- Hardware & Software IT Services

- Power Banks Market

Power Banks Market Size, Share, and Growth Forecast 2026 - 2033

Power Banks Market by Capacity Range (Up to 3,000 mAh, 3,001 to 8,000 mAh, 8,001 to 20,000 mAh, Above 20,000 mAh), Energy Source (Electric, Solar), Battery Type (Lithium-ion, Lithium Polymer), Distribution Channel (Online, Offline), by Regional Analysis, 2026 - 2033

Power Banks Market Size and Trend Analysis

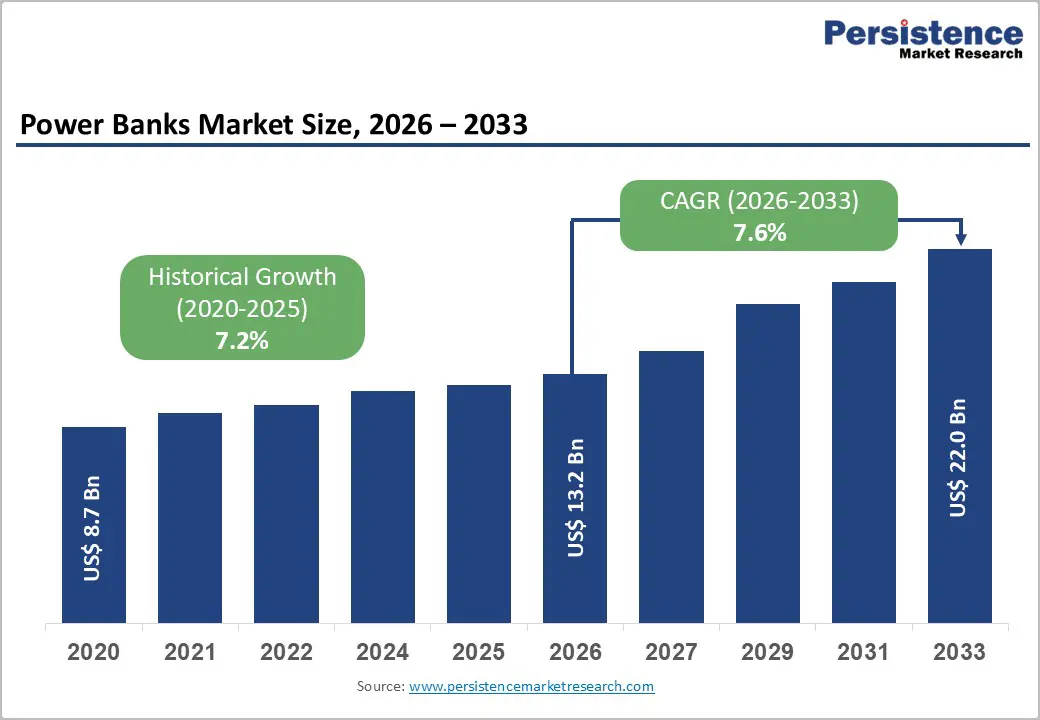

The global power banks market size is expected to be valued at US$ 13.2 billion in 2026 and projected to reach US$ 22.0 billion by 2033, growing at a CAGR of 7.6% between 2026 and 2033. The market is being driven by the rapid proliferation of smartphones, tablets, wearables, and IoT-enabled devices worldwide, combined with growing consumer preference for mobility and uninterrupted device usability.

Rising adoption of outdoor recreational activities, increasing frequency of international travel, and the integration of fast-charging and wireless charging technologies are further accelerating demand. The market's upward trajectory is also reinforced by expanding e-commerce penetration globally, which is broadening consumer access to diverse product offerings across price segments and geographies.

Key Industry Highlights

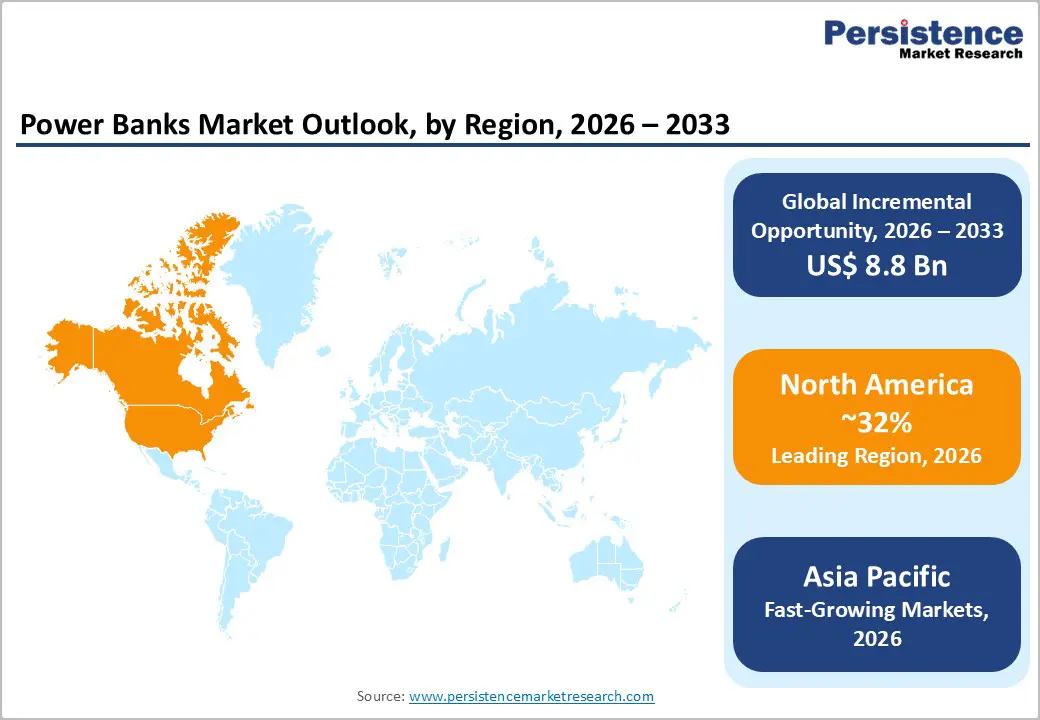

- Leading Region: North America leads the global power banks market with a 32% revenue share in 2026, supported by high per-capita electronics spending, robust 5G adoption, and a large outdoor recreation economy driving demand for high-capacity portable charging solutions.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, expanding at a 9% CAGR from 2026 - 2033, propelled by surging smartphone penetration in China, India, and Southeast Asia, improving e-commerce access, and rising disposable incomes across emerging economies.

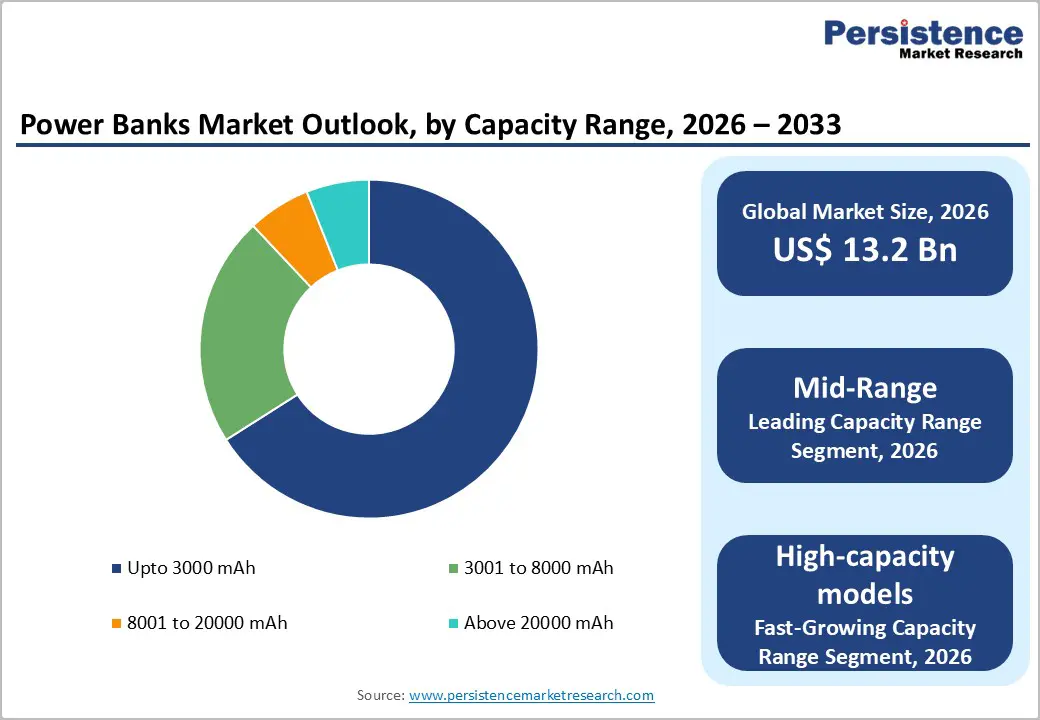

- Dominant Segment: The mid-range 8,001-20,000 mAh capacity segment dominates with 66% market share in 2026, favored for its optimal balance between portability and charging capability, making it the preferred choice for everyday multi-device users and travelers.

- Fastest Growing Segment: High-capacity above 20,000 mAh models represent the fastest-growing product segment at 9% CAGR, driven by demand from outdoor enthusiasts, laptop charging needs, and emergency preparedness applications across key markets.

- Key Market Opportunities: Integration of GaN technology and solar charging capabilities presents a significant market opportunity, enabling lighter, more powerful chargers and expanding use cases for off-grid consumers in underserved markets across Sub-Saharan Africa, Southeast Asia, and Latin America.

DRO Analysis

Market Growth Drivers

Surging Global Smartphone Penetration and Multi-Device Ecosystems

The exponential growth in smartphone adoption is a primary force propelling the power banks market. According to the International Telecommunication Union (ITU), global smartphone subscriptions surpassed 8.9 billion by end-2023, with mobile broadband penetration exceeding 90% in developed economies. Consumers increasingly operate within multi-device ecosystems, smartphones, smartwatches, wireless earbuds, and laptops, all competing for limited battery life.

The emergence of 5G-enabled handsets, while delivering faster connectivity, tends to drain batteries faster, further elevating the necessity for portable charging solutions. This multi-device reality incentivizes consumers to invest in higher-capacity and multi-port power banks, sustaining consistent volume and revenue growth across key global markets.

Growing Outdoor, Adventure Travel, and Emergency Preparedness Culture

Rising global participation in outdoor recreation, adventure tourism, and emergency preparedness activities is bolstering demand for rugged, high-capacity power banks. The U.S. Outdoor Recreation Economy, as reported by the Bureau of Economic Analysis (BEA), contributes over US$ 862 billion annually to the national GDP, illustrating the scale of the outdoor consumer segment. Increasingly, hikers, campers, and expeditionary travelers require reliable portable power for navigation devices, cameras, and emergency communication tools.

Similarly, heightened awareness of natural disasters and power outages, amplified by climate change impacts, has encouraged households to maintain portable charging reserves. This behavioral shift is driving demand for solar-compatible and above-20,000 mAh high-capacity power banks with rugged, waterproof form factors.

Market Restraints

Aviation Regulations and Capacity Restrictions on Air Travel

A persistent restraint on power bank adoption is the stringent regulatory framework imposed by civil aviation authorities globally. The International Air Transport Association (IATA) and the Federal Aviation Administration (FAA) enforce strict limits on lithium-ion battery capacity on passenger flights, generally capping portable batteries at 100 Wh (approximately 27,000 mAh at 3.7V) in carry-on luggage, while batteries exceeding 160 Wh are completely prohibited.

These restrictions limit the commercial appeal of ultra-high-capacity power banks for frequent fliers, constraining sales in the premium segment and creating consumer hesitancy around large-format products. Non-compliance risks confiscation, reducing consumer confidence and acting as a behavioral deterrent for purchasing high-capacity units.

Battery Safety Concerns and Short Product Lifespan

Safety incidents related to lithium battery thermal runaway, swelling, and fire hazards remain a notable restraint for the power banks market. Regulatory bodies including the Consumer Product Safety Commission (CPSC) in the U.S. have issued multiple recalls for substandard power bank products. Lithium-ion cells typically deliver 300-500 charge cycles before notable capacity degradation, translating to a product lifespan of 2-3 years under regular use.

This relatively short lifecycle, combined with consumer concerns around counterfeit batteries in unorganized retail channels, undermines brand trust and suppresses willingness to pay premium prices, particularly in price-sensitive emerging markets.

Market Opportunities

Integration of Solar Charging Technology for Off-Grid and Sustainable Use Cases

The growing emphasis on renewable energy and off-grid power solutions is creating substantial opportunities for solar-integrated power banks. According to the International Energy Agency (IEA), global solar photovoltaic capacity additions reached a record 295 GW in 2022, and consumer-level adoption of solar-assisted devices is accelerating. Solar power banks are increasingly relevant for emergency preparedness kits, military field applications, humanitarian aid deployments, and eco-conscious outdoor enthusiasts.

Governments across Southeast Asia, Sub-Saharan Africa, and Latin America are promoting solar-powered portable devices to bridge energy access gaps in rural regions. Companies investing in monocrystalline solar panel efficiency for compact form factors and integrating USB-C PD fast charging are well-positioned to capture this high-growth sub-segment, which is projected to outpace the broader market with a significantly high CAGR.

Rising Adoption of GaN Technology and Wireless Charging in Premium Power Banks

Gallium Nitride (GaN) semiconductor technology is transforming portable charging by enabling smaller, lighter chargers and power banks with dramatically improved power efficiency compared to traditional silicon-based designs. GaN chargers can deliver up to 100W of power in a form factor 40-60% smaller than equivalent silicon alternatives, according to industry assessments from the U.S. Department of Energy.

Simultaneously, the proliferation of Qi2-certified wireless charging standards, as certified by the Wireless Power Consortium (WPC), is accelerating the adoption of wireless-enabled power banks among premium device users. Manufacturers integrating GaN circuits with MagSafe-compatible magnetic alignment modules are unlocking new premium price tiers, enhancing margins and expanding the addressable market among Apple ecosystem and Android flagship device consumers.

Category-wise Analysis

Capacity Range Insights

The mid-range 8,001-20,000 mAh segment is the leading category by capacity range, commanding approximately 66% of the global power banks market share in 2026. This dominance is driven by the optimal balance between portability, weight, and charging capability, making these units capable of fully recharging most modern smartphones two to four times on a single charge.

The average battery capacity of flagship smartphones reached approximately 4,800 mAh in 2023, reinforcing the practical utility of mid-range power banks for daily commuters and business travelers. Their compatibility with USB-C Power Delivery (PD) and Qualcomm Quick Charge protocols further amplifies consumer preference, while competitive pricing across online and offline retail channels sustains broad accessibility across both premium and value-conscious segments.

Energy Source Insights

Electric-powered power banks constitute the dominant energy source segment, accounting for an estimated 93% share of the global market in 2026. Their supremacy is underpinned by superior energy conversion efficiency, typically exceeding 85-90% round-trip efficiency, compared to solar alternatives, which are constrained by panel size and ambient light conditions in portable form factors.

The widespread availability of AC wall outlets and USB charging infrastructure in urban and semi-urban environments globally makes electric-charged units the preferred choice for the mainstream consumer base. Advances in fast-charging protocols such as USB Power Delivery 3.1, supporting up to 240W, are consistently expanding the capability ceiling of electrically charged power banks, reinforcing their market leadership in both volume and revenue terms through the forecast period.

Battery Type Insights

Lithium-ion (Li-ion) batteries represent the dominant battery chemistry in the power banks market, capturing approximately 72% market share in 2026. Li-ion technology benefits from decades of manufacturing scale, robust supply chains anchored by major producers such as Samsung SDI, Panasonic Corporation, and CATL, and well-established global recycling infrastructure.

The technology delivers energy densities of 150-250 Wh/kg, a cycle life of up to 500 charges, and broad operating temperature tolerance from -20°C to 60°C, making it ideal for mass-market power bank applications. While Lithium Polymer (LiPo) batteries offer design flexibility and marginally higher energy density in thin-profile devices, their higher manufacturing cost and relative fragility have limited their penetration to premium and slim-form-factor power bank segments.

Distribution Channel Insights

The online distribution channel is the leading sales route for power banks globally, accounting for approximately 62% of total sales volume in 2026. E-commerce platforms including Amazon, JD.com, Flipkart, and brand-owned direct-to-consumer stores have fundamentally transformed purchasing behavior for consumer electronics accessories. Consumers benefit from extensive product comparison tools, peer review ecosystems, and frequent discount-driven promotional events such as Amazon Prime Day and Singles Day in China, reported to have generated over US$ 156 billion in gross merchandise volume in 2023 according to Alibaba Group.

The ability to reach consumers in Tier-II and Tier-III cities across emerging markets without physical retail infrastructure further amplifies the online channel's dominance and growth trajectory.

Regional Analysis

North America Power Banks Market Trends and Insights

North America leads the global power banks market with a 32% revenue share in 2026, underpinned by high per-capita consumer electronics spending, mature e-commerce infrastructure, and a culture of mobility-driven lifestyles. The region benefits from widespread adoption of premium 5G devices, a robust outdoor recreation economy, and strong demand for multi-port and wireless-charging-enabled power banks from enterprises and prosumer segments.

U.S. Power Banks Market Size

The United States accounts for approximately 78% of North America's power banks revenue, driven by high smartphone penetration, exceeding 85% of the adult population per the Pew Research Center, and a thriving outdoor recreation sector. Demand for solar and rugged power banks is particularly strong in western states, and premium fast-charging models command a significant share of urban consumer spending.

Europe Power Banks Market Trends and Insights

Europe represents a significant and steadily expanding power banks market, driven by high digital device adoption rates, robust e-commerce growth, and increasing sustainability consciousness among consumers. The region's stringent EU Battery Regulation (2023/1542) framework is encouraging the shift toward safer, recyclable battery chemistries and transparent supply chain disclosures, influencing product development and procurement strategies across the value chain.

Germany Power Banks Market Size

Germany is Europe's largest power banks market, holding approximately 22% of the regional share, supported by a large base of technologically savvy consumers, high online retail penetration, and the country's status as a leading trade fair hub through events like IFA Berlin. Demand for high-quality, certified products with CE marking compliance is particularly strong in the German market.

U.K. Power Banks Market Size

The United Kingdom contributes approximately 18% of European power banks revenue, underpinned by strong consumer electronics retail channels and one of Europe's highest mobile internet usage rates. Post-pandemic growth in domestic travel and outdoor activities has further spurred demand for mid-to-high-capacity power banks, particularly solar-compatible models popular among younger demographic cohorts.

France Power Banks Market Size

France accounts for approximately 14% of the European power bank market, driven by high urban mobility rates and a strong tourism industry that generates consistent demand for portable charging solutions among domestic and inbound international travelers. The French government's France Relance plan supporting digital infrastructure upgrades has indirectly boosted consumer electronic device adoption, sustaining power bank demand.

Asia Pacific Power Banks Market Trends and Insights

Asia Pacific is the fastest-growing region for power banks, projected to expand at a CAGR of 9% from 2026 to 2033, driven by massive smartphone adoption, rapidly improving e-commerce ecosystems, and rising disposable incomes across emerging economies. China remains the manufacturing and consumption epicenter, China's domestic power bank market is anchored by brands like Xiaomi and Baseus, with the country also serving as the primary export manufacturing hub supplying global demand through Shenzhen-based original equipment manufacturers (OEMs).

India Power Banks Market Size

India is among the fastest-growing individual markets for power banks within Asia Pacific, accounting for approximately 12% of the region's revenue in 2026. With over 750 million active smartphone users per the Telecom Regulatory Authority of India (TRAI) and a rapidly expanding 4G/5G subscriber base, domestic demand is robust. Rising rural mobile connectivity and the popularity of affordable mid-range devices are key growth engines.

Japan Power Banks Market Size

Japan holds approximately 8% of Asia Pacific's power banks market share, characterized by preference for premium, compact, and high-quality products. Japanese consumers prioritize device safety certification under PSE (Product Safety Electrical Appliance & Material) standards. The ageing population's adoption of health-monitoring wearables and tablets is generating sustained demand for lightweight, easy-to-use portable charging solutions.

Southeast Asia Power Banks Market Size

Southeast Asia is a high-growth sub-region, contributing approximately 15% of Asia Pacific's power bank market revenue in 2026 and growing faster than the regional average. Nations including Indonesia, Vietnam, Thailand, and the Philippines are experiencing rapid smartphone penetration growth. Unreliable grid power supply in rural and peri-urban areas is a structural driver elevating power bank necessity beyond discretionary consumption.

Competitive Landscape

The global power banks market is moderately fragmented, featuring a mix of established consumer electronics giants and agile specialized players. Anker Technology Co. Ltd. and Xiaomi Corporation lead in volume and brand recognition, leveraging vertically integrated supply chains and direct-to-consumer digital strategies.

Market leaders differentiate through proprietary fast-changing technologies, such as Anker's GaNPrime and Xiaomi's HyperCharge, alongside product certifications and ecosystem compatibility. Emerging players are competing on design aesthetics, solar integration, and competitive pricing. Strategic partnerships with e-commerce platforms and investments in GaN technology and wireless charging capabilities are key growth initiatives shaping competitive positioning in the forecast period.

Key Developments

- In January 2025, Anker Technology Co. Ltd. launched its GaNPrime 27,650 mAh power bank featuring 140W USB-C PD output, the company's highest wattage portable charger, targeting laptop and multi-device power users globally.

- In March 2024, Xiaomi Corporation unveiled its 33W PD wireless power bank in China and Southeast Asian markets, integrating Qi2 magnetic wireless charging and USB-C passthrough charging for simultaneous device support.

- In September 2023, Mophie (by Zagg) introduced MagSafe-compatible power bank with Apple-certified 15W wireless output, expanding its premium accessory lineup targeted at the iOS device ecosystem.

Companies Covered in Power Banks Market

- Anker Technology Co. Ltd.

- Xiaomi Corporation

- Samsung SDI Co., Ltd.

- RAVPower (by Sunvalley)

- AUKEY

- Ambrane India Private Ltd.

- ASUSTeK Computer Inc.

- Lenovo Group Ltd.

- Sony

- Otterbox

- Mophie

- Philips

- GoalZero

- Baseus

- Panasonic Corporation

Frequently Asked Questions

The global power banks market is projected to be valued at US$ 13.2 billion in 2026, growing from US$ 8.7 billion in 2020, reflecting a historical CAGR of 7.2% driven by rising smartphone adoption and consumer demand for portable charging solutions.

The primary growth drivers include surging global smartphone and multi-device adoption, with ITU reporting over 8.9 billion mobile subscriptions by 2023, rising demand from outdoor recreation and adventure travel segments, and technological advancements in GaN fast charging and wireless charging platforms that are expanding the product's functional appeal.

North America is the leading regional market, accounting for approximately 32% of global revenue in 2026. The region benefits from high consumer electronics expenditure, widespread 5G device adoption, a large outdoor recreation economy, and mature e-commerce channels facilitating broad product accessibility.

Significant opportunities lie in the integration of solar charging technology for off-grid and sustainability-focused applications, and in the development of GaN-powered premium power banks with wireless Qi2 charging. Emerging markets across Southeast Asia, Sub-Saharan Africa, and Latin America also present high-growth opportunities driven by expanding mobile connectivity and energy access gaps.

Leading companies in the global power banks market include Anker Technology Co. Ltd., Xiaomi Corporation, Samsung SDI Co., Ltd., RAVPower (by Sunvalley), AUKEY, Mophie, Baseus, Panasonic Corporation, GoalZero, Lenovo Group Ltd., and Sony, among others.