- Home Care & Utilities

- Bedroom Furniture Market

Bedroom Furniture Market Size, Share, and Growth Forecast 2026 - 2033

Bedroom Furniture Market by Product Type (Beds; Wardrobes & Closets; Dressers & Mirrors; Mattresses; Others), Material Type (Wood, Metal, Glass, Plastic, Upholstered), Category (New, Refurbished/Second-hand), Distribution Channel (Specialty Furniture Stores, Multi-brand Outlets, Carpenter Shops, Company-owned Websites, E-commerce), End-user (Residential, Commercial), by Regional Analysis, 2026 - 2033

Bedroom Furniture Market Size and Trend Analysis

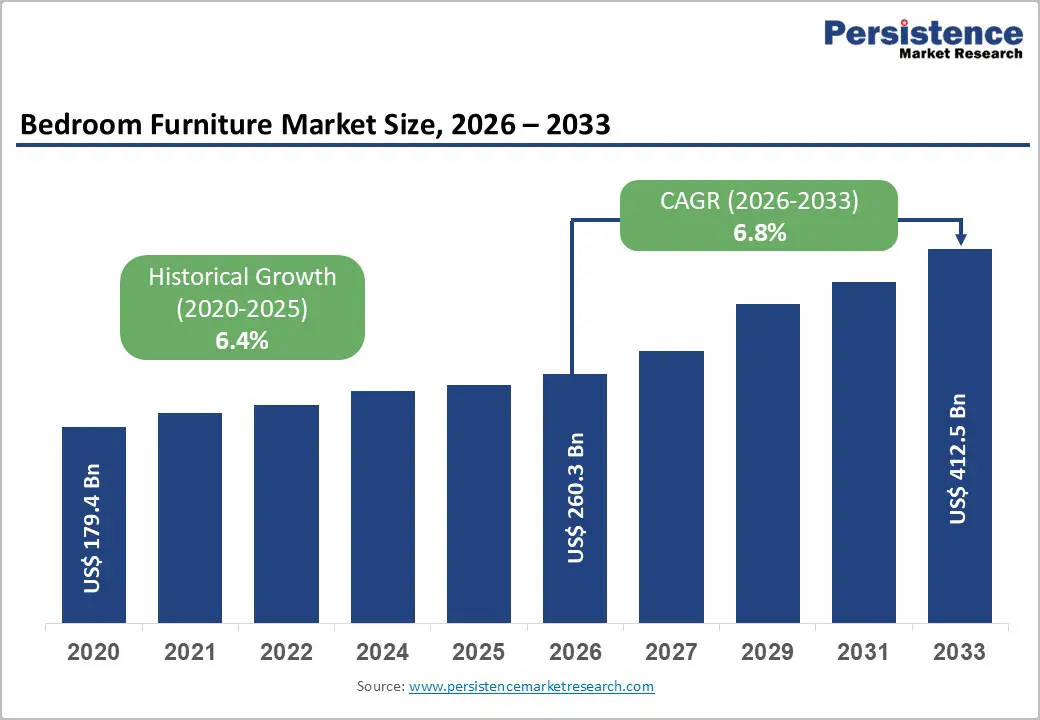

The global bedroom furniture market size is expected to be valued at US$ 260.3 billion in 2026 and projected to reach US$ 412.5 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033.

Growth in the bedroom furniture market is driven by rapid urbanization and new household formation in Asia Pacific and the Middle East, rising premiumization among global middle-class consumers, and the shift toward e-commerce and brand-owned digital channels expanding market reach. The market grew from US$ 179.4 billion in 2020 at a 6.4% CAGR, supported by post-pandemic home improvement trends, work-from-home lifestyles, and expanding digital presence of major retailers in emerging markets.

Key Industry Highlights

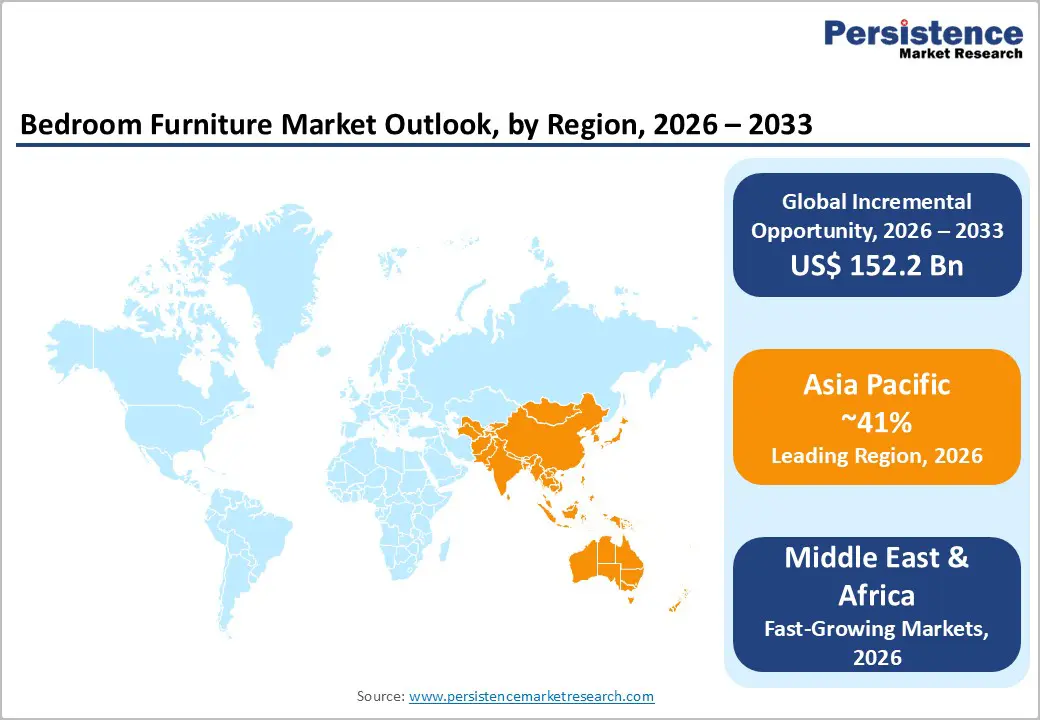

- Leading Region: Asia Pacific commands 41% global bedroom furniture market share in 2025, driven by China's 48% intra-regional dominance through urbanization-fueled first-time buyer demand, Oppein Home Group's organized retail scale, and IKEA's aggressive market expansion across the region's growing middle class.

- Fastest Growing Region: MEA is the fastest growing region at 8.5% CAGR through 2033, propelled by Gulf Vision 2030 and 2031 mega-project hospitality development, rapid urban household formation in Africa, and GCC luxury residential development generating consistent premium bedroom furniture FF&E procurement cycles.

- Dominant Product Type: Beds hold 38% product type market share in 2025, commanding an irreplaceable position as the bedroom's non-discretionary anchor purchase, sustained by the National Sleep Foundation's documentation of quality sleep investment as a health priority and upgrade cycles among existing homeowners globally.

- Fastest Growing Distribution Channel: E-commerce is the fastest growing distribution channel, with Wayfair's US$ 12B annual furniture revenue and IKEA's digital-first transformation demonstrating consumers' willingness to purchase high-consideration bedroom items online when AR visualization, free returns, and white-glove delivery eliminate traditional friction.

- Key Market Opportunity: Williams-Sonoma's 70%+ digital bedroom sales and IKEA's 45-market buy-back program signal that companies combining premium digital experience with circular economy credentials can simultaneously capture the highest-margin growth segment and the highest-volume sustainability-conscious consumer cohort through 2033.

Market Dynamics

Market Growth Drivers

Urbanization and Household Formation Creating Structural First-Time Buyer Demand

Rapid urbanization across Asia Pacific, the Middle East, and Sub-Saharan Africa is the most consequential structural driver for bedroom furniture demand, as new urban households require complete furnishing for the first time, creating a geographically concentrated and time-compressed demand wave. The United Nations Human Settlements Programme projects 2.5 billion additional urban residents by 2050, with over 90% in Asia and Africa. Large-scale housing programs in India and ongoing urbanization in China are generating millions of first-time buyers annually, each needing beds, wardrobes, and storage. This demand differs from replacement cycles in mature markets, as it is additive, volume-driven, and concentrated in price-sensitive segments that favor cost-efficient, scalable suppliers.

Premiumization of Residential Interiors and Rising Aspirational Spending on Bedroom Design

Beyond volume expansion, the bedroom furniture market is experiencing a parallel premiumization trend as globally rising incomes, particularly in the growing urban middle classes of India, Southeast Asia, and the Gulf states, translate into a higher willingness to pay for design-led, durable, and brand-name bedroom furniture. The World Bank documents consistent growth in the global middle-class population toward 5.3 billion by 2030, with aspirational spending on home interiors indexed as a primary lifestyle expenditure category. Premium bedroom furniture brands, including RH, Ethan Allen Interiors, and Williams-Sonoma have documented consistent revenue growth in premium residential furniture, driven by affluent consumers treating bedroom interiors as investments in personal lifestyle expression rather than purely functional purchases.

Restraints - Raw Material and Supply Chain Cost Volatility Compressing Manufacturer Margins

Bedroom furniture manufacturers face sustained margin pressure from the structural volatility of key inputs, timber, steel, foam, and fabric, that collectively represent 55-70% of variable production cost for most product types. Timber prices demonstrated this vulnerability clearly during the 2020-2022 period when U.S. lumber prices spiked over 300% per Random Lengths lumber market data, compressing margins for furniture manufacturers unable to pass through cost increases to price-sensitive retail customers.

For mid-market manufacturers without pricing power, particularly those serving volume retail accounts, this input cost volatility creates persistent margin compression cycles that limit capital available for R&D, digital channel investment, and geographic expansion, disadvantaging them relative to vertically integrated competitors that control upstream material supply.

Shifting Consumer Preferences Toward Sustainability Forcing Supply Chain Transformation

Growing consumer and regulatory demand for sustainably sourced and certified furniture is forcing bedroom furniture manufacturers to undertake costly supply chain transformation that smaller producers and those reliant on uncertified timber sources cannot easily absorb.

The EU Deforestation Regulation (EUDR) effective from December 2024 mandates that timber and wood-derived products, including furniture, entering the EU market must demonstrate zero-deforestation supply chain compliance, effectively requiring certification through FSC (Forest Stewardship Council) or PEFC standards. For furniture manufacturers in Southeast Asia and South Asia dependent on uncertified timber supply chains, achieving EUDR compliance represents a multi-year restructuring investment that increases procurement costs and may restrict EU market access, creating a significant competitive disadvantage versus EU-origin and certified producers.

Opportunities- E-commerce Channel Expansion: The Highest-Growth Distribution Transformation in the Market

The shift of bedroom furniture purchasing toward e-commerce and direct-to-consumer digital channels represents the most transformative and time-sensitive commercial opportunity for market participants, rewarding companies that invest in digital capabilities now while competitors remain primarily brick-and-mortar. Wayfair generated approximately US$ 12 billion in annual e-commerce furniture revenue in 2023, demonstrating that consumers will purchase high-consideration furniture items online when the experience, including 3D room visualization, free returns, and white-glove delivery, eliminates traditional friction points.

Inter IKEA Systems has prioritized e-commerce rollout as a central strategic pillar, with online sales representing a growing share of total IKEA revenue globally. In China, Tmall and JD.com furniture platforms are enabling domestic brands like Oppein Home Group to reach rural and lower-tier city consumers for the first time. Furniture companies that build integrated logistics, AR visualization, and seamless returns capabilities in the e-commerce channel can capture the highest-growth distribution opportunity in the market across all geographies through 2033.

Refurbished and Circular Economy Bedroom Furniture: Emerging Premium Opportunity

The growing consumer movement toward sustainable consumption, combined with rising furniture prices, is creating a premium refurbished and pre-owned bedroom furniture market that sophisticated brands should treat as a strategic growth channel rather than a competitive threat. The Ellen MacArthur Foundation documents consistent growth in global recommerce and circular economy product adoption across home furnishings, with platforms including Chairish, AptDeco, and IKEA's buyback and resell program demonstrating that consumers, particularly affluent millennials and Gen Z, actively seek quality pre-owned furniture as both a sustainability statement and a value proposition.

IKEA's circular initiative processed over 70,000 pre-owned items in its first year of the buyback program, indicating significant latent consumer demand. Furniture brands that establish certified refurbishment programs, offering warranty, quality grading, and delivery infrastructure for pre-owned bedroom furniture, can capture incremental revenue from the circular economy trend while building brand loyalty among the sustainability-conscious consumer cohort that will dominate long-term purchasing.

Category-wise Analysis

Product Type Insights

Beds hold the leading product position with around 38% market share in 2025, driven by their essential and non-discretionary nature across all income levels and regions. Demand spans both economy segments with basic designs and premium categories featuring adjustable and designer options. Growing awareness of sleep quality and its impact on health is encouraging higher consumer spending on sleep solutions. Additionally, when combined with mattresses, beds represent the highest-value purchase in bedroom furniture, making them the primary driver of replacement and upgrade cycles in existing households.

Material Type Insights

Wood holds the dominant material type position at approximately 52% market share in 2025, a leadership position that reflects the enduring consumer and cultural association of wood with quality, warmth, and durability across virtually all global markets from North America to Southeast Asia. The American Hardwood Export Council (AHEC) documents consistent specification of hardwood species, oak, walnut, maple, and teak, in premium bedroom furniture, while engineered wood products (MDF, plywood, particleboard) enable the mass-market accessibility of wood aesthetics at economy price points.

Wood's designability, stainable, paintable, and carvable across an enormous style range from Scandinavian minimalism to Asian traditional, means it serves design requirements across every price tier and cultural aesthetic. This material versatility makes wood the standard specification against which all alternative materials (metal, glass, upholstered) are positioned as specialty alternatives rather than mainstream replacements.

Category Insights

New bedroom furniture commands approximately 87% market share in 2025, reflecting the cultural primacy of new furniture purchase in most global markets, particularly in Asia, where first-time household formation dominates demand and the new purchase carries social significance beyond mere utility. However, the refurbished and second-hand segment is growing faster than the overall market, driven by structural forces including rising furniture prices, growing sustainability consciousness, and the maturation of online ecommerce platforms that address the trust and logistics barriers that historically suppressed pre-owned furniture adoption.

IKEA's buy-back program, the growth of Chairish and specialist premium ecommerce platforms, and the integration of second-hand furniture listings into mainstream retail environments signal that the refurbished segment will capture rising share over the forecast period.

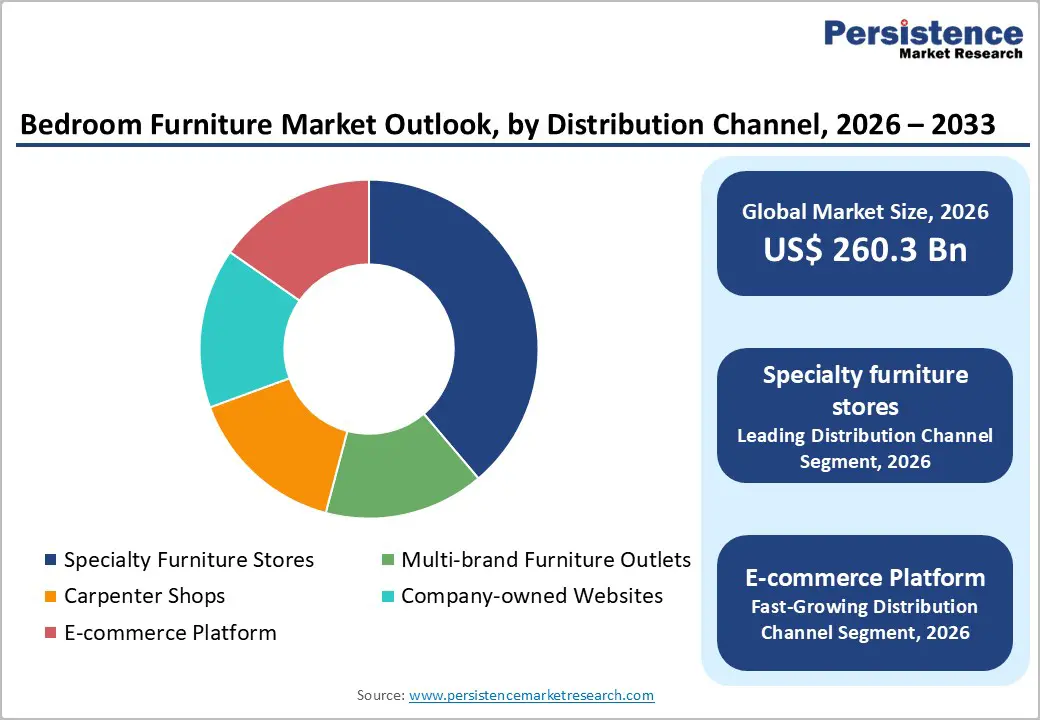

Distribution Channel Insights

Specialty furniture stores hold the leading distribution channel position at approximately 34% market share in 2025, sustained by the consumer preference for in-person evaluation of high-consideration, high-touch bedroom furniture purchases, particularly beds and mattresses where physical testing remains a critical part of the purchase decision process. Ashley Global Retail, Ethan Allen, La-Z-Boy, and Rooms to Go each operate extensive specialty retail networks precisely because consumers converting from browsing to purchasing benefit from the tactile, consultative in-store experience.

The e-commerce channel is the fastest growing distribution segment, with Wayfair and brand-owned websites gaining consistent share, but specialty stores retain a structural advantage in high-consideration categories where product quality cannot be fully assessed through digital content.

End-user Insights

Residential end use accounts for around 82% of bedroom furniture demand in 2025, driven by new housing construction, renovation and replacement cycles, and first-time household formation. Demand is closely tied to home ownership and furnishing needs. Meanwhile, the commercial segment, including hospitality and serviced housing, is growing faster due to expanding global hotel developments and large-scale, recurring procurement cycles managed by specialized buyers.

Regional Insights

North America Bedroom Furniture Market Trends and Insights

North America is a mature, premiumization-led bedroom furniture market where replacement cycles, home renovation investment, and the upgrade from mass-market to mid-premium furniture drive consistent above-average per-household spending. The Home Improvement Research Institute (HIRI) documents bedroom furniture as a consistent top-five home improvement spending category in the U.S. E-commerce disruption is reshaping the channel landscape, with Wayfair, Williams-Sonoma, and IKEA expanding digital channels that are capturing the replacement purchase cycle from traditional specialty store incumbents.

The region's forward trajectory points toward further digital channel consolidation, premium private label development, and sustainability-mandated supply chain transformation as the dominant competitive themes.

U.S. Bedroom Furniture Market Size

The United States accounts for approximately 78% of North American bedroom furniture revenue in 2025, making it the world's single largest national market for bedroom furniture by value. The U.S. Census Bureau documents over 1.4 million new housing starts annually providing a consistent first-time outfitting demand base, while HIRI confirms bedroom furniture replacement spending among existing homeowners sustains a parallel upgrade cycle. U.S. CAGR is projected at approximately 6.2% through 2033, driven by premium channel premiumization and e-commerce share gains.

Europe Bedroom Furniture Market Trends and Insights

Europe's bedroom furniture market is defined by design sophistication, sustainability compliance mandates under EUDR, and the strongest per-capita furniture spending of any major region. Inter IKEA Systems dominates volume across European markets, while premium specialist brands from Scandinavia, Italy, and the UK sustain the region's premium segment. The EU's circular economy and deforestation regulation frameworks are accelerating supply chain transformation, with FSC-certified and sustainably sourced wood becoming a de facto specification standard for European retail compliance.

The region's forward trajectory is toward premium sustainable products, circular recommerce programs, and digital channel integration at scale.

Germany Bedroom Furniture Market Size

Germany holds approximately 21% of European bedroom furniture market revenue in 2025, sustained by one of Europe's highest per-household furniture expenditure rates and a structurally robust renovation market. Germany's Destatis-documented housing renovation investment and export-oriented furniture manufacturing heritage, anchored by companies including Hülsta and Rolf Benz, make it both the region's largest demand and a significant supply market.

U.K. Bedroom Furniture Market Size

The United Kingdom represents approximately 15% of European bedroom furniture market revenue in 2025. The UK's active residential renovation market, driven by a large existing housing stock and the cultural propensity for home improvement documented by HBIS data, sustains consistent bedroom furniture replacement demand. IKEA UK, DFS, and John Lewis are leading specialty channel players.

France Bedroom Furniture Market Size

France accounts for approximately 12% of European bedroom furniture market revenue in 2025. France's design-forward renovation culture and active residential real estate market, documented by INSEE household spending data, sustain consistent bedroom furniture demand. IKEA France, BUT, and Maisons du Monde are leading furniture distribution platforms.

Asia Pacific Bedroom Furniture Market Trends and Insights

Asia Pacific commands the global bedroom furniture market, driven by the convergence of the world's most rapid urbanization, adding hundreds of millions of first-time urban household buyers annually, and a growing aspirational middle class investing in residential quality. China accounts for approximately 48% of Asia Pacific bedroom furniture demand, with domestic brands including Oppein Home Group competing alongside IKEA for the expanding urban consumer base.

India, Southeast Asia, and South Korea are the region's fastest-growing sub-markets, where demographic youth and housing programs create the highest volume of new household formations globally. Companies scaling in this region must navigate price sensitivity, a transition from carpenter-shop custom procurement toward organized retail, and the rapid adoption of e-commerce distribution.

India Bedroom Furniture Market Size

India represents approximately 13% of Asia Pacific bedroom furniture market revenue in 2025. India's PMAY program targeting 29.5 million urban homes and rapidly expanding urban middle-class household formation are generating the region's fastest-growing first-time buyer cohort. The transition from carpenter-shop procurement toward organized retail and e-commerce is reshaping distribution. India is projected at approximately 9.4% CAGR through 2033.

Japan Bedroom Furniture Market Size

Japan contributes approximately 8% of Asia Pacific bedroom furniture market revenue in 2025. Japan's mature, design-sophisticated bedroom furniture market is driven by replacement cycles and renovation of an aging existing housing stock rather than new household formation. IKEA Japan, Nitori Holdings, and MUJI are leading domestic specialty channels.

Southeast Asia Bedroom Furniture Market Size

Southeast Asia collectively accounts for approximately 11% of Asia Pacific bedroom furniture market revenue in 2025. Vietnam, Indonesia, and Thailand are experiencing rapid urban household formation and middle-class growth, with Vietnam additionally serving as a major global furniture export manufacturing hub. IKEA is expanding its Southeast Asia footprint aggressively, and regional e-commerce platforms are broadening distribution reach.

Competitive Landscape

The global bedroom furniture market is highly fragmented, with a large number of regional manufacturers, unorganized players, and organized retailers competing across price segments. Despite low concentration at the top, scale advantages remain critical, particularly in sourcing, manufacturing efficiency, and distribution reach. At the same time, niche positioning through design, customization, and premium branding enables smaller or specialized players to compete effectively in targeted segments.

From a strategic standpoint, companies are increasingly investing in digital channels, including e-commerce platforms and direct-to-consumer models, to expand reach and improve margins. Supply chain optimization and sustainable sourcing practices are becoming essential, driven by regulatory requirements and shifting consumer preferences. Additionally, mid-market players are moving toward premiumization through improved design and product quality. High logistics costs and the need for strong brand trust act as entry barriers, although new entrants can still gain traction through innovative designs, online-first strategies, and differentiated customer experiences.

Key Developments

- March 2026: Furniture in Fashion launched a new seasonal home furniture collection featuring contemporary designs, diverse product ranges, and affordable pricing, aiming to cater to evolving consumer preferences for stylish, trend-driven interiors and enhance its online retail offering.

- February 2026: Westwing launched in the UK with a curated European design offering, expanding its premium home & living e-commerce presence and providing British consumers access to a wide assortment of in-house and partner furniture brands.

- August 2025: Interio by Godrej launched “Ready-to-Furnish Flat Solutions” in collaboration with real estate developers, offering fully furnished, customizable homes with modular furniture packages, digital planning tools, and fast installation to simplify the home-buying and move-in experience.

Bedroom Furniture Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 179.4 Billion |

| Current Market Value (2026) | US$ 260.3 Billion |

| Projected Market Value (2033) | US$ 412.5 Billion |

| CAGR (2026 - 2033) | 6.8% |

| Leading Region | Asia Pacific, 41% market share (2025) |

| Dominant Product Type | Beds, 38% share (2025) |

| Top-Ranking Material Type | Wood, 52% share (2025) |

| Incremental Opportunity (2026 - 2033) | US$ 152.2 Billion |

Companies Covered in Bedroom Furniture Market

- Williams-Sonoma Inc.

- Crystal Furnitech Pvt Ltd

- RH (Restoration Hardware)

- Inter IKEA Systems B.V.

- American Signature, Inc.

- Jasons Furniture Outlet

- La-Z-Boy Incorporated

- Oppein Home Group Inc.

- Raymour & Flanigan Furniture and Mattresses

- Ashley Global Retail, LLC

- Wayfair LLC

- Crate and Barrel (Euromarket Designs Inc.)

- Rooms to Go

- Ethan Allen Interiors Inc.

- Nitori Holdings Co., Ltd.

- Dorel Industries Inc.

Frequently Asked Questions

The bedroom furniture market is projected to reach US$ 260.3 billion in 2026.

The demand is driven by urbanization, rising middle-class income, and new housing formation.

Asia Pacific leads, accounting for around 41% of the market share.

The key opportunity lies in e-commerce premiumization and circular economy furniture resale.

Leading players include Inter IKEA Systems B.V., Ashley Global Retail, Williams-Sonoma Inc., RH, Wayfair LLC, Ethan Allen Interiors, La-Z-Boy, and Oppein Home Group.