- Home Care & Utilities

- Pet Toys Market

Pet Toys Market Size, Share, and Growth Forecast 2026 - 2033

Pet Toys Market by Product Type (Chew Toys, Plush Toys, Interactive Toys, Rope Toys, Others), Pet Type (Dogs, Cats, Others), Material (Rubber, Plastic, Fabric, Natural Materials), Distribution Channel (Pet Specialty Stores, Supermarkets/Hypermarkets, Online Retail, Veterinary Clinics), and Regional Analysis, 2026 - 2033

Pet Toys Market Size and Trend Analysis

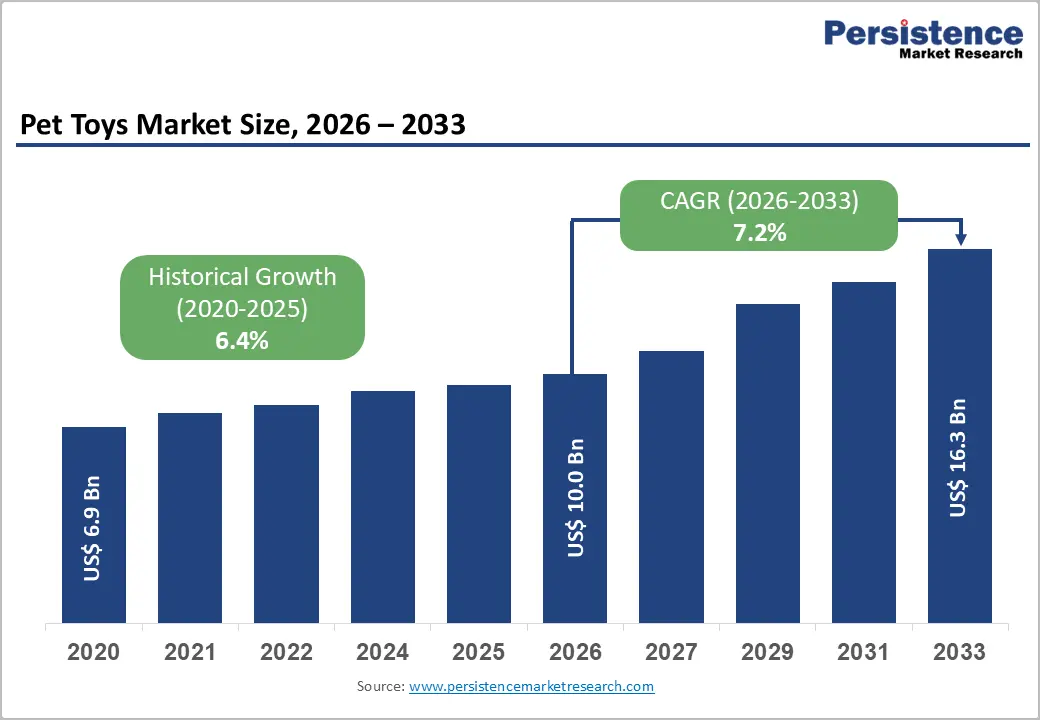

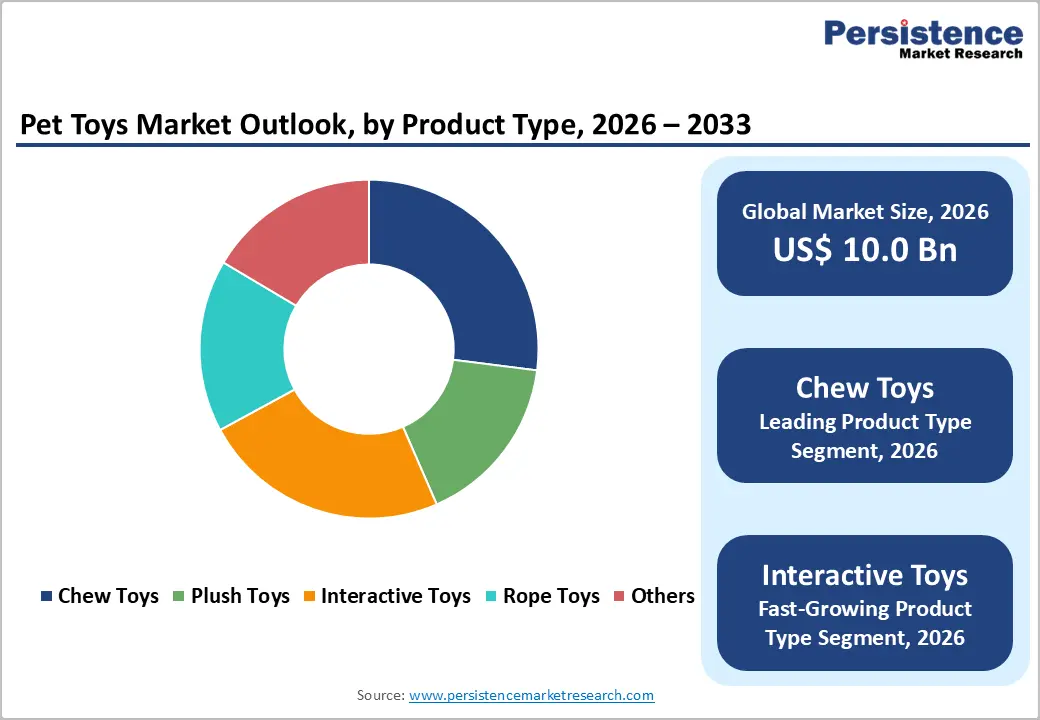

The global pet toys market size is expected to be valued at US$ 10.0 billion in 2026 and projected to reach US$ 16.3 billion by 2033, expanding at a CAGR of 7.2% between 2026 and 2033.

Robust pet humanization, rising disposable incomes, and a structural shift toward premiumization are propelling industry growth. According to the American Pet Products Association (APPA), U.S. pet industry expenditures crossed US$ 152 billion in 2024, with non-food supplies forming a meaningful share. The rise in single-person households across OECD countries and pet ownership exceeding 66% of U.S. households per the AVMA are reinforcing demand for enrichment-focused pet toys globally.

Key Industry Highlights:

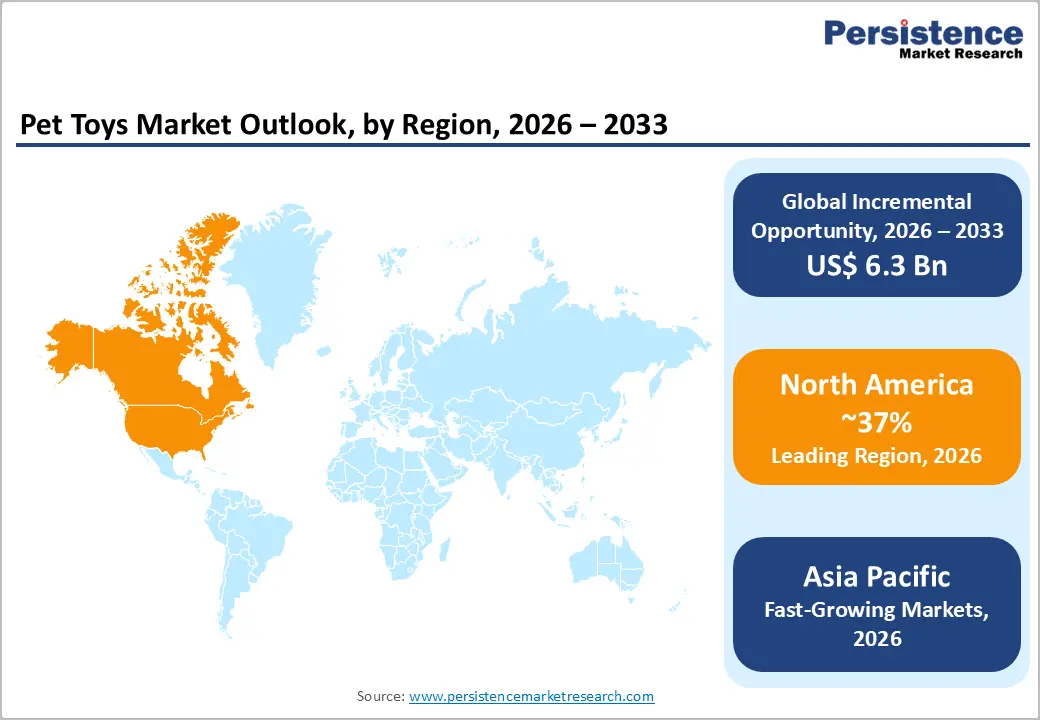

- Leading Region: North America leads with nearly 37% share in 2025, driven by pet humanization and mature e-commerce infrastructure.

- Fast-Growing Market: Asia Pacific expands fastest at a CAGR of nearly 8.7% during 2026 - 2033, led by China and India.

- Dominant Pet Type: Dogs dominate the pet type segment with approximately 68% market share in 2025, supported by higher per-pet toy expenditure.

- Fast-Growing Toy Type: Interactive toys lead category growth, fueled by IoT integration, smart treat dispensers, and anti-anxiety enrichment demand.

- Key Opportunity: Sustainable and natural-material toys offer strong upside, backed by eco-conscious consumers and tightening plastic regulations globally.

Market Dynamics

Drivers - Pet Humanization Reshaping Premium Spending Across Toy Categories Globally

The treatment of pets as family members is fundamentally reshaping purchase behavior across the pet toys category. The American Pet Products Association (APPA) reported that around 86.9 million U.S. households owned a pet in 2024, with owners increasingly willing to spend on enrichment products that mirror human-grade quality. Total U.S. pet industry spending surpassed US$ 152 billion in 2024, signaling sustained category resilience even amid inflationary pressures across discretionary consumer goods.

This generational shift is most visible among millennial and Gen Z pet parents, who outspend older cohorts on enrichment items. U.S. Bureau of Labor Statistics data shows household pet expenditures rose nearly 11% between 2022 and 2024. Combined with social-media-fueled pet content, this is sustaining strong demand for plush, interactive, and personality-aligned toys, supporting the broader pet care accessories ecosystem.

E-commerce Boom and Subscription Boxes Accelerating Pet Toy Sales

The accelerated digitalization of pet retail is unlocking new growth pathways for toy manufacturers. According to the U.S. Census Bureau, e-commerce sales accounted for nearly 16.1% of total retail sales in 2024, and pet supplies emerged as one of the fastest-growing online categories. Subscription-based services such as BarkBox ship millions of curated boxes annually, embedding novelty toys into recurring purchases and lifting average customer lifetime value.

The U.K. Pet Food Manufacturers' Association (PFMA) notes that nearly 62% of British pet owners now buy pet supplies online at least occasionally, while Eurostat confirms cross-border e-commerce in the EU grew 9% year-on-year in 2024. This frictionless access, combined with personalized recommendations powered by data analytics, is widening assortment depth and accelerating repeat purchases of pet toys worldwide.

Restraints - Safety Recalls and Strict Regulatory Scrutiny Constrain Toy Manufacturers

Heightened oversight on chemical safety and choking hazards is curtailing margin flexibility for manufacturers. The U.S. Consumer Product Safety Commission (CPSC) and the European Chemicals Agency (ECHA) have intensified screening of phthalates, lead, and BPA used in plastic and rubber toys. In 2023, several pet toy SKUs were pulled from major U.S. retailers after independent testing flagged lead levels exceeding 90 ppm, denting consumer trust.

Compliance with REACH and CPSIA standards adds 8-12% to production costs, particularly straining small and mid-sized manufacturers. The CPSC logged over 300 pet-product-related safety incidents in 2023, prompting tighter import inspections. These compounding compliance burdens slow time-to-market for innovative designs and discourage experimentation with novel polymer blends across the broader pet products ecosystem.

Plastic Waste Concerns Pressuring Conventional Pet Toy Producers

Sustainability pressure is becoming a tangible barrier for conventional pet toy producers. The U.S. Environmental Protection Agency (EPA) estimates that nearly 35.7 million tons of plastic waste are generated annually in the country, and pet products contribute a small but growing share. The World Wildlife Fund (WWF) indicates that nearly 55% of millennial pet owners now consider environmental footprint before purchasing pet accessories.

Brands relying heavily on virgin plastics face reputational and regulatory headwinds, especially in Europe, where the EU Single-Use Plastics Directive is reshaping perception of plastic-based consumer goods. The European Environment Agency (EEA) reports plastic packaging recycling rates plateauing near 41%, limiting circularity claims. These structural pressures are compelling reformulation, raising input costs for legacy pet toy manufacturers.

Opportunities - Smart IoT and AI-Driven Interactive Toys Unlocking New Frontiers

Technology-enabled enrichment is emerging as one of the most lucrative frontiers for the pet toys market. App-controlled treat dispensers, motion-tracking laser toys, and AI-driven puzzle feeders are gaining traction as pet owners look for solutions to combat separation anxiety and behavioral issues. The American Veterinary Medical Association (AVMA) notes that nearly 17% of dogs display separation-related behaviors, creating a clear use case for interactive engagement.

Companies such as PetSafe, Wickedbone, and Petcube are scaling smart toy lineups, while connected pet care spending climbs in line with the broader smart home segment. The U.S. Federal Communications Commission (FCC) authorized over 2,500 connected pet device filings through 2024. Rising adoption of voice assistants and pet cameras further integrates interactive toys into connected ecosystems.

Sustainable and Natural Material Innovation Driving Premiumization Opportunities

Eco-conscious consumption is opening fresh white space for differentiated toy offerings. The Pet Sustainability Coalition reports that nearly 45% of new pet product launches in 2024 carried a sustainability claim, up from 28% in 2021, reflecting both consumer demand and retailer assortment shifts toward responsibly sourced enrichment products across mainstream channels.

Brands such as West Paw, Beco Pets, and Green Toys are pioneering toys made from recycled rubber, hemp, organic cotton, and FSC-certified natural fibers. The U.S. Department of Agriculture (USDA) BioPreferred Program now lists multiple certified pet toy materials, easing procurement for retailers. This trajectory aligns closely with the broader natural pet care market, presenting attractive premiumization opportunities for early movers across both developed and emerging economies.

Category-wise Analysis

Product Type Insights

Chew Toys lead the product type segment, accounting for nearly 34% of the global pet toys market in 2025. Their dominance stems from the universal need to address dental health, teething behavior, and destructive chewing across dog populations. The American Veterinary Dental College reports that nearly 80% of dogs show signs of periodontal disease by age three, making dental-focused chew toys a recurring household purchase.

Interactive Toys represent the fastest-growing sub-category, propelled by rising demand for cognitive enrichment and anti-anxiety solutions. The AVMA notes that pet behavioral consultations have risen sharply post-pandemic, fueling adoption of puzzle feeders and app-controlled toys. Brands such as PetSafe, Outward Hound, and Wickedbone are accelerating launches, integrating sensors, treat dispensing, and motion tracking, broadening engagement-driven product portfolios across global pet specialty channels.

Pet Type Insights

Dogs account for the largest share within the pet type segment, contributing approximately 68% of total pet toys revenue in 2025. The American Pet Products Association (APPA) estimates that nearly 65 million U.S. households own at least one dog, with average annual toy and supply expenditure exceeding US$ 75 per dog versus US$ 30 per cat as reported by the AVMA, embedding stronger replacement cycles.

Cats are the fastest-growing pet type sub-segment, driven by rising urban adoption and apartment-friendly companionship trends. The APPA confirms cat-owning households are climbing steadily, with feline parents increasingly investing in feather wands, laser pointers, and interactive plush toys. ASPCA behavioral guidelines emphasizing indoor enrichment for cats are reinforcing repeat purchases, expanding the category footprint across both developed and emerging pet care markets globally.

Material Analysis

Rubber holds the leading position within the material segment, capturing nearly 37% of the global pet toys market in 2025. Its dominance is driven by superior durability, bounce, and safety performance for chew and fetch applications. Natural rubber toys from manufacturers like KONG are widely recommended by veterinarians, with the American Kennel Club (AKC) highlighting rubber's resistance to fragmentation under ASTM F963 safety testing standards.

Natural materials represent the fastest-growing material sub-segment, fueled by sustainability preferences and regulatory pressure on virgin plastics. Brands such as West Paw, Beco Pets, and Green Toys are pioneering toys made from hemp, organic cotton, and FSC-certified fibers. The Pet Sustainability Coalition confirms a sharp rise in eco-claims among new launches, while the EU Single-Use Plastics Directive is accelerating adoption across European pet specialty retail networks.

Distribution Channel Insights

Online retail has emerged as the leading distribution channel, capturing nearly 42% share of the global pet toys market in 2025. Pet owners increasingly favor digital storefronts for assortment depth, competitive pricing, subscription convenience, and home delivery. According to the U.S. Census Bureau, e-commerce contributed 16.1% of total retail sales in 2024, with Chewy, Amazon, and PetSmart.com dominating online pet toy distribution.

Veterinary Clinics represent the fastest-growing distribution sub-segment, driven by rising trust in vet-recommended products and integrated wellness purchases. The AVMA reports nearly 78% of pet owners consider veterinarian's endorsement highly influential during purchase decisions. Expansion of corporate vet chains such as VCA Animal Hospitals and Banfield Pet Hospital is broadening in-clinic retail of dental chews, enrichment toys, and behavioral aids across North America and Europe.

Regional Insights

North America Pet Toys Market Trends and Insights

North America leads the global pet toys market with an estimated share of nearly 37% in 2025. The region benefits from extremely high pet ownership penetration, premiumization trends, and a mature retail infrastructure. The American Pet Products Association (APPA) confirms that pet humanization and rising demand for interactive and enrichment-focused toys are accelerating regional category growth, with strong contributions from chew toys, smart toys, and sustainable plush categories.

- U.S. Pet Toys Market Size

The United States accounts for nearly 88% of the North American pet toys market in 2025, supported by approximately 86.9 million pet-owning households as reported by the APPA. Strong disposable incomes, advanced e-commerce penetration via Chewy and Amazon, and rising spend on premium and tech-enabled toys underpin sustained U.S. leadership across the chew, interactive, and plush toy sub-categories.

Europe Pet Toys Market Trends and Insights

Europe represents the second-largest pet toys market, holding nearly 27% share globally in 2025. The European Pet Food Industry Federation (FEDIAF) estimates over 340 million pets across the region. Growing demand for sustainable and natural-material toys, alongside stringent REACH chemical compliance, is steering brands toward eco-friendly innovations and certified non-toxic offerings.

- Germany Pet Toys Market Size

Germany leads the European pet toys market, accounting for nearly 22% of the regional share in 2025. According to the Zentralverband Zoologischer Fachbetriebe (ZZF), Germany hosts over 34 million pets, and German consumers display strong preference for premium, sustainable, and TÜV-tested toys, supporting steady growth in rubber and natural-material categories.

- U.K. Pet Toys Market Size

The United Kingdom holds approximately 18% share of the European pet toys market in 2025. The U.K. Pet Food Manufacturers' Association (PFMA) estimates 38 million pets in British households, with nearly 62% of owners purchasing supplies online. Growing demand for interactive and dental chew toys is fueling brand competition across pet specialty and digital channels.

- France Pet Toys Market Size

France contributes nearly 15% of the European pet toys market in 2025. FACCO, the French pet food association, estimates over 75 million pets in France, including a leading share of cats. Rising adoption of plush and interactive feline toys, alongside growing premiumization through specialty pet boutiques, is supporting consistent market expansion.

Asia Pacific Pet Toys Market Trends and Insights

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of nearly 8.7% during 2026 - 2033. China leads regional growth, with the China Pet Industry Association estimating over 120 million urban pet dogs and cats in 2024. Rising urbanization, single-person households, and rapid e-commerce expansion via Tmall and JD.com are key catalysts.

- India Pet Toys Market Size

India holds approximately 9% share of the Asia Pacific pet toys market in 2025, anchored by rapidly rising urban pet adoption. According to the Indian Veterinary Association, the country's pet dog population exceeds 30 million. Growing middle-class spending, expansion of online platforms such as Heads Up For Tails, and increased awareness of pet enrichment are driving robust demand.

- Japan Pet Toys Market Size

Japan accounts for nearly 17% of the Asia Pacific pet toys market in 2025. The Japan Pet Food Association reports over 15.9 million dogs and cats in Japanese households. Aging demographics, small-breed dominance, and high spending on premium plush and interactive toys for indoor pets continue to support strong category performance.

- Southeast Asia Pet Toys Market Size

Southeast Asia represents nearly 13% of the Asia Pacific pet toys market in 2025, led by Thailand, Indonesia, and Vietnam. Rising pet adoption among urban millennials, expansion of pet specialty chains, and growth of cross-border e-commerce platforms such as Shopee and Lazada are accelerating accessibility and assortment of imported and locally produced pet toys.

Competitive Landscape

The global pet toys market exhibits a moderately fragmented structure, with established multinational manufacturers competing alongside regional players, private-label brands, and emerging digital-native challengers across diverse price tiers. Industry leaders prioritize R&D-driven product innovation, durability claims, veterinary endorsements, and proprietary material formulations as key differentiators, leveraging deep distribution networks and brand heritage to defend share against fast-moving disruptors.

Strategic priorities increasingly center on expansion of sustainable product lines, IoT-enabled interactive toys, and direct-to-consumer subscription models that strengthen recurring revenue. Mergers and acquisitions, exclusive retail partnerships, and licensed character collaborations are emerging as pivotal business model trends, reshaping competitive positioning and accelerating premiumization across both developed and emerging pet care markets globally.

Key Developments:

- In March 2024, KONG Company launched its expanded "KONG Sport" line, introducing high-durability fetch and tug toys engineered with reinforced rubber compounds aimed at active large-breed dogs.

- In September 2024, PetSafe unveiled an upgraded smart interactive treat-dispensing toy integrating app connectivity and remote feeding capabilities, targeting separation-anxiety pet care.

- In January 2025, West Paw announced a new collection of Zogoflex-based recyclable chew toys made from post-industrial recycled material, reinforcing its sustainability leadership.

Pet Toys Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 6.9 billion |

| Current Market Value (2026) | US$ 10.0 billion |

| Projected Market Value (2033) | US$ 16.3 billion |

| CAGR (2026 - 2033) | 7.2% |

| Leading Region | North America, 37% |

| Dominant Category-1 (Product Type) | Chew Toys, 34% share |

| Top-ranking Category-2 (Pet Type) | Dogs, 68% share |

| Incremental Opportunity | US$ 6.3 billion (2026 - 2033) |

Companies Covered in Pet Toys Market

- KONG Company

- Nylabone Products (Central Garden & Pet)

- PetSafe (Radio Systems Corporation)

- Hartz Mountain Corporation

- Mars Petcare (including Whimzees)

- Spectrum Brands (FURminator, GoodBoy)

- West Paw Inc.

- Benebone LLC

- Petmate Holdings Co.

- JW Pet (Petmate)

- Outward Hound (Kyjen Company)

- Chuckit! (Petmate)

- Beco Pets

- Wickedbone (Cheerble)

- Petcube Inc.

Frequently Asked Questions

The global pet toys market is expected to reach US$ 10.0 billion in 2026, growing steadily at a CAGR of 7.2% through 2033 to attain US$ 16.3 billion.

Rising pet humanization, supported by 86.9 million pet-owning U.S. households per the APPA, and surging premium spending by millennial and Gen Z owners are key demand drivers for pet toys globally.

North America leads with nearly 37% global share in 2025, driven by high pet ownership, premiumization, advanced e-commerce penetration via Chewy and Amazon, and a mature pet specialty retail ecosystem.

Smart, IoT-enabled interactive toys and sustainable natural-material toys present major opportunities, with 45% of 2024 pet product launches carrying sustainability claims per the Pet Sustainability Coalition.

Key players include KONG Company, Nylabone, PetSafe, Hartz Mountain Corporation, Mars Petcare, West Paw Inc., Benebone LLC, Petmate Holdings, Outward Hound, and Petcube Inc., among others.