- Medical Devices

- Medical Implants Market

Medical Implants Market Size, Share, and Growth Forecast 2026 - 2033

Medical Implants Market by Product Type (Orthopedic Implants, Cardiovascular Implants, Spinal Implants, Dental Implants, Ophthalmic Implants, Neurological Implants, Others), Material Type (Metallic Implants, Polymer Implants, Ceramic Implants), End-user (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, Dental Clinics, Others), Regional Analysis, 2026 - 2033

Medical Implants Market Share and Trends Analysis

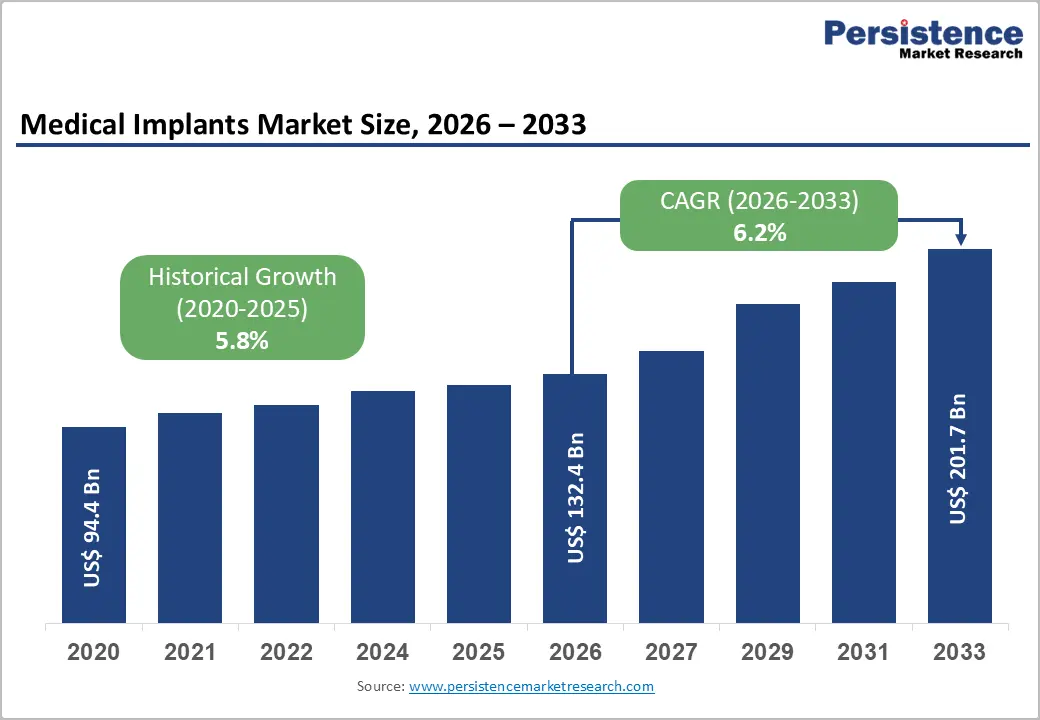

The global medical implants market size is expected to be valued at US$ 132.4 billion in 2026 and projected to reach US$ 201.7 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. This robust expansion is primarily fueled by the accelerating global burden of chronic musculoskeletal disorders, cardiovascular diseases, and age-related degenerative conditions that demand long-term implantable solutions.

According to the World Health Organization (WHO), musculoskeletal conditions affect more than 1.71 billion people worldwide, generating sustained demand for orthopedic and spinal implants. Simultaneously, rapid advances in biomaterial science, miniaturization, and digital health integration are broadening the clinical applicability of implants, enabling surgeons to address previously inoperable conditions and expanding the addressable patient pool across both developed and emerging healthcare markets.

Key Industry Highlights:

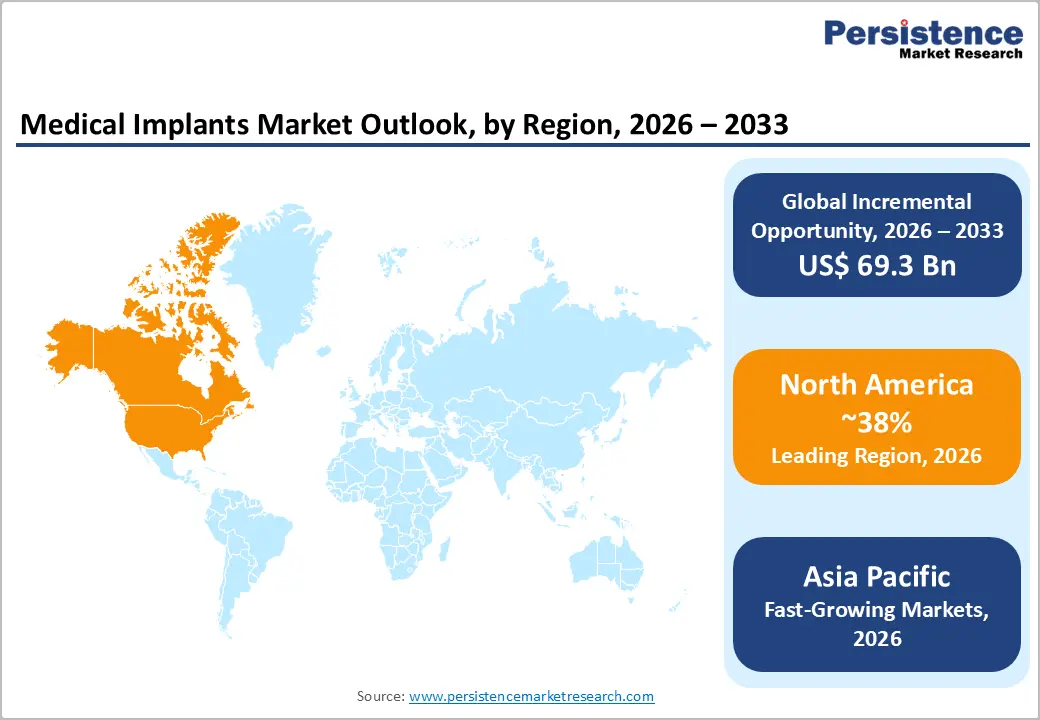

- Leading Region: North America dominates the global medical implants market with approximately 38% market share in 2025, underpinned by advanced healthcare infrastructure, strong Medicare/Medicaid reimbursement, and headquarters of the world's largest implant manufacturers.

- Fast-Growing Market: Asia Pacific is the fastest-growing regional market, driven by China's Healthy China 2030 policy, India's PM-JAY health coverage expansion, and rapidly rising healthcare expenditure across Southeast Asian economies.

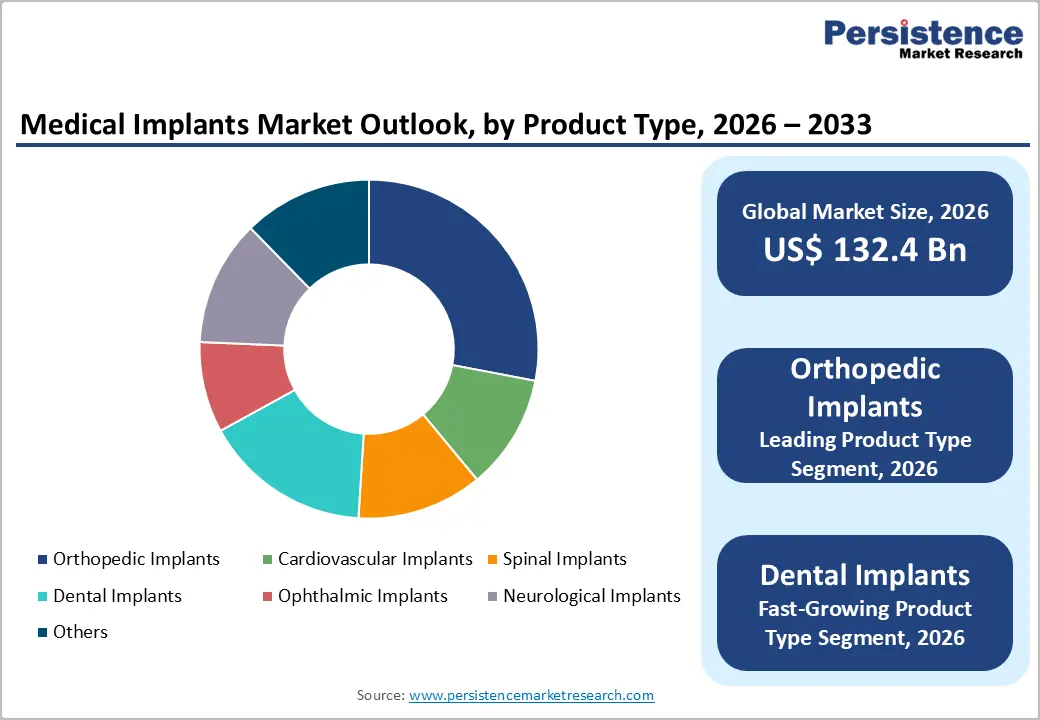

- Dominant Product Segment: Orthopedic implants lead by product type with ~28% market share in 2025, propelled by the global burden of musculoskeletal disease affecting over 1.71 billion people and growing adoption of robotic-assisted joint replacement surgery.

- Fast-Growing Product Segment: Dental implants are the fast-growing products driven by the rising edentulism rates among aging populations, expanding dental insurance coverage in emerging markets, and adoption of digital implant planning workflows.

Market Dynamics

Drivers - Rising Prevalence of Chronic Diseases and an Aging Global Population

The surging incidence of chronic conditions, particularly osteoarthritis, cardiovascular disease, and diabetes-related complications, is a foremost catalyst for medical implant adoption. The United Nations projects that by 2050 the global population aged 60 years or older will reach 2.1 billion, nearly double the 2019 figure of 1.0 billion. Older patients disproportionately require joint replacement, cardiac pacemakers, and intraocular lenses.

The Global Burden of Disease (GBD) Study estimates that ischemic heart disease and stroke together account for over 15 million deaths annually, underpinning persistent demand for cardiovascular implants. Demographic aging is therefore creating a structural, long-term tailwind that will sustain market momentum well beyond the current forecast period.

Technological Innovation in Implant Design and Smart Biomaterials

Continuous innovation in implant manufacturing, encompassing additive manufacturing (3D printing), surface nanotechnology, and bioactive coatings, is dramatically improving osseointegration, implant longevity, and patient outcomes. The adoption of titanium alloy and PEEK (polyether ether ketone) materials has enhanced biocompatibility and reduced rejection rates. Furthermore, the emergence of smart implants embedded with biosensors for real-time physiological monitoring aligns with broader digital health trends.

The U.S. Food and Drug Administration (FDA) approved over 6,000 medical devices in fiscal year 2023 alone, reflecting an accelerating regulatory pipeline that supports the commercialization of next-generation implant technologies. These advances are expanding surgical indications and reducing revision surgery rates, delivering compelling clinical and economic value.

Restraints - High Cost of Implant Procedures and Reimbursement Challenges

The elevated cost of medical implants and associated surgical procedures remains a significant access barrier, particularly in low- and middle-income countries. A primary total knee replacement in the United States can cost between US$ 30,000 and US$ 50,000, with implant components representing a substantial share. Inconsistent reimbursement policies across national healthcare systems create additional uncertainty for manufacturers and patients alike. In many Asia Pacific and Latin American markets, out-of-pocket expenditure remains high, limiting market penetration among lower-income demographics and constraining volume growth in high-potential emerging economies.

Stringent Regulatory Requirements and Extended Approval Timelines

The medical implant industry operates under some of the most rigorous regulatory frameworks globally. In the European Union, the transition to the Medical Device Regulation (EU MDR 2017/745) has substantially lengthened device certification timelines, with some manufacturers reporting delays of 12–24 months compared to predecessor directives.

Similarly, the FDA's 510(k) and PMA pathways require extensive clinical evidence, increasing development costs and time-to-market. These regulatory burdens disproportionately affect smaller innovators and can slow the introduction of clinically superior devices, temporarily constraining market expansion.

Opportunities - Rapid Expansion of Dental Implant Adoption in Emerging Markets

Dental implants represent one of the fastest-growing product segments and a compelling opportunity, particularly in emerging economies where rising disposable incomes and expanding dental insurance coverage are driving adoption.

According to the International Osteoporosis Foundation, edentulism (complete tooth loss) affects approximately 10% of the global population aged 60–74, representing a vast addressable market. Countries such as India, Brazil, and China are witnessing double-digit growth in dental tourism and domestic implant procedures, driven by government oral health initiatives and the proliferation of affordable dental clinic chains. Manufacturers investing in cost-effective implant systems and digital workflow solutions, including intraoral scanning and computer-aided implant planning, are well-positioned to capitalize on this structural opportunity through the forecast period.

Integration of Active and Smart Implants with Digital Health Ecosystems

The convergence of implantable medical devices with the Internet of Medical Things (IoMT) presents a transformative opportunity for market players. Smart implants equipped with wireless telemetry, strain sensors, and drug-eluting capabilities are enabling continuous post-operative monitoring and personalized therapeutic interventions. The U.S. National Institutes of Health (NIH) has significantly increased funding for neuromodulation and bioelectronic medicine research, with the BRAIN Initiative allocating over US$ 500 million in recent years to advance implantable neurotechnology. Companies that develop platforms integrating implant data with electronic health records and AI-driven diagnostics are poised to command premium pricing and create durable competitive advantages, particularly in the neurological and cardiovascular implant sub-segments.

Category-wise Analysis

Product Type Insights

Orthopedic implants dominate the medical implants market, commanding approximately 28% of total market share in 2025. This dominance is attributable to the globally high and growing burden of musculoskeletal disorders, including osteoarthritis, osteoporosis-related fractures, and sports injuries. According to the Bone & Joint Initiative USA, over 7 million hip and knee replacement procedures are performed globally each year.

The widespread availability of hip, knee, and shoulder replacement systems from established manufacturers, combined with increasing procedural volumes in ambulatory surgical centers, reinforces orthopedic implants' market leadership. The adoption of robotic-assisted surgery platforms—exemplified by Stryker's Mako system further amplifies procedure accuracy and patient outcomes, sustaining strong clinician and patient preference for this segment.

Material Type Insights

Metallic implants hold the leading position within the material type category, accounting for approximately 60% of the market in 2025. Metals such as titanium, cobalt-chromium alloys, and stainless steel remain the materials of choice for high-load-bearing applications, including joint replacements, spinal fixation hardware, and dental implants, due to their exceptional mechanical strength, fatigue resistance, and proven biocompatibility.

The ASTM International and ISO standards governing metallic implant manufacturing are well established, providing manufacturers with a clear regulatory pathway. Advances in additive manufacturing now enable the production of patient-specific metallic implants with optimized porosity for enhanced osseointegration, further consolidating the segment's dominant position while simultaneously opening new value-added product tiers.

End-user Insights

Hospitals represent the leading end-user segment, accounting for approximately 55% of total market revenue in 2025. Tertiary care and academic medical centers are the primary sites for complex implant procedures, including total joint replacements, cardiac device implantations, and spinal surgeries—given their access to advanced imaging infrastructure, specialized surgical teams, and comprehensive post-operative care facilities. According to the American Hospital Association (AHA), there are over 6,100 registered hospitals in the United States alone, with high-volume implant centers concentrated in major metropolitan areas. Favorable reimbursement rates for hospital-based procedures and established procurement relationships with leading device manufacturers further reinforce hospitals' dominant share within this category.

Regional Insights

North America Medical Implants Market Trends and Insights

North America leads the global medical implants market, accounting for approximately 38% of total revenue in 2025. The region benefits from a highly developed healthcare infrastructure, favorable reimbursement policies under Medicare and Medicaid, and the presence of the world's foremost implant manufacturers. Increasing adoption of robotic-assisted surgical systems and strong R&D investment underpin continued regional dominance.

U.S. Medical Implants Market Size

The United States accounts for over 85% of the North American market, driven by high procedural volumes, an aging population exceeding 55 million people aged 65+, and robust private health insurance coverage. The FDA's active device approval pipeline and a concentration of leading medical device companies further reinforce U.S. market leadership.

Europe Medical Implants Market Trends and Insights

Europe holds the second-largest share of the global medical implants market, supported by universal healthcare systems across major economies, strong public hospital networks, and proactive adoption of minimally invasive surgical techniques. The implementation of EU MDR 2017/745 is reshaping the competitive landscape by raising the clinical evidence bar, potentially consolidating market share among well-resourced incumbents and driving innovation in post-market surveillance.

Germany Medical Implants Market Size

Germany is the largest medical implants market in Europe, representing approximately 22% of regional revenue. Its Statutory Health Insurance (SHI) system ensures broad patient access to implant procedures, while Germany's advanced engineering ecosystem supports a vibrant domestic manufacturing base. High per-capita orthopedic and dental implant procedure rates further distinguish the German market.

U.K. Medical Implants Market Size

The United Kingdom accounts for roughly 14% of the European market revenue. The National Health Service (NHS) drives consistent procedural volume for orthopedic and cardiovascular implants. Growing investment in NHS surgical capacity post-pandemic and expanding private pay channels for dental and elective orthopedic procedures are key near-term growth drivers.

France Medical Implants Market Size

France represents approximately 13% of the European medical implants market. Strong public hospital reimbursement for orthopedic and cardiovascular procedures, combined with France's active participation in EU-funded medical device research programs, supports sustained market growth. A growing geriatric population with over 21% of citizens aged 65 or above underpins long-term demand.

Asia Pacific Medical Implants Market Trends and Insights

Asia Pacific is the fastest-growing regional market, propelled by rapidly expanding healthcare expenditure, a massive and aging population base, and government initiatives to upgrade hospital infrastructure. China represents the dominant national market in the region, benefiting from its "Healthy China 2030" Plan which targets expanded coverage of essential medical devices and procedures. Rising medical tourism in Southeast Asia and increasing domestic manufacturing capabilities are additional growth catalysts.

India Medical Implants Market Size

India is emerging as a high-growth market, supported by the Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PM-JAY) scheme, which provides health coverage to over 500 million beneficiaries. India holds approximately 8% of the Asia Pacific implants market, with orthopedic and dental implant adoption accelerating rapidly amid an expanding middle class and increasing private hospital investment.

Competitive Landscape

The medical implants market is highly competitive and innovation-driven, supported by strong investments in research, product development, and regulatory approvals. Companies compete through advanced implant materials, minimally invasive technologies, 3D-printed implants, and smart implant solutions to improve patient outcomes and surgical precision. Strategic partnerships, acquisitions, and geographic expansion remain key growth strategies to strengthen market presence.

Key Developments

- In March 2025, Dentsply Sirona launched an affordable dental implant solution, MIS LYNX, in the U.S. MIS Implants Technologies designed this solution that offers an excellent value proposition for both patients and clinicians.

- In December 2024, MedCAD developed reconstruction plates for the midface and mandible by using 3D printing. The company focuses on offering more features and geometries to address different surgical complexities with this innovation.

- In September 2024, GC Aesthetics launched its YOUTHLY brand in China. It features the company’s latest breast implant innovations, including Luna XT, PERLE, and the Round Collection. The company aims to provide premium silicone breast implants to plastic surgeons and women in China, in collaboration with G&S Group.

Global Medical Implants Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 94.4 billion |

|

Current Market Value (2026) |

US$ 132.4 billion |

|

Projected Market Value (2033) |

US$ 201.7 billion |

|

CAGR (2026–2033) |

6.2% |

|

Leading Region |

North America, 38% market share (2025) |

|

Dominant Category (Product Type) |

Orthopedic Implants, ~28% market share (2025) |

|

Top-ranking Category (Material Type) |

Metallic Implants, ~60% market share (2025) |

|

Incremental Opportunity (2026–2033) |

US$ 69.3 billion |

Companies Covered in Medical Implants Market

- Medtronic

- Johnson & Johnson

- Stryker

- Zimmer Biomet

- Boston Scientific

- Abbott Laboratories

- Smith+Nephew

- Straumann Group

- Dentsply Sirona

- Cochlear Limited

- Globus Medical

- Biotronik

- B. Braun

Frequently Asked Questions

The global medical implants market is valued at US$ 132.4 billion in 2026.

The principal demand drivers include the rising global burden of musculoskeletal disorders affecting over 1.71 billion people according to the WHO, an aging global population projected to reach 2.1 billion people aged 60+ by 2050, and sustained technological innovation in biomaterials, 3D-printed patient-specific implants, and smart implant integration with digital health ecosystems.

North America is the leading region, holding approximately 38% of the global market share in 2025.

The integration of smart and active implants with the Internet of Medical Things (IoMT) represents the most transformative market opportunity.

Key players include Medtronic, Johnson & Johnson (DePuy Synthes), Stryker, Zimmer Biomet, Boston Scientific, Abbott Laboratories, Smith+Nephew, Straumann Group, Dentsply Sirona, Cochlear Limited, Globus Medical, Biotronik, and B. Braun.