- Pharmaceuticals

- Pharmaceuticals Market

Pharmaceuticals Market Size, Share, and Growth Forecast 2026 - 2033

Pharmaceuticals Market by Drug Classification (Branded/Innovator Drugs, Generic Drugs, Branded Generics, Biologics & Biosimilars), Therapeutic Area (Oncology, Infectious Diseases & Vaccines, Diabetes, Cardiovascular, Anti-Rheumatic & Immunology, Others), Distribution Channel, by Regional Analysis, 2026 - 2033

Pharmaceuticals Market Size and Trend Analysis

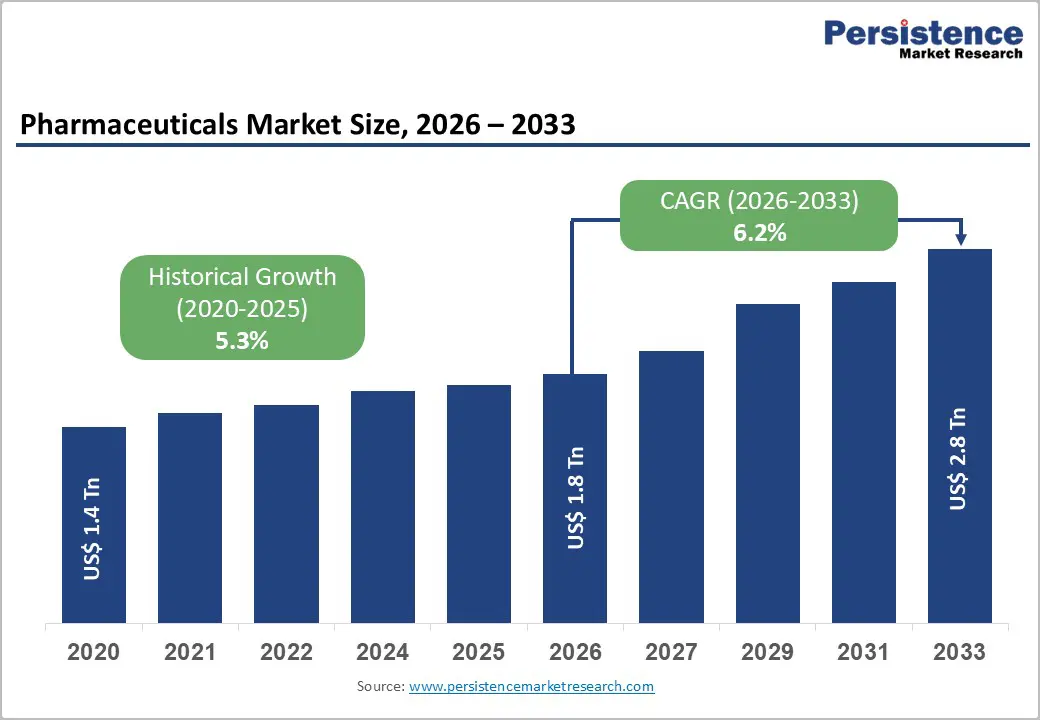

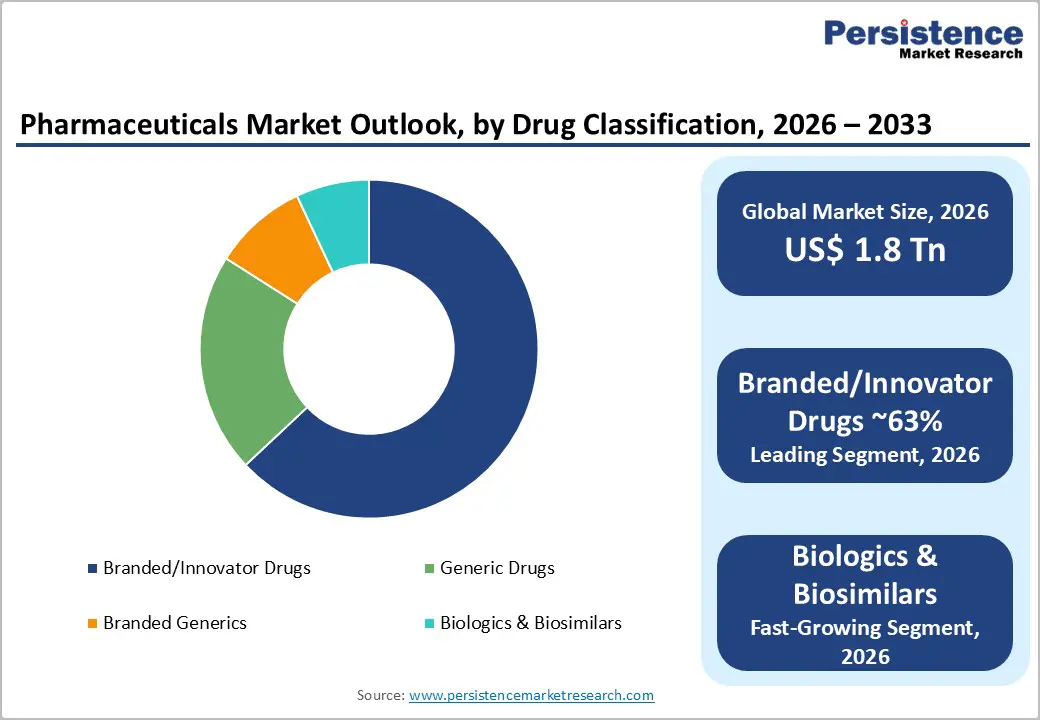

The global pharmaceuticals market size is expected to be valued at US$ 1.8 trillion in 2026 and projected to reach US$ 2.8 trillion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Pharmaceuticals are vital to the healthcare industry, focused on the research, development, manufacturing, and commercialization of medicines used to prevent, diagnose, and treat diseases. At a global scale, pharmaceuticals encompass branded drugs, generic medicines, biologics, vaccines, and specialty therapeutics across areas such as oncology, cardiovascular diseases, diabetes, infectious diseases, and neurology.

The rising prevalence of chronic diseases, aging population, increasing healthcare expenditure, and continuous innovation in drug discovery technologies, including biologics, mRNA therapies, and AI-based platforms, fuel demand for specialized pharmaceuticals. In addition, expanding access to healthcare, strong pharmaceutical R&D investments, and growing demand for personalized medicine are further supporting market expansion across both developed and emerging economies worldwide.

Key Industry Highlights

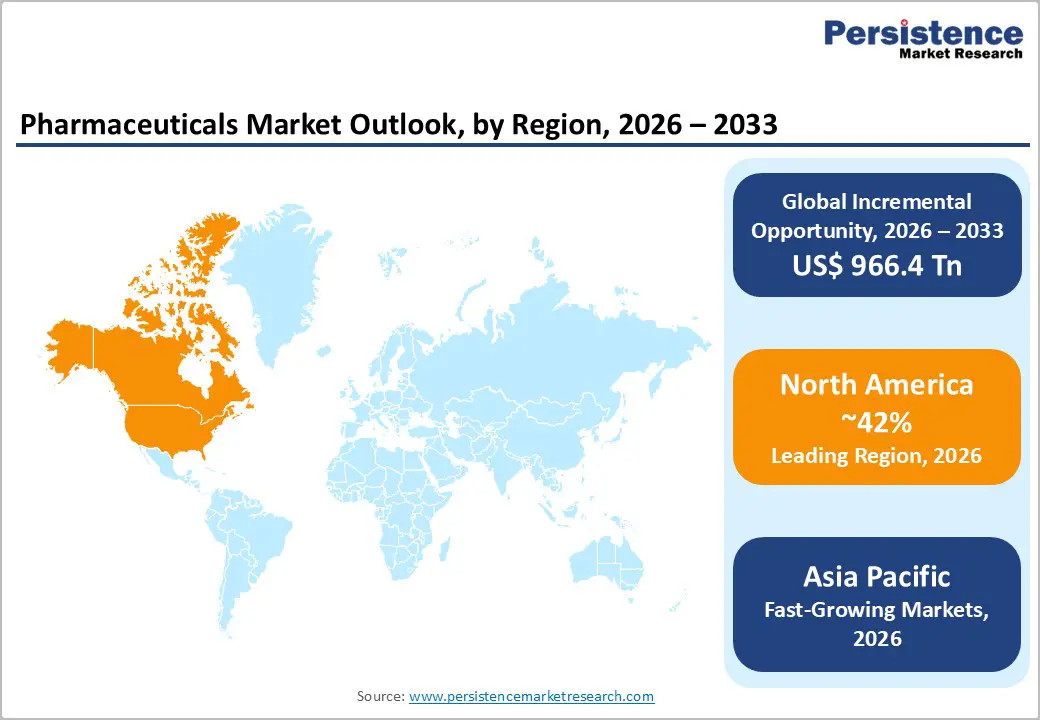

- Leading Region - North America commands ~42% of the global pharmaceuticals market in 2025, driven by high per-capita healthcare spending, robust drug approvals, and a dominant specialty biologics market centered in the U.S.

- Fastest Growing Region - Asia Pacific is set to register the highest CAGR through 2033, fueled by universal health coverage expansion, China's drug access reforms, India's generic drug manufacturing leadership, and rapid e-pharmacy growth across Southeast Asia.

- Dominant Segment - Branded/Innovator Drugs lead the market with ~63% revenue share in 2025, benefitting from strong IP protection, premium oncology and immunology pricing, and unrivaled brand trust among clinicians and healthcare systems globally.

- Fast-Growing Segment - Biologics & biosimilars are the fastest-growing drug classification, driven by accelerating patent expiries of high-value biologics, expanding EMA and FDA biosimilar approvals, and rising healthcare system demand for cost-effective biologic alternatives worldwide.

- Key Opportunity - E-commerce/online pharmacy channels across Asia Pacific and Latin America present a US$ 100+ billion incremental opportunity, enabled by digital health infrastructure development and government-backed universal health coverage programs.

Market Dynamics

Drivers - Rising Burden of Chronic and Infectious Diseases Fuelling Drug Demand

The rising burden of chronic and infectious diseases is significantly driving growth in the global pharmaceuticals market. According to the World Health Organization, non-communicable diseases (NCDs) account for nearly 74% of global deaths each year, with cardiovascular diseases, cancer, diabetes, and respiratory disorders being major contributors.

Increasing urbanization, sedentary lifestyles, unhealthy dietary habits, tobacco use, and aging populations are accelerating disease prevalence worldwide. As a result, demand for long-term medications, specialty therapeutics, biologics, and preventive treatments continues to rise across both developed and emerging economies. Pharmaceutical companies are therefore intensifying investments in drug development, clinical research, and therapeutic innovation to address expanding patient needs.

In addition, infectious diseases continue to create substantial pharmaceutical demand globally. The growing incidence of viral infections, antimicrobial resistance, and emerging public health threats has increased the need for vaccines, antivirals, antibiotics, and immune-based therapies. The International Diabetes Federation estimates that 537 million adults were living with diabetes in 2021, projected to reach 783 million by 2045. This expanding patient pool is encouraging pharmaceutical manufacturers to strengthen production capacities, diversify product pipelines, and expand global market presence.

Surge in Pharmaceutical R&D Investment and Innovation Pipeline

Unprecedented investment in pharmaceutical research and development is transforming the global healthcare landscape and serving as a major growth driver for the pharmaceuticals market. According to the Pharmaceutical Research and Manufacturers of America, U.S. biopharmaceutical companies invested more than US$ 102 billion in R&D activities in 2022. Increasing focus on innovative therapies, personalized medicine, and advanced biologics is encouraging pharmaceutical companies to strengthen their research capabilities and accelerate drug development programs. In addition, regulatory support for breakthrough therapies and orphan drugs is further stimulating innovation across the industry.

The growing adoption of mRNA technology, gene therapies, and AI-driven drug discovery platforms is significantly improving development efficiency and enabling breakthroughs in complex disease areas such as oncology, rare diseases, and neurological disorders. The U.S. Food and Drug Administration approved 55 novel drugs in 2023, highlighting strong innovation momentum globally. Continuous advancements in therapeutic technologies are expected to generate substantial commercial opportunities and expand pharmaceutical market growth through 2033.

The increasing focus on innovation is further reflected in the substantial R&D spending by leading pharmaceutical companies worldwide. The table below highlights the top 10 pharmaceutical companies by R&D expenditure in 2025, demonstrating the industry’s strong commitment to drug development and pipeline expansion.

| Company | 2025 R&D Expenditure (YoY Change) |

|---|---|

| Merck & Co., Inc. | US$ 15.79 Billion (-12%) |

| Roche Holding AG | US$ 14.73 Billion (-6%) |

| Johnson & Johnson | US$ 14.66 Billion (-14.90%) |

| AstraZeneca PLC | US$ 14.23 Billion (+5%) |

| Eli Lilly and Company | US$ 13.34 Billion (+21.40%) |

| Novartis AG | US$ 11.20 Billion (+12%) |

| Pfizer Inc. | US$ 10.44 Billion (-4%) |

| Bristol Myers Squibb | US$ 9.95 Billion (-11%) |

| AbbVie Inc. | US$ 9.10 Billion (-28.90%) |

| Sanofi | US$ 8.85 Billion (+6%) |

The pharmaceutical industry continues to witness strong R&D investment growth across major global markets, particularly in the United States, Europe, and China. Rising focus on innovative therapies, biologics, and advanced drug discovery technologies is driving sustained annual growth in pharmaceutical R&D expenditure across these regions.

Restraint - Stringent Regulatory Frameworks and Prolonged Drug Approval Timelines

Stringent regulatory frameworks and lengthy drug approval timelines remain major restraints for the global pharmaceuticals market. Pharmaceutical companies must comply with complex regulations established by agencies such as the U.S. Food and Drug Administration and the European Medicines Agency before launching new therapies. Drug development involves extensive preclinical studies, multiple phases of clinical trials, and rigorous safety and efficacy evaluations. These processes often take 10-15 years and require substantial financial investments, significantly increasing development risks and delaying commercialization timelines for innovative treatments.

Additionally, high clinical trial failure rates further challenge market growth and innovation. According to the Tufts Center for the Study of Drug Development, developing a new drug molecule can cost more than US$ 2.6 billion, while only a small proportion of drug candidates successfully reach the market. Such high costs and regulatory uncertainties particularly impact small and mid-sized pharmaceutical companies, limiting their ability to invest in advanced research, expand pipelines, and compete effectively in the global market.

Opportunities - Digital Health Integration and E-Pharmacy Emergence in Emerging Markets

The convergence of digital health platforms with pharmaceutical distribution is opening substantial new market opportunities. E-commerce and online pharmacy channels are expanding rapidly, with the Indian Pharmacy Market witnessing a surge in digital prescriptions under the National Digital Health Mission (NDHM) framework. In China, the government's "Internet + Healthcare" initiative has catalyzed the integration of e-prescriptions with licensed online pharmacies. Per IQVIA data, pharmaceutical e-commerce sales grew at a double-digit rate in Asia Pacific between 2020 and 2023.

For pharmaceutical companies and distributors, this channel expansion reduces distribution costs, improves patient adherence, and provides access to previously underserved rural populations across Southeast Asia, Latin America, and Africa, presenting a compelling incremental revenue opportunity exceeding US$ 100 billion over the forecast horizon.

Category-wise Analysis

Drug Classification Insights

Branded/innovator drugs account for a leading position in the pharmaceuticals market, commanding ~63% of the global market share in 2026. This dominance is attributed to the premium pricing power of originator products, sustained by robust intellectual property protections, strong brand equity among healthcare professionals, and demonstrated clinical superiority over generics in complex therapeutic areas. According to IQVIA, the top 20 best-selling drugs globally are predominantly branded biologics and specialty molecules, reflecting the sustained commercial strength of innovator pipelines.

Oncology and immunology branded therapies, in particular, command high average selling prices, reinforcing segment leadership. The continued investment in specialty and rare disease drug development further entrenches branded drugs as the revenue backbone of the global pharmaceutical market.

Distribution Channel Insights

Hospitals and Healthcare Facilities represent the leading distribution channel in the pharmaceuticals market, accounting for ~45% of global drug distribution in 2026. This leadership is attributable to the channel's critical role in dispensing specialty, injectable, and high-value biologic therapies that require clinical supervision. The WHO Global Health Expenditure Database confirms that hospital-based pharmaceutical spending constitutes the largest component of total medicine expenditure in both high- and middle-income countries.

The increasing shift toward specialty medications, particularly intravenous oncology regimens, biologics, and hospital-administered vaccines, further reinforces the primacy of this distribution channel. Government procurement and institutional tenders also operate substantially through hospital networks, adding volume-driven revenue stability.

Regional Insights

North America Pharmaceuticals Market Trends and Insights

North America leads the global pharmaceuticals market with a 42% share in 2026, underpinned by world-class healthcare infrastructure, the highest per-capita pharmaceutical spending, and a favourable regulatory environment for drug approvals. The region continues to drive innovation through substantial private and public R&D investment, with the U.S. National Institutes of Health (NIH) allocating over US$ 47 billion in research funding in 2023. The rapid uptake of specialty therapies and biologics, alongside growing GLP-1 receptor agonist demand, sustains the region's dominance.

U.S. Pharmaceuticals Market Size

The U.S. accounts for the lion's share of North American pharmaceutical revenues, representing ~80% of the regional market. The U.S. pharmaceutical market was valued at ~US$ 600 billion in 2026. The Inflation Reduction Act's drug pricing negotiation provisions, robust biosimilar launches, and strong specialty drug pipeline are the defining forces shaping the market's near-term outlook.

Europe Pharmaceuticals Market Trends and Insights

Europe holds the second-largest share in the global pharmaceuticals market, accounting for ~22% of global revenues in 2026. The region benefits from universal healthcare coverage in most member states, systematic generic drug adoption through national health systems, and a proactive regulatory stance by the EMA toward biosimilar approvals. However, pricing controls and parallel trade across EU member states exert downward pressure on average selling prices.

Germany Pharmaceuticals Market Size

Germany is the largest pharmaceutical market in Europe, contributing ~20% of European revenues in 2026. Strong statutory health insurance coverage, high healthcare expenditure per capita exceeding €5,000 per person, and a well-established domestic pharmaceutical manufacturing base anchored by companies such as Bayer AG consolidate Germany's regional leadership. The AMNOG benefit assessment framework continues to shape drug pricing dynamics.

UK Pharmaceuticals Market Size

The UK accounts for ~10% of the European pharmaceuticals market in 2026. Post-Brexit regulatory autonomy under the Medicines and Healthcare products Regulatory Agency (MHRA) has enabled the UK to pioneer faster approvals for novel therapies, including gene therapies and mRNA-based treatments. The NHS remains the dominant drug purchaser, leveraging volume-based procurement to manage costs.

France Pharmaceuticals Market Size

France represents ~9% of European pharmaceutical revenues in 2026. The country's Transparency Commission (Haute Autorité de Santé) governs drug reimbursement decisions, influencing market access. France is a top-five global destination for pharmaceutical clinical trials and hosts major manufacturing facilities of Sanofi, further reinforcing its strategic importance within the European pharmaceutical value chain.

Asia Pacific Pharmaceuticals Market Trends and Insights

Asia Pacific is the fast-growing market for global pharmaceuticals, propelled by demographic expansion, rising middle-class healthcare spending, and government-led universal health coverage initiatives. China remains the dominant country in the region, with a pharmaceutical market approaching US$ 180 billion in 2025, driven by the national drug access reforms, volume-based procurement policy, and a booming domestic innovative drug sector. Regional governments are increasingly investing in local pharmaceutical manufacturing to reduce import dependency.

India Pharmaceuticals Market Size

India is a significant region for Asia Pacific pharmaceutical market, likely to be valued at ~US$ 55 billion in 2026 and growing at a strong pace. India is the world's largest supplier of generic medicines by volume, supplying over 50% of global generic drug demand. Government initiatives such as Pradhan Mantri Bhartiya Janaushadhi Pariyojana (PMBJP) and Production Linked Incentive (PLI) schemes are fostering domestic pharmaceutical manufacturing competitiveness.

Japan Pharmaceuticals Market Size

Japan is the third-largest pharmaceutical market globally, valued at ~US$ 85 billion in 2025. The country's universal health insurance system, ageing population with over 29% aged above 65 (Statistics Bureau of Japan) and government-led drug pricing revisions under the National Health Insurance (NHI) price list define market dynamics. Japan's PMDA-approved innovative therapies, particularly in oncology, represent a high-value revenue segment.

Competitive Landscape

The global pharmaceuticals market is moderately consolidated, with the top 15 companies collectively accounting for over 50% of global revenues. Market leaders such as Pfizer, Johnson & Johnson, and Roche rely on diversified portfolios spanning branded drugs, biologics, and vaccines. Key competitive strategies include strategic M&A to bolster pipelines (e.g., AstraZeneca's oncology acquisitions), biosimilar launches to defend market share post-patent cliff, and AI-driven drug discovery platforms. Emerging business models, including outcome-based pricing and direct-to-patient digital channels, are gaining traction, reshaping competitive differentiation across therapeutic areas.

Key Developments

- In May 2026, Roche Pharma India announced the launch of Tecentriq SC in India, marking the country’s first subcutaneous immunotherapy for lung cancer. The treatment can be administered in around 7 minutes, significantly reducing administration time compared to traditional IV infusions that may take several hours.

- In May 2026, Eli Lilly and Company announced the launch of Lormalzi (350 mg/20 mL IV vial) in India after receiving marketing approval from the Central Drugs Standard Control Organization for the treatment of Alzheimer’s disease in patients with mild cognitive impairment or mild dementia stage.

- In October 2025, Aspen Pharmacare gained South African approval to market Eli Lilly’s Mounjaro (tirzepatide) for chronic weight management, expanding from its Type 2 diabetes use and competing with Wegovy in the growing obesity market via a convenient KwikPen injector.

- In October 2025, India’s Natco Pharma acquired a significant stake in South Africa’s Adcock Ingram, strengthening its Southern African presence and regional market access, while maintaining Adcock’s operations and product lineup, focusing on growth in the generics segment.

- In August 2025, Sub-Saharan Africa advanced health self-reliance as the Global Fund procured locally manufactured first-line HIV treatment (TLD) for Mozambique, following the WHO prequalification of Kenya’s Universal Corporation, strengthening supply chains and improving outcomes for people living with HIV.

- In November 2024: AstraZeneca PLC announced a US$ 1.5 billion investment to expand its biologics manufacturing capacity in Singapore, strengthening supply chain resilience and catering to growing Asia Pacific demand for biologic therapies.

Companies Covered in Pharmaceuticals Market

- Pfizer Inc.

- Johnson & Johnson

- Roche Holding AG

- Novartis AG

- Merck & Co., Inc. (MSD)

- Sanofi

- AstraZeneca PLC

- GlaxoSmithKline (GSK)

- AbbVie Inc.

- Bristol Myers Squibb

- Eli Lilly and Company

- Bayer AG

- Takeda Pharmaceutical Company Limited

- Amgen Inc.

- Others

Frequently Asked Questions

The global market is projected to be valued at US$ 1.8 trillion in 2026.

Growth is driven by rising chronic and infectious diseases, increasing pharmaceutical R&D spending, biologics expansion, mRNA innovation, and AI-based drug discovery advancements globally.

North America leads the pharmaceuticals market due to high healthcare spending, strong FDA approvals, advanced innovation capabilities, and widespread adoption of specialty therapies.

Major opportunities include biosimilar expansion after biologic patent expiries and rapid e-pharmacy growth across emerging economies supported by healthcare digitization initiatives.

Leading pharmaceutical companies include Pfizer Inc., Johnson & Johnson, Roche Holding AG, Novartis AG, Merck & Co., Inc., and Sanofi.