- Home Care & Utilities

- Gardening Pesticides Market

Gardening Pesticides Market Size, Share, and Growth Forecast 2026 - 2033

Gardening Pesticides Market by Product Type (Herbicides, Insecticides, Fungicides, Fumigants, Rodenticides, Others), Source (Chemical, Organic – Microbial, Botanical, Biochemical), Formulation Type (Liquid, Powder, Granular, Spray, Others), by Distribution Channel (Offline, Online), and Regional Analysis, 2026 - 2033

Gardening Pesticides Market Size and Trend Analysis

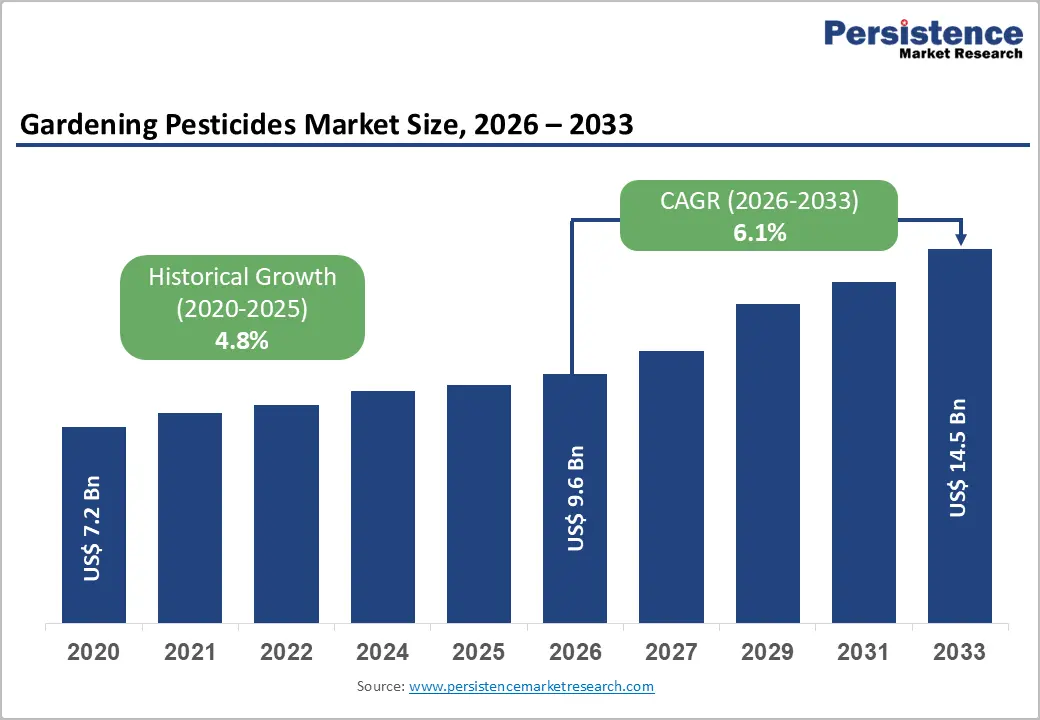

The global gardening pesticides market size is projected to reach US$ 9.6 billion in 2026 and grow to US$ 14.5 billion by 2033, registering a CAGR of 6.1%. Growth is supported by rising residential gardening, urban horticulture, and professional landscaping activities across both developed and emerging economies.

Increasing household spending on lawn care products and heightened awareness of pest-related crop damage are key drivers. Concerns over invasive species such as the Japanese beetle and emerald ash borer, highlighted by the U.S. Department of Agriculture, along with regulatory support from the U.S. Environmental Protection Agency for safer, bio-based formulations, are further accelerating market expansion.

Key Industry Highlights:

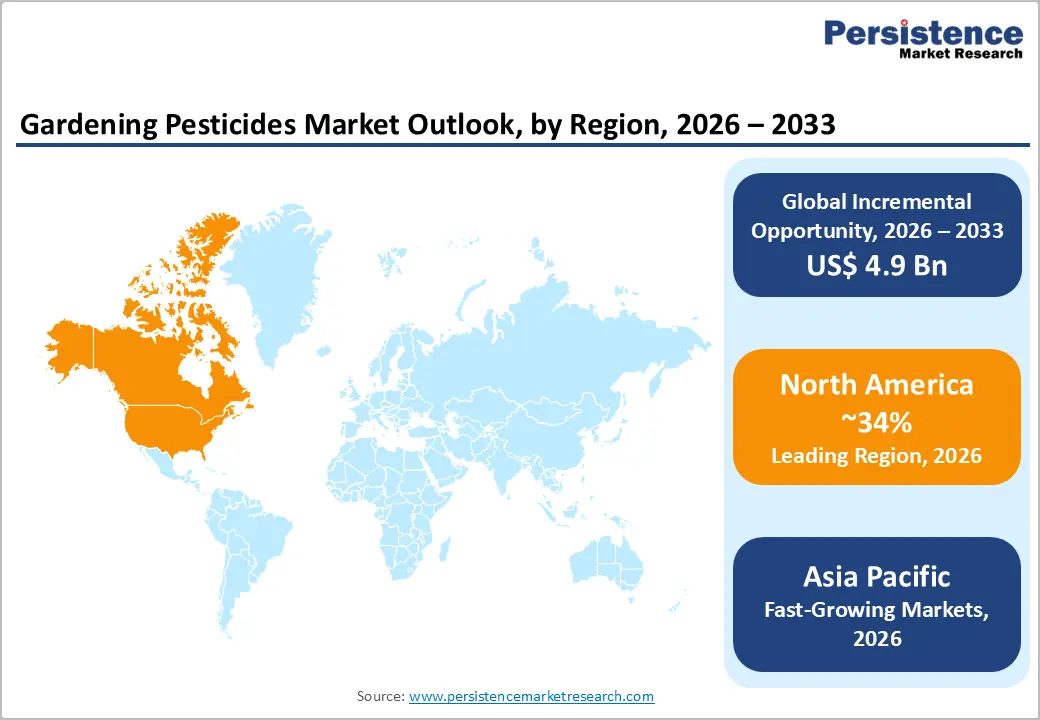

- Leading Region: North America dominates with approximately 34% market share in 2025, supported by strong gardening participation, retail networks, and innovation driven by the U.S. Environmental Protection Agency.

- Fastest Growing Region: Asia Pacific is projected to grow fastest, driven by urban gardening expansion in China and India, rising disposable incomes, and rapid adoption of e-commerce platforms.

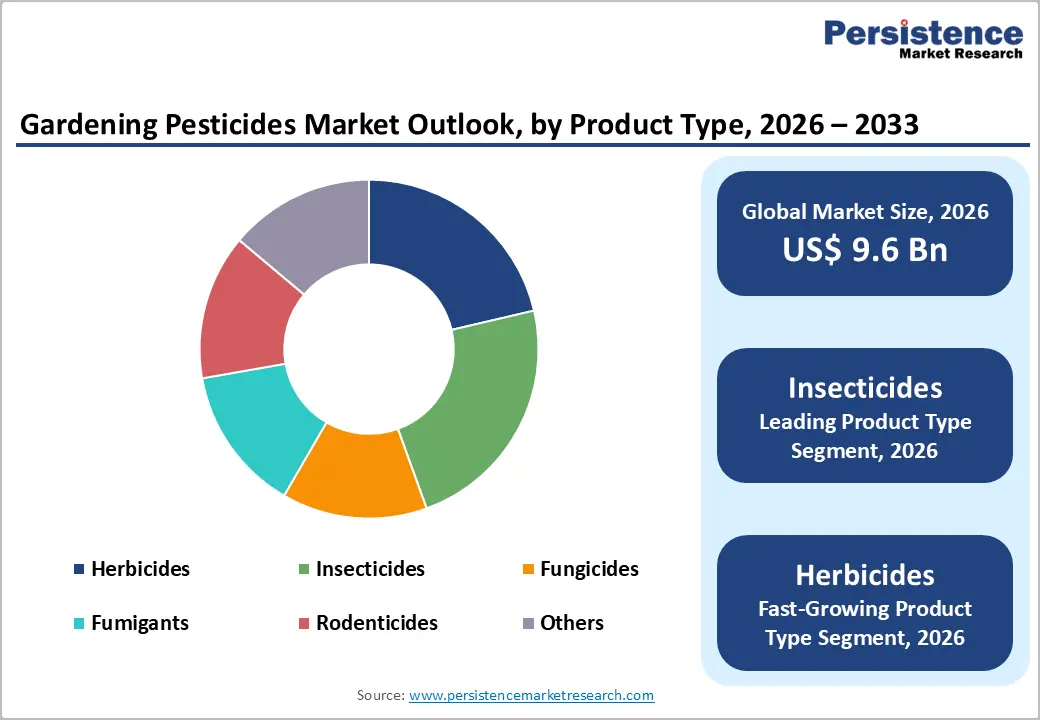

- Dominant Segment: Insecticides lead with around 38% share in 2025, supported by widespread pest issues in residential gardening and availability across both chemical and bio-based formulations.

- Fastest Growing Segment: Bio-based organic pesticides are witnessing strong growth, driven by regulatory restrictions on synthetics, eco-certifications, and increasing consumer preference for safer, environmentally friendly solutions.

- Opportunity: Digital distribution and smart gardening ecosystems are creating opportunities, supported by growing online sales, subscription models, and increasing adoption of connected pest-management solutions globally.

Market Dynamics

Drivers - Rising Home Gardening Trends Expanding Consumer Pesticide Demand Globally

The continued expansion of home gardening is a primary driver of gardening pesticide demand across residential markets. The National Gardening Association reports over 18.3 million new gardeners between 2020 and 2022, while the U.S. Bureau of Labor Statistics highlights average household spending on lawn and garden supplies exceeding US$ 503 in 2023, reflecting strong consumer engagement.

Simultaneously, urban horticulture trends such as balcony gardening, rooftop farming, and community plots are widening their application scope. The Royal Horticultural Society estimates nearly 30 million adults in the UK participate in gardening. This sustained involvement is boosting consistent demand for herbicides, insecticides, and fungicides used in both ornamental and edible plant care.

Climate Change Intensifying Pest Activity and Treatment Frequency

Climate variability is significantly increasing pest populations, creating sustained demand for gardening pesticides. The Food and Agriculture Organization indicates that climate change may drive up to 40% of new pest invasions globally. Additionally, the U.S. Environmental Protection Agency reports a 17% increase in residential pest-related service demand between 2018 and 2023.

Gardeners are facing broader exposure to pests such as aphids, whiteflies, and fungal infections beyond traditional regions. The spread of invasive species documented by CABI further intensifies treatment needs. These pressures are structurally increasing pesticide consumption while accelerating the adoption of more sustainable and environmentally compliant pest management solutions.

Restraints - Strict Regulatory Policies and Ingredient Restrictions Limiting Market Growth

Regulatory tightening across global markets is restricting the use of several conventional pesticide formulations. The European Commission has phased out multiple active ingredients, while France’s Labbé Law limits non-professional use of synthetic pesticides. These regulations significantly reduce product availability and increase compliance requirements for manufacturers operating in residential gardening segments.

Similarly, the U.S. Environmental Protection Agency has imposed restrictions on substances such as chlorpyrifos and neonicotinoids. Meeting evolving regulatory standards increases R&D costs and extends product approval timelines by up to 36 months. This creates barriers for smaller players and slows innovation, ultimately constraining overall market growth momentum.

Increasing Health and Environmental Concerns Reducing Chemical Adoption

Growing awareness of health and ecological risks linked to pesticide use is limiting demand for synthetic products. The World Health Organization estimates around 385 million unintentional pesticide poisoning cases annually, raising concerns among consumers. Environmental contamination and biodiversity loss are also influencing purchasing decisions and encouraging caution in pesticide application.

Research by the U.S. Geological Survey shows pesticide residues present in nearly 90% of water samples, while pollinator decline tracked by the USDA National Agricultural Statistics Service reinforces public concern. These factors are reducing repeat purchases of chemical pesticides and pushing demand toward safer alternatives.

Opportunities - Growing Adoption of Bio-Based and Organic Pest Control Solutions

The increasing shift toward bio-based pesticides presents a strong growth opportunity in the gardening pesticides market. The U.S. Environmental Protection Agency Biopesticide Division has approved over 390 active ingredients across more than 1,400 products, reflecting strong expansion. The Food and Agriculture Organization notes that biopesticides are growing at 15–17% annually.

Natural solutions derived from neem, pyrethrum, and Bacillus thuringiensis are gaining popularity among environmentally conscious consumers. Increasing willingness to pay a premium for organic-certified products is further accelerating adoption. This trend is expected to sustain double-digit growth, especially among home gardeners seeking safer and eco-friendly pest management alternatives.

Digital Platforms and Smart Gardening Enhancing Market Accessibility

Digitalization is transforming how gardening pesticides are marketed and distributed globally. The U.S. Census Bureau reported that online lawn and garden product sales grew by 11.4% in 2024, highlighting strong e-commerce expansion. Consumers increasingly prefer online platforms for product comparison, convenience, and subscription-based purchasing options.

Additionally, smart gardening technologies are improving pest management efficiency through data-driven insights. Integration of AI-based pest detection tools, connected devices, and mobile applications enables targeted pesticide usage. These innovations are enhancing customer engagement, improving product effectiveness, and creating recurring revenue streams for manufacturers investing in digital ecosystems.

Category-wise Analysis

Product Type Insights

Insecticides lead the product-type segment, accounting for approximately 38% market share in 2025. This dominance is driven by the wide range of pests encountered in home gardening, including aphids, caterpillars, whiteflies, mealybugs, and thrips, which require continuous management. The U.S. Environmental Protection Agency identifies insecticides as the most widely purchased category, while the U.S. Department of Agriculture highlights significant ornamental plant losses due to insect damage.

Bio-insecticides are emerging as the fastest-growing sub-segment within this category. Increasing demand for eco-friendly pest control and retailer expansion of organic product portfolios are driving adoption. Products based on Bacillus thuringiensis and plant-derived compounds are gaining popularity among environmentally conscious gardeners seeking safer and sustainable alternatives.

Source Insights

The chemical source segment dominates the market, holding an estimated 74% share in 2025. Synthetic pesticides continue to be preferred due to their rapid effectiveness, extended residual activity, and cost efficiency compared to organic alternatives. Widely used active ingredients such as pyrethroids, neonicotinoids, and carbamates maintain strong regulatory approvals from authorities, including the U.S. Environmental Protection Agency and European Food Safety Authority.

The organic source segment is witnessing the fastest growth, supported by increasing environmental awareness and sustainability trends. Microbial, botanical, and biochemical pesticides are gaining traction among consumers seeking low-toxicity solutions. Expanding organic certifications and retailer commitments toward eco-friendly products are further strengthening demand for these alternatives across developed markets.

Formulation Type Insights

Liquid formulations dominate the formulation segment with an estimated 42% share in 2025. Their popularity stems from ease of use, accurate dosing, and rapid absorption by plants, making them suitable for both residential and commercial gardening. The U.S. Environmental Protection Agency notes that liquid-based products account for a large share of residential pesticide registrations, reinforcing their widespread adoption.

Spray-based formats are the fastest-growing within this category, driven by convenience and targeted application benefits. Ready-to-use aerosol sprays are increasingly preferred for indoor plants and small gardening spaces. Manufacturers are expanding their portfolios with user-friendly solutions tailored to urban gardening needs and quick pest treatment requirements.

Distribution Channel Insights

Offline distribution channels hold the largest market share at approximately 71% in 2025. Physical retail outlets such as garden centers and hardware stores remain preferred due to immediate product availability, hands-on comparison, and in-store guidance. Major retailers like The Home Depot and Lowe's continue to dominate sales, supported by strong consumer trust and accessibility.

Online channels are the fastest-growing segment, driven by increasing digital adoption and convenience. E-commerce platforms and direct-to-consumer websites are expanding product reach, offering subscription models and fast delivery services. Growing consumer comfort with online purchasing is steadily reshaping distribution dynamics in the gardening pesticides market.

Regional Insights

North America Gardening Pesticides Market Trends and Insights

North America commands the leading regional position, accounting for nearly 34% of the global gardening pesticides market in 2025. The region benefits from high gardening participation rates, well-established big-box retail networks, and progressive EPA regulation that drives steady reformulation. Trends include rapid pivoting toward organic-certified products, smart-garden integrations, and rising demand for ready-to-use sprays among first-time gardeners.

- U.S. Gardening Pesticides Market Size

The United States represents approximately 84% of North America's gardening pesticides market and is valued at roughly US$ 2.7 billion in 2026. Strong household gardening culture, supported by the National Gardening Association's finding of 71.5 million participating households, and elevated retail penetration through chains such as Home Depot and Lowe's, anchors consistent demand and steady premium-segment expansion.

Europe Gardening Pesticides Market Trends and Insights

Europe is the second-largest market and is rapidly shifting toward bio-based formulations under the European Green Deal and Farm to Fork Strategy. Stringent restrictions on synthetic actives, sustained popularity of allotment gardening, and rising indoor-plant culture across Germany, France, and the U.K. drive structural change. Retailers are aggressively expanding natural and pet-safe pesticide assortments to align with EU regulations and evolving consumer preferences.

- Germany Gardening Pesticides Market Size

Germany leads continental Europe with roughly 19% share of the regional market, supported by the country's deeply rooted Schrebergarten allotment culture spanning over 900,000 plots, per the Bundesverband Deutscher Gartenfreunde. Demand for biopesticides is robust, with retailers such as OBI and Hornbach expanding eco-certified assortments to meet Bundesamt für Verbraucherschutz compliance requirements.

- U.K. Gardening Pesticides Market Size

The U.K. accounts for nearly 17% of Europe's gardening pesticides market in 2026. The Royal Horticultural Society reports the U.K. has more than 23 million active gardeners, and tightening HSE registrations have accelerated reformulations toward natural pyrethrins and neem-based products. Strong online sales via B&Q and Wickes further reinforce consistent demand momentum across categories.

- France Gardening Pesticides Market Size

France contributes around 14% of Europe's gardening pesticides market value, shaped heavily by the Labbé Law prohibiting synthetic pesticide sales for non-professional use. As a result, biopesticide adoption is among the highest in Europe. Retailers such as Truffaut and Jardiland are expanding microbial and botanical product ranges to support household gardeners transitioning to compliant, eco-certified alternatives.

Asia Pacific Gardening Pesticides Market Trends and Insights

Asia Pacific is the fastest-growing region with an expected CAGR of 8.1% during 2025-2032. Rapid urbanization, rising disposable incomes, and an explosion of balcony and rooftop gardening across China, India, and Southeast Asia underpin growth. China alone, according to the National Bureau of Statistics of China, has seen a 25% rise in urban household gardening since 2020, supported by domestic giants like Sinochem expanding consumer-grade portfolios.

- India Gardening Pesticides Market Size

India represents approximately 11% of the Asia Pacific's gardening pesticides market in 2026, with strong tailwinds from urban gardening movements in metros like Bengaluru, Mumbai, and Delhi. The Indian Council of Agricultural Research (ICAR) highlights rising demand for neem-based and microbial products, while domestic players such as UPL Limited and PI Industries are expanding home-garden SKUs to meet retail growth.

- Japan Gardening Pesticides Market Size

Japan accounts for nearly 18% of the Asia Pacific's gardening pesticides market in 2026, supported by an aging population with high gardening participation and rigorous Ministry of Agriculture, Forestry and Fisheries (MAFF) safety standards. Demand for compact, ready-to-use sprays is strong, and brands such as Sumitomo Chemical Garden drive recurring purchases through specialty centers and online platforms.

- Southeast Asia Gardening Pesticides Market Size

Southeast Asia contributes about 9% of Asia Pacific's gardening pesticides market in 2026, led by Indonesia, Thailand, and Vietnam. Tropical climates create high pest pressure on home gardens, while a growing middle class is driving spending. Local distributors and global brands like Syngenta are expanding their presence to serve the region's accelerating residential and ornamental gardening demand.

Competitive Landscape

The global gardening pesticides market is moderately consolidated, with a mix of established multinational players and numerous regional manufacturers catering to localized demand. Leading companies compete through strong research and development capabilities, expansion of bio-based product portfolios, eco-certifications, and digital advisory tools that help consumers select and apply products more effectively across residential and commercial gardening applications.

Key competitive strategies include retail collaborations, subscription-based replenishment models, and continuous reformulation of active ingredients to align with evolving environmental and safety regulations. Companies are increasingly focusing on sustainability-driven product innovation and integrated smart-gardening solutions, combining pest control with digital monitoring tools to enhance user experience and build long-term customer engagement.

Key Developments:

- In March 2025, Scotts Miracle-Gro launched a new line of OMRI-listed organic pest control sprays under its Natria brand, expanding its biopesticide portfolio to meet rising consumer demand for pet- and pollinator-safe gardening solutions across U.S. retailers.

- In November 2024, Bayer AG announced the global rollout of its Vynyty Citrus biological insecticide for home gardeners, leveraging pheromone-based pest control technology developed in partnership with EU research institutes.

- In July 2024, Syngenta acquired Intrinsyx Bio, a U.S.-based biopesticide innovator, to strengthen its bio-based residential and ornamental gardening pesticide pipeline and accelerate registrations under EPA's reduced-risk pathway.

Companies Covered in Gardening Pesticides Market

- Scotts Miracle-Gro Company

- Bayer AG

- Syngenta AG

- BASF SE

- Corteva Agriscience

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- UPL Limited

- Spectrum Brands Holdings, Inc. (Spectracide)

- Central Garden & Pet Company (AMDRO, Sevin)

- Bonide Products LLC

- Woodstream Corporation (Safer Brand)

- Neudorff GmbH KG

- Westland Horticulture Ltd.

- PI Industries Limited

- Nufarm Limited

- Certis Biologicals

- Marrone Bio Innovations

Frequently Asked Questions

The market is projected to reach US$ 9.6 billion in 2026 and grow to US$ 14.5 billion by 2033 at a CAGR of 6.1%.

Rising home gardening and urban horticulture, supported by millions of new gardeners and increasing climate-driven pest pressure, are the primary demand drivers globally.

North America leads with approximately 34% share, driven by strong gardening culture, advanced retail infrastructure, and regulatory innovation supported by the U.S. Environmental Protection Agency.

Bio-based pesticides and digital distribution channels present key opportunities, supported by sustainability trends, online sales growth, and integration of smart gardening technologies globally.

Leading players include Scotts Miracle-Gro, Bayer AG, Syngenta AG, BASF SE, Corteva Agriscience, FMC Corporation, and Sumitomo Chemical.