- Healthcare IT

- Telemedicine Market

Telemedicine Market Size, Share, and Growth Forecast 2026 - 2033

Telemedicine Market by Component (Product, Services), by Mode of Delivery (Web/Cloud-based Delivery, On-Premises Delivery), Application (Tele-radiology, Tele-pathology, Tele-dermatology, Tele-consultation, Tele-cardiology, Others), End-user (Providers, Payers, Patients, Others), and Regional Analysis, 2026 - 2033

Telemedicine Market Size and Trend Analysis

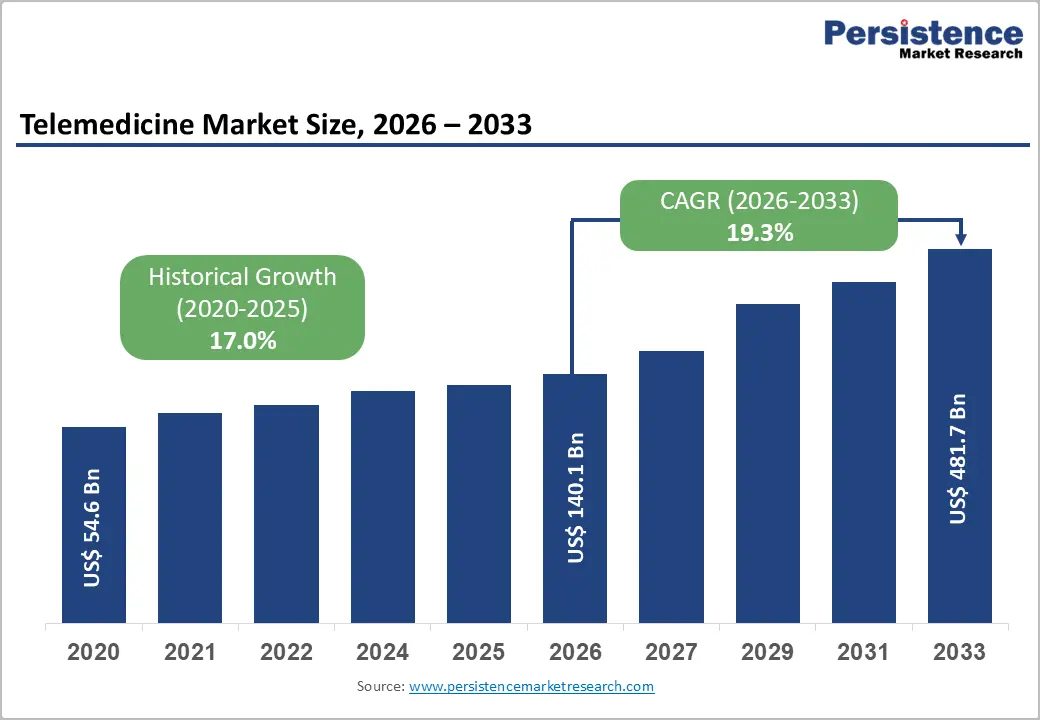

The global telemedicine market size is expected to be valued at US$ 140.1 billion in 2026 and projected to reach US$ 481.7 billion by 2033, growing at a CAGR of 19.3% between 2026 and 2033. This exceptional growth trajectory is driven by shifts in global healthcare delivery, including the rise in adoption of virtual care models post-COVID-19, rapid proliferation of smartphone and broadband connectivity, and strong policy support from governments and regulatory bodies worldwide.

The World Health Organization (WHO) has actively promoted telehealth as an essential pillar of universal health coverage. Simultaneously, growing physician shortages particularly in rural and underserved areas are amplifying institutional reliance on telemedicine platforms for efficient, scalable patient care delivery across all healthcare settings.

Key Industry Highlights

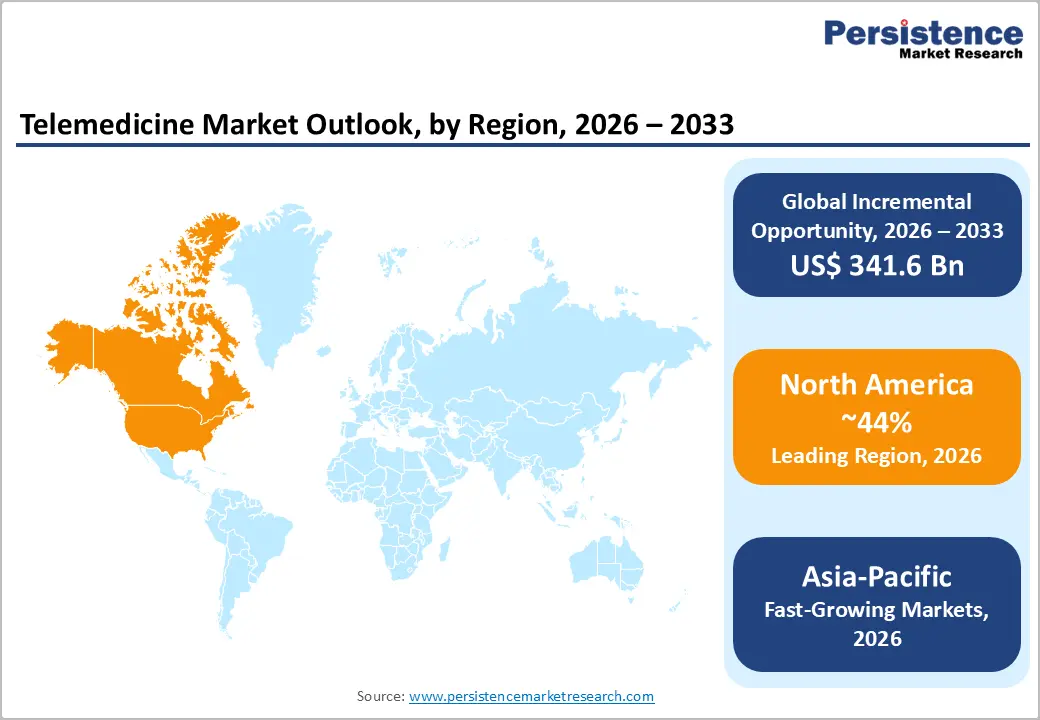

- Leading Region: North America leads the global telemedicine market with approximately 44% share in 2025, supported by CMS reimbursement expansions, a dense ecosystem of platform innovators, and high virtual care adoption post-COVID-19.

- Fastest Growing Region: Asia Pacific is the fastest-growing telemedicine region, driven by China's internet hospital network, India's eSanjeevani platform exceeding 100 million consultations, and rapid mobile health adoption across ASEAN economies.

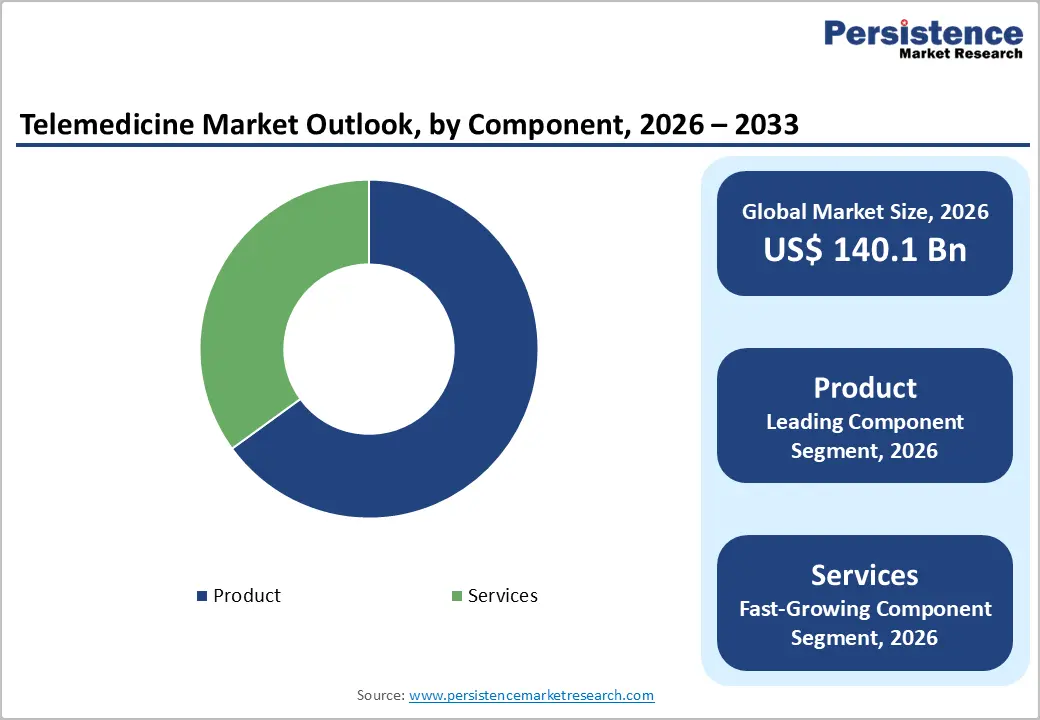

- Dominant Segment: The Product component segment dominates with approximately 65% share in 2025, underpinned by high institutional spending on telehealth hardware, EHR-integrated software platforms, and connected diagnostic devices.

- Fastest Growing Segment: The Services segment, including tele-consulting, tele-monitoring, and tele-education is the fastest growing, fueled by AI-driven remote patient monitoring adoption and permanent CMS reimbursement for telehealth services.

- Key Opportunity: AI-powered cloud-based telemedicine platforms integrated with remote patient monitoring represent the highest growth opportunity, enabling scalable virtual care delivery across provider, payer, and patient segments globally.

Market Dynamics

Drivers - Post-Pandemic Normalization of Virtual Care and Regulatory Tailwinds

The COVID-19 pandemic served as a pivotal inflection point for telemedicine adoption, compressing years of behavioral and institutional change into months. In the U.S., the Centers for Medicare & Medicaid Services (CMS) expanded telehealth reimbursement under emergency provisions, and subsequent legislation, including the Consolidated Appropriations Act, 2023 extended these flexibilities through 2024. According to the U.S. Department of Health and Human Services (HHS), telehealth utilization reached 38 times pre-pandemic levels at peak adoption.

With permanent reimbursement reforms progressing across multiple countries, the structural shift toward virtual-first care models is now embedded in mainstream healthcare delivery, sustaining high demand for telemedicine platforms, hardware, and services globally.

Restraints - Data Privacy, Cybersecurity Risks, and Regulatory Fragmentation

Telemedicine platforms handle highly sensitive patient health information, making them prime targets for cyberattacks. The U.S. Department of Health and Human Services (HHS) reported a 93% increase in large healthcare data breaches between 2018 and 2022. Regulatory requirements such as HIPAA in the U.S. and GDPR in Europe impose significant compliance obligations. Furthermore, inconsistent cross-border regulatory frameworks for telemedicine licensure and data localization create operational complexity for multinational platform providers, hindering market scalability and increasing compliance costs across geographies.

Opportunities - Expansion of AI-Powered Tele-Diagnostics and Remote Patient Monitoring Services

Artificial intelligence is transforming telemedicine from a simple consultation channel into a comprehensive remote diagnostic ecosystem. AI-driven tools for tele-radiology, tele-dermatology, and tele-cardiology are enabling faster and more accurate diagnoses without physical patient presence. The U.S. FDA had authorized over 950 AI/ML-enabled medical devices by 2023, many of which are integrated into telehealth workflows. Remote patient monitoring (RPM) is a particularly high-growth services sub-segment; CMS established dedicated reimbursement codes for RPM in 2019 and expanded coverage subsequently.

Companies developing AI-embedded telemedicine platforms with tele-monitoring capabilities are positioned to capture disproportionate market share as healthcare systems seek cost-efficient, data-driven care models.

Category-wise Analysis

Component Insights

The product segment leads the component category, commanding approximately 65% of the total telemedicine market share in 2025. This dominance is driven by sustained investment in telehealth hardware infrastructure, including video conferencing systems, remote monitoring devices, medical imaging equipment, and diagnostic peripherals, as well as proprietary software platforms and electronic health record (EHR) integrations. Healthcare facilities and provider networks must continually upgrade their technology stacks to meet expanding virtual care demands.

The Office of the National Coordinator for Health Information Technology (ONC) reports that 96% of U.S. non-federal acute care hospitals had adopted certified EHR systems as of recent years, creating a large installed base for complementary telemedicine product integration.

Mode of Delivery Insights

Web/Cloud-based Delivery is the leading mode of delivery in the telemedicine market, accounting for approximately 72% of total market share in 2025. The cloud model's dominance is attributed to its lower upfront infrastructure cost, rapid deployment capability, and seamless integration with existing hospital information systems and mobile health applications. Cloud platforms support multi-device access, enabling both synchronous video consultations and asynchronous store-and-forward services, which is critical across diverse healthcare settings.

Post-pandemic, the urgency to deploy scalable telehealth solutions rapidly accelerated cloud adoption. Major cloud hyperscalers, including Microsoft Azure, Amazon Web Services (AWS), and Google Cloud, have developed dedicated HIPAA-compliant healthcare cloud environments, further validating cloud-based deployment as the standard for enterprise telemedicine infrastructure.

Regional Insights

North America Telemedicine Market Trends and Insights

North America dominates the telemedicine market due to mature reimbursement frameworks, high digital health penetration, and strong provider adoption. The region benefits from widespread EHR integration and favorable policy support, particularly post-pandemic. The U.S. Census Bureau highlights that over 90% of households have internet access, enabling large-scale virtual care delivery. Additionally, the CDC reported a sharp rise in telehealth utilization, with millions of weekly visits during peak periods. North America maintains leadership through advanced infrastructure, payer support, and continuous innovation in remote monitoring and AI-based care delivery.

U.S. Telemedicine Market Trends and Insights

The U.S. leads the region due to strong reimbursement systems and large-scale adoption across hospitals and insurers. According to the CDC, telehealth usage increased 38 times compared to pre-pandemic levels, reflecting structural adoption. Over 75% of hospitals in the country use telemedicine systems, supported by Medicare expansion and private payer coverage. The U.S. telemedicine market is likely to surpass US$ 65 billion in 2026, driven by chronic disease burden and integration of remote patient monitoring into mainstream care delivery systems.

Canada Telemedicine Market Trends and Insights

Canada is the fastest-growing country due to strong government-led virtual care expansion and rural healthcare demand. The Canadian Institute for Health Information reported that over one-third of healthcare interactions shifted to virtual platforms during recent years. Investments in telehealth infrastructure and digital health funding continue to accelerate adoption. Canada’s telemedicine market is expected to grow at a 22-24% CAGR, supported by physician shortages, long wait times, and increasing reliance on virtual consultations across primary and specialist care.

Europe Telemedicine Market Trends and Insights

Europe is a key region due to strong public healthcare systems and regulatory-driven digital health adoption. The European Commission reports that over 70% of EU countries have implemented telemedicine services within national healthcare frameworks. The rising aging population over 21% aged 65+ in EU, is driving demand for remote care solutions. With increasing healthcare costs and workforce shortages, telemedicine is becoming essential for efficiency. Within the US$ 140.1 Bn global market (2026), Europe maintains a significant share due to policy-backed expansion, interoperability initiatives, and growing acceptance of digital consultations across primary and specialist care.

Germany Telemedicine Market Trends and Insights

Germany leads Europe due to strong regulatory support such as the Digital Healthcare Act (DVG), enabling reimbursement for digital health applications. Statutory health insurance covers teleconsultations and driving physician adoption. The country has seen a rapid uptake of e-prescriptions and virtual consultations. Germany’s telemedicine market is expected to reach US$ 12-15 Bn by 2026, supported by nationwide digitization initiatives, high healthcare spending, and integration of telehealth into outpatient and chronic care management systems.

UK Telemedicine Market Trends and Insights

The UK is the fastest-growing market, driven by NHS-led digital transformation. According to NHS data, over 30-35% of GP consultations are conducted remotely, indicating strong adoption. Government strategies focusing on reducing waiting times and improving access continue to boost telehealth demand. The UK telemedicine market is expected to grow at a 20-22% CAGR, supported by digital-first primary care models, mobile health adoption, and expansion of virtual mental health services.

Asia Pacific Telemedicine Market Trends and Insights

Asia Pacific is the fastest-growing region due to a large population base, rising smartphone penetration, and increasing healthcare access gaps. The International Telecommunication Union reports that internet penetration in Asia Pacific exceeds 64%, creating a strong foundation for telemedicine expansion. Governments across China, India, and Japan are investing heavily in digital health ecosystems. Asia Pacific is accelerating rapidly due to unmet demand, cost-sensitive populations, and rapid adoption of mobile-based healthcare services.

China Telemedicine Market Trends and Insights

China leads the region due to large-scale digital health platforms and strong government support for “internet hospitals.” The country has over 1 billion internet users, enabling widespread telemedicine adoption. Online healthcare platforms handle millions of consultations annually, supported by AI integration and hospital digitization. Therefore, China’s telemedicine market is expected to reach US$ 30 billion by 2026, mainly driven by urban-rural healthcare disparities and expansion of digital consultation platforms.

India Telemedicine Market Trends and Insights

India is the fastest-growing telemedicine market due to expanding digital infrastructure and government initiatives like the National Digital Health Mission. According to official data, over 100 million teleconsultations have been conducted through public platforms such as eSanjeevani. Increasing smartphone penetration and doctor shortages in rural areas are key drivers. India’s telemedicine market is expected to grow at a 25% CAGR, supported by policy support, affordability, and rising awareness of virtual healthcare services.

Competitive Landscape

The global telemedicine market is moderately fragmented, characterized by a mix of large integrated platform providers, specialist telehealth companies, and regional players. Teladoc Health, American Well (Amwell), and MDLIVE lead in North America through broad service portfolios and payer partnerships. Key competitive differentiators include AI-driven diagnostic integration, specialty telehealth coverage, EHR interoperability, and mobile-first platform design. Strategic acquisitions such as Teladoc's acquisition of Livongo reflect consolidation trends. Emerging business models include employer-sponsored virtual care benefits, subscription-based direct-to-consumer platforms, and B2B white-label telehealth solutions for hospital networks.

Key Developments:

- March 2025: UniDoc Health Corp. announced that it had entered into a purchase agreement to acquire the AGNES Connect software from AMD Telemedicine. The agreement marked a strategic step for UniDoc to strengthen its telehealth capabilities by integrating a widely used clinical communication and device integration platform into its ecosystem.

- January 2025: Amwell announced that it had divested its virtual psychiatric care business to Avel eCare through an all-cash transaction. The move reflected Amwell’s strategic decision to streamline its portfolio and focus more on its core digital health platform and enterprise telehealth solutions.

Telemedicine Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 54.6 Billion |

| Projected Market Value (2026) | US$ 140.1 Billion |

| Projected Market Value (2033) | US$ 481.7 Billion |

| CAGR (2026 - 2033) | 19.3% |

| Leading Region | North America, 44% share |

| Dominant Component | Product, 65% share |

| Top-ranking Mode of Delivery | Web/Cloud-based Delivery, 83% share |

| Incremental Opportunity | US$ 341.7 billion |

Companies Covered in Telemedicine Market

- Babylon

- CareClix

- Global Telehealth Services

- AMD Global Medicine

- Tele-Med International

- American well

- Doctor on Demand, Inc.

- MD International AB

- Encounter Telehealth

- MDLIVE, Inc.

- Teladoc Health, Inc.

- MeMD

- Global Med

- SnapMD

- AMC Health

- Others

Frequently Asked Questions

The global telemedicine market is estimated to reach US$ 140.1 billion in 2026.

Rising chronic diseases, digital adoption, cost efficiency, remote access needs, aging population, and provider shortages

North America is the leading region with approximately 44% of total market share in 2025.

Expansion in rural healthcare access, AI integration, remote monitoring, emerging markets, and personalized virtual care solutions.

Babylon, CareClix, Global Telehealth Services, AMD Global Medicine, Tele-Med International, American well.