pricing Insights

The subscription segment is anticipated to dominate with a share of nearly 44.2% in 2026, as enterprises require continuous, updated, and integrated data streams. Most enterprise use cases require fresh and regularly updated data. Subscription models ensure uninterrupted access to datasets, analytics tools, and APIs. Companies such as Dun & Bradstreet and RELX provide ongoing data feeds instead of one-time datasets. This model supports use cases such as fraud detection, credit monitoring, and supply chain risk tracking, where outdated data reduces accuracy.

The pay-per-use segment is expected to remain in the second position in 2026 as it suits flexible, short-term, and cost-sensitive data requirements. Not all users need continuous access to data. Many prefer to buy specific datasets for one-time analysis. This is common in market research, due diligence, and academic studies. For example, platforms such as Oracle Data Marketplace allow users to purchase datasets based on usage. Government-backed open data initiatives also support this model indirectly. The data.gov platform provides datasets that can be accessed as required, encouraging selective consumption.

Regional Insights

North America Data Broker Market Trends

North America is predicted to lead in 2026 with a share of approximately 48.3%, due to infrastructure maturity, industry diversity, and a relatively flexible regulatory environment. The region harbors a prosperous economy with prominent international companies in technology, trade, health, and finance. These sectors generate massive data volumes and routinely rely on broker services to evaluate competitive environments, market trends, and consumer behavior.

What sets the region apart is its early investment in ad-tech. Key players such as Experian and TransUnion are headquartered in North America and continue to expand. Experian reported 8% year-on-year revenue growth in fiscal 2024, while TransUnion achieved 12% organic constant-currency expansion in Q3 2024. Even regulatory pressure has not slowed spending. Instead, it has shifted budgets toward vendors with superior compliance tools, a dynamic that favors well-resourced North America’s incumbents.

U.S. Data Broker Market Trends

The U.S. will likely account for a regional share of around 60.4% in 2026, owing to the convergence of healthcare data demand, programmatic advertising, and fintech expansion. The U.S. Centers for Medicare and Medicaid Services processed over 1.2 billion fee-for-service claims in 2024. The data exhaust from these transactions, when properly de-identified and aggregated by healthcare data brokers such as IQVIA and Veeva, is worth billions annually to payers, providers, and pharmaceutical manufacturers.

On the advertising side, TransUnion launched TruValidate in 2024, an AI-assisted platform to improve fraud prevention and identity verification. These moves show that U.S. brokers are diversifying beyond traditional consumer profiling into high-growth verticals.

Asia Pacific Data Broker Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026 with a share of nearly 25.9%, owing to its digital transformation, especially across mobile-first economies. Growth is driven by ongoing digitization in China, India, Japan, and Southeast Asia, as well as the expansion of mobile-first financial services. Also, the development of new consent-based data intermediary networks enabled by India's digital public infrastructure, including UPI and the Account Aggregator framework, is pushing the market.

The volume of data being created across the region is staggering. China alone produced 7.6 zettabytes of data in 2018 and is forecast to account for 27.8% of the global total by 2025, surpassing the U.S., stated the Center for International Governance Innovation.

China Data Broker Market Trends

China is anticipated to hold a leading share of nearly 30.2% in 2026. The country’s trajectory is influenced by a tightly regulated framework. The government is actively building structured data trading infrastructure. Through local pilot initiatives, efforts are being made to fully harness and activate the market value of data elements. It is further promoting the development of the digital economy under the coordination of the National Data Bureau. Cross-border data flows, however, remain a constraint. As of January 2024, only 25% of applications for data exports had allegedly been approved, with thousands of requests from both local and international businesses still pending.

Japan Data Broker Market Trends

In 2026, a substantial share of approximately 22.8% is predicted to be held by Japan, backed by favorable government policy and enterprise adoption of AI and IoT. The government's Society 5.0 initiative, which aims to integrate cyberspace into everyday physical society, is a key catalyst. The push toward Society 5.0 creates opportunities for both domestic and foreign firms, especially in areas such as robotics, IoT, and advanced analytics, where Japan aims to lead globally, as highlighted in the 2024 Annual Economic and Fiscal Report. Alongside this, government funding for big data projects was anticipated to reach around US$500 million in 2025, aimed at fostering innovation and collaboration between public and private sectors through data-sharing platforms.

Europe Data Broker Market Trends

Europe will likely see decent growth in the forecast period, with a share of nearly 16.2% in 2026, mainly as the General Data Protection Regulation (GDPR) has fundamentally changed what data is worth. Rather than suppressing demand, the regulation has created a quality premium. GDPR compliance has created a tiered market in which premium and consent-verified data commands significantly higher prices per record. It helps in benefiting well-capitalized brokers with superior data governance infrastructures such as RELX, Wolters Kluwer, and Thomson Reuters. Demand from regulated industries such as BFSI, healthcare, and government remains high.

U.K. Data Broker Market Trends

In 2026, the U.K. is estimated to account for a share of around 38.3%, as it is using its post-Brexit flexibility to build a data-friendly regulatory environment. The U.K. Data (Use and Access) Act 2025, which came into effect on June 19, 2025, is a cornerstone of the country’s government's post-Brexit strategy to position it as an international tech and innovation hub. It aims to ease rules on automated decision-making and enable data processing for purposes such as direct marketing with few bureaucratic hurdles.

Open banking is a standout example of U.K. data infrastructure in action. As of March 2025, about 13 million consumers and small businesses in the country were using open banking technology, and around 60 jurisdictions worldwide have adopted the U.K.'s approach.

Germany Data Broker Market Trends

Germany will likely hold a share of approximately 29.5% in 2026, as its enormous manufacturing and automotive sectors are now adopting data-based decision-making. SAP showcased AI-supported improvements to its Digital Manufacturing solution at Hannover Messe in May 2024, incorporating real-time visual inspection, predictive analytics, and AI-powered insights. Siemens also extended its Xcelerator platform through mid-2024 to early 2025, with its industrial software sales experiencing an 82% increase in the past year.

Big tech is doubling down on Germany as a data hub. Microsoft announced a US$3.7 billion investment in February 2024 to quadruple its AI and cloud infrastructure capacity in Germany.

Competitive Landscape

The global data broker market is moderately consolidated at the top but highly fragmented overall, with the presence of a few large multinational players controlling a significant share of revenues. Dominant companies such as Acxiom, Experian, Equifax, TransUnion, CoreLogic, Oracle, RELX (LexisNexis Risk Solutions), Dun & Bradstreet, and Thomson Reuters use extensive proprietary datasets, advanced analytics platforms, and long-standing enterprise relationships to maintain competitive advantages.

Competition is now centered on data quality, real-time intelligence, AI-supported enrichment, and privacy compliance rather than simply the volume of data collected. Established firms are investing heavily in machine learning, predictive analytics, identity resolution, and cloud-based delivery platforms to deliver more actionable insights to clients in advertising, financial services, healthcare, and risk management.

Key Industry Developments:

- In May 2026, Publicis Groupe announced an agreement to acquire LiveRamp. The deal followed Publicis' acquisition of Epsilon in 2019 and Lotame in March 2025. It will combine LiveRamp's clean room and data connectivity technology with the identity capabilities of Epsilon and the technology services provided by Publicis Sapient.

- In February 2026, researchers from Stanford University and affiliated organizations published a large-scale study assessing compliance among California-registered data brokers. The study found that only 9% of registered brokers fully complied with transparency requirements under the state’s privacy regulations, showcasing increasing regulatory scrutiny of the data broker market.

- In March 2026, Datavault AI entered into a definitive agreement to acquire NYIAX. The acquisition is intended to combine Datavault AI’s data monetization technologies with NYIAX’s institutional-grade marketplace infrastructure to support next-generation digital data trading ecosystems.

Companies Covered in Data Broker Market

- Acxiom LLC

- Experian PLC

- CoreLogic, Inc.

- Equifax Inc.

- Oracle America, Inc.

- Nielsen Holdings plc

- RELX PLC (LexisNexis Risk Solutions)

- LiveRamp Holdings, Inc.

- Epsilon Data Management, LLC

- Dun & Bradstreet, Inc.

- Intelius LLC

- TowerData, Inc.

- FullContact, Inc.

- Thomson Reuters Corporation

- TruthFinder LLC

- Others

Frequently Asked Questions

The global data broker market is projected to be valued at US$316.8 billion in 2026.

The data broker market is expected to reach US$557.1 billion by 2033.

Key market trends include the ongoing adoption of AI-based data enrichment and rising demand for real-time data delivery.

Consumer data is expected to be the leading data category with a share of nearly 46.6% in 2026, as it enables companies to build dynamic profiles for real-time decision-making and monetization.

The data broker market is expected to grow at a CAGR of 8.4% from 2026 to 2033.

Acxiom LLC, Experian PLC, CoreLogic, Inc., and Equifax Inc. are a few key market players.