- Hardware & Software IT Services

- Asset Finance Software Market

Asset Finance Software Market Size, Share, and Growth Forecast 2026 - 2033

Asset Finance Software Market by Component (Software, Services), by Deployment (Cloud-based, On-premises, Hybrid), Asset Type (Hard Assets, Soft Assets), Industry (BFSI, Transportation, Construction, Industrial/Manufacturing Equipment, Healthcare & Medical Equipment, IT & Telecom, Energy & Utilities, Government & Public Sector, Others), and Regional Analysis, 2026 - 2033

Asset Finance Software Market Size and Trend Analysis

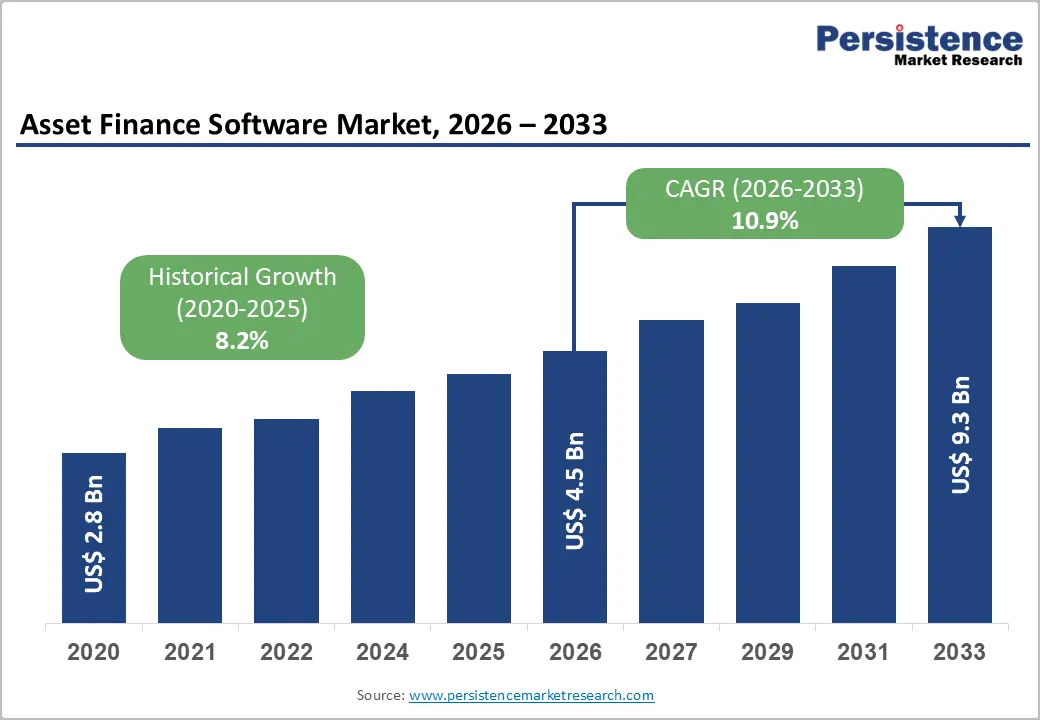

The global asset finance software market is expected to be valued at US$ 4.5 billion in 2026 and is projected to reach US$ 9.3 billion, growing at a CAGR of 10.9% between 2026 and 2033.

A widening global SME financing gap enables financial institutions to scale credit origination and servicing through automated, cloud-based asset finance platforms that enhance speed, risk assessment, and portfolio visibility. The transition toward equipment-as-a-service models across industrial sectors is increasing the need for real-time asset utilization data, enabling lenders to integrate telematics and IoT-driven insights into underwriting, pricing, and residual value estimation.

Key Industry Highlights:

- Leading Offering: Software is a dominant sector anticipated with over 74% share in 2026, driven by demand for integrated platforms covering origination, leasing, billing, and portfolio analytics.

- Fast-Growing Deployment: Cloud-based deployment is the fast-growing model, driven by scalability, lower infrastructure costs, faster upgrades, and support for cross-border operations.

- Leading Asset Type: Hard assets are poised for over 70% share in 2026, valued at ~US$ 3.15 Billion, supported by structured financing needs for vehicles, machinery, and industrial equipment requiring lifecycle tracking.

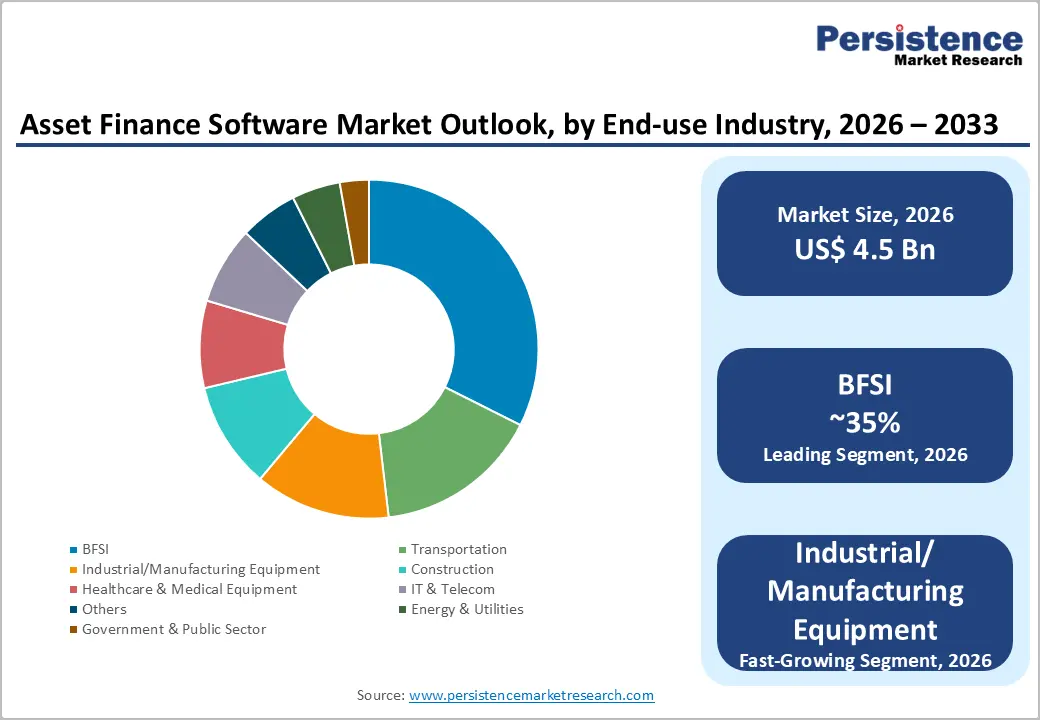

- Leading Industry: BFSI is expected to lead with over 35% share in 2026, exceeding US$ 1.57 Billion, due to its dual role as both provider and user of asset finance platforms, with strong requirements for compliance, risk analytics, and portfolio management.

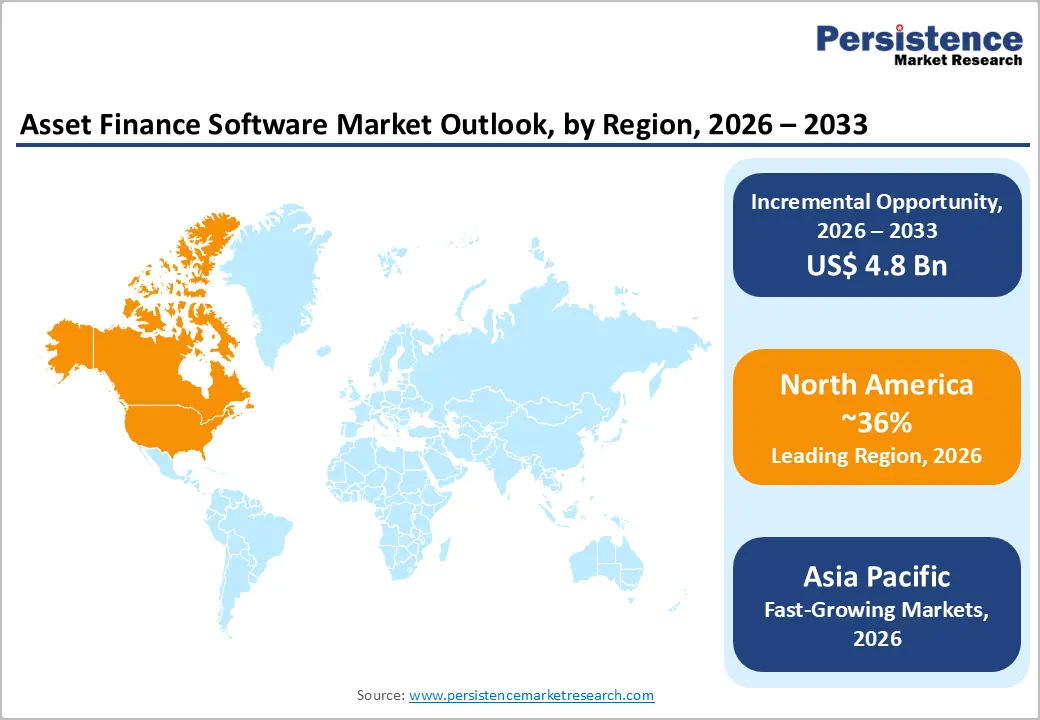

- Leading Region: North America leads the market with over 36% share in 2026, valued at ~US$ 1.62 Billion, supported by advanced digital lending infrastructure, strong independent finance company ecosystem, and rapid modernization of legacy systems.

- Fast-Growing Market: Asia Pacific is the fast-growing market with a CAGR of 16.1%, owing to the rapid leasing market formalization, infrastructure investment, and regulatory modernization across India, China, and Southeast Asia.

Market Dynamics

Drivers - IFRS 16 & ASC 842 Compliance-Driven Platform Modernization

IFRS 16 and ASC 842 lease accounting standards continue to drive sustained demand for asset finance software as enterprises move beyond initial compliance implementation into ongoing optimization and audit readiness. These regulations require organizations to recognize most lease obligations on balance sheets, significantly increasing reporting complexity and data management requirements.

Organizations still face challenges related to fragmented lease data, manual reconciliations, and inconsistent reporting across entities. Enterprises are upgrading from spreadsheet-based systems and ERP bolt-ons to dedicated lease and asset finance platforms. This is particularly evident among mid-market lessors and corporates under increasing audit scrutiny. This is driving continuous investment in scalable, compliance-focused software solutions.

Equipment Finance Digitalization Agendas at Tier-1 Banks Creating Greenfield Software Demand

Tier-1 commercial banks and financial institutions are accelerating the digital transformation of their equipment finance and leasing operations to improve efficiency and scalability. Legacy systems built on fragmented architectures are increasingly unable to support real-time processing, automated credit decisions, and integrated servicing workflows. Institutions are therefore shifting toward API-enabled, cloud-based asset finance platforms that support straight-through processing and end-to-end lifecycle management.

Rising volumes of equipment and commercial lending are further intensifying the need for automation and operational efficiency. Banks are also integrating analytics and workflow automation tools to enhance credit risk assessment and servicing accuracy.

Restraints - Data Sovereignty and Cross-Border Regulatory Fragmentation Elevating Integration Costs

Differing national data residency laws force multinational lessors to maintain separate software instances or invest in costly geo-partitioned architectures, compressing vendor margins and extending enterprise sales cycles beyond eighteen months. The European Union's General Data Protection Regulation (GDPR) combined with China's Personal Information Protection Law (PIPL), obliges vendors selling into both markets to maintain regionally isolated data environments adding an estimated 20-30% premium to implementation costs compared with single-region deployments.

New entrants with shallow implementation footprints find this compliance overhead disproportionately burdensome relative to established vendors with pre-certified regional cloud infrastructure already in place.

Legacy System Lock-in Among Mid-Tier Lessors Suppressing Replacement Cycles

A significant share of regional banks and independent finance companies continue to operate asset finance platforms that are deeply integrated with core banking and ERP systems, creating high switching costs and limiting full system replacement. These tightly coupled architectures make rip-and-replace migrations financially expensive and operationally risky, particularly for institutions managing mid-sized lease portfolios.

Migration programs often require extended parallel run phases to ensure data integrity, reconciliation accuracy, and uninterrupted servicing continuity. Many organizations pursue incremental modernization rather than full system replacement. This dynamic extends asset finance software replacement cycles while benefiting incumbent vendors and accelerating demand for modular, cloud-native alternatives.

Opportunities - Embedded Finance APIs Enabling Non-Bank Originators to Build Asset Finance Capability at Speed

Embedded finance is enabling non-bank platforms such as equipment dealers, marketplaces, and SaaS commerce providers to offer point-of-sale leasing and lending without becoming regulated lenders themselves. API-first, white-label asset finance platforms allow these originators to integrate underwriting, loan origination, and servicing capabilities directly into their customer journeys. For example, Stripe Capital and Shopify Capital demonstrate how commerce ecosystems are expanding into financing adjacent to their core transactions.

This shift is driven by demand for frictionless credit access and higher conversion rates at the point of sale. The asset finance software vendors are increasingly positioned as infrastructure providers powering embedded lending ecosystems rather than standalone lending systems.

Infrastructure Supercycle Driving Demand for Heavy Asset Portfolio Management Tools in Emerging Markets

Large-scale infrastructure investment across emerging markets is increasing the volume of financed long-life assets such as power equipment, transport infrastructure, and water systems. These projects typically involve complex financing structures including concessional funding, blended finance, and multi-currency repayment arrangements.

Development finance institutions and multilateral lenders such as the World Bank and regional development banks play a key role in channeling capital into such assets. Managing these portfolios requires specialized asset finance software capable of lifecycle tracking, structured lease accounting, and regulatory reporting across jurisdictions. The demand is increasing for platforms that go beyond generic ERP systems to support infrastructure-grade asset financing complexity.

Category-wise Analysis

Component Insights

Software commands 74% of the global asset finance software market in 2026 driven by demand for centralized control over core finance operations. Organizations prefer integrated platforms that unify origination, billing, contract lifecycle, and portfolio analytics. Strong emphasis is placed on real-time decisioning, automated pricing, and regulatory compliance across workflows. Financial institutions favor scalable and configurable systems aligned with internal governance structures. This dominance reflects a broader shift away from fragmented and outsourced operational setups.

Services are the fast-growing component, expanding as firms move from deployment to continuous optimization. Integration, configuration, data migration, and regulatory alignment form key post-implementation requirements. Increasing platform complexity is driving reliance on managed analytics and external expertise. AI-enabled credit scoring and forecasting further increase dependence on specialized support for model governance. The growth is reinforced by limited in-house capability for advanced system customization and analytics.

Deployment Insights

On-premises hold over a 30% share in 2026 since it enables strict data control and compliance adherence. Institutions rely on internal infrastructure to maintain audit transparency and meet jurisdictional regulations. Large banks and regulated leasing firms continue operating legacy systems that are difficult to migrate. Security concerns and integration with existing IT ecosystems also support continued usage. This model remains stable in highly regulated financial settings.

Cloud-based deployment is the fast-growing model, driven by demand for scalability and operational efficiency. It eliminates heavy infrastructure costs while enabling faster deployment and upgrades. Cloud environments support fluctuating transaction volumes and cross-border operations. Stronger security certifications and compliance frameworks are improving adoption confidence. Transition toward cloud is accelerating as organizations modernize legacy finance infrastructure.

Asset Type Insights

Hard assets are likely to register more than 70% of the global asset finance software market in 2026, due to financing requirements linked to physical asset lifecycles. Equipment such as vehicles, machinery, and industrial tools requires tracking of depreciation, maintenance, and residual value. Platforms enable serial-number-based monitoring and lifecycle automation. Predictable leasing structures make this category central to portfolio operations.

Soft assets are the fast-growing category, supported by rising financing of intangible assets such as software, intellectual property, and subscriptions. These assets require systems capable of handling usage-based billing and renewal tracking. The growth in digital business models is expanding exposure to non-physical asset financing. Platforms are evolving to manage entitlements and dynamic pricing mechanisms. Expansion is driven by increasing corporate investment in digital ecosystems.

Industry Insights

BFSI accounts for over 35% of market share in 2026, exceeding the value of US$ 1.57 Billion, due to its dual role as both provider and primary user of asset finance systems. Complex operations such as lending, leasing, and securitization require integrated platforms. Strong focus is placed on risk analytics, compliance reporting, and capital adequacy management. Large portfolios demand centralized and efficient processing systems. Regulatory intensity continues to reinforce this segment’s dominance.

Industrial/Manufacturing Equipment is the fast-growing end-use segment, driven by the adoption of equipment-as-a-service models. Manufacturers are linking financing structures with real-time machine performance data. Usage-based and variable payment models are becoming increasingly common. This shift requires flexible platforms capable of integrating operational and financial data. The growth is supported by Industry 4.0 adoption and smart factory expansion.

Regional Insights

North America Asset Finance Software Market Trends and Insights

North America accounts over 36.0% share of the global asset finance software market in 2026, reaching US$ 1.62 Billion, supported by a highly digitized and mature equipment finance ecosystem. The region’s dominance is driven by widespread adoption of cloud-based leasing platforms, strong penetration of independent finance companies, and continuous replacement of legacy loan origination and servicing systems with API-enabled solutions. The presence of more than 700 independent finance companies is accelerating platform modernization cycles, while integration of embedded finance capabilities across banking and non-banking lenders is further strengthening software demand.

The United States asset finance software market is expected to exceed the US$ 1.39 billion value in 2026, driven by strict regulatory compliance requirements and advanced digital lending infrastructure. The finalization of Dodd-Frank Act Section 1071 rules in 2023 has significantly increased demand for automated data capture, reporting, and analytics capabilities within lending workflows, compelling financial institutions to upgrade their software systems. The expansion of the SBA 7(a) loan guarantee programme (2023) to include digital infrastructure assets has broadened the addressable financing base, encouraging community banks and regional lenders to enter equipment finance.

Europe Asset Finance Software Market Trends and Insights

Europe accounts over 29% of the global asset finance software market in 2026, reaching US$ 1.30 Billion, driven by strong regulatory harmonization under the European Banking Authority (EBA) supervisory convergence framework. The EBA guidelines on loan origination and monitoring (EBA/GL/2020/06 updated) are accelerating demand for automated credit risk, collateral valuation, and covenant monitoring tools across European lessors. This is increasing preference for standardized, compliance-ready platforms over highly customized systems, reinforcing consolidation among leading vendors.

Germany is likely to account for over 25% share in the Europe asset finance software market in 2026 supported by its large industrial base and strong Mittelstand ecosystem of approximately 3.5 million mid-sized enterprises. These firms rely heavily on equipment leasing to finance machinery, making Germany a structurally important demand hub for asset finance platforms.

France asset finance software market value is expected to surpass US$ 210 million by 2026, driven by platform modernization initiatives such as Société Générale Equipment Finance’s transition to cloud-native systems and national investment under the France 2030 programme, which allocates €54 Billion toward industrial and digital transformation, boosting equipment finance origination volumes.

United Kingdom is more likely to register over 20% share in 2026, supported by strong leasing activity under the Finance & Leasing Association (FLA), which represents lenders advancing approximately £35 billion annually. The demand is increasingly driven by open-finance initiatives requiring API-enabled, interoperable platforms, encouraging significant software upgrades across lenders.

The Rest of Europe market is projected to surpass the value of US$ 290 million in 2026, with robust contributions from Poland, the Netherlands, and Nordic countries. The Netherlands benefits from its role as a European leasing holding hub, while Nordic countries are increasingly adopting ESG-focused asset tracking systems aligned with regional sustainable finance reporting frameworks.

Asia Pacific Asset Finance Software Market Trends and Insights

Asia Pacific accounts for more than 26% of the global asset finance software market in 2026, exceeding US$ 1.17 billion, and is the fastest-growing region with a projected CAGR of 16.1%, due to the rapid formalization of leasing ecosystems across India and Southeast Asia, alongside China’s ongoing financial technology modernization and regulatory tightening. Growing investments in digital financial infrastructure and cloud-based lending ecosystems are reinforcing long-term regional expansion.

China asset finance software market is projected to reach US$ 0.43 Billion in 2026. The country’s regulatory shift following the consolidation of CBIRC into the National Financial Regulatory Administration (NFRA) has intensified compliance requirements for more than 12,000 registered leasing companies. This has accelerated adoption of auditable, compliant portfolio management and lease accounting systems. Japan growth is supported by stable lease contract volumes exceeding ¥5 trillion annually and demand for software aligned with J-GAAP leasing conventions.

India's asset finance software market value is expected to surpass US$ 190 million, driven by regulatory tightening under the Reserve Bank of India’s updated NBFC-AFC framework requiring enhanced credit risk reporting for large portfolios. This has directly increased software adoption among 200+ regulated NBFCs. India’s National Infrastructure Pipeline, targeting US$ 1.4 trillion in infrastructure investment by 2030, is expanding demand for construction and industrial equipment leasing platforms.

Southeast Asia’s growth is supported by ASEAN financial integration initiatives and harmonization of cross-border financial infrastructure under AFMGM 2023. Indonesia’s OJK regulations mandating digital-first origination documentation for 170+ multifinance companies are accelerating software deployment ahead of enforcement deadlines.

Competitive Landscape

The global asset finance software market operates as a moderately concentrated oligopoly, where top companies collectively command an estimated 35-40% of addressable enterprise software spend, competing primarily on depth of asset class coverage, regulatory pre-certification, and integration breadth. Focusing on platform consolidation through API orchestration vendors are racing to become the system of record that aggregates data from IoT sensors, credit bureaus, and secondary market valuers into a single portfolio intelligence layer.

Key Developments:

- In May 2026, Fox Ridge Capital selected LTi Technology Solutions ASPIRE platform to support the launch of its new hybrid equipment finance business. The platform will be used to manage end-to-end leasing and loan operations, including origination, servicing, and portfolio management.

- In November 2025, FIS expanded its presence in the auto finance market by enhancing its cloud-based Asset Finance solution. The upgraded SaaS platform now supports end-to-end lifecycle management for consumer auto, wholesale, and equipment financing. This move strengthens its ability to help lenders modernize operations and improve efficiency across lending processes.

Companies Covered in Asset Finance Software Market

- Odessa Technologies

- Alfa Financial Software Holdings

- NETSOL Technologies

- Oracle Corporation

- Finastra

- FIS Global

- Fiserv

- Linedata Services

- Sopra Banking Software

- Solifi

- SS&C Technologies

- SAP SE

- IBM Corporation

- Tavant Technologies

- Codix Group

- Others

Frequently Asked Questions

The global asset finance software market is valued at US$ 4.5 billion in 2026 and is projected to reach US$ 9.3 billion by 2033, at a CAGR of 10.9%, driven by the need for scalable digital systems to manage expanding global asset leasing and financing portfolios efficiently.

The growth is driven by mandatory compliance with IFRS 16 and ASC 842, requiring digitized lease accounting systems. Rising infrastructure lending and large-scale asset creation are increasing the need for structured lifecycle asset management platforms.

Software holds the largest component share over 74.0% due to the need for a centralized, auditable system of record for lease and contract management. Organizations increasingly require purpose-built platforms to ensure compliance, accuracy, and operational control.

North America dominates with over 36.0% of the global asset finance software market in 2026, due to its mature equipment finance ecosystem and strong regulatory compliance environment. Continuous procurement cycles from banks and lessors sustain high demand for advanced software platforms.

The key opportunities lie in API-first and white-label embedded finance solutions for non-bank platforms. The demand is rising for fast-deployable financing engines that enable seamless integration of lending into commerce and equipment dealer ecosystems.

The leading companies include Alfa Financial Software Holdings, Odessa Technologies, FIS Global, Finastra, NETSOL Technologies, Solifi, and Sopra Banking Software, among others.