- Hardware & Software IT Services

- Smart Parcel Locker Market

Smart Parcel Locker Market Size, Share, and Growth Forecast 2026 - 2033

Smart Parcel Locker Market by Component (Hardware, Software, Services), Deployment Type (Indoor Lockers, Outdoor Lockers), Locker Type (Modular Parcel Lockers, Postal Lockers, Cooling/Temperature-Controlled Lockers, Laundry Lockers), End-user (Commercial Buildings, Corporate Offices, Residential/Condos & Apartments, Retail BOPIS, Universities & Colleges, Government Buildings, Logistics Centers), and Regional Analysis, 2026 - 2033

Smart Parcel Locker Market Size and Trend Analysis

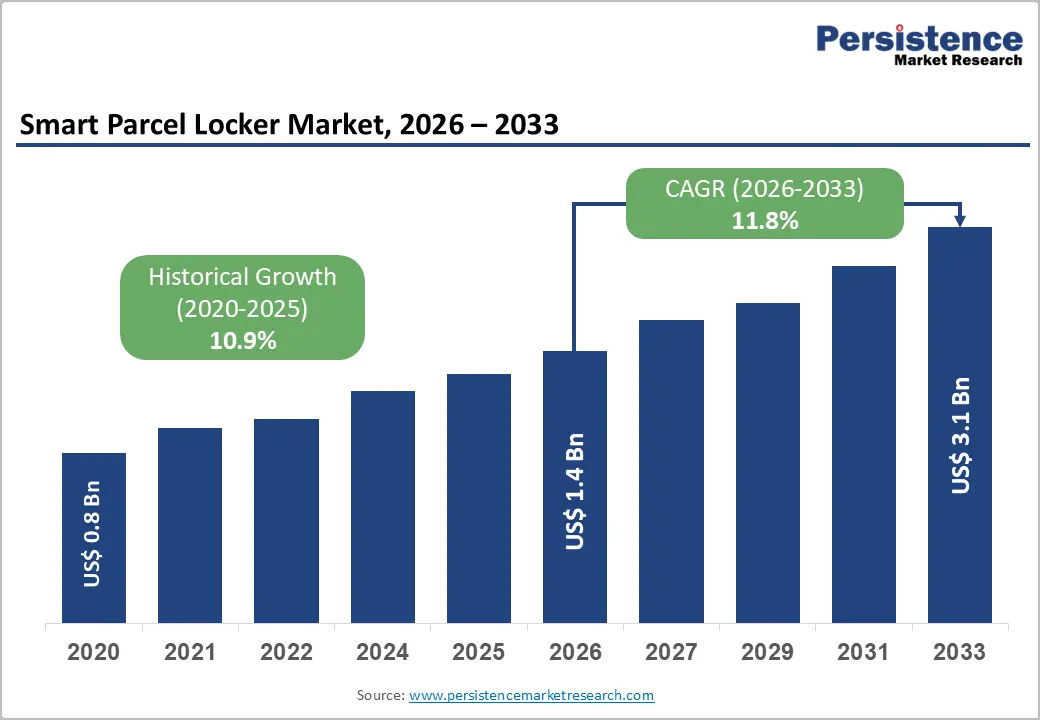

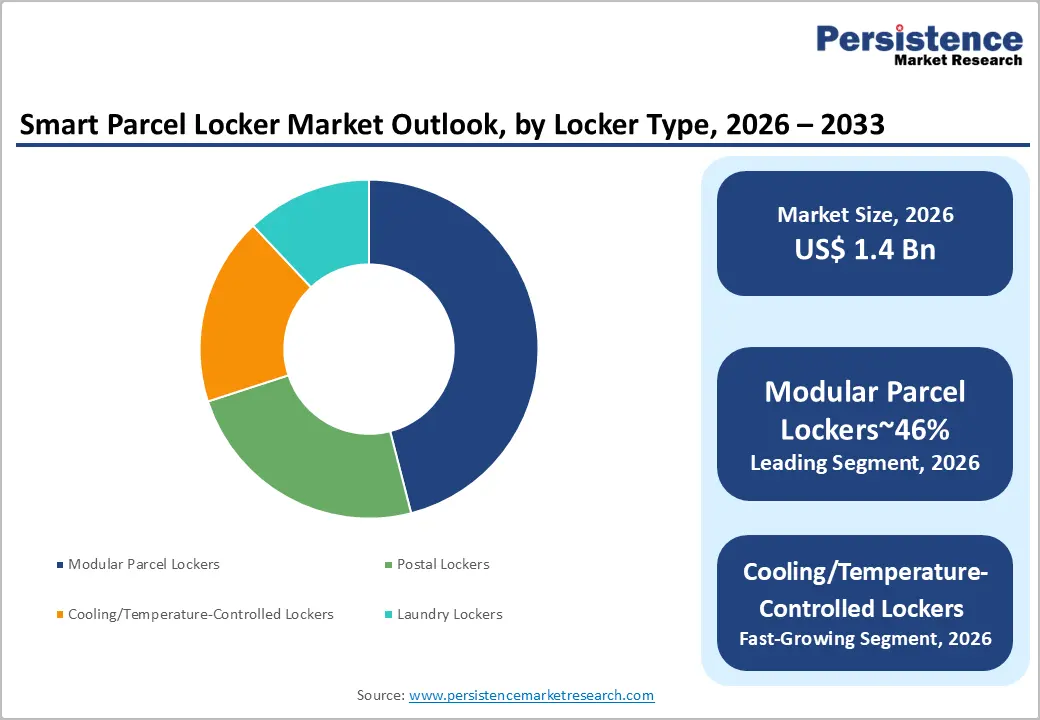

The global smart parcel locker market size is likely to be valued at US$ 1.4 billion in 2026 and is expected to reach US$ 3.1 billion, growing at a CAGR of 11.8% during the forecast period from 2026 to 2033.

The market's strong expansion trajectory is fundamentally driven by the explosive growth of global e-commerce, acute last-mile delivery inefficiencies, and surging consumer demand for flexible, contactless parcel collection.

Key Industry Highlights:

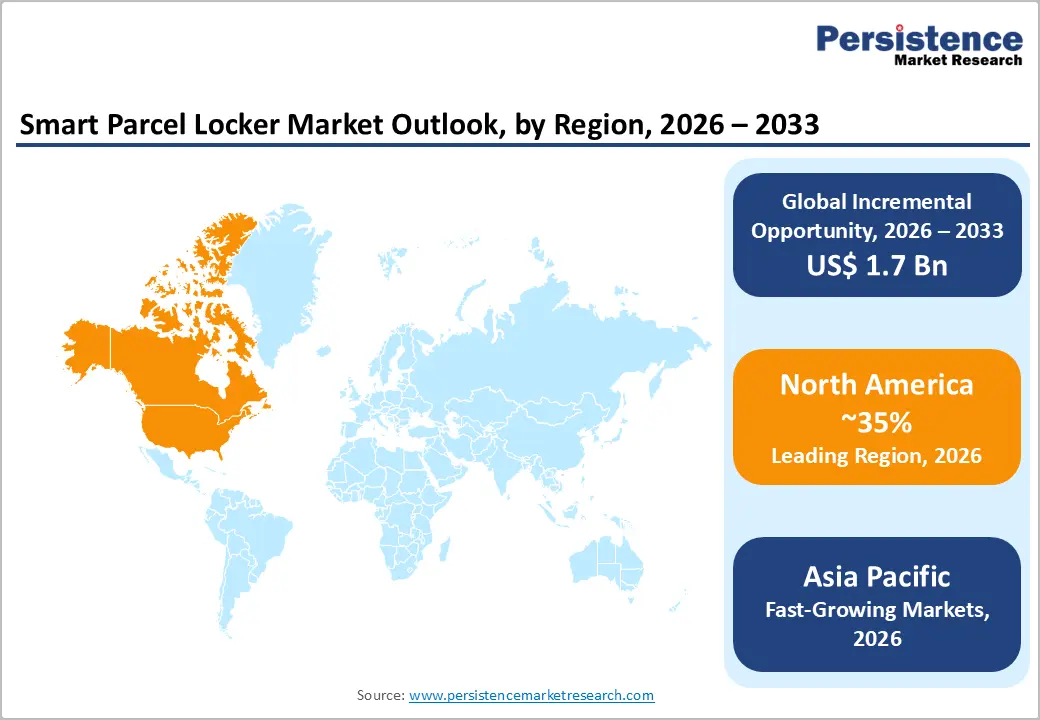

- Leading Region: North America dominates the smart parcel locker market holding 35% share, underpinned by the U.S. e-commerce industry exceeding US$ 1.1 trillion in annual sales, the widespread BOPIS retail model adoption, and leading domestic players including Luxer One and Florence Corporation.

- Fast-Growing Market: Asia Pacific is the fast-growing market, fueled by China's massive Cainiao locker network, sIndia's Digital India policy initiatives, and surging parcel volumes from ASEAN e-commerce platforms such as Shopee and Lazada, driving locker infrastructure investment.

- Dominant End-user Segment: Residential/condos & apartments is the leading end-user segment (31% share), driven by unprecedented residential parcel volumes, NMHC data confirming 80%+ weekly delivery rates, and parcel lockers becoming a standard amenity in multi-family housing developments.

- Fast-Growing Locker Type Segment: Cooling/Temperature-Controlled Lockers represent the fastest-growing locker type segment, powered by online grocery, pharmaceutical e-commerce, and meal-kit delivery growth, with FAO data highlighting critical cold chain gaps in last-mile logistics infrastructure.

- Key Opportunity: Temperature-controlled and residential locker deployments present the highest-growth opportunity, supported by EU sustainability mandates, NMHC tenant satisfaction data, and expanding regulatory frameworks mandating package management infrastructure in new multi-family construction globally.

Market Dynamics

Drivers - E-Commerce Boom and Last-Mile Delivery Transformation

The relentless growth of global e-commerce remains a dominant catalyst for smart parcel locker adoption. The United Nations Conference on Trade and Development (UNCTAD) estimated that global e-commerce sales surpassed US$ 27 trillion in 2022, with business-to-consumer (B2C) online retail growing at an accelerated pace across both developed and emerging economies. This volume surge has created a severe last-mile delivery crisis: delivery networks face mounting costs, failed delivery rates, and growing urban congestion.

Smart parcel lockers directly mitigate these pain points by consolidating multiple deliveries at a single access point, reducing per-parcel delivery costs by up to 60% compared to individual home delivery attempts. The parallel expansion of the Buy Online, Pick Up In Store (BOPIS) model, adopted aggressively by major retailers, further entrenches parcel lockers as essential retail infrastructure across commercial and urban environments.

Urbanization and Smart City Infrastructure Investment

Accelerating global urbanization is generating powerful structural demand for smart parcel lockers as city authorities and property developers integrate them into smart city frameworks. The United Nations Department of Economic and Social Affairs (UN DESA) projects that 68% of the world's population will reside in urban areas by 2050, intensifying the need for efficient urban logistics solutions. Municipalities across Europe and Asia are actively incorporating parcel locker networks into public transit hubs, post offices, and residential complexes as part of broader smart city initiatives.

The European Commission's Urban Mobility Framework explicitly endorses consolidated parcel delivery solutions to reduce urban freight vehicle movements and associated carbon emissions. This regulatory alignment between sustainability policy and parcel locker deployment is accelerating public and private investment in locker infrastructure across major metropolitan centers globally.

Restraints - High Capital Expenditure and Infrastructure Complexity

The significant upfront capital expenditure required for smart parcel locker deployment, encompassing hardware procurement, installation, network connectivity, and software integration, represents a material barrier for small and mid-sized property managers, retailers, and logistics operators.

A standard outdoor smart locker installation can cost between US$ 15,000 and US$ 80,000, depending on capacity, technology features, and connectivity requirements. For residential property managers operating on thin margins, these costs are difficult to justify without established revenue-sharing or subsidized deployment models, constraining organic market penetration in lower-tier real estate segments.

Cybersecurity Vulnerabilities and Data Privacy Concerns

Smart parcel lockers, as networked IoT devices processing sensitive user data, including identity verification, payment credentials, and delivery histories, are increasingly exposed to cybersecurity threats. The European Union Agency for Cybersecurity (ENISA) has consistently flagged connected physical infrastructure as a high-risk attack vector.

Data privacy regulations such as the EU General Data Protection Regulation (GDPR) impose stringent data handling obligations on locker operators, increasing compliance costs. High-profile data breaches in connected logistics infrastructure erode consumer trust and slow institutional adoption, particularly in government and healthcare facility deployments.

Opportunities - Temperature-Controlled Lockers: Capturing the Cold Chain Last Mile

Cooling and temperature-controlled smart parcel lockers represent one of the most compelling high-growth opportunities in the market, driven by the explosive expansion of online grocery delivery, pharmaceutical e-commerce, and meal-kit subscription services. The Food and Agriculture Organization (FAO) estimates that global food losses in cold chain logistics exceed 14% of post-harvest food production, highlighting the systemic need for temperature-controlled last-mile infrastructure.

Companies such as Cleveron and Quadient are actively developing refrigerated locker solutions for grocery retailers and pharmacies. Post-pandemic growth in online pharmacy orders, which require temperature-specific handling, further strengthens this segment's commercial viability. Manufacturers that invest in energy-efficient refrigeration technology compliant with EU F-Gas Regulation and U.S. energy efficiency standards are well-positioned to capture this emerging demand segment.

Residential and Multi-Family Housing Deployment: A High-Volume Growth Frontier

The residential and multi-family housing segment, encompassing condominiums, apartment complexes, and mixed-use developments, represents the fastest-growing end-user opportunity for smart parcel locker manufacturers. The surge in parcel volumes delivered to residential addresses, accelerated by pandemic-driven behavioral shifts toward online shopping, has made parcel management a critical amenity decision factor for property developers and tenants alike.

According to the National Multifamily Housing Council (NMHC) in the United States, over 80% of apartment residents receive package deliveries at least once per week, and properties offering smart locker amenities report meaningfully higher tenant satisfaction and retention scores. Government-backed affordable housing programs and urban development mandates in Europe and Asia Pacific requiring last-mile logistics infrastructure further amplify this opportunity for solution providers targeting residential real estate stakeholders.

Category-wise Analysis

By Component Insights

The hardware segment dominates the smart parcel locker market by component, commanding approximately 58% of total market revenue. Hardware encompasses the physical locker units, electronic locking mechanisms, touchscreens, barcode/QR code scanners, cameras, and network connectivity modules that constitute the core product offering. The capital-intensive nature of locker deployment, where hardware constitutes the primary upfront investment, inherently drives hardware's revenue dominance relative to software and services.

Additionally, as the installed base of smart lockers continues to expand globally, driven by large-scale deployments by logistics operators such as InPost and postal agencies, cumulative hardware procurement volumes compound significantly. Ongoing product innovation, including solar-powered outdoor units, modular expandable cabinets, and ADA-compliant accessibility features, further sustains premium hardware pricing and revenue concentration in this segment.

By Deployment Type Insights

Outdoor lockers lead the deployment type category, representing approximately 62% of total market revenue. Outdoor smart parcel lockers, deployed at retail parking lots, transit stations, grocery store exteriors, and residential building entrances, benefit from 24/7 accessibility without the access restrictions inherent to indoor deployments.

Their capacity to serve a significantly larger addressable catchment, including non-residents and multiple delivery carriers simultaneously, makes them the preferred solution for logistics network operators seeking maximum utilization efficiency. InPost's extensive outdoor locker network across Poland and the UK, exceeding 20,000 locations across Europe, exemplifies the scalability advantage of outdoor deployment models. Advances in weather-resistant enclosure engineering and solar energy integration continue to broaden viable deployment environments for outdoor units.

By Locker Type Insights

The modular parcel lockers account for a leading position within the locker type category, accounting for approximately 46% of market revenue. The dominance of modular systems reflects their fundamental operational advantage: scalable compartment configurations that can be customized to accommodate diverse parcel sizes and volumetric throughput requirements without requiring complete system replacement.

Property managers, logistics operators, and retailers value the capital efficiency of modular lockers, which allow capacity expansion through the addition of individual cabinet modules as package volumes grow. Quadient and Luxer One have established modular architectures as the commercial standard across residential and commercial deployments. The ability to integrate modular lockers with carrier-agnostic delivery management platforms, supporting UPS, FedEx, Amazon, and USPS simultaneously, further underpins their market leadership.

By End-user Insights

The residential/condos & apartments end-user segment commands the leading share in the smart parcel locker market, accounting for approximately 31% of total end-user revenue. This dominance is underpinned by the unprecedented surge in residential parcel deliveries driven by e-commerce growth, the structural challenge of managing high delivery volumes in multi-family buildings with limited staff, and the increasing standardization of parcel lockers as a premium residential amenity.

According to the National Multifamily Housing Council (NMHC), parcel management consistently ranks among the top technology amenities that apartment residents expect from their properties. Property developers and real estate investment trusts (REITs) are systematically incorporating smart lockers into new construction specifications and retrofit programs to enhance competitive positioning and tenant retention in an increasingly amenity-driven rental market.

Regional Insights

North America Smart Parcel Locker Market Trends and Insights

North America accounted for approximately 35% of the global smart parcel locker market in 2026, representing an estimated market value of around US$ 0.48 Billion. Regional dominance is supported by strong e-commerce penetration, high parcel delivery density, and rapid expansion of BOPIS and contactless delivery infrastructure. The U.S. continues to lead deployment activity across residential complexes, universities, retail stores, and office campuses, while retailers and logistics providers increasingly integrate AI-enabled locker management systems to optimize last-mile efficiency.

- United States Smart Parcel Locker Market Size

The U.S. smart parcel locker market is estimated at nearly US$ 0.41 Billion in 2026, accounting for over 85% of the North American market. Market growth is driven by surging e-commerce volumes, expansion of Amazon Hub Locker installations, and rising adoption among multifamily housing operators. Increasing investments in smart city infrastructure and automated last-mile logistics solutions are expected to sustain double-digit market expansion through 2033.

Europe Smart Parcel Locker Market Trends and Insights

Europe represented approximately 30.0% of the global smart parcel locker market in 2026, reaching an estimated value of about US$ 0.42 Billion. The region benefits from highly mature parcel automation ecosystems, dense urban populations, and strong regulatory support for sustainable urban logistics. Governments and postal operators increasingly promote parcel locker networks to reduce delivery congestion and carbon emissions, while GDPR-driven software upgrades continue improving operational security and consumer trust.

- Germany Smart Parcel Locker Market Size

Germany is one of Europe’s largest smart parcel locker markets, valued at approximately US$ 1100 million in 2026. The country’s strong position is supported by Deutsche Post DHL’s extensive Packstation network and high consumer preference for self-service parcel collection. Rising online retail sales and urban delivery optimization initiatives continue accelerating locker installations across transportation hubs and residential districts.

- United Kingdom Smart Parcel Locker Market Size

The U.K. smart parcel locker market is estimated at around US$ 90 million in 2026. Strong e-commerce penetration, widespread click-and-collect adoption, and increasing investment by grocery and retail chains are major growth drivers. Retailers are rapidly integrating automated lockers into convenience stores and transit stations to improve customer delivery flexibility and reduce failed home deliveries.

- France Smart Parcel Locker Market Size

France is likely to witness a rapid expansion of InPost and national courier locker networks is reshaping last-mile delivery models across major urban centers. Sustainability-focused logistics policies and growing consumer demand for flexible delivery options are encouraging further deployment across residential communities and retail environments.

Asia Pacific Smart Parcel Locker Market Trends and Insights

Asia Pacific accounted for nearly 27% of the global smart parcel locker market in 2026, reaching an estimated value of approximately US$ 380 million. The region is the fastest-growing market globally, driven by explosive e-commerce expansion, rapid urbanization, and strong digital payment adoption. China dominates regional deployments, while India and Southeast Asia are witnessing accelerated investments in automated logistics infrastructure under smart city and digital commerce initiatives.

- China Smart Parcel Locker Market Size

China leads the Asia Pacific smart parcel locker market with an estimated value of nearly US$ 0.19 Billion in 2026. Massive parcel volumes generated by Alibaba, JD.com, and other e-commerce giants continue driving locker network expansion nationwide. Cainiao’s extensive smart locker ecosystem and strong government support for intelligent logistics infrastructure position China as a global leader in automated parcel delivery systems.

- India Smart Parcel Locker Market Size

India’s smart parcel locker market is estimated at approximately US$ 50 million in 2026 and is projected to witness one of the fastest growth rates globally through 2033. Rising e-commerce penetration, rapid growth of tier-2 city logistics networks, and government-backed Digital India initiatives are accelerating pilot deployments by logistics providers, residential developers, and organized retail operators.

- Japan Smart Parcel Locker Market Size

Japan smart parcel locker market is driven by high urban density, advanced automation infrastructure, and strong consumer preference for unattended delivery systems support widespread locker adoption. Major railway stations, convenience stores, and apartment complexes increasingly utilize smart parcel lockers to address labor shortages and improve delivery efficiency in metropolitan regions.

Competitive Landscape

The global smart parcel locker market exhibits a moderately fragmented competitive structure, with the top five players collectively accounting for an estimated 45% of global revenue. Quadient (through its Parcel Pending acquisition) and InPost lead the market, differentiated through carrier-agnostic software platforms, API integration capabilities, and geographic network scale.

Key competitive differentiators include locker modularity, mobile app user experience, real-time delivery notifications, and cloud-based management dashboards. Emerging business model trends include locker-as-a-service (LaaS) subscription models, revenue-sharing partnerships with property managers, and open-network carrier collaboration platforms that allow multiple couriers to utilize the same locker infrastructure.

Key Developments:

- February, 2025: Quadient announced the expansion of its Parcel Pending smart locker network in the U.S. with the launch of an AI-powered predictive maintenance platform, reducing locker downtime by up to 40% through proactive diagnostics.

- October, 2024: InPost reported the milestone of surpassing 25,000 Paczkomat locker locations across Europe, with aggressive expansion into France and Italy, targeting 30,000 locations by 2025 to serve growing cross-border e-commerce volumes.

- March, 2024: Cleveron unveiled its next-generation Cleveron 501 temperature-controlled outdoor parcel locker, designed for grocery and pharmaceutical retailers, featuring dual-zone cooling capability maintaining temperatures from -20°C to +10°C for cold chain last-mile fulfillment.

Smart Parcel Locker Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 0.8 Billion |

| Current Market Value (2026) | US$ 1.4 Billion |

| Projected Market Value (2033) | US$ 3.1 Billion |

| CAGR (2026 - 2033) | 11.8% |

| Leading Region | North America (35%) |

| Top-ranking Locker Type | Modular Parcel Lockers (46.0%) |

| Top-ranking End-User | Residential/Condos & Apartments (31.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 1.7 Billion |

Companies Covered in Smart Parcel Locker Market

- Quadient

- Parcel Pending by Quadient

- TZ Limited

- Cleveron

- Pitney Bowes

- KEBA AG

- Smartbox Ecommerce Solutions

- Luxer One

- Hollman Inc.

- Florence Corporation

- Meridian Kiosks

- Ricoh Group

- InPost

- Bell and Howell

- Apex Supply Chain Technologies

- Renault Easy'Box

- Swisslog Holding AG

Frequently Asked Questions

The global smart parcel locker market is estimated to be valued at US$ 1.4 billion in 2026 and is projected to reach US$ 3.1 billion by 2033, growing at a CAGR of 11.8% during the forecast period.

The primary demand drivers include the global e-commerce boom, with UNCTAD estimating worldwide e-commerce sales exceeding US$ 27 trillion, combined with escalating last-mile delivery costs, the widespread adoption of BOPIS retail models, rapid urbanization driving smart city infrastructure investment, and the structural shift toward contactless, self-service parcel collection behaviors accelerated by the COVID-19 pandemic.

The hardware is the leading segment for the smart parcel locker market by component, accounting for approximately 58% of global revenue. Hardware dominance reflects the capital-intensive nature of locker deployment, where physical units, including electronic locking mechanisms, touchscreens, scanners, and connectivity modules, constitute the primary upfront investment for operators and property managers across all end-user verticals.

North America holds the largest regional share in the global smart parcel locker market, with the United States serving as the primary demand driver through its trillion-dollar e-commerce retail economy, widespread BOPIS adoption, and established locker networks deployed by companies including Luxer One, Parcel Pending by Quadient, Florence Corporation, and Amazon through its Hub Locker infrastructure.

The most significant growth opportunities lie in temperature-controlled locker deployments for grocery and pharmaceutical last-mile fulfillment, addressing FAO-identified cold chain gaps, and in the residential/multi-family housing segment, where NMHC data confirms over 80% of apartment residents receive weekly deliveries, driving demand for smart locker amenities in new construction and retrofit programs.

Leading companies in the global smart parcel locker market include Quadient, Parcel Pending by Quadient, InPost, Cleveron, TZ Limited, KEBA AG, Luxer One, Florence Corporation, Pitney Bowes, Bell and Howell, Meridian Kiosks, Ricoh Group, Hollman Inc., Smartbox Ecommerce Solutions, and Apex Supply Chain Technologies, among others including Amazon, Cainiao Network, and Deutsche Post DHL.