- Healthcare IT

- Femtech Market

Femtech Market Size, Share, and Growth Forecast 2026 - 2033

Femtech Market by Product Type (Devices, Software, Services, Consumer Products), Application (Pregnancy and Nursing Care, Reproductive Health & Contraception), End-user (Direct to Consumer, Hospitals), and Regional Analysis, 2026 - 2033

Femtech Market Size and Trends Analysis

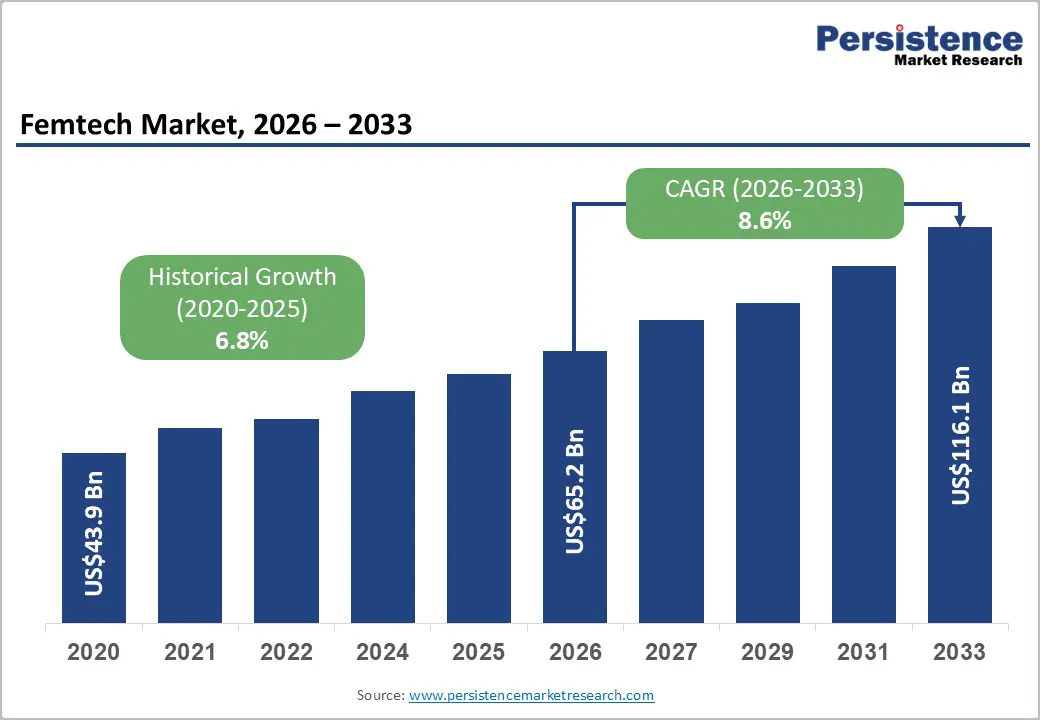

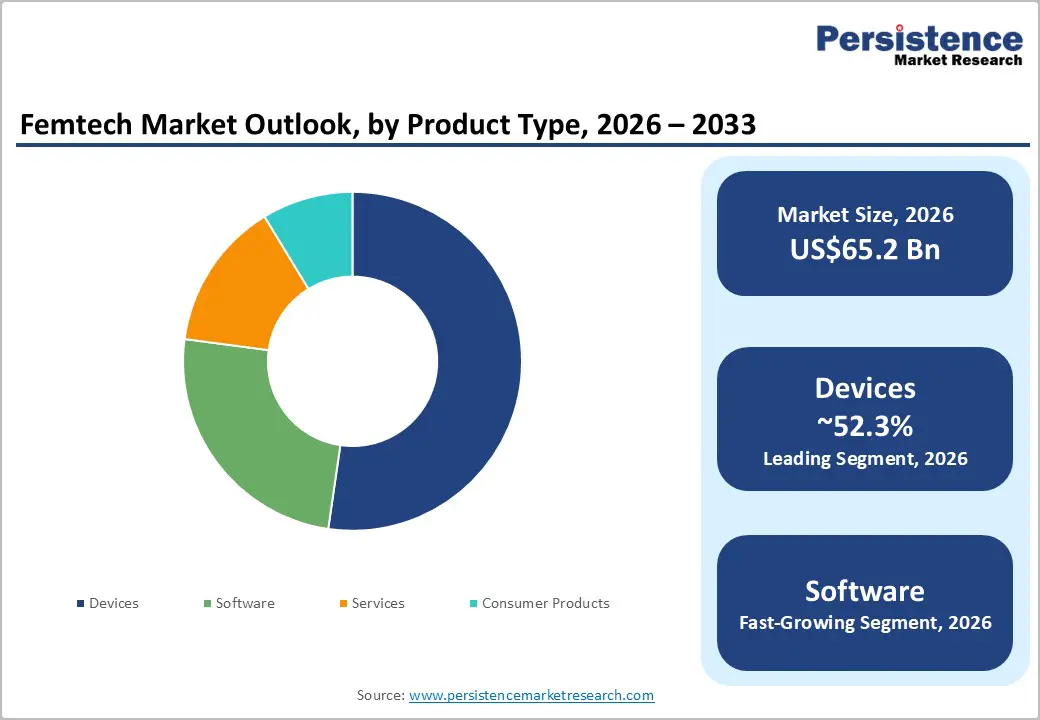

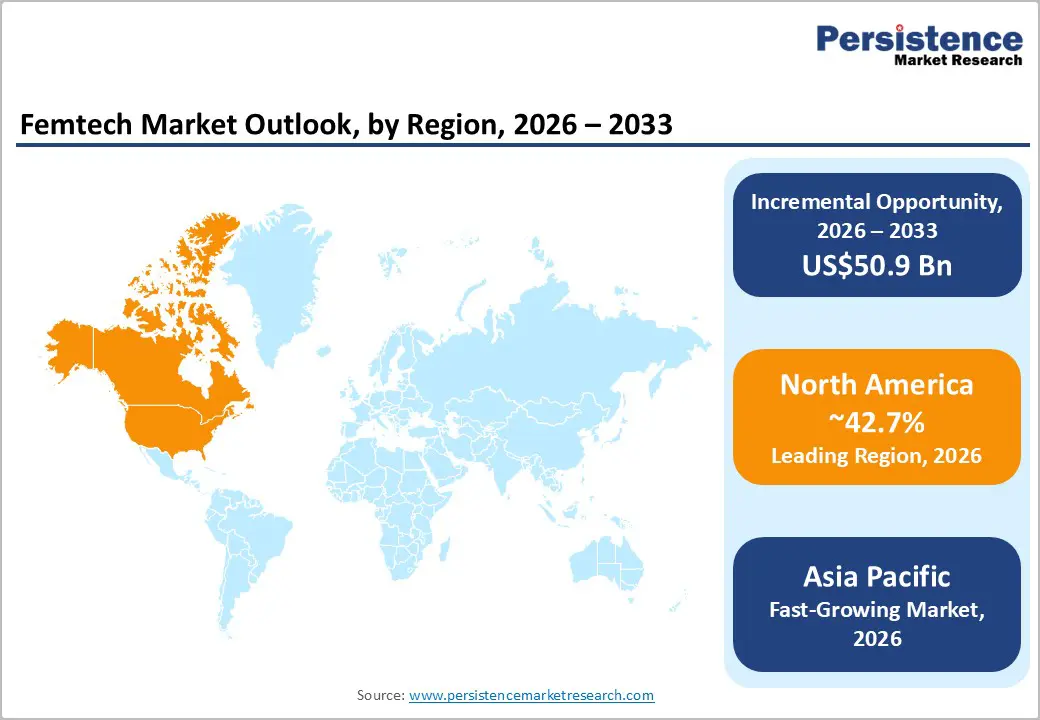

The global femtech market size is likely to be valued at US$65.2 billion in 2026 and is expected to reach US$116.1 billion by 2033, growing at a CAGR of 8.6% during the forecast period from 2026 to 2033, driven by increasing demand from women for personalized healthcare solutions for fertility, menstrual health, pregnancy, menopause, and hormonal wellness.

Surging awareness around historically underserved women’s health conditions is also pushing the market.

Key Industry Highlights:

- New Funding Initiative: The Île-de-France region recently launched the Femtech Île-de-France Fund to support various initiatives associated with women’s health throughout their lives. The Innovation Santé team from Turenne Groupe and Université Paris Cité will bring their expertise on women’s health.

- Leading Region: North America, with 42.7% share in 2026, backed by novel digital healthcare infrastructure and strong venture capital activity.

- Fast-growing Region: Asia Pacific, spurred by rising smartphone penetration and expanding telehealth access.

- Leading Product Type: Devices, around 52.3% in 2026, as wearable fertility trackers and smart breast pumps provide continuous, real-time health insights.

- Dominant Application: Pregnancy and nursing care, nearly 32.6% in 2026, because women now prefer remote maternity monitoring and personalized postpartum care tools.

DRO Analysis

Driver- Increasing Burden of Reproductive and Menstrual Health Conditions

The rising prevalence of fertility complications and menstrual disorders is augmenting demand for femtech solutions focused on diagnosis, monitoring, and personalized care. Conditions such as polycystic ovary syndrome (PCOS), endometriosis, and infertility are becoming widely diagnosed due to better awareness and digital health access. According to the World Health Organization (WHO), around one in six people globally experience infertility during their lifetime.

It showcases the urgent requirement for fertility tracking and reproductive support technologies. Menstrual health apps and wearable devices are also helping users monitor irregular cycles and hormonal patterns in real time. Companies, including Flo Health and Clue, have expanded their platforms beyond cycle tracking into areas such as ovulation prediction, symptom analysis, and menopause management. This reflects the widening healthcare role of femtech platforms.

Integration of Digital Health Tools Transforming Women’s Healthcare Access

Surging adoption of digital health technologies is becoming a key growth driver for the market as women increasingly rely on mobile apps, AI-based platforms, and wearable devices for personalized healthcare management. Modern femtech solutions now go far beyond period tracking, delivering real-time fertility monitoring, menopause management, hormonal analysis, and virtual consultations. Apps such as Flo Health reported over 70 million monthly active users in 2024, showcasing the mainstream acceptance of digital reproductive health tools.

Wearable devices are also gaining popularity for tracking ovulation, sleep, temperature, and stress biomarkers linked to hormonal health. AI integration is improving predictive insights and personalized recommendations, making women’s healthcare more preventive and data-driven. This shift is specifically important in regions where access to gynecological care remains limited.

Restraint- Data Bias and Clinical Validation Gaps Limit Trust in Femtech Algorithms

One of the important restraints in femtech is the lack of balanced and clinically validated women’s health datasets used to train AI-based platforms. Several digital health algorithms are still built on historically male-dominated medical data, making predictions less accurate for female-specific conditions such as endometriosis, PCOS, menopause, and hormonal disorders. A 2024 study published in Frontiers in Big Data showed that gender bias in healthcare AI remains a key challenge due to the underrepresentation of women in clinical datasets.

In a few cases, algorithms have reportedly misclassified women’s symptoms or produced inconsistent fertility and cycle predictions. Experts have also raised concerns that unvalidated AI systems in reproductive health could generate flawed evaluations and reduce patient trust. These issues are creating regulatory scrutiny and slowing adoption among healthcare providers seeking clinically reliable femtech solutions.

Opportunity - Femtech Providers Join Hands with Employers to Add New Programs

Employers are increasingly adding women-focused healthcare programs to workplace benefit packages, creating new growth opportunities for femtech providers. Companies are now covering services related to fertility treatment, pregnancy support, menopause care, and mental wellness to improve employee retention and workplace inclusivity. For instance, Maven Clinic partners with large multinational employers to provide digital fertility and maternity care services across multiple countries.

Organizations are also providing access to fertility preservation benefits such as egg freezing and IVF support, especially in the technology and finance sectors. This shift is transforming femtech from a direct-to-consumer model into an enterprise-supported healthcare category. It is further allowing digital health start-ups to expand their presence through corporate partnerships rather than relying only on individual subscriptions.

Increasing Investor and Corporate Capital Creates Expansion Avenues

Rising venture capital activity and corporate investments are creating lucrative growth opportunities for femtech companies by accelerating product development and global expansion. Investors are increasingly recognizing women’s health as an underserved but high-impact healthcare segment. In 2024, Flo Health secured over US$ 200 million in Series C funding from General Atlantic, becoming the first purely digital women’s health app to achieve unicorn status.

Beyond large firms, AI-based start-ups such as Ema and regional players, including Newmi Care, are also attracting funding for specialized women’s healthcare platforms. This inflow of capital is helping femtech companies broaden clinical services, improve AI-backed diagnostics, and expand into areas such as menopause care, cardiovascular health, and preventive wellness.

Category-wise Analysis

Product Type Insights

In 2026, devices are anticipated to lead with approximately 52.3% of the market share, as these provide measurable, real-time health data that users and healthcare professionals can directly act upon. Unlike apps that rely heavily on self-reported information, devices such as fertility trackers, breast pumps, pelvic floor trainers, smart thermometers, and wearable hormone monitors deliver continuous physiological monitoring. Products such as the Oura Ring and Ava Fertility Tracker are being used for ovulation prediction and sleep-hormone correlation analysis. Smart breast pumps from companies such as Elvie have also transformed postpartum care by enabling discreet and app-connected pumping.

Software platforms are predicted to remain the fastest-growing segment as femtech companies are constantly integrating AI, telehealth, and predictive analytics into women’s healthcare. Modern platforms now deliver personalized symptom tracking, virtual consultations, fertility coaching, and menopause management through a single digital ecosystem. Apps, including Flo Health and Clue, are moving beyond period tracking by using machine learning to identify irregular cycles, fertility windows, and hormonal trends.

Application Insights

Pregnancy and nursing care are projected to dominate in 2026, with nearly 32.6% of the share as women increasingly seek continuous monitoring, remote support, and personalized guidance throughout maternity and postpartum stages. Femtech solutions are helping manage high-risk pregnancies, breastfeeding challenges, sleep issues, and postpartum recovery outside traditional hospital settings. Wearables and mobile apps now track fetal movements, contractions, maternal vitals, and breastfeeding schedules in real time. Companies such as Bloomlife provide digital maternity care and contraction monitoring tools that reduce dependence on repeated clinic visits.

Menstrual health is expected to be the fastest-growing segment, as millions of women experience cycle-related symptoms and disorders that often remain undiagnosed for years. Conditions such as endometriosis and PCOS frequently require long-term symptom monitoring, making digital tracking tools highly valuable. According to studies published by the WHO, menstrual health awareness remains inadequate in several regions, increasing dependence on self-monitoring technologies. Femtech platforms are addressing this gap through cycle prediction, pain tracking, hormone monitoring, and educational support.

Regional Insights

North America Femtech Market Trends

North America is expected to be the leading market with a share of around 42.7% in 2026. The region is a hub of superior venture capital activities, novel digital healthcare infrastructure, and high consumer awareness around women’s health. The U.S. and Canada have seen steady adoption of AI-based fertility tracking, telehealth platforms, and connected wearable devices.

The region also benefits from strong employer-sponsored women’s healthcare programs covering fertility, menopause, and maternity care. According to a recent study, North America accounted for over one-third of global femtech ventures in 2024, reflecting its mature start-up culture. The Bay Area alone has seen femtech-related venture deals increase by 2.5 times since 2020, showcasing surging investor confidence in women-focused health innovation.

U.S. Femtech Market Trends

The U.S. remains the central force in femtech due to the presence of leading start-ups, prominent funding networks, and rising public awareness around women’s healthcare gaps. Companies such as Maven Clinic, Flo Health, and Willow are expanding services in fertility, menopause, postpartum care, and AI-backed reproductive health monitoring.

California and New York continue to attract key femtech investments, mainly in diagnostics and digital care platforms. The country is also seeing rising federal support for women’s health innovation, including grants for maternal and reproductive healthcare technologies. However, concerns around data privacy and clinical validation are influencing regulatory discussions around femtech apps and AI-based recommendations.

Asia Pacific Femtech Market Trends

Asia Pacific is anticipated to be the fastest-growing market over the forecast period, owing to rising smartphone penetration, increasing awareness of reproductive health, and government-backed digital healthcare expansion. Countries such as China, Japan, India, and South Korea are witnessing increasing adoption of menstrual tracking apps, fertility platforms, and wearable monitoring devices.

The region is also experiencing high demand for affordable telehealth solutions as access to specialized women’s healthcare remains uneven in multiple areas. Asia Pacific has become one of the most active regions for femtech diagnostics funding, especially in AI-enabled medical diagnostics and preventive healthcare technologies.

Japan Femtech Market Trends

Japan’s market is evolving around workplace wellness, menstrual health, and fertility support technologies. The country has seen rising corporate interest in supporting women’s health through employer-led wellness programs and femtech partnerships. Local companies are introducing menstrual leave management tools, cycle tracking apps, and fertility assistance platforms.

Awareness, however, remains relatively low compared to Western countries. A new report stated that over 78% of women in Japan were unfamiliar with the term femtech as of 2023. It indicates that the market still has significant awareness-building potential despite constant developments.

China Femtech Market Trends

China is maintaining a steady growth through large-scale digital healthcare adoption and domestic development in AI-backed health platforms. The country’s superior e-commerce networks and mobile healthcare infrastructure allow femtech services to expand swiftly across urban populations. Domestic start-ups are now focusing on fertility management, online gynecology consultations, and hormone monitoring solutions integrated with super-app ecosystems.

The government’s broad push toward digital healthcare modernization is further helping women’s health platforms expand beyond key cities. Local companies are mainly emphasizing affordable digital consultations and preventive healthcare services to reach young consumers.

Europe Femtech Market Trends

Europe remains a significant femtech region due to strong healthcare infrastructure, supportive digital health policies, and rising public awareness around reproductive and hormonal health. The region has seen increasing focus on underserved areas such as menopause care, pelvic health, and fertility diagnostics. Local femtech start-ups are also benefiting from government-backed healthcare innovation programs and sustainability-focused healthcare policies.

U.K. Femtech Market Trends

The U.K. has emerged as one of Europe’s most prominent markets due to high start-up activity and increasing investor attention toward women’s health technologies. London-based Flo Health became Europe’s first femtech unicorn, pointing toward the ongoing expansion of the sector. The country is also home to companies such as Hertility Health, which focuses on at-home fertility and hormone testing. Despite this progress, U.K.-based start-ups continue to face funding bias challenges, mainly for women-led companies seeking large-scale investments.

Germany Femtech Market Trends

Germany is remaining competitive by focusing on clinically validated diagnostics, wearable technologies, and precision healthcare platforms. Start-ups are integrating AI into reproductive diagnostics, hormone monitoring, and preventive women’s healthcare solutions. The country’s novel medical technology and engineering base gives local firms an advantage in developing medically regulated femtech products rather than purely wellness-focused apps. A few companies are also collaborating with hospitals and research institutions to improve clinical credibility. It is becoming a key differentiator as regulatory scrutiny around women’s health technologies increases across Europe.

Competitive Landscape

The global femtech market is highly fragmented but constantly evolving. It has a mix of digital health start-ups, medical device firms, fertility platforms, and large healthcare technology companies. Competition is spread across areas such as fertility care, menstrual tracking, menopause management, maternal health, pelvic care, and AI-supported diagnostics. Companies that can provide medical-grade diagnostics, regulatory approvals, and healthcare integration are gaining strong market positions.

Teal Health, for instance, gained attention after receiving U.S. Food and Drug Administration (FDA) authorization for its at-home cervical cancer screening technology, which demonstrated 96% accuracy in clinical studies. AI-supported prenatal imaging company Sonio also strengthened its position after being acquired by Samsung to extend its unique pregnancy diagnostics capabilities. A few firms are competing through predictive analytics, hormone tracking algorithms, virtual care platforms, and personalized healthcare recommendations.

Key Industry Developments:

- In May 2026, UNICEF activated a five-year catalytic investment platform (2025-2030), the first cohort of UNICEF Femtech Ventures. It is supported by the Government of Sweden and the Temasek Foundation. Eleven start-ups were selected from Asia and Africa to apply blockchain, data science, and AI to reproductive and maternal care.

- In April 2026, Qatar Science & Technology Park, in collaboration with Merck, marked the beginning of the QSTP× Merck FemTech Accelerator. The program aims to support impact-driven solutions that improve access to care for women across different markets.

- In February 2026, Femto Technologies Inc. declared the launch of its flagship tech-enabled intimacy device, Sensera, in the U.S. It is the company’s flagship tech-enabled feminine wellness device featuring adaptive machine-learning algorithms and Smart Release System (SRS).

Companies Covered in Femtech Market

- Chiaro Technology Limited

- HeraMED

- Flo Health, Inc.

- Natural Cycles USA Corp.

- Glow, Inc.

- Allara Health

- NUVO Inc.

- Bloomlife

- Syrona Health

- Sirona Hygiene Private Limited

- Samplytics Technologies Private Limited

- iSono Health, Inc.

- Athena Feminine Technologies

Frequently Asked Questions

The global femtech market is projected to be valued at US$65.2 billion in 2026.

The femtech market is expected to reach US$116.1 billion by 2033.

Launch of wearable hormone tracking devices, investments in digital menopause care platforms, and expansion of clinically validated at-home diagnostics are the key trends.

Pregnancy and nursing care is set to be the leading application segment with nearly 32.6% of share in 2026, owing to rising employer-sponsored maternity benefits.

The femtech market is expected to grow at a CAGR of 8.6% from 2026 to 2033.

Chiaro Technology Limited, HeraMED, Flo Health, Inc., and Natural Cycles USA Corp. are a few key market players.