- Home Care & Utilities

- Musical Instrument Market

Musical Instrument Market Size, Share, and Growth Forecast 2026 - 2033

Musical Instrument Market by Instrument Type (String Instruments, Keyboard Instruments, Percussion Instruments, Wind Instruments, Electronic Instruments), Application (Professional, Educational, Personal), Distribution Channel (Specialty Stores, Online Retail, Supermarkets/Hypermarkets, Direct Sales), and Regional Analysis, 2026 - 2033

Musical Instrument Market Size and Trend Analysis

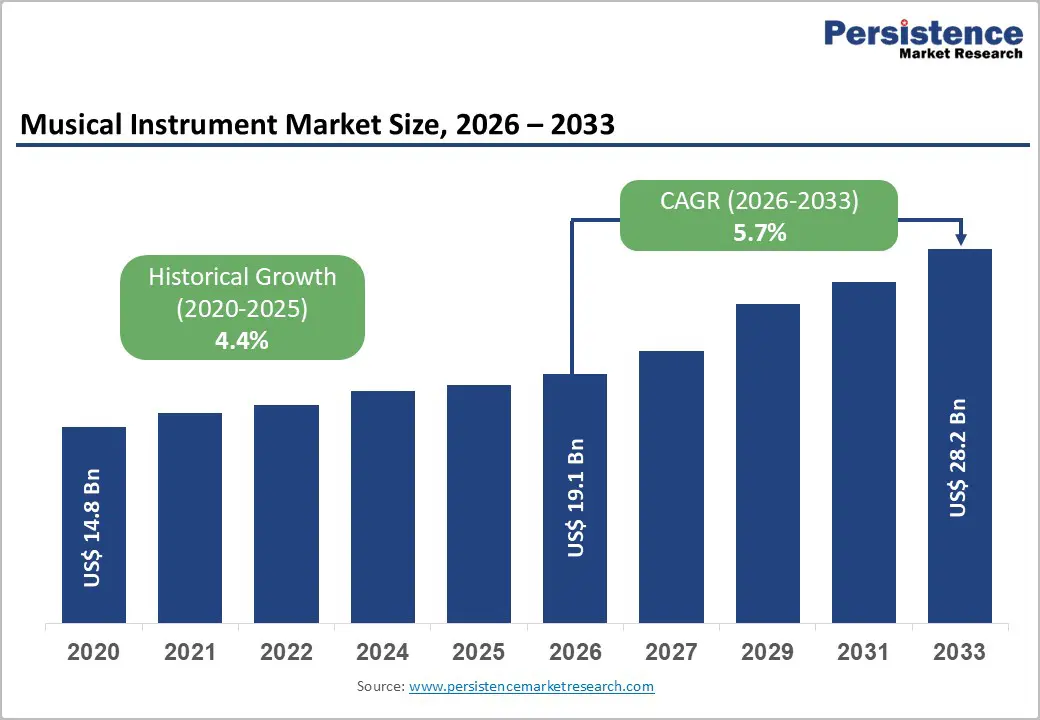

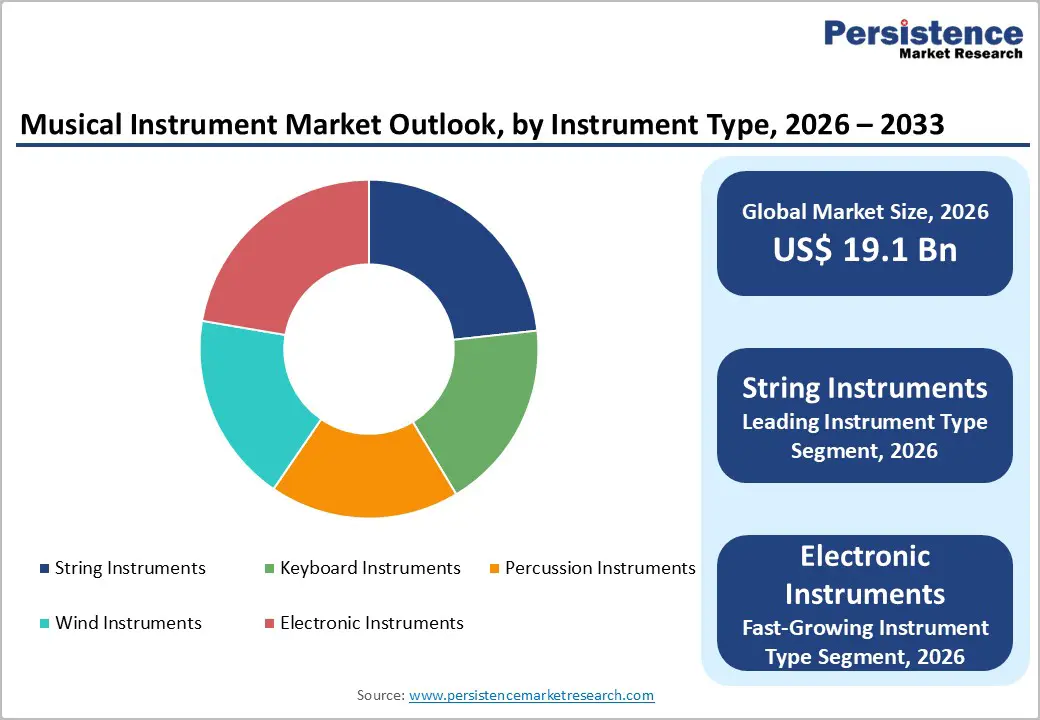

The global musical instrument market size is likely to reach US$ 19.10 billion in 2026 and grow to US$ 28.16 billion by 2033, registering a CAGR of 5.7%, supported by expanding music-integrated education policies, rising hobbyist participation, and rapid adoption of hybrid acoustic-digital instruments.

Technologies such as TransAcoustic pianos and digitally connected instruments are reshaping purchasing patterns across professional, educational, and personal applications. Post-pandemic growth in first-time buyers, alongside government-backed music education initiatives such as the U.S. ESSA framework, continues to strengthen long-term institutional and consumer demand globally, sustaining steady market expansion.

Key Industry Highlights:

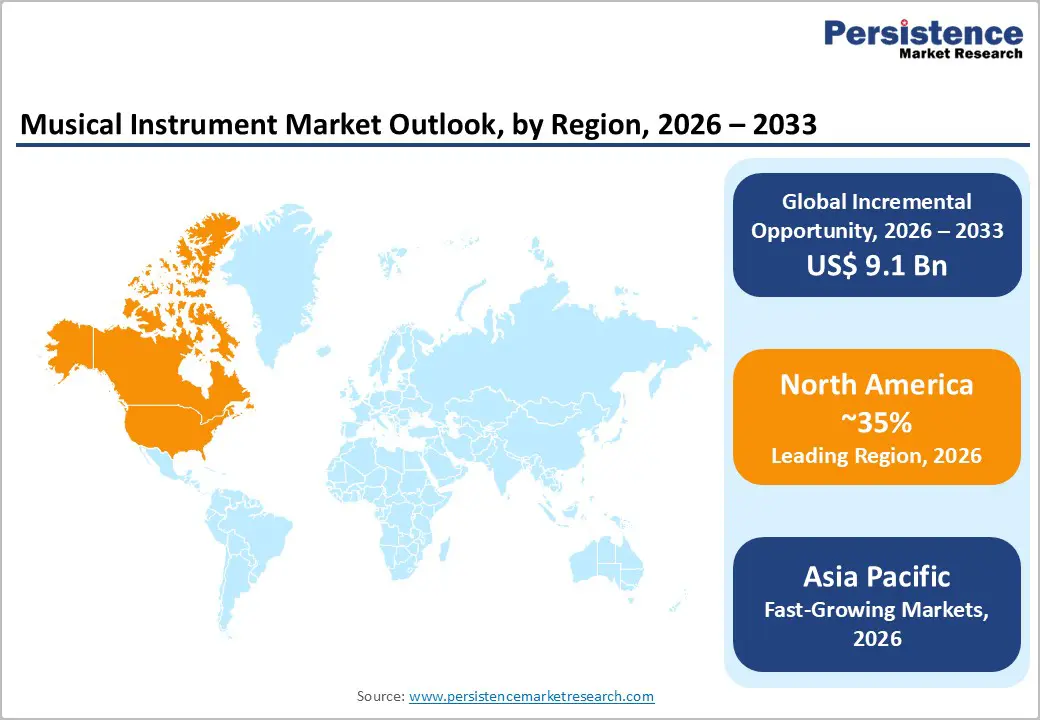

- Leading Region: North America leads the global musical instrument market with a 35.0% share in 2026, supported by strong music education policies, professional music infrastructure, and high consumer spending on instruments.

- Fast-growing Market: Asia Pacific is the fast-growing market, driven by expanding music education programs, rising middle-class participation, and strong demand for electronic and hybrid instruments.

- Leading Category: String instruments dominate with a 34.0% share in 2026, supported by the global popularity of acoustic and electric guitars across beginner, educational, and professional applications.

- Fastest Growing Category: Electronic instruments witness the fast-growth due to the rising adoption of MIDI controllers, digital music production tools, and software-integrated learning systems.

- Key Opportunity: Integration of digital music-learning platforms with instrument ecosystems is creating major long-term revenue opportunities through subscription services, customer retention, and connected learning experiences.

Market Dynamics

Drivers - Institutionalised Music Education Mandates Driving Recurring Instrument Procurement

Government-backed music education programs are creating one of the most stable demand foundations for the global musical instrument market. National education frameworks increasingly classify music as a core developmental subject, encouraging schools to allocate recurring budgets toward instrument procurement. UNESCO’s arts education recommendations and similar national curriculum reforms across the Asia Pacific, Latin America, and Africa are accelerating purchases of keyboards, wind instruments, and percussion products for classroom and extracurricular activities.

In the United States, school music enrollment recovered strongly after pandemic-related disruptions, supported by policies such as the Every Student Succeeds Act (ESSA). This institutional demand reduces reliance on discretionary consumer spending and provides predictable revenue streams for manufacturers supplying educational programs. Companies with direct institutional sales networks and tender participation capabilities are expected to benefit significantly as emerging economies continue integrating structured music education into long-term academic planning.

The Hybrid Digital-Acoustic Innovation Wave Expanding the Addressable Market

The growing adoption of hybrid acoustic-digital instruments is significantly expanding the consumer base beyond traditional musicians. Urban consumers, apartment residents, remote learners, and content creators increasingly prefer instruments that combine authentic acoustic sound with silent-practice and digital connectivity features. Products such as Yamaha’s TransAcoustic and Silent Piano series demonstrate how integrated technology can attract premium buyers seeking flexibility, portability, and software compatibility within a single instrument ecosystem.

Manufacturers are also embedding Bluetooth MIDI, cloud-based learning integration, and recording functionality into keyboards, drums, and guitars. This shift is transforming instruments from standalone hardware products into connected digital platforms linked to music-learning applications and production software. Companies investing in firmware development, app ecosystems, and subscription-based learning partnerships are expected to gain stronger pricing power and customer retention, particularly in premium and intermediate product categories during the forecast period.

Restraints - Raw Material Cost Inflation and Tightening Timber Regulations Compressing Manufacturer Margins

Rising raw material costs and stricter timber regulations are placing significant financial pressure on musical instrument manufacturers worldwide. Acoustic guitars, violins, pianos, and orchestral instruments rely heavily on premium tonewoods such as rosewood, ebony, and spruce, many of which face tighter environmental oversight under international trade regulations. Compliance requirements, certification processes, and restricted sourcing channels are increasing procurement lead times and elevating production costs across the industry.

Manufacturers are responding by adopting alternative materials and certified sustainable wood sources, but these transitions require substantial research, tooling, and product redesign investments. Smaller regional manufacturers often struggle to absorb these additional expenses, especially in mid-priced product categories where consumers remain highly price sensitive. As a result, profit margins are narrowing while competitive pricing pressure continues to intensify across entry-level and intermediate instrument segments globally.

U.S.-China Trade Tariffs Creating Structural Cost Disadvantages for Import-Dependent Distributors

Trade tensions between the United States and China continue to create structural cost challenges for import-dependent musical instrument distributors. A significant portion of entry-level keyboards, electronic drums, and student-grade instruments sold in Western markets is manufactured in China. Tariffs imposed under Section 301 have increased landed costs for distributors, reducing pricing flexibility and compressing already narrow margins in highly competitive consumer segments.

Many established brands have attempted to diversify manufacturing toward Vietnam, Malaysia, and other Asian production hubs, but supply-chain relocation requires capital investment and operational restructuring. Smaller entrants lacking diversified sourcing networks face greater vulnerability to tariff-related volatility and shipping cost fluctuations. These conditions raise barriers to entry for new competitors while forcing manufacturers to carefully balance affordability, profitability, and supply-chain resilience across global distribution operations.

Opportunities - Music Education Infrastructure Build-Out Offers a Decade-Long Volume Growth Window

Emerging economies are creating substantial long-term opportunities for musical instrument manufacturers through expanding investment in arts and music education infrastructure. Governments across India, Southeast Asia, and parts of Africa are increasingly integrating music and creative arts into national education strategies. These reforms are encouraging large-scale procurement of educational instruments, creating sustained demand for affordable keyboards, percussion products, and beginner-level string instruments across public and private institutions.

India’s National Education Policy 2020 represents a major structural catalyst by formally incorporating arts and music into mainstream curricula. In response, manufacturers and distributors are expanding retail, training, and institutional partnerships throughout the country. Companies with local manufacturing capabilities and region-specific product customization strategies are expected to benefit most from this opportunity, particularly as state-level implementation budgets and educational procurement programs continue expanding over the coming decade.

Digital Music Learning Platform Ecosystem Partnerships as a Distribution and Demand-Generation Engine

Digital music learning platforms are emerging as powerful demand-generation channels for the musical instrument market. Applications such as Simply Piano, Yousician, and Fender Play have introduced millions of users to structured music education through subscription-based digital learning models. Since instrument ownership is essential for platform engagement, these ecosystems directly stimulate purchases of guitars, keyboards, drums, and beginner-focused instruments across global consumer markets.

Manufacturers are increasingly partnering with learning platforms through bundled subscriptions, app integrations, and co-branded educational programs designed to improve customer acquisition and long-term retention. These collaborations also strengthen brand loyalty by connecting beginners with specific instrument ecosystems during the early stages of learning. As platform consolidation accelerates, companies establishing early strategic partnerships are expected to secure stronger market visibility, recurring revenue opportunities, and higher engagement across digitally connected consumer segments.

Category-wise Analysis

Instrument Type Insights

The String Instruments segment dominates the global musical instrument market with a 34.0% share in 2026. The category maintains leadership due to the widespread popularity of acoustic and electric guitars across beginner, educational, and professional user groups. String instruments also benefit from strong orchestral demand and consistent retail sales through music schools, performance institutions, and hobbyist consumers globally, supporting stable long-term volume demand across developed and emerging markets.

The electronic instruments segment is the fast-growing category, supported by increasing adoption of MIDI controllers, digital keyboards, electronic drum kits, and home music-production equipment. Younger consumers increasingly prefer software-integrated instruments compatible with digital audio workstations and online learning platforms. The expansion of content creation, livestream performances, and home recording studios is accelerating demand for connected electronic instruments among both amateur musicians and professional creators worldwide.

Application Insights

The professional segment accounts for 41.0% of the global musical instrument market in 2026. The segment leads due to the premium pricing associated with professional-grade pianos, guitars, orchestral instruments, and studio equipment used by touring artists, recording studios, and performing arts institutions. Recurring replacement cycles, customization requirements, and higher spending capacity among professional musicians continue to support strong revenue generation within this application category globally.

The educational segment is emerging as the fast-growing application area, driven by the increasing integration of music programs into school curricula and institutional learning frameworks. Governments and educational institutions are expanding investments in classroom music equipment, beginner instruments, and extracurricular arts programs. Rising participation in structured music learning, combined with growing enrollment in private music academies and online instruction platforms, is strengthening demand for student-friendly and entry-level instruments worldwide.

Distribution Channel Insights

The Specialty Stores segment holds the largest share of the global musical instrument market at 32.0% in 2026. The channel remains dominant because consumers prefer in-store product testing, expert guidance, maintenance support, and personalized recommendations before purchasing instruments. Specialty retailers also play a critical role in premium product sales, repairs, rentals, and professional musician servicing, making them highly relevant despite increasing competition from digital commerce platforms.

Online retail is the fastest growing distribution channel, supported by rising consumer confidence in digital purchasing and expanding e-commerce capabilities among manufacturers and retailers. Online platforms provide wider product availability, competitive pricing, virtual tutorials, and convenient delivery options for buyers globally. Growth in direct-to-consumer sales models, digital product demonstrations, and music-focused online marketplaces is further accelerating the transition toward hybrid omnichannel purchasing behavior across the musical instrument industry.

Regional Insights

North America Musical Instrument Market Trends and Insights

North America accounts for 35.0% of the global musical instrument market in 2026, representing US$ 6.68 Billion. Growth is supported by strong professional music infrastructure, ESSA-backed school music programs, and high consumer spending on instruments. The region also benefits from established specialty retail networks and rapid adoption of hybrid digital instruments, supporting stable long-term demand across educational, professional, and personal applications.

United States Musical Instrument Market Size

The United States represents approximately 75-78% of the North American market. Strong participation in school music programs, a large professional entertainment industry, and rising hobbyist engagement continue driving demand. Leading domestic brands such as Fender and Gibson maintain strong pricing power, while growth in educational and beginner-focused instrument purchases supports long-term market expansion across consumer segments.

Europe Musical Instrument Market Trends and Insights

Europe holds approximately 22-24% of the global musical instrument market in 2026. Demand is supported by established conservatories, orchestras, and professional performance institutions across Germany, France, Austria, and the United Kingdom. Sustainability initiatives and certified material sourcing are increasingly influencing procurement decisions, while premium orchestral and keyboard instrument manufacturing continues strengthening Europe’s global competitive position.

Germany Musical Instrument Market Size

Germany accounts for nearly 28-30% of the European musical instrument market. The country remains a major global manufacturing hub for orchestral and premium instruments, supported by specialized craftsmanship clusters in Saxony. Strong conservatory enrollment, export-oriented production, and demand for professional-grade instruments continue positioning Germany as Europe’s leading musical instrument market.

United Kingdom Musical Instrument Market Size

The United Kingdom represents around 18-20% of the European musical instrument market. London’s global influence in music production, live entertainment, and recording industries supports strong professional demand. Government-backed music education initiatives and established premium retail infrastructure continue driving purchases across educational institutions, performance venues, and consumer-focused music-learning segments throughout the country.

France Musical Instrument Market Size

France accounts for nearly 14-16% of the European musical instrument market. Government-supported music education programs and strong cultural investment continue driving institutional demand for wind and string instruments. France also maintains a strong professional music heritage, supported by internationally recognized instrument manufacturers and increasing cultural tourism linked to major performing arts activities.

Asia Pacific Musical Instrument Market Trends and Insights

Asia Pacific accounts for 31.0% of the global musical instrument market in 2026. The region is driven by expanding music education programs, rising middle-class incomes, and strong demand for digital and hybrid instruments. Growth across India, China, Japan, and South Korea is further supported by online learning adoption, youth participation in music production, and expanding regional manufacturing capabilities.

Japan Musical Instrument Market Size

Japan represents approximately 25-28% of the Asia Pacific musical instrument market. The country benefits from the presence of globally recognized manufacturers, including Yamaha, Roland, Casio, and Kawai. Japanese consumers consistently prefer premium-quality instruments, while continued innovation in digital connectivity, AI-assisted tuning, and app-enabled music systems supports stable high-value market demand.

India Musical Instrument Market Size

India accounts for approximately 18% of the Asia Pacific musical instrument market, valued at around US$ 1.07 billion in 2026. Rapid implementation of music-integrated education policies, expanding private music academies, and a large youth population are driving substantial demand growth. Manufacturers are increasingly targeting Tier-2 and Tier-3 cities, where rising disposable incomes and growing interest in music learning create strong long-term opportunities.

South Korea Musical Instrument Market Size

South Korea represents nearly 12% of the Asia Pacific musical instrument market. The country’s strong K-pop and music-production ecosystem continues driving demand for electronic instruments, MIDI equipment, and professional studio tools. Entertainment companies, trainee programs, and digital music creators contribute significantly to instrument purchases, making South Korea an important innovation-focused market within the region.

Competitive Landscape

The global musical instrument market remains moderately consolidated, with competition concentrated among established premium manufacturers and numerous regional producers. Companies compete primarily through craftsmanship quality, brand reputation, product durability, and artist endorsements. Demand for digitally connected instruments is also reshaping competition, as consumers increasingly prefer products integrated with recording software, mobile applications, and online music-learning ecosystems. Strong distribution networks and premium retail presence continue influencing long-term competitive positioning across developed and emerging markets.

Competitive dynamics are steadily shifting toward ecosystem-based business models where instruments support subscription learning, digital engagement, and long-term customer retention. Manufacturers with strong omnichannel strategies and direct-to-consumer capabilities are gaining advantages in premium and mid-tier categories. Meanwhile, rapidly improving low-cost Asian manufacturers are intensifying pricing competition globally.

Key Developments:

- In January 2025, Yamaha Corporation launched the AvantGrand N3X hybrid piano with AI-driven Neural Processing Technology, replicating concert grand acoustic response in compact environments. The launch strengthened competition in premium hybrid pianos and accelerated innovation expectations across digitally integrated keyboard instruments globally.

- In March 2024, Fender Musical Instruments partnered with Spotify to integrate Fender Play lessons into the Spotify platform, expanding digital customer engagement. The collaboration highlighted the growing importance of subscription-based learning ecosystems in driving instrument sales, user retention, and long-term beginner musician engagement.

- In September 2023, Gibson Brands completed the acquisition of premium amplifier manufacturer MESA/Boogie, expanding its presence in professional audio equipment. The acquisition reflected increasing industry consolidation as instrument manufacturers broaden portfolios beyond hardware to strengthen recurring revenue opportunities and customer ecosystem integration.

Musical Instrument Market - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 14.75 Billion |

| Current Market Value (2026) | US$ 19.10 Billion |

| Projected Market Value (2033) | US$ 28.16 Billion |

| CAGR (2026 - 2033) | 5.7% |

| Leading Region | North America (35.0%) |

| Dominant Instrument Type | String Instruments (34.0%) |

| Top-ranking Application | Professional (41.0%) |

| Top-ranking Distribution Channel | Specialty Stores (32.0%) |

| Incremental Opportunity (2026 - 2033) | US$ 9.06 Billion |

Companies Covered in Musical Instrument Market

- Yamaha Corporation

- Roland Corporation

- Fender Musical Instruments

- Gibson Brands

- Casio

- Kawai Musical Instruments

- Pearl Musical Instrument

- Steinway & Sons

- C.F. Martin & Co.

- Ibanez

- Tama Drums

- Selmer Paris

- Conn-Selmer

- Harman International

- Shure Incorporated

- Korg Inc.

- Moog Music

- Steinberg Media Technologies

- D'Addario & Company

- Donner Music

Frequently Asked Questions

The global musical instrument market is valued at US$ 19.10 billion in 2026 and is projected to reach US$ 28.16 billion by 2033.

Growth is driven by expanding music education policies, rising beginner participation, and increasing adoption of digital music-learning and hybrid instrument ecosystems globally.

String Instruments lead the market with a 34.0% share in 2026 due to strong demand across beginner, professional, and collector consumer segments.

North America dominates with a 35.0% market share in 2026, supported by a strong music education infrastructure and the world’s largest professional music industry.

Key opportunities include digital learning platform integration, subscription-based music ecosystems, and expanding institutional instrument procurement across emerging education markets globally.

Key participants include Yamaha Corporation, Roland Corporation, Fender Musical Instruments, Gibson Brands, and Casio.