- Hardware & Software IT Services

- Maritime Cybersecurity Market

Maritime Cybersecurity Market Size, Share, and Growth Forecast, 2026 - 2033

Maritime Cybersecurity Market by Component (Solutions, Services, Others), Security Type (Network Security, Operational Technology (OT) Security, Others), Deployment Model, End-user, and Regional Analysis for 2026 - 2033

Maritime Cybersecurity Market Size and Trends Analysis

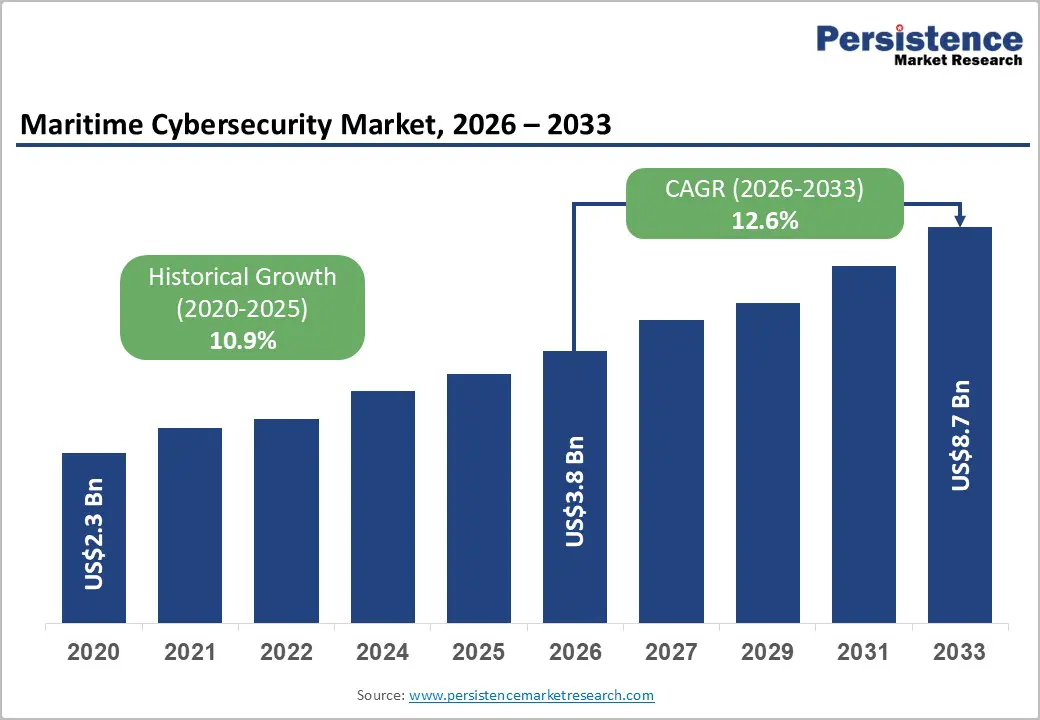

The global maritime cybersecurity market size is likely to be valued at US$3.8 billion in 2026 and is expected to reach US$8.7 billion by 2033, growing at a CAGR of 12.6% during the forecast period from 2026 to 2033, driven by increasing investments in digital transformation initiatives across the maritime sector, including connected navigation systems, cloud-based communication platforms, and operational technology (OT) networks.

Shipping companies, port operators, offshore energy providers, and naval organizations are strengthening cybersecurity frameworks in response to the rising frequency and sophistication of cyberattacks targeting vessel operations, cargo management systems, and maritime logistics infrastructure, thereby accelerating market adoption worldwide.

Key Industry Highlights:

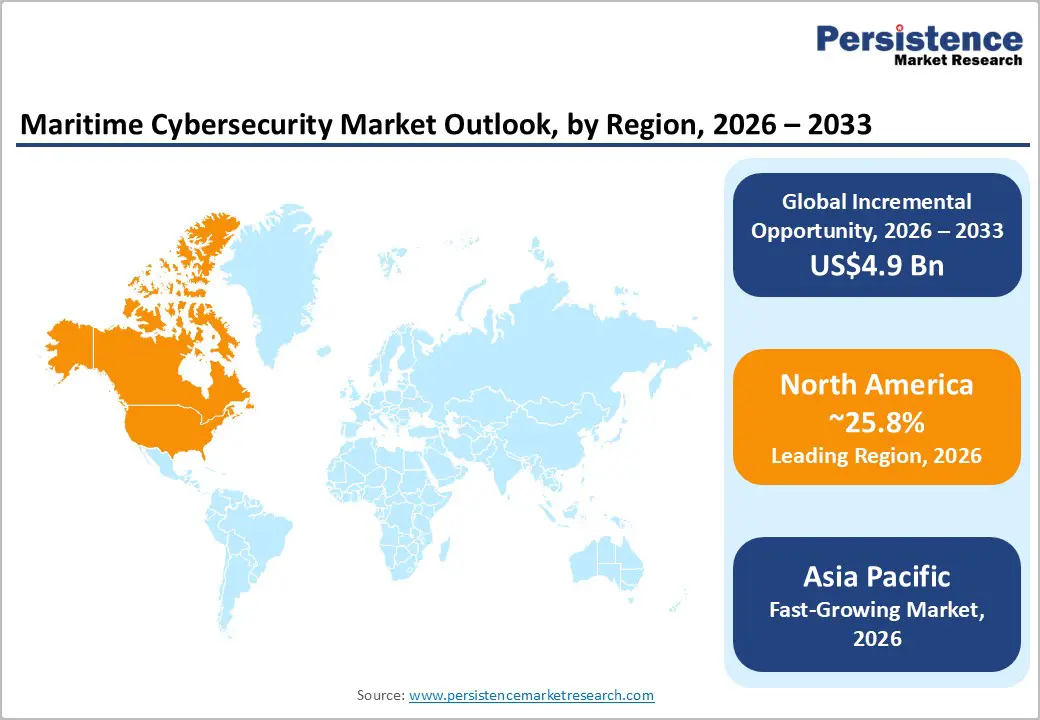

- Leading Region: North America is projected to account for 25.8% of market revenue in 2026, supported by stringent cybersecurity regulations, smart port investments, and strong adoption of OT security solutions across maritime operations.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing regional market during the forecast period due to rapid port modernization, expanding shipbuilding activity, increasing maritime trade, and rising deployment of digital vessel technologies.

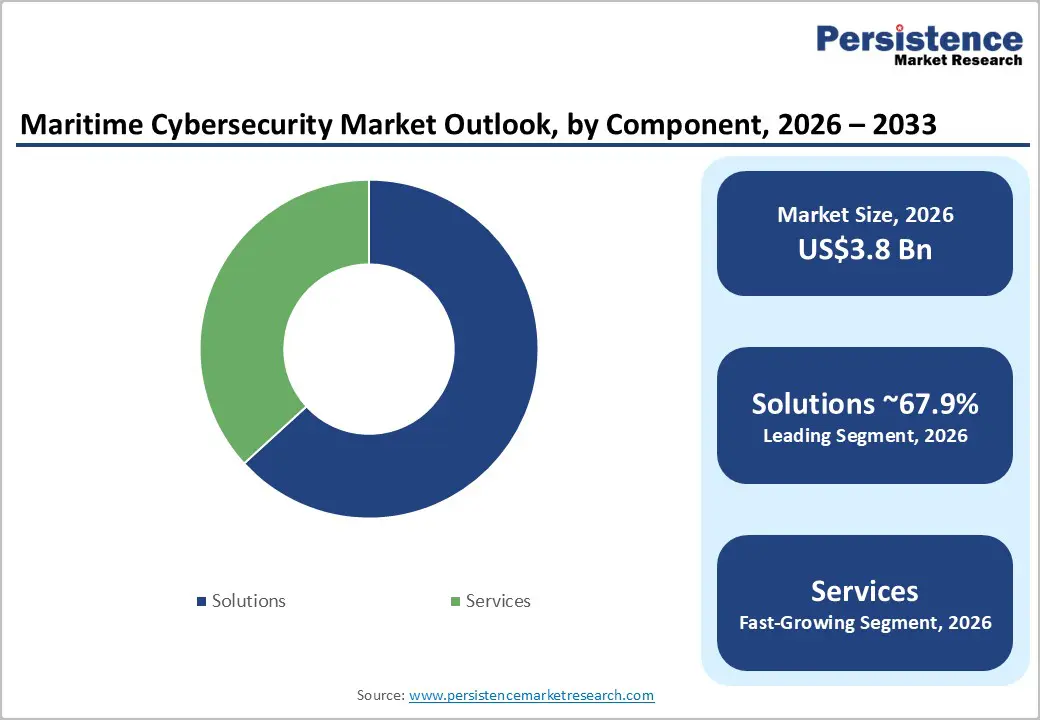

- Dominant Component: The solutions segment is anticipated to account for 67.9% of the market share in 2026, driven by growing demand for risk and compliance management platforms, intrusion detection systems, encryption technologies, and identity and access management solutions.

- Leading Security Type: The network security segment is expected to hold 34.1% of market share, supported by increasing deployment of secure communication systems, network segmentation platforms, firewalls, and threat monitoring technologies across vessels and port infrastructure.

DRO Analysis

Driver - Regulatory Hardening is Converting Cybersecurity into a Core Operational Requirement

Regulatory enforcement has become one of the strongest catalysts for maritime cybersecurity investments globally. The International Maritime Organization (IMO) continues to emphasize cyber risk management across vessel systems, while the U.S. Coast Guard’s cybersecurity regulation, implemented in 2025, introduces mandatory cybersecurity plans, designates cybersecurity officers, and imposes incident reporting obligations for regulated maritime entities. In Europe, the NIS2 Directive expanded cybersecurity obligations to maritime transport companies, vessel traffic service operators, and port authorities.

These regulatory frameworks are transforming cybersecurity from a discretionary IT initiative into a mandatory operational requirement linked to licensing, insurance eligibility, vessel certification, and operational continuity. Maritime organizations are therefore increasing spending on compliance management platforms, cybersecurity audits, risk assessments, managed detection services, and OT security controls. The market impact is particularly significant for consulting providers, managed security service vendors, and companies offering integrated compliance and cyber resilience solutions for fleet-wide deployment.

Increasing Digitalization of Vessel and Port Operations is Expanding the Attack Surface

The maritime sector is undergoing rapid digital transformation through integrated bridge systems, smart ports, remote monitoring platforms, cloud-connected logistics, and automated cargo management systems. Maritime transport remains the backbone of global trade, with seaborne shipping accounting for more than 80% of global merchandise trade by volume. As shipping ecosystems become more connected, cyber incidents can disrupt supply chains, terminal operations, fuel management, navigation systems, and cargo handling activities.

Growing reliance on operational technology environments has significantly increased the need for network segmentation, asset visibility, encryption, secure remote access, and intrusion detection systems. Maritime organizations are also adopting predictive maintenance systems, real-time analytics platforms, and digital fleet management tools, thereby further expanding their cybersecurity exposure. This shift is driving sustained demand for integrated IT-OT cybersecurity frameworks that protect both enterprise systems and mission-critical operational environments without disrupting vessel or port operations.

Restraint - Legacy Infrastructure and Long Vessel Lifecycles Increase Deployment Complexity

One of the primary restraints affecting maritime cybersecurity adoption is the prevalence of legacy infrastructure across fleets, ports, and offshore facilities. Maritime vessels often remain operational for several decades, creating significant challenges for cybersecurity modernization. Many ships operate with outdated control systems, fragmented vendor architectures, and equipment that was not originally designed for secure connectivity or remote monitoring.

Retrofitting cybersecurity controls into existing maritime environments frequently requires operational downtime, system recertification, and extensive integration work. The coexistence of legacy OT systems with modern cloud-connected applications also increases implementation complexity and elevates project costs. Many fleet operators continue to face shortages of specialized maritime cybersecurity personnel, particularly in OT security and compliance management. As a result, organizations often adopt phased deployment strategies that slow large-scale implementation and increase reliance on third-party consulting and managed services providers.

Opportunity - Rapid Expansion of OT Security and Managed Cybersecurity Services

Operational Technology (OT) security and managed cybersecurity services represent the most commercially attractive opportunities within the maritime cybersecurity ecosystem. Maritime operators increasingly require continuous monitoring, threat intelligence, incident response, penetration testing, compliance advisory, and fleet-wide cybersecurity visibility. Many organizations lack internal OT cybersecurity expertise, which is accelerating demand for outsourced managed security services and subscription-based monitoring platforms.

Vendors capable of delivering integrated cybersecurity operations centers (SOCs), compliance automation, and real-time threat detection across vessels and ports are positioned to benefit from recurring revenue opportunities. The market is also witnessing increased demand for cyber resilience assessments tied to insurance requirements and vessel certification programs.

Compliance-driven Fleet Modernization is Creating Long-Term Revenue Streams

The tightening global regulatory environment is creating a multi-year modernization cycle across vessels, ports, offshore infrastructure, and maritime logistics networks. New cybersecurity standards introduced by international classification societies and maritime regulators are encouraging operators to adopt secure-by-design digital architectures during both retrofit and newbuild projects.

Shipowners and port operators are increasingly integrating cybersecurity considerations into procurement decisions, automation upgrades, and digital transformation initiatives. This trend is generating opportunities for cybersecurity vendors offering integrated solutions that combine OT protection, compliance management, vessel certification support, training programs, and secure communications infrastructure. The transition toward connected and semi-autonomous maritime operations will further increase demand for embedded cybersecurity technologies, particularly across navigation systems, smart port infrastructure, and cloud-based operational platforms.

Category-wise Analysis

Component Insights

The solutions segment is anticipated to account for 67.9% of the market share in 2026, maintaining its position as the leading component category. Maritime operators continue to invest heavily in risk and compliance management solutions, identity and access management (IAM), firewall and intrusion detection systems, encryption technologies, and incident response platforms to secure vessel operations and shore-based infrastructure. For instance, shipping companies are increasingly deploying OT monitoring and network segmentation solutions to protect navigation systems and cargo management platforms from cyber threats.

The segment’s dominance is further supported by stricter cybersecurity regulations and the growing integration of digital technologies across ports and fleets. Operators are prioritizing cybersecurity frameworks capable of supporting secure vessel automation, satellite communications, and remote diagnostics. Demand remains particularly strong for integrated cybersecurity platforms that provide centralized visibility across fleet-wide operations.

The services segment is likely to be the fastest-growing component category. Growing demand for cybersecurity consulting, penetration testing, managed detection and response (MDR), compliance advisory, and incident response services is driving segment expansion. Maritime organizations increasingly rely on third-party specialists to manage cybersecurity risks across geographically dispersed fleets and port facilities. Limited in-house OT cybersecurity expertise among shipping operators and port authorities continues to accelerate outsourcing trends.

For example, managed security service providers are supporting commercial fleets with 24/7 threat monitoring, vulnerability assessments, and compliance reporting aligned with IMO and regional cybersecurity regulations. Vendors offering integrated consulting and monitoring services are expected to benefit significantly from the market’s long-term shift toward resilience-based cybersecurity strategies.

Security Type Insights

The network security segment is anticipated to account for 34.1% of the market share in 2026, making it the leading security category within the maritime cybersecurity market. Maritime organizations rely heavily on satellite communications, cloud-linked logistics systems, and interconnected vessel networks, making network protection a critical operational requirement. Investments in secure gateways, firewalls, intrusion detection systems, and network segmentation solutions continue to increase across shipping fleets and port infrastructure.

The growing adoption of connected vessel technologies and smart port operations is further strengthening demand for advanced network visibility and threat detection capabilities. For example, port operators are implementing network monitoring platforms to detect unauthorized access attempts targeting cargo management and vessel traffic systems. Maritime companies are also deploying encrypted communications and secure remote-access frameworks to strengthen operational resilience against cyberattacks.

The Operational Technology (OT) security segment is the fastest-growing security category. Maritime operators are increasingly prioritizing protection for propulsion systems, power management infrastructure, cargo handling systems, and industrial control environments as cyber risks targeting operational assets continue to rise. The convergence of IT and OT systems is significantly increasing cybersecurity complexity across maritime environments.

For instance, offshore operators and naval fleets are deploying OT-specific intrusion detection and asset visibility solutions to secure mission-critical systems without disrupting operations. Demand is also increasing for cybersecurity platforms capable of protecting legacy operational systems while maintaining regulatory compliance and continuous uptime across highly automated maritime environments.

Regional Insights

North America Maritime Cybersecurity Market Trends

North America is projected to account for 25.8% of market revenue in 2026 and continues to represent one of the most technologically advanced regional markets. Growth is primarily supported by stringent cybersecurity regulations, modernization of port infrastructure, and rising adoption of OT cybersecurity solutions across maritime operations. Maritime operators across the region are increasing investments in cyber risk management, incident response readiness, and compliance-focused cybersecurity frameworks to protect vessel operations, logistics systems, and port infrastructure.

U.S. Maritime Cybersecurity Market Trends

The U.S. remains the dominant contributor to the North America maritime cybersecurity market, due to its large commercial shipping infrastructure, advanced port ecosystem, and strong regulatory environment. The country continues to witness rising investments in cybersecurity planning, threat monitoring, compliance management, and OT protection solutions across ports and offshore facilities. Major U.S. ports are increasingly deploying network segmentation, real-time threat detection, and secure remote-access technologies to protect cargo handling systems and vessel traffic operations.

Canada Maritime Cybersecurity Market Trends

Canada is strengthening cybersecurity frameworks across critical infrastructure sectors, including maritime transportation and port operations. Canadian ports are increasingly integrating automated cargo handling systems, digital trade platforms, and connected logistics technologies, driving demand for advanced cybersecurity controls. The country is also emphasizing cyber resilience strategies to secure Arctic shipping routes and cross-border maritime trade infrastructure.

Europe Maritime Cybersecurity Market Trends

Europe represents a highly regulated and technologically mature maritime cybersecurity market supported by advanced shipping infrastructure, strong regulatory harmonization, and extensive international maritime trade activity. Regional growth is largely driven by increasing compliance requirements under the NIS2 Directive, which strengthened cybersecurity obligations for maritime transport companies, vessel traffic service providers, and port authorities.

Germany Maritime Cybersecurity Market Trends

Germany remains one of the largest contributors to maritime cybersecurity spending in Europe due to its advanced industrial base, port infrastructure, and strong maritime logistics sector. German shipping operators and port authorities are prioritizing investments in OT security, industrial control system protection, and secure automation technologies to support digital shipping operations and port modernization programs.

U.K. Maritime Cybersecurity Market Trends

The U.K. continues to strengthen cybersecurity frameworks across maritime infrastructure through increasing investments in cyber resilience, port security, and maritime risk management. The country’s focus on digital trade systems, offshore energy operations, and naval cybersecurity is creating sustained demand for network security, incident response, and managed cybersecurity services.

Asia Pacific Maritime Cybersecurity Market Trends

Asia Pacific is projected to be the fastest-growing regional market during the forecast period. The region benefits from extensive shipping activity, large-scale shipbuilding operations, expanding port infrastructure, and rapid digitalization of maritime ecosystems across China, Japan, India, South Korea, Singapore, and ASEAN economies.

The increasing deployment of smart ports, automated cargo terminals, cloud-connected logistics systems, and digitally integrated vessel operations is driving substantial cybersecurity demand across the region. Offshore energy expansion and rising adoption of maritime automation technologies are also contributing to strong growth in OT cybersecurity, network protection, and managed security services.

China Maritime Cybersecurity Market Trends

China remains a major contributor to regional market growth due to its large commercial shipping fleet, expanding port infrastructure, and dominant role in global maritime trade. The country is increasing investments in smart port technologies, digital shipping systems, and maritime automation, which is significantly strengthening demand for cybersecurity solutions protecting logistics platforms, vessel operations, and cargo management infrastructure.

India Maritime Cybersecurity Market Trends

India is emerging as a high-growth maritime cybersecurity market, driven by investments in port modernization, smart logistics infrastructure, and digital maritime initiatives. Government-backed port development projects and increasing adoption of connected operational systems are accelerating demand for cybersecurity frameworks capable of protecting cargo operations, port management systems, and maritime communications infrastructure.

Competitive Landscape

The global maritime cybersecurity market remains fragmented, with multiple vendors competing across cybersecurity software, managed services, OT protection, compliance consulting, and maritime automation security. Competitive differentiation is primarily based on maritime domain expertise, regulatory compliance capabilities, integrated IT-OT security offerings, and global service coverage.

Major market participants are prioritizing secure-by-design innovation, managed cybersecurity services, geographic expansion, and compliance-focused product development. Companies are increasingly integrating OT security, cloud-based monitoring, and incident response capabilities into broader maritime digitalization strategies. Strategic partnerships, recurring-service business models, and cybersecurity certification support are becoming key competitive differentiators across the global maritime cybersecurity market.

Key Industry Developments

- In April 2025, S&P Global announced an agreement to acquire ORBCOMM’s Automatic Identification System (AIS) data services business to strengthen its maritime analytics, vessel tracking, and supply chain intelligence capabilities for global shipping and maritime security operations.

- In May 2025, Infosys completed the acquisition of cybersecurity services specialist The Missing Link to expand its managed cybersecurity, threat detection, and compliance capabilities across critical infrastructure and maritime-connected industries.

Companies Covered in Maritime Cybersecurity Market

- DNV

- Kongsberg Maritime

- Wärtsilä

- Thales

- Lloyd’s Register

- ABS Group

- Bureau Veritas

- Marlink

- Honeywell

- Cydome

- VikingCloud

- Navtor

- Fortinet

- Palo Alto Networks

- BAE Systems

- Crowley Government Solutions

Frequently Asked Questions

The global maritime cybersecurity market is anticipated to be valued at US$3.8 Bn in 2026.

The market is projected to reach US$8.7 Bn by 2033.

The maritime cybersecurity market is expected to grow at a CAGR of 12.6% between 2026 and 2033.

Key trends include increasing adoption of OT cybersecurity solutions, rising deployment of cloud-based maritime security platforms, growing investments in smart ports and connected vessel technologies, expansion of managed cybersecurity services, and stronger regulatory compliance requirements across global maritime operations.

The Solutions segment is anticipated to lead the market with a 67.9% share in 2026, supported by growing demand for intrusion detection systems, identity and access management platforms, encryption technologies, and compliance management solutions.

Major companies include DNV, Kongsberg Maritime, Wärtsilä, Thales, and Lloyd’s Register.