- Executive Summary

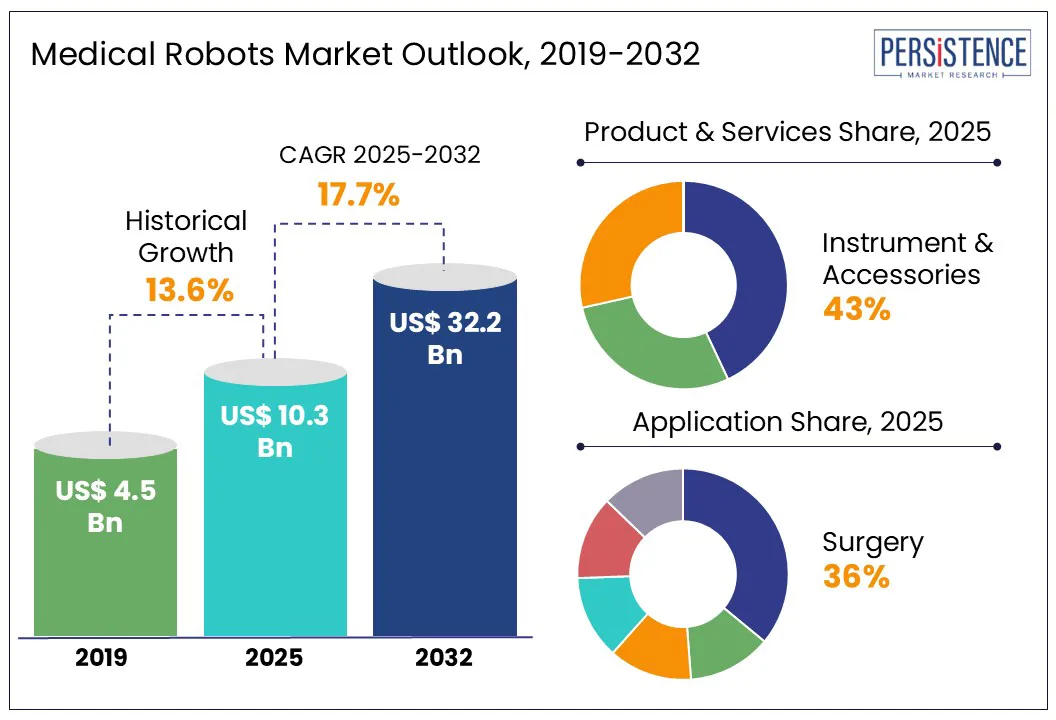

- Global Medical Robots Market Snapshot, 2025 and 2032

- Market Opportunity Assessment, 2025 - 2032, US$ Mn

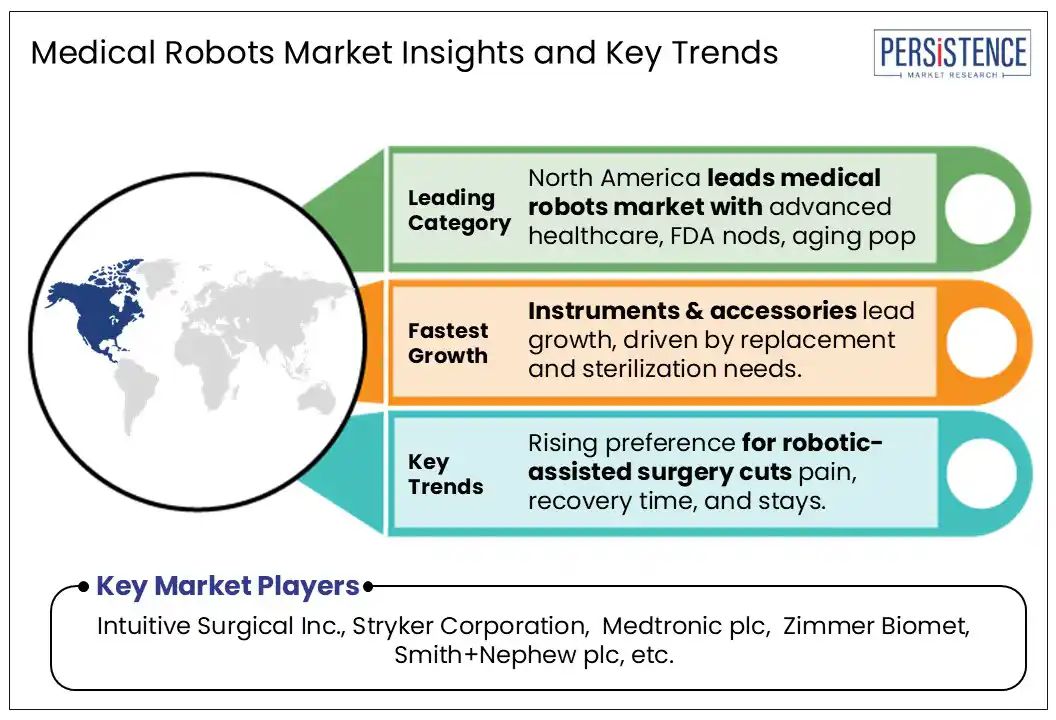

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Key Trends

- Macro-Economic Factors

- Global Sectorial Outlook

- Global GDP Growth Outlook

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Product & Services Adoption Analysis

- Regulatory Landscape

- Reimbursement Scenario

- Key Deals and Mergers

- PESTLE Analysis

- Porter’s Five Force Analysis

- Global Medical Robots Market Outlook:

- Key Highlights

- Market Size (US$ Mn) and Y-o-Y Growth

- Absolute $ Opportunity

- Market Size (US$ Mn) Analysis and Forecast

- Historical Market Size (US$ Mn) Analysis, 2019-2024

- Market Size (US$ Mn) Analysis and Forecast, 2025-2032

- Global Medical Robots Market Outlook: Product & Services

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Product & Services, 2019-2024

- Market Size (US$ Mn) Analysis and Forecast, By Product & Services, 2025-2032

- Instrument & Accessories

- Robotic Systems

- Services

- Market Attractiveness Analysis: Product & Services

- Global Medical Robots Market Outlook: Application

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By Application, 2019-2024

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025-2032

- Surgery

- General Surgery

- Gynecological Surgery

- Urological Surgery

- Orthopedic Surgery

- Neurosurgery

- Rehabilitation

- Diagnostics

- Radiation Therapy

- Hospital Automation

- Others

- Surgery

- Market Attractiveness Analysis: Application

- Global Medical Robots Market Outlook: End User

- Introduction / Key Findings

- Historical Market Size (US$ Mn) Analysis, By End User, 2019-2024

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025-2032

- Hospitals & Clinics

- Research Institutions and Universities

- Ambulatory Surgical Centers

- Diagnostic Imaging Centers

- Rehabilitation Centers

- Others

- Market Attractiveness Analysis: End User

- Key Highlights

- Global Medical Robots Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Region, 2019-2024

- Market Size (US$ Mn) Analysis and Forecast, By Region, 2025-2032

- North America

- Europe

- East Asia

- South Asia and Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Medical Robots Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019-2024

- By Country

- By Product & Services

- By Application

- By End User

- Market Size (US$ Mn) Analysis and Forecast By Country, 2025-2032

- U.S.

- Canada

- Market Size (US$ Mn) Analysis and Forecast, By Product & Services, 2025-2032

- Instrument & Accessories

- Robotic Systems

- Services

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025-2032

- Surgery

- General Surgery

- Gynecological Surgery

- Urological Surgery

- Orthopedic Surgery

- Neurosurgery

- Rehabilitation

- Diagnostics

- Radiation Therapy

- Hospital Automation

- Others

- Surgery

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025-2032

- Hospitals & Clinics

- Research Institutions and Universities

- Ambulatory Surgical Centers

- Diagnostic Imaging Centers

- Rehabilitation Centers

- Others

- Market Attractiveness Analysis

- Europe Medical Robots Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019-2024

- By Country

- By Product & Services

- By Application

- By End User

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025-2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Türkiye

- Rest of Europe

- Market Size (US$ Mn) Analysis and Forecast, By Product & Services, 2025-2032

- Instrument & Accessories

- Robotic Systems

- Services

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025-2032

- Surgery

- General Surgery

- Gynecological Surgery

- Urological Surgery

- Orthopedic Surgery

- Neurosurgery

- Rehabilitation

- Diagnostics

- Radiation Therapy

- Hospital Automation

- Others

- Surgery

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025-2032

- Hospitals & Clinics

- Research Institutions and Universities

- Ambulatory Surgical Centers

- Diagnostic Imaging Centers

- Rehabilitation Centers

- Others

- Market Attractiveness Analysis

- East Asia Medical Robots Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019-2024

- By Country

- By Product & Services

- By Application

- By End User

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025-2032

- China

- Japan

- South Korea

- Market Size (US$ Mn) Analysis and Forecast, By Product & Services, 2025-2032

- Instrument & Accessories

- Robotic Systems

- Services

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025-2032

- Surgery

- General Surgery

- Gynecological Surgery

- Urological Surgery

- Orthopedic Surgery

- Neurosurgery

- Rehabilitation

- Diagnostics

- Radiation Therapy

- Hospital Automation

- Others

- Surgery

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025-2032

- Hospitals & Clinics

- Research Institutions and Universities

- Ambulatory Surgical Centers

- Diagnostic Imaging Centers

- Rehabilitation Centers

- Others

- Market Attractiveness Analysis

- South Asia & Oceania Medical Robots Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019-2024

- By Country

- By Product & Services

- By Application

- By End User

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025-2032

- India

- Southeast Asia

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Mn) Analysis and Forecast, By Product & Services, 2025-2032

- Instrument & Accessories

- Robotic Systems

- Services

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025-2032

- Surgery

- General Surgery

- Gynecological Surgery

- Urological Surgery

- Orthopedic Surgery

- Neurosurgery

- Rehabilitation

- Diagnostics

- Radiation Therapy

- Hospital Automation

- Others

- Surgery

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025-2032

- Hospitals & Clinics

- Research Institutions and Universities

- Ambulatory Surgical Centers

- Diagnostic Imaging Centers

- Rehabilitation Centers

- Others

- Market Attractiveness Analysis

- Latin America Medical Robots Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019-2024

- By Country

- By Product & Services

- By Application

- By End User

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025-2032

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Mn) Analysis and Forecast, By Product & Services, 2025-2032

- Instrument & Accessories

- Robotic Systems

- Services

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025-2032

- Surgery

- General Surgery

- Gynecological Surgery

- Urological Surgery

- Orthopedic Surgery

- Neurosurgery

- Rehabilitation

- Diagnostics

- Radiation Therapy

- Hospital Automation

- Others

- Surgery

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025-2032

- Hospitals & Clinics

- Research Institutions and Universities

- Ambulatory Surgical Centers

- Diagnostic Imaging Centers

- Rehabilitation Centers

- Others

- Market Attractiveness Analysis

- Middle East & Africa Medical Robots Market Outlook

- Key Highlights

- Historical Market Size (US$ Mn) Analysis, By Market, 2019-2024

- By Country

- By Product & Services

- By Application

- By End User

- Market Size (US$ Mn) Analysis and Forecast, By Country, 2025-2032

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Mn) Analysis and Forecast, By Product & Services, 2025-2032

- Instrument & Accessories

- Robotic Systems

- Services

- Market Size (US$ Mn) Analysis and Forecast, By Application, 2025-2032

- Surgery

- General Surgery

- Gynecological Surgery

- Urological Surgery

- Orthopedic Surgery

- Neurosurgery

- Rehabilitation

- Diagnostics

- Radiation Therapy

- Hospital Automation

- Others

- Surgery

- Market Size (US$ Mn) Analysis and Forecast, By End User, 2025-2032

- Hospitals & Clinics

- Research Institutions and Universities

- Ambulatory Surgical Centers

- Diagnostic Imaging Centers

- Rehabilitation Centers

- Others

- Market Attractiveness Analysis

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Intuitive Surgical Inc.

- Overview

- Segments and Product & Services

- Key Financials

- Market Developments

- Market Strategy

- Stryker Corporation

- Medtronic plc

- Zimmer Biomet

- Smith+Nephew plc

- Johnson & Johnson (through Ethicon and Auris Health)

- Siemens Healthineers AG

- Asensus Surgical, Inc.

- Renishaw plc

- Cyberdyne Inc.

- ReWalk Robotics Ltd.

- Ekso Bionics Holdings Inc.

- Brainlab AG

- Intuitive Surgical Inc.

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

Loading page data

Please wait a moment