- Beverages

- Diet Soft Drinks Market

Diet Soft Drinks Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Diet Soft Drinks Market by Product Type (Carbonates, Dilutables, Flavored Water, Still and Juice Drinks, Sports and Energy Drinks, Fruit Juice), by Flavor (Natural, Artificial), by Distribution Channel (HoReCa, Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, Others), Regional Analysis, 2026 - 2033

Diet Soft Drinks Market Share and Trends Analysis

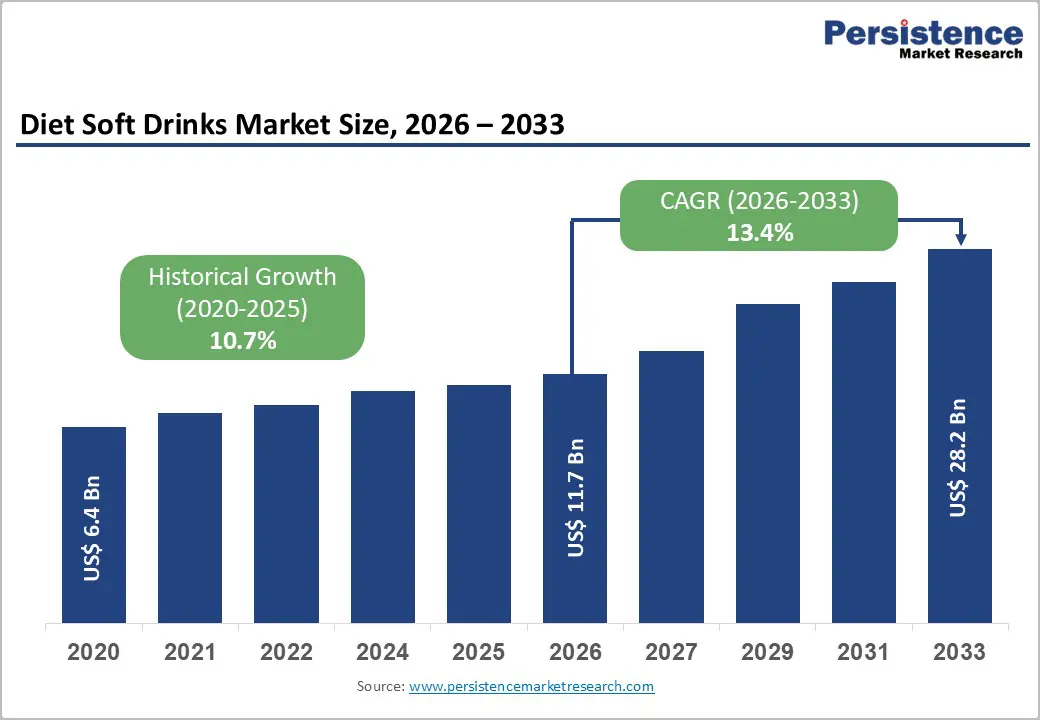

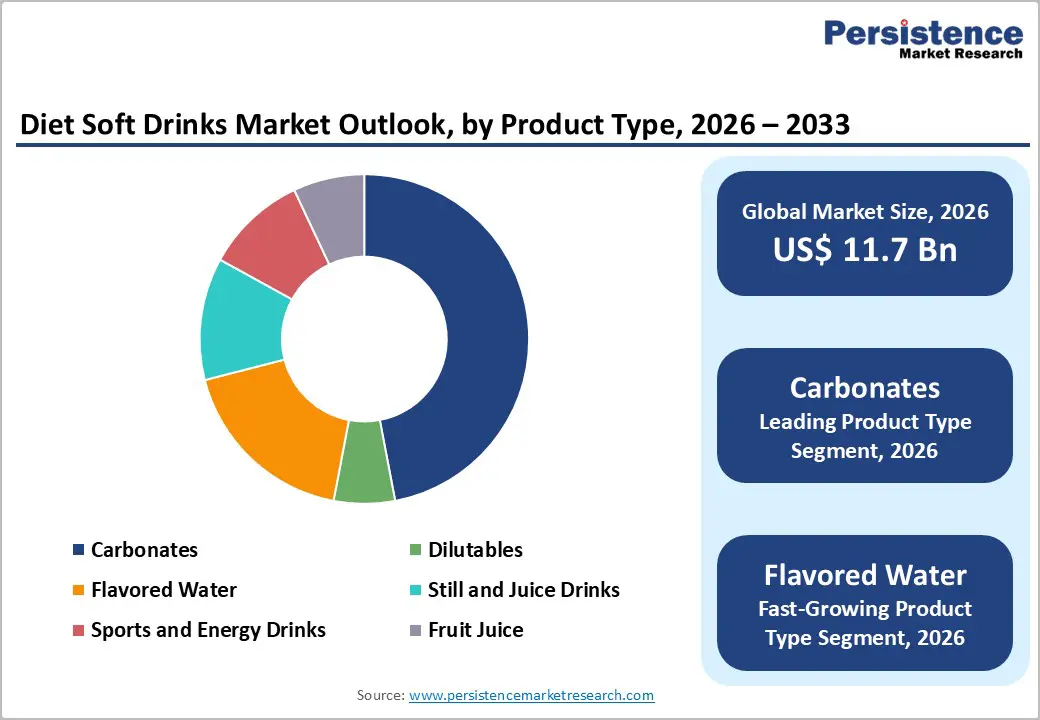

The global diet soft drinks market is estimated to grow from US$ 11.7 billion in 2026 to US$ 28.2 billion by 2033. The market is projected to record a CAGR of 13.4% during the forecast period from 2026 to 2033.

The market is primarily propelled by a rise in global obesity rates, with the World Health Organization (WHO) reporting that 1 in 8 people worldwide were living with obesity as of 2022, which is steering consumers toward low-calorie and zero-sugar beverage alternatives.

Regulatory momentum, including sugar-sweetened beverage (SSB) taxes enacted across more than 50 countries globally, is further accelerating the structural shift toward diet formulations. Simultaneously, rapid innovation in natural sweeteners such as stevia and monk fruit, combined with rising health awareness among Millennials and Gen Z, is sustaining robust demand growth across both developed and emerging economies.

Key Industry Highlights:

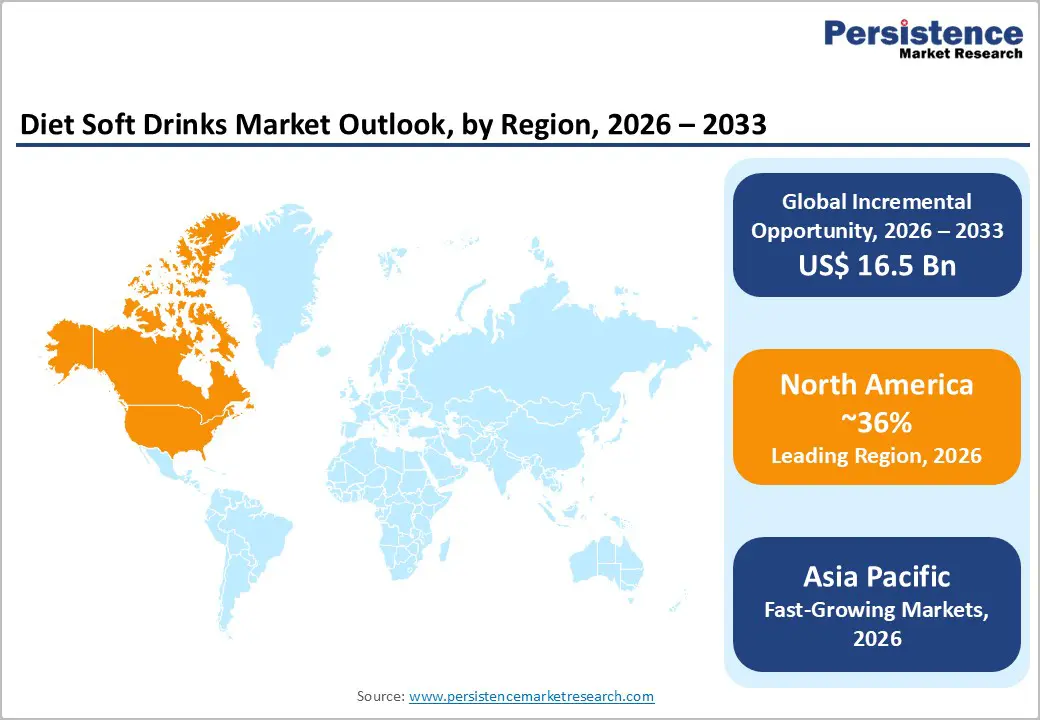

- Leading Region: North America leads with 36% share (2025), driven by a mature beverage ecosystem, strong regulatory support, and high adoption of low- and zero-sugar formulations.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, supported by urbanization, rising disposable incomes, and increasing prevalence of Diabetes driving demand for diet beverages.

- Leading Product Type: Carbonates dominate with 47% share (2025), backed by strong brand loyalty, extensive global distribution, and continuous innovation from The Coca-Cola Company and PepsiCo, Inc.

- Fastest Growing Distribution Channel: Online retail is witnessing the highest growth, fueled by rapid e-commerce expansion, convenience, and improved last-mile delivery capabilities.

- Growth Indicator: Rising global obesity and diabetes prevalence is accelerating demand for low-calorie and sugar-free beverage alternatives.

- Key Opportunity: Flavored water expansion and natural sweetener innovation are creating strong growth potential, aligning with clean-label, functional, and hydration-focused consumer trends.

Market Dynamics

Driver: Rising Health Consciousness and Obesity-Driven Demand for Low-Calorie Beverages

Surging global health consciousness represents the foremost growth catalyst for the diet soft drinks market. According to the World Health Organization (WHO), over 2.5 billion adults were overweight in 2022, of whom 890 million were living with obesity a figure that has more than doubled since 1990. Simultaneously, the National Institutes of Health (NIH) reported that 38.4 million Americans, approximately 11.6% of the U.S. population, were living with diabetes in 2021, creating a substantial consumer base actively seeking sugar-free alternatives. These epidemiological trends have driven mainstream adoption of diet carbonated drinks, zero-sugar sodas, and flavored low-calorie waters among health-aware shoppers.

Leading brands, including The Coca-Cola Company and PepsiCo, Inc. have responded with aggressive zero-sugar portfolio expansions, reflecting the tangible commercial dividends that health-driven demand is generating. Pepsi Zero Sugar achieved an exceptional 30.8% year-to-date sales growth in 2025, underscoring how deeply this demand driver is reshaping purchasing behavior.

Restraint: Regulatory Scrutiny and Consumer Skepticism Over Artificial Sweeteners

Despite strong demand fundamentals, the diet soft drinks market faces significant headwinds from evolving regulatory assessments of artificial sweeteners. The World Health Organization (WHO) and the European Food Safety Authority (EFSA) regularly re-evaluate the safety profiles of sweeteners including aspartame, saccharin, and sucralose. In 2023, the WHO categorized aspartame as a "possibly carcinogenic to humans" (Group 2B) substance, triggering widespread media coverage that adversely influenced consumer sentiment.

Such regulatory pronouncements amplify public skepticism, potentially depressing sales and intensifying labeling complexity for manufacturers. Companies face mounting compliance costs when reformulating products to replace questioned ingredients, which can dampen the pace of innovation and erode margins, particularly for smaller market participants.

Opportunity: Flavored Water and Natural Sweetener Innovation as Growth Accelerators

The surging consumer preference for clean-label, plant-derived ingredients is creating a transformative opportunity for diet soft drink manufacturers. Natural sweeteners such as stevia, monk fruit, and allulose are rapidly gaining commercial traction as credible alternatives to aspartame and saccharin, addressing both regulatory risk and consumer perception challenges simultaneously. Persistence Market Research notes that the natural flavors segment within diet soft drinks is projected to record a CAGR of 9.6% through the forecast period.

The flavored water sub-segment is emerging as the fastest-growing category within the broader diet soft drinks market, supported by rising hydration awareness, with 67% of global consumers recognizing the link between hydration and overall health, per a Persistence Market Research 2025 survey. Companies that invest in stevia-forward formulations, botanical infusions, and functional add-ons such as vitamins, probiotics, and electrolytes will be best positioned to capitalize on the convergence of health, taste, and transparency that next-generation consumers demand.

Category-wise Analysis

By Product Type, carbonates dominate the global diet soft drinks market

Carbonates represent the dominant segment within the diet soft drinks market by product type, commanding approximately 47% of the total market share in 2025. This leadership is firmly anchored in decades of consumer brand loyalty, extensive global distribution, and continuous innovation by the world's largest beverage corporations. The Coca-Cola Company and PepsiCo, Inc. have invested heavily in expanding zero-sugar and diet carbonated variants: Coca-Cola introduced multiple new zero-sugar SKUs in January 2024, launched the Fanta Zero line in February 2025, and Pepsi Zero Sugar achieved over 30.8% year-to-date sales growth in 2025.

The carbonated segment benefits from unmatched retail shelf presence, aggressive promotional activity, and increasing adoption in foodservice and convenience channels globally. High consumption rates in North America and growing market penetration in the Asia Pacific continue to reinforce carbonates as the segment of choice for health-conscious consumers seeking familiar taste profiles without caloric burden.

By Distribution Channel, online retail is expected to show promising growth

Online retail is emerging as a high-growth distribution channel in the global diet soft drinks market, driven by rapid digitalization and shifting consumer purchasing behavior. Increasing preference for convenience, doorstep delivery, and access to a wider variety of products is encouraging consumers to purchase beverages through e-commerce platforms. According to the International Trade Administration, global B2C e-commerce revenue is projected to reach USD 5.5 trillion by 2027, expanding at a CAGR of 14.4%, with food and beverages among the leading segments. This growth is directly supporting the expansion of online beverage sales.

Additionally, digital platforms enable brands to showcase diverse diet soft drink portfolios, including zero-sugar, functional, and flavored variants, while offering subscription models and personalized promotions. The rise of quick-commerce and improved cold-chain logistics further enhances product accessibility and delivery efficiency. As consumers increasingly prioritize convenience and product variety, online retail is set to become a key growth driver in the evolving diet soft drinks market.

Regional Insights

North America Diet Soft Drinks Market Trends

North America leads the global diet soft drinks market, holding approximately 36% of the total market share in 2025, supported by a mature beverage ecosystem and strong consumer shift toward low- and zero-sugar formulations. Regulatory support, including updated labeling standards and dietary guidelines, is accelerating reformulation across major brands. High disposable incomes and widespread retail penetration further strengthen demand. Innovation in functional beverages, including prebiotic and fortified drinks, is expanding category boundaries. The region’s focus on clean-label ingredients and health-driven consumption continues to reinforce its leadership.

- U.S. Diet Soft Drinks Market Trends

The U.S. dominates the regional market, driven by rising awareness of metabolic health and strong demand for sugar-free beverages. Companies like Keurig Dr Pepper have rapidly expanded zero-sugar portfolios, reflecting aggressive product innovation. Policy frameworks from the U.S. Food and Drug Administration and dietary recommendations are pushing manufacturers toward transparency and reformulation. Additionally, growing interest in functional beverages, such as prebiotic sodas introduced by The Coca-Cola Company, is reshaping consumer preferences.

Canada Diet Soft Drinks Market Trends

Canada is witnessing rapid growth, supported by increasing health consciousness and regulatory alignment with clean-label standards. Consumers are actively reducing sugar intake, driving demand for diet and zero-calorie beverages across carbonated and non-carbonated segments. Retail expansion and e-commerce penetration are improving product accessibility nationwide. Additionally, demand for natural sweeteners and functional drink options is rising, encouraging innovation among both domestic and international beverage brands.

Asia Pacific Diet Soft Drinks Market Trends

Asia Pacific is the fastest-growing market for diet soft drinks, driven by rapid urbanization, rising disposable incomes, and increasing awareness of lifestyle-related health conditions such as Diabetes. A growing middle-class population is shifting toward low-calorie and functional beverages, supported by expanding retail infrastructure and strong e-commerce penetration. Multinational players like The Coca-Cola Company and PepsiCo, Inc. are accelerating investments in no-sugar variants across key markets, while Southeast Asia is witnessing rising adoption due to evolving consumer lifestyles and Westernized consumption patterns.

- China Diet Soft Drinks Market Trends

China dominates the regional market in both production and consumption, supported by its large urban population and increasing health awareness. Consumers are increasingly opting for diet variants as part of broader wellness trends, particularly in tier-1 and tier-2 cities. E-commerce platforms play a crucial role in distribution, enabling premium access and imported diet beverages while supporting rapid product innovation and market penetration.

- India Diet Soft Drinks Market Trends

India represents one of the fastest-growing markets, driven by rising health consciousness and a high burden of Diabetes, affecting over 77 million adults. Government-backed initiatives promoting reduced sugar consumption are influencing consumer preferences toward diet beverages. Major companies are expanding zero-sugar portfolios to capture demand, intensifying competition with domestic brands. Increasing urbanization, expanding retail channels, and rising acceptance of functional and low-calorie drinks are positioning India as a key growth engine in the region.

Competitive Landscape

The global diet soft drinks market is moderately consolidated, with The Coca-Cola Company and PepsiCo, Inc. collectively commanding the majority of global revenue share through dominant zero-sugar brand portfolios, extensive distribution networks spanning over 200 countries, and billion-dollar marketing investments. Key competitive differentiators include natural sweetener technology, sustainable packaging credentials, and functional ingredient integration. The competitive frontier is being actively contested by challenger brands in the prebiotic soda segment and regional players across Asia Pacific and Latin America.

Market leaders are pursuing inorganic growth strategies exemplified by PepsiCo's acquisition of Poppi in 2025, alongside continuous R&D investment in next-generation sweetener systems and personalized beverage formulations to defend and extend their competitive moats.

Key Industry Developments:

- In February 2026, The Coca-Cola Company relaunched Diet Coke Cherry in U.S. with refreshed branding, zero sugar formulation, and updated cherry-focused packaging, available in cans and bottles.

- In January 2026, BLU Energy Drink announced the full-scale launch of its brand and product lineup in the United States, including a Zero Sugar variant targeting health-conscious energy drink consumers.

- In December 2025, Celsius Holdings, Inc. introduced four new zero-sugar, fruit-forward flavors across the UK and Ireland, expanding its portfolio in line with growing demand for healthier energy beverages.

- In March 2025, PepsiCo, Inc. acquired prebiotic soda brand Poppi to strengthen its position in the functional low-calorie beverage segment.

Diet Soft Drinks Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 5.9 Bn |

| Projected Market Value (2026) | US$ 11.7 Bn |

| Projected Market Value (2033) | US$ 28.2 Bn |

| CAGR (2026 - 2033) | 13.4% |

| Leading Region | North America, 36% share |

| Dominant Product Type | Carbonates, 47% share |

| Top-ranking Flavor | Natural, 62% share |

| Incremental Opportunity | US$ 16.5 Bn |

Companies Covered in Diet Soft Drinks Market

- The Coca-Cola Company

- PepsiCo, Inc.

- Keurig Dr Pepper

- Nestlé S.A.

- National Beverage Corp.

- Red Bull GmbH

- Monster Beverage Corporation

- Asahi Group Holdings Ltd.

- Britvic plc

- Suntory Beverage and Food Limited

- Danone S.A.

- The Kraft Heinz Company

- Unilever

- Jones Soda Co.

- Others

Frequently Asked Questions

The global Diet Soft Drinks market is projected to be valued at US$ 11.7 Bn in 2026.

Rising Health Consciousness and Obesity-Driven Demand for Low-Calorie Beverages is driving the global Diet Soft Drinks market.

The global Diet Soft Drinks market is poised to witness a CAGR of 13.4% between 2026 and 2033.

Flavored water expansion and natural sweetener innovation are emerging as key growth opportunities in the global diet soft drinks market.

The Coca-Cola Company, PepsiCo, Inc., Keurig Dr Pepper, Nestlé S.A., National Beverage Corp., Red Bull GmbH, Monster Beverage Corporation, Danone S.A., and The Kraft Heinz Company.