- Inks, Coatings, Adhesives & Sealants (ICAS)

- Metal Coatings Market

Metal Coatings Market Size, Share and Growth Forecast, 2026 - 2033

Metal Coatings Market by Metal Type (Aluminum, Steel, Stainless Steel), Process (Coil Coating, Extrusion Coating, Hot-Dip Galvanizing), Technology (Liquid Coating, Powder Coating), and Regional Analysis 2026 - 2033

Metal Coatings Market Share and Trends Analysis

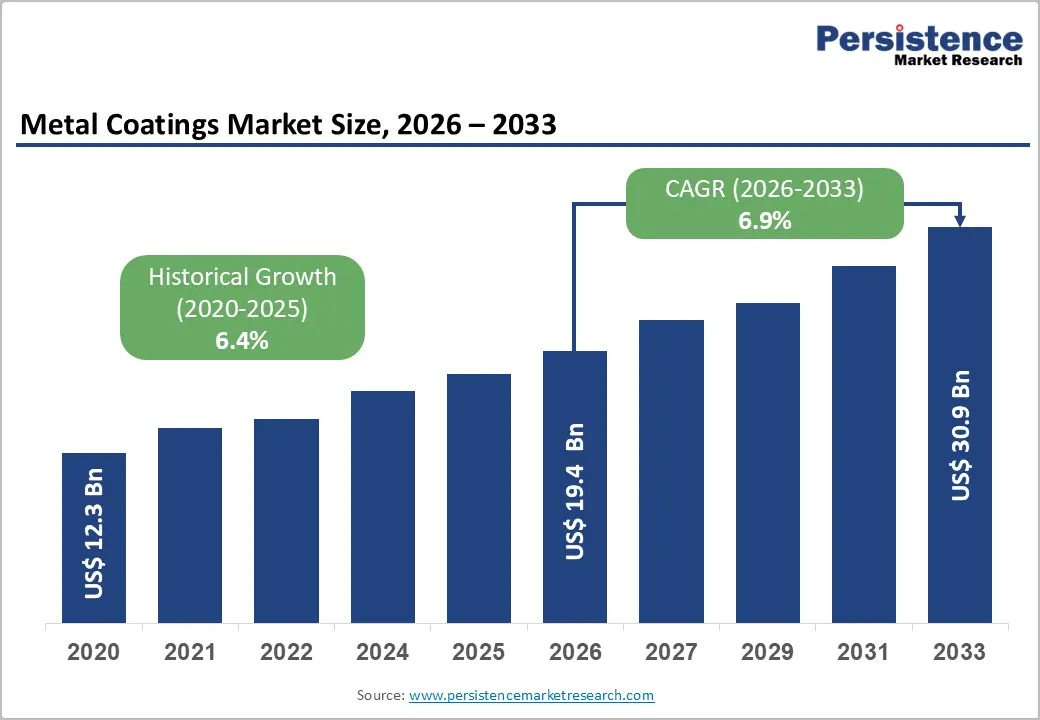

The global metal coatings market is likely to be valued at US$19.4 billion in 2026 and is anticipated to reach US$30.9 billion by 2033, growing at a CAGR of 6.9% during the forecast period from 2026 to 2033, driven by infrastructure expansion, rising automotive lightweighting, and strong manufacturing activity in Asia Pacific. Increasing environmental regulations are accelerating the shift toward sustainable, solvent-free powder coatings, while demand for high-performance formulations continues to support durability and extended asset life across industries.

Key Industry Highlights:

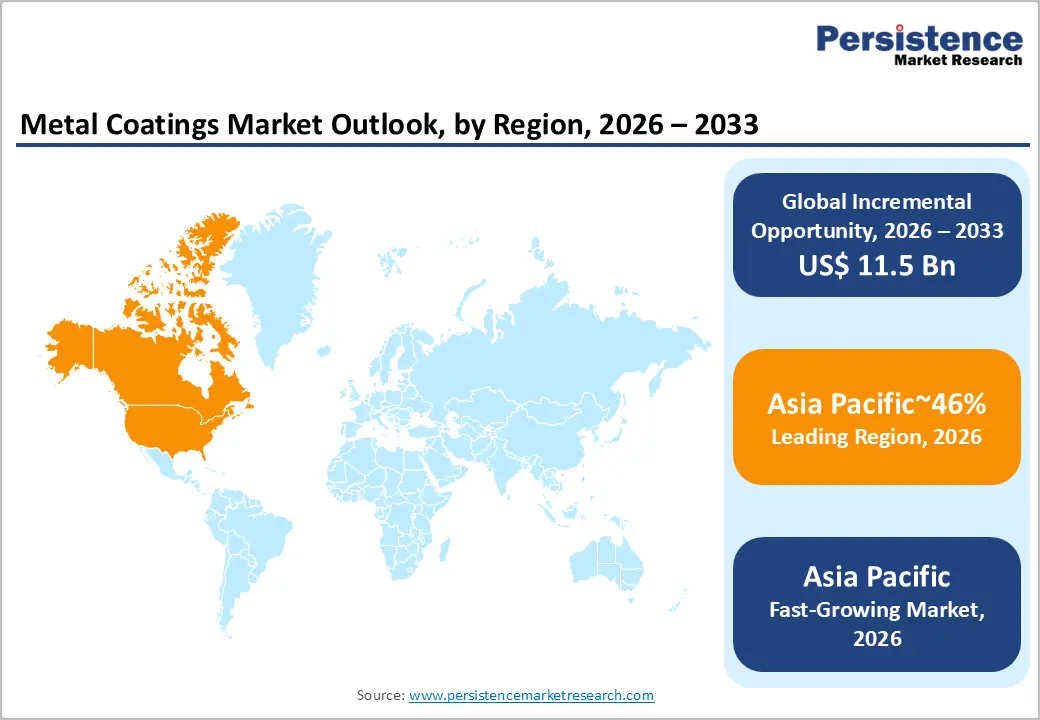

- Leading Region: Asia Pacific is expected to lead the market, accounting for around 46% share in 2026, driven by rapid urbanization, large-scale infrastructure development, expanding industrial manufacturing, and growing automotive production requiring advanced performance standards.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, due to massive urbanization, aggressive infrastructure modernization, surging industrial manufacturing, and expanding automotive assembly networks.

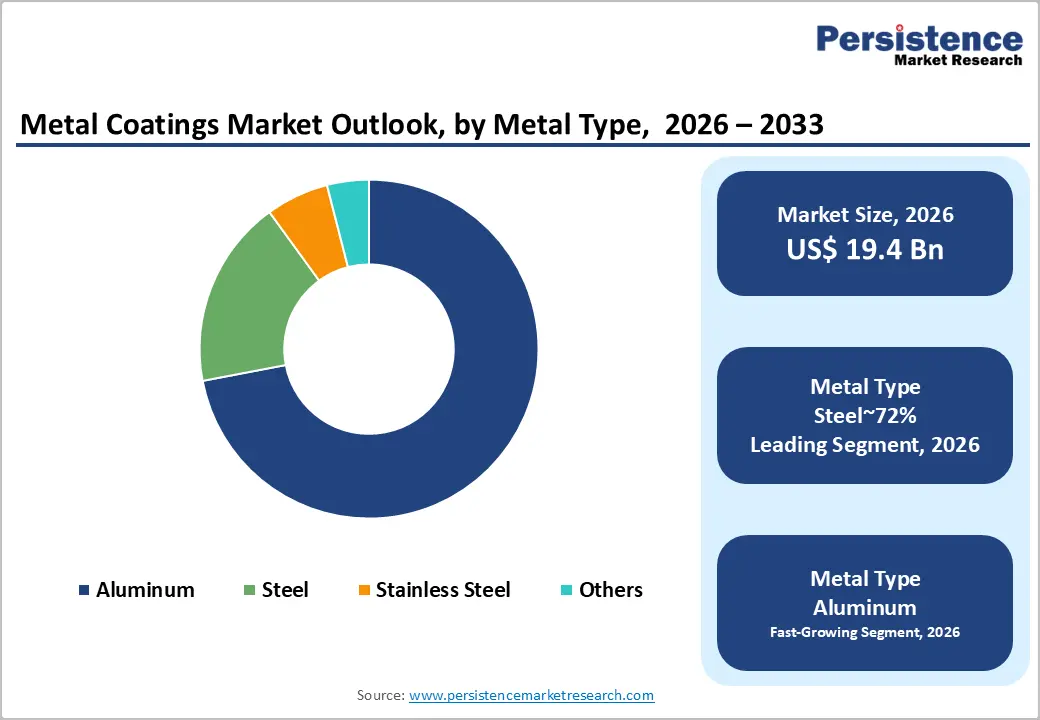

- Leading Metal Type: Steel is expected to dominate the market with around 72% share in 2026, driven by infrastructure expansion, strong demand for corrosion-resistant coatings, high consumption in heavy machinery manufacturing, and a consistent focus on durability in procurement decisions.

- Leading Process: Coil coating is projected to dominate the market due to its continuous efficiency, with automated high-speed processing lines that maximize throughput and minimize material waste, accounting for approximately 45% of the market share in 2026.

- Leading Technology: Liquid coating is projected to dominate due to established infrastructure, traditional application equipment dominating existing regional industrial fabrication networks, and reliable formulations maintaining dominance 53% share in 2026.

- Competitive Environment: Major manufacturers prioritize targeted strategic acquisitions, securing specialized geographic production capacities. Recent investments focus strictly on advancing sustainable zero-emission formulations. Accelerated technological partnerships optimize regional supply chain efficiency networks.

DRO Analysis

Driver - Rising Infrastructure Investments Driving Demand for Durable Protective Coatings

Large-scale infrastructure modernization projects generate massive procurement requirements for durable structural steel treatments. Infrastructure spending across emerging markets accelerated by 14%. This measurable expansion directly forces construction consortiums to secure resilient exterior architectural finishes. Intense environmental exposure conditions mandate robust barrier technologies preventing accelerated asset corrosion processes. Consequently, supply pipelines prioritize advanced coating architectures, ensuring long-term structural integrity under stress.

Industrial buyers increasingly favor proven coating systems that deliver superior edge coverage during component assembly. Major manufacturers are responding with specialized formulations designed to withstand severe degradation in demanding environments. As a result, adoption is rising for advanced solutions such as ENVIROCRON Extreme Protection Edge Plus from PPG Industries. This high-performance capability helps prevent early failure in heavy equipment and structural applications, supporting consistent demand and strengthening revenue growth across the broader commercial coatings supply chain.

Stringent Environmental Regulations Accelerating Adoption of Low-VOC and Sustainable Coatings

Strict government legislation restricting volatile organic compounds compels facility operators toward sustainable formulations. Environmental compliance mandates have increased coating application expenses notably. This regulatory pressure effectively eliminates legacy solvent-based systems from confined industrial painting operations. Contractors quickly adopt alternative chemical platforms delivering functional equivalence without exceeding emission thresholds. Consequently, market dynamics shift permanently toward safer architectural and structural asset protection technologies.

Commercial applicators seek resilient flooring systems resisting chemical spills without violating air quality parameters. High-traffic industrial environments necessitate rapid return-to-service characteristics, minimizing expensive facility operational downtime periods. Facilities increasingly deploy Sherwin-Williams with Accelera One, addressing these critical parameters. These fast-curing alternatives maintain structural aesthetics while ensuring compliance during heavy usage. Sustained regulatory enforcement ensures continuous procurement momentum for these advanced low-emission protective barriers.

Restraint - Raw Material Cost Volatility

Unpredictable pricing fluctuations affecting essential pigment supplies compress profit margins for mid-tier manufacturers. Titanium dioxide spot prices climbed 12%. This acute input inflation disrupts established operational budgets across independent regional fabrication networks. Formulators struggle to match fixed-price supply contracts against rapidly escalating foundational chemical component costs. Consequently, financial instability restricts capital reinvestment into modernized application equipment or capacity expansion.

Elevated expenses force commercial applicators to evaluate alternative substrate treatments offering equivalent durability. Some procurement departments delay scheduled recoating maintenance programs, mitigating immediate capital expenditure burdens. Axalta Coating Systems’ AquaEC 3500 mitigates partial material losses. Despite such optimization strategies, overall market expansion faces structural resistance from these financial barriers. Sustained margin pressure remains a formidable obstacle, inhibiting rapid industry-wide technological adoption curves.

Supply Chain Bottlenecks

Chronic upstream chemical shortages severely constrain production scheduling across numerous secondary formulation facilities. Propylene oxide shortages increased formulation expenses by 18%. This supply deficit prevents manufacturers from maintaining adequate safety stock for sudden orders. Unreliable delivery timelines jeopardize massive industrial construction projects requiring coordinated material arrival sequences. Therefore, unpredictable availability suppresses total volume output despite robust baseline end-user demand levels.

Interrupted resin deliveries force application contractors to substitute inferior alternatives, risking premature failure. Strategic inventory management becomes exceptionally difficult when primary chemical building blocks remain scarce. Procurement shifts favor Covestro with Desmophen CQ NH, establishing reliable sourcing. Regardless, persistent logistical bottlenecks deter large-scale industrial commitments requiring guaranteed continuous volume delivery. These structural friction points fundamentally throttle accelerated expansion targets within heavy manufacturing sectors.

Opportunity - Sensor-Integrated Technologies

Emerging predictive maintenance paradigms generate substantial demand for advanced functional surfaces monitoring strain. Sensor-integrated surface technologies registered a 22% adoption increase. These intelligent films detect microscopic structural fissures before catastrophic mechanical failure events occur. Asset managers deploy these systems, lowering lifetime inspection costs across remote offshore infrastructure. Thus, functionalization elevates basic commodity protection into high-margin preventative diagnostic engineering data solutions.

Infrastructure operators urgently need continuous condition data to secure critical load-bearing structural connection points. Advanced diagnostic capabilities integrate seamlessly without compromising underlying primary anti-corrosive chemical barrier properties. Engineers implement Nippon Paint with Protec HB 2024, fulfilling these parameters. This continuous feedback loop revolutionizes traditional manual visual inspection procedures across dangerous environments. Capitalizing upon real-time data streaming creates massive commercial upside for specialized chemical developers.

Offshore Wind Expansion

Massive investments expanding renewable energy generation networks require specialized marine-grade structural steel protection. According to Bloomberg (January 2025), offshore wind additions reached 12 GW globally. These extreme aquatic environments demand unparalleled resistance against continuous saltwater immersion and ultraviolet degradation. Failing to secure proper barrier systems compromises multi-billion-dollar capital-intensive generation assets rapidly. Therefore, aggressive renewable infrastructure deployment guarantees enormous specialized volume requirements spanning multiple decades.

Turbine monopile foundations necessitate exceptionally thick film applications, preventing catastrophic submerged biological fouling. Energy consortiums strictly qualify application protocols, guaranteeing zero maintenance intervals exceeding twenty years. Operators implement Jotun with SteelMaster 1200HFE protecting critical structural tower segments. This uncompromising durability validates extreme-environment formulations, justifying considerable upfront application expenditure investments. Serving this expanding alternative energy vertical constitutes a magnificent, sustained revenue generation engine.

Category-wise Analysis

Metal Type Insights

Steel is expected to lead, capturing approximately 72% share in 2026, supported by infrastructure growth. Structural frameworks absolutely require heavy-duty barriers preventing catastrophic oxidative degradation during service lifetimes. Heavy industrial machinery manufacturing sustains immense volume consumption across widespread fabrication networks. Procurement departments consistently specify Hempel's Hempaprime C5, ensuring durability. These fundamental requirements anchor steady financial returns across diversified construction supply chains.

Aluminum is anticipated to be the fastest-growing segment, driven by rapid automotive lightweighting initiatives. Modern electric vehicle assembly absolutely requires specialized substrates, minimizing total structural chassis weight. Thinner metallic panels demand exceptional scratch resistance, guaranteeing continuous exterior aesthetic protection. Engineers implement Kansai Paint with Retan PG Eco, optimizing performance. Accelerating transportation sector evolution permanently alters fundamental material specification protocols across manufacturing.

Process Insights

Coil coating is projected to lead the metal coatings market, accounting for approximately 45% share in 2026, anchored by continuous efficiency. Automated high-speed processing lines maximize throughput velocity, minimizing localized chemical material waste. This exceptional operational efficiency satisfies massive architectural panel manufacturing requirements flawlessly. Industrial facilities utilize Beckers Group's BeckryMix, maintaining consistent production standards. These streamlined methodologies guarantee robust profit margins across continuous heavy industrial operations.

Hot-dip galvanizing is forecast to be the fastest-growing segment, driven by heavy infrastructure demands. Submerged application techniques provide impenetrable internal metallurgical bonding, preventing aggressive subsurface rust. Civil engineering consortiums mandate these comprehensive treatments, securing critical load-bearing structural joints. Construction operators deploy Henkel with Bonderite M-NT to improve bond strength. Expanding regional urbanization ensures a persistent requirement for pipelines supporting intense industrial fabrication networks.

Technology Insights

Liquid coating is set to lead, accounting for approximately 53% share in 2026, underpinned by established infrastructure. Traditional application equipment infrastructure thoroughly dominates existing regional industrial fabrication facility networks. Operators hesitate to abandon proven solvent platforms despite increasingly rigorous environmental compliance restrictions. Consequently, reliable formulations, including Arkema's Kynar 500, maintain dominance. Familiar handling characteristics ensure steady, continuous consumption volumes across diverse manufacturing verticals.

Powder coating is poised to be the fastest-growing segment, driven by strict ecological regulations. Zero-emission solid particulate systems completely eliminate hazardous atmospheric volatile organic compound releases. Advanced electrostatic deposition techniques guarantee uniform thickness profiles, maximizing protective barrier integrity. Facilities integrate Evonik with Protectosil Antirust, achieving these objectives. Sustainability targets continuously force sweeping technological transitions, reshaping industrial surface treatment methodologies.

Regional Analysis

Asia Pacific Metal Coatings Market Trends

Asia Pacific is expected to lead the market, accounting for approximately 46% of the market share in 2026, supported by massive urbanization, and is anticipated to be the fastest-growing region. Aggressive infrastructure modernization creates immense baseline requirements, prioritizing resilient exterior structural defense. Surging industrial manufacturing continuously expands aggregate material consumption across heavy equipment sectors. Expanding automotive assembly networks dictate rigorous functional specifications ensuring optimal component longevity.

China anchors this massive regional expansion through aggressive state-sponsored civil engineering initiatives. Extensive residential tower construction demands uninterrupted supplies, maintaining accelerated building completion timelines. Contractors frequently select Nippon Paint's Protec HB, protecting structural beams. Intense capital allocation ensures formidable market momentum, defining future long-term consumption trajectories.

Europe Metal Coatings Market Trends

Europe is projected to remain a structurally stable market, with demand anchored in strict environmental compliance upgrades. Stringent regulatory frameworks actively force transition toward highly sustainable, low-emission formulation architectures. Established automotive manufacturing hubs prioritize advanced application technologies, minimizing total energy expenditure. Substantial offshore renewable energy deployments require exceptionally durable marine-grade barrier defense mechanisms.

Germany dictates technological advancement, prioritizing zero-waste continuous industrial fabrication assembly protocols. Advanced automotive engineering absolutely requires lightweight substrate treatments, preventing premature oxidation. Assembly plants integrate Jotun with SteelMaster 1200HFE (Reuters, March 2025), fulfilling rigorous specifications. This relentless pursuit of optimizing application efficiency secures continuous high-margin specialized product procurement.

North America Metal Coatings Market Trends

North America is projected to remain a structurally stable market, with demand anchored in replacement cycles. Aging commercial infrastructure urgently requires comprehensive restoration to prevent critical mechanical failure events. Rigorous regional environmental mandates accelerate adoption curves, favoring sustainable solid particulate technologies. Advanced aerospace manufacturing necessitates uncompromising precision, maintaining critical flight hardware surface integrity.

The U.S. accelerates growth by deploying massive federal funding to upgrade domestic bridges. Stringent public procurement standards strictly govern chemical barrier selections across infrastructure projects. Agencies consistently approve PPG Industries's ENVIROCRON Extreme Protection Edge Plus (Reuters, October 2025). Such massive institutional investment guarantees robust long-term financial stability across regional supply chains.

Competitive Landscape

The global metal coatings market reflects a moderately fragmented structure, where global leaders exert influence through advanced formulation technologies and extensive industrial distribution networks. Companies such as AkzoNobel, Sherwin-Williams, and Axalta Coating Systems shape procurement standards by delivering high-performance coating systems for automotive, construction, and industrial applications. Their scale and R&D capabilities enable consistent innovation in durability, corrosion resistance, and curing efficiency. Technology footprints anchored in integrated platforms ensure long-term contracts with OEMs and infrastructure developers.

Competitive positioning emphasizes sustainability-driven differentiation and performance optimization across coating chemistries. Covestro with Desmophen CQ NH highlights innovation in low-emission polyurethane systems, challenging solvent-based alternatives. Premium vendors focus on low-VOC, waterborne, and powder coatings aligned with regulatory compliance, while value-oriented players prioritize cost-efficient bulk solutions. Strategic activity includes selective acquisitions to expand localized production and bridge formulation gaps. Platform evolution centers on energy-efficient curing and digital application monitoring.

Key Developments

- In April 2026, PPG Industries launched end-to-end protective coating solutions specifically for data center infrastructure. This creates a new high-growth revenue stream by providing fire, thermal, and corrosion protection for the rapidly expanding AI-driven infrastructure market.

- In April 2026, Axalta Coating Systems earned three Edison Awards for innovations in Electric Vehicle (EV) safety and AI-powered color technology. Validates Axalta’s competitive lead in specialized "Mobility Coatings" that handle the thermal management and safety requirements of EV battery packs.

Companies Covered in Metal Coatings Market

- PPG Industries

- AkzoNobel

- Sherwin-Williams

- Axalta Coating Systems

- BASF

- Nippon Paint

- Kansai Paint

- RPM International

- Jotun Group

- Hempel A/S

- Beckers Group

- Arkema

- Evonik Industries

- Allnex

- Wacker Chemie

- DuPont

Frequently Asked Questions

The global metal coatings market is projected to be valued at US$19.4 billion in 2026 and is expected to reach US$30.9 billion by 2033.

Unpredictable pricing fluctuations, such as a 12% climb in titanium dioxide spot prices, compress profit margins and disrupt established operational budgets across independent fabrication networks.

The global metal coatings market is forecast to grow at a CAGR of 6.9% from 2026 to 2033.

Asia Pacific leads with approximately 46% share in 2026, driven by massive urbanization and aggressive infrastructure modernization.

Key players include PPG Industries, AkzoNobel, Sherwin-Williams, Axalta Coating Systems, BASF, Nippon Paint, Jotun Group, and Hempel A/S.