- Biotechnology

- Analytical Instrumentation Market

Analytical Instrumentation Market Size, Share, and Growth Forecast 2026 - 2033

Analytical Instrumentation Market by Product Type (Instruments, Services, Software), Technology (Polymerase Chain Reaction, Spectroscopy, Microscopy), Application (Life Sciences Research and Development), and Regional Analysis, 2026 - 2033

Analytical Instrumentation Market Size and Trends Analysis

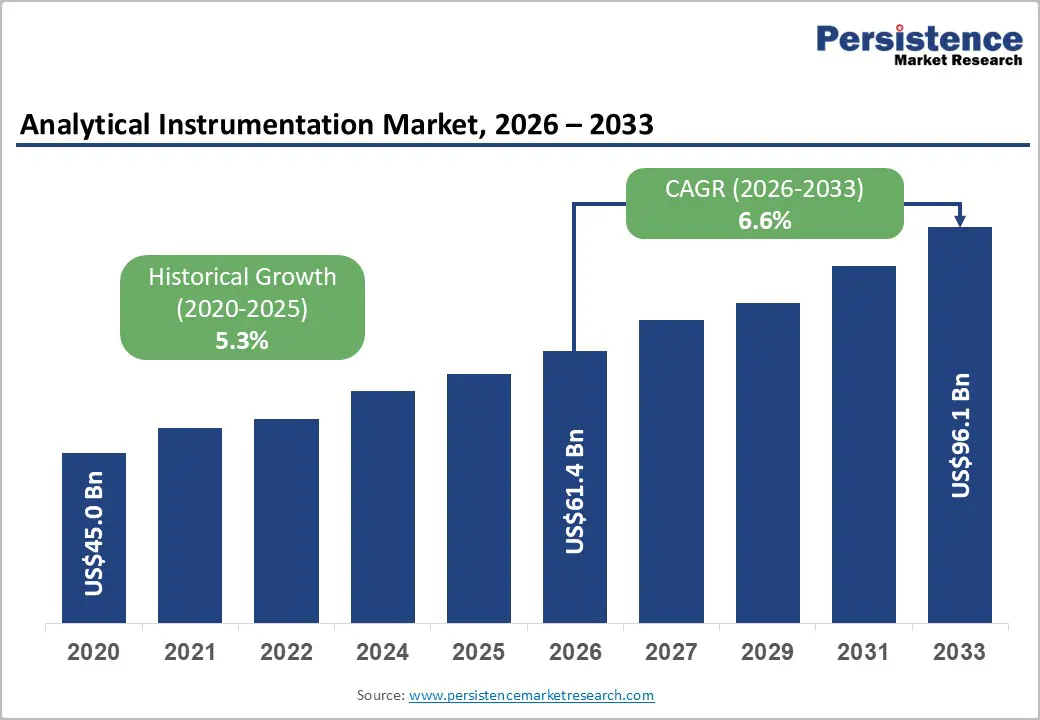

The global analytical instrumentation market size is likely to be valued at US$61.4 billion in 2026 and is expected to reach US$96.1 billion by 2033, growing at a CAGR of 6.6% during the forecast period from 2026 to 2033, driven by rising demand for advanced analytical technologies in pharmaceutical and biotechnology research.

Increasing adoption of automation and AI-assisted laboratory solutions and surging demand for stringent quality control across food safety, environmental monitoring, and clinical diagnostics are also predicted to spur the market.

Key Industry Highlights:

- Latest Acquisition: In March 2026, Agilent Technologies announced the acquisition of Biocare Medical in a US$950 million all-cash transaction. Agilent indicated that the addition of Biocare's tissue diagnostics portfolio, including antibodies and staining systems, would improve its life sciences and diagnostic instrumentation business and strengthen its position in pathology testing.

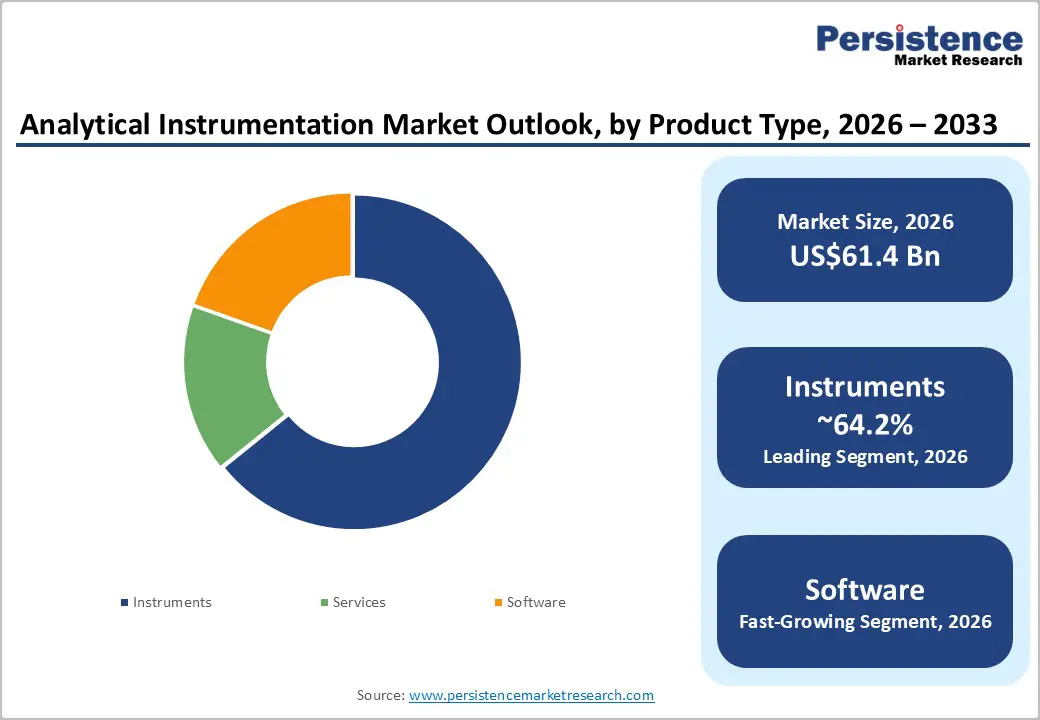

- Leading Product Type: Instruments, approximately 64.2% share in 2026, as they are essential for performing core analytical functions such as detection, separation, and quantification.

- Dominant Application: Life sciences research and development, nearly 49.8% share in 2026, owing to the continuous demand for analytical validation in drug discovery, biologics development, and clinical trials.

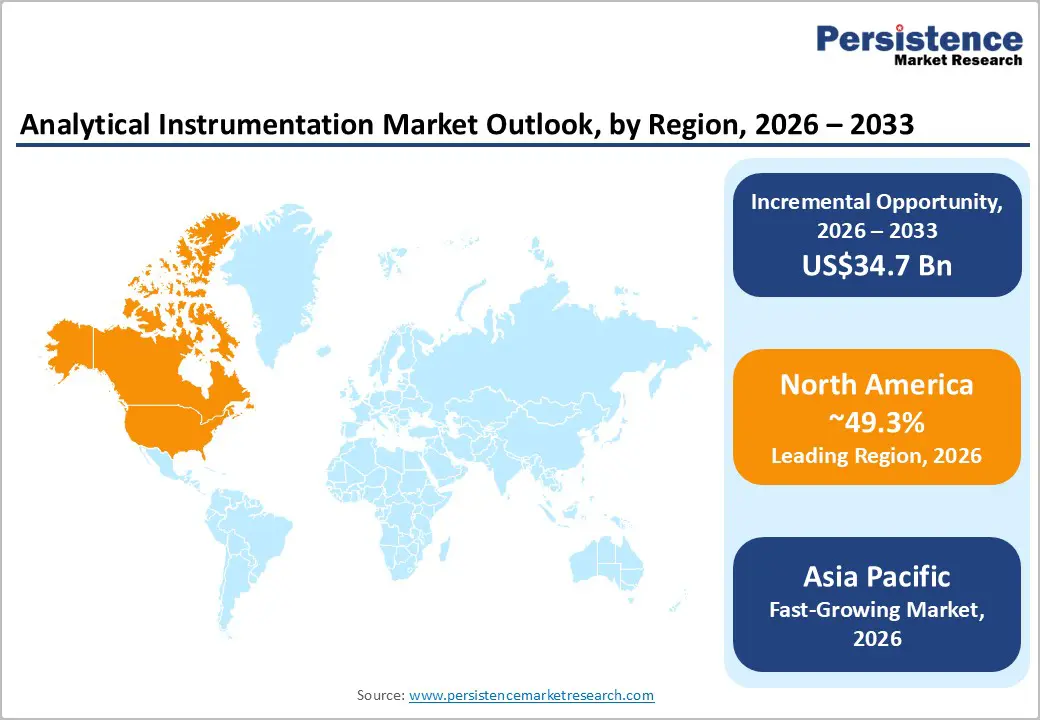

- Leading Region: North America, with about 49.3% share in 2026, backed by its well-established pharmaceutical and biotechnology hub.

- Fast-growing Region: Asia Pacific, owing to expanding pharmaceutical manufacturing in China and rising government investments in research infrastructure.

DRO Analysis

Driver - Strict Compliance Mandates from Global Regulators

Regulatory bodies are raising the bar on analytical validation requirements across industries. In March 2024, the Food and Drug Administration (FDA) published two final guidance documents, namely, ICH Q2(R2) and Q14, outlining principles for analytical procedure validation and harmonized scientific approaches for analytical procedure development, including risk-based post-approval change management. These guidelines now cover spectroscopic data and multivariate methods, which pushes labs to upgrade their instrumentation.

PIC/S guidelines PI-046-1 and Aide-Memoire PI-052-1 require validated sampling and analytical methods, with HPLC and other validated techniques, supported by scientifically justified acceptance criteria. For manufacturers, compliance is no longer a one-time checkbox. It demands continuous and instrument-supported monitoring across the entire product lifecycle.

Rise of Precision Medicine and Complex Biologics

The shift toward personalized therapies is creating high demand for sensitive and high-throughput analytical tools. In 2025, the FDA approved a personalized CRISPR therapy after a one-week review, marking a shift toward individualized N-of-1 therapies for ultra-rare diseases. These complex modalities require instruments capable of deep molecular characterization.

A study published in Nature Biotechnology reported a 40% increase in novel biomarker identification using multi-omic approaches. These integrate genomic, proteomic, and metabolomic data, all requiring high-sensitivity analytical platforms. As biologics pipelines grow in complexity, instruments that can handle multi-layer molecular profiling are becoming standard lab infrastructure.

Restraint - Shortage of Skilled Operators Limits Instrument Utilization

Advanced analytical instruments are only as effective as the people running them. The global lab industry is dealing with a persistent and worsening workforce gap. Over 30% of labs experience delays due to a lack of trained personnel, as these instruments require specialized knowledge for calibration, troubleshooting, and accurate data interpretation. The problem runs deeper than headcount.

The gap between demand and available lab professionals continues to widen, propelled by an aging workforce, an expansion of molecular diagnostics, and increasing regulatory requirements around data integrity. A 2020 American Society for Clinical Pathology (ASCP) vacancy survey showed an average five-year retirement rate of 12.3% across clinical labs, and replacement pipelines are not keeping up. With new platforms also requiring cross-disciplinary skills in data science, the barrier to effective instrument use is rising, further leading to underutilization, miscalibration, and avoidable downtime.

Opportunity - Emergence of Hyphenated and Multi-Modal Systems

Rather than running separate tests across multiple instruments, labs are now turning to coupled analytical systems that deliver rich data in a single workflow. Techniques such as LC-MS, GC-MS, LC-NMR, CE-MS, and SFC-MS have seen surging adoption in drug discovery, impurity profiling, bioanalysis, and quality control over the past two decades. Recent advances include miniaturized systems, green chemistry techniques, and AI-based data processing.

A 2025 review in Analytical Science Advances (Wiley) confirmed that LC-MS/MS and GC-MS/MS deliver high throughput, minimal sample preparation, and exceptional sensitivity and specificity, making them essential in food and pharmaceutical laboratories worldwide. The direction is toward multi-dimensional and hyphenated platforms that replace sequential single-technique runs with integrated, high-confidence results.

Launch of Next-Generation High-Resolution Mass Spectrometry

High-resolution mass spectrometry is moving beyond niche research use into mainstream biopharma and omics workflows. In June 2025, Thermo Fisher Scientific launched two new Orbitrap instruments at ASMS 2025. The Orbitrap Astral Zoom MS is designed to enable a new strategy for early detection and precision oncology. It provides greater depth and coverage for biomarker discovery and clinical research translation.

On the biopharma side, the Orbitrap Excedion Pro is the first platform to combine next-generation Orbitrap hybrid mass spectrometry with alternative fragmentation technologies. It is specifically designed to efficiently analyze complex biomolecules for biological drug development. These launches reflect an industry push toward fast scan rates, high sensitivity, and multi-omics-ready platforms that compress discovery timelines for complex therapeutics.

Category-wise Analysis

Product Type Insights

Instruments are predicted to lead with a share of approximately 64.2% in 2026, as they form the foundation of every analytical workflow. Software and services cannot generate results unless laboratories first invest in core equipment such as chromatography systems, mass spectrometers, spectrophotometers, electron microscopes, and elemental analyzers. These instruments perform the actual detection, separation, identification, and quantification of samples. It makes them indispensable across pharmaceutical, biotechnology, food safety, environmental, and semiconductor industries.

The software segment is estimated to be the fastest-growing over the forecast period, as laboratories are generating far more data than they can manage manually. Modern analytical instruments can produce millions of data points in a single experiment. Laboratories increasingly require software for data processing, workflow automation, regulatory compliance, and AI-assisted interpretation.

Application Insights

The life sciences research and development segment is anticipated to dominate with a share of nearly 49.8% in 2026, as nearly every stage of biological and pharmaceutical research depends on analytical instruments. Scientists use these tools to study proteins, genes, metabolites, cells, antibodies, and drug compounds. Without analytical instrumentation, modern drug discovery and biotechnology research would be impossible.

The clinical and diagnostics analysis segment is expected to remain in the second position in 2026, as healthcare providers increasingly rely on analytical instruments to detect diseases earlier and improve treatment decisions. Hospitals, diagnostic laboratories, and research centers use analytical systems for molecular diagnostics, biomarker detection, infectious disease testing, cancer screening, and genetic analysis.

Regional Insights

North America Analytical Instrumentation Market Trends

North America is expected to maintain its leading position in 2026, accounting for approximately 49.3% of the market share. This dominance is supported by strong investments in research and development, a well-established pharmaceutical and biotechnology ecosystem, and the presence of several leading life sciences instrument manufacturers. Demand for life sciences instrumentation continues to rise due to expanding applications in pharmaceutical research, bioprocessing, and clinical diagnostics.

The region’s leadership is further reinforced by stringent regulatory requirements. Ongoing efforts by the U.S. Food and Drug Administration (FDA) to strengthen quality and compliance standards are encouraging laboratories to regularly upgrade and modernize their analytical equipment. In April 2025, Roche announced plans to invest US$50 billion in pharmaceuticals and diagnostics operations across the United States over the next five years. The investment will support research and development expansion, manufacturing capacity enhancements, and clinical trial activities, which is expected to drive additional demand for advanced analytical instruments.

U.S. Analytical Instrumentation Market Trends

In 2026, the U.S. is anticipated to hold a regional share of nearly 67.4%, backed by the volume and velocity of its drug pipeline. In 2024, the FDA approved 50 novel molecular entities, with around one-third in oncology and hematology alone. Each approval cycle requires exhaustive analytical work at the discovery, development, and manufacturing stages. The FDA anticipated as many as 20 new cell and gene therapies to reach the market annually by 2025, while more than 200 investigational new drug applications are currently in the pipeline. This creates a sustained pull for advanced analytical platforms.

Asia Pacific Analytical Instrumentation Market Trends

Asia Pacific is anticipated to be the fastest-growing region in 2026 with a share of nearly 24.6%, as multiple large economies are simultaneously extending their pharma, biotech, and environmental sectors. The region is also expected to be driven by ongoing industrialization and expansion of the pharmaceutical and biotechnology industries. Infrastructure investments are keeping pace. In March 2024, SGS opened a new bioanalysis center in Shanghai featuring triple-quad LC-MS/MS and MSD platforms. In August 2025, Agilent Technologies inaugurated a new biopharma experience center in Hyderabad, India. It is equipped with chromatography, mass spectrometry, and cell analysis tools.

China Analytical Instrumentation Market Trends

China’s regional share of nearly 32.1% in 2026 is associated with its rapidly maturing biopharma industry. The country is attracting large global pharma investments. In March 2025, AstraZeneca announced a US$2.5 billion investment in Beijing to establish its sixth global strategic research and development center, alongside manufacturing and research agreements with multiple China-based biotechs. Drug development is accelerating too. In 2023, China had five first-in-class domestic drug approvals, compared to just two total before 2013.

As of June 2025, investment bank Stifel projected that the country would be responsible for 37% of molecules licensed by large pharmaceutical companies in 2025. This rise in novel drug activity requires more sophisticated analytical tools throughout the development chain.

Japan Analytical Instrumentation Market Trends

Japan is predicted to account for a regional share of around 28.5% in 2026, supported by a structural advantage, i.e., the world's oldest population. Public funding is also rising. According to data from the Japan Analytical Instruments Manufacturers' Association (JAIMA), the market posted a total production value of approximately US$4.7 billion in 2024. In the fiscal year 2026 budget proposal, Japan's science and research funding reached nearly ¥36.7 trillion (US$245 billion), a 6.7% increase from the previous year. The country is also a market leader in diagnostic imaging, with the aging population and rising prevalence of neurological diseases such as Alzheimer's. It is propelling demand for advanced In Vitro Diagnostic (IVD) instruments and high modalities.

Europe Analytical Instrumentation Market Trends

Europe will likely see steady growth over the forecast period with a share of nearly 17.9% in 2026, fueled by pharmaceutical innovation and strict environmental regulation. According to Eurostat data from 2024, the continent hosts more than 2,500 public research institutions and employs over 300,000 researchers in higher education. The EU's Zero Pollution Action Plan is augmenting adoption of analytical tools such as ion chromatography and ICP-OES for monitoring nitrates and phosphates. The 2024 revision of the Industrial Emissions Directive also introduced strict monitoring obligations across manufacturing sectors.

Germany Analytical Instrumentation Market Trends

Germany will likely dominate Europe in 2026 by generating a regional share of approximately 38.8%, backed by its dominant chemical sector, a productive pharma manufacturing base, and superior public research and development support. Government initiatives such as the High-Tech Strategy 2025 aim to strengthen Germany's position in global research and innovation, further supporting sustained demand for life science analytical instruments. Environmental goals are adding to instrument demand too. The country is targeting 80% renewable electricity by 2030, which requires rigorous analytical testing across energy and industrial applications.

U.K. Analytical Instrumentation Market Trends

A share of nearly 19.2% is expected to be held by the U.K. in 2026, attributed to a well-established biotech cluster and National Health Service (NHS)-backed data-driven healthcare initiatives. Domestic instrument makers such as Malvern Panalytical and Oxford Instruments contribute to a competitive edge. The NHS's push for personalized medicine and AI-integrated diagnostics is creating fresh demand for molecular-level analytical tools. This trend complies well with the U.K.'s strength in genomics research and the life sciences corridor around Cambridge and London.

Competitive Landscape

The global analytical instrumentation market is moderately consolidated with a handful of multinational companies controlling a large share of high-end chromatography, spectroscopy, mass spectrometry, and molecular analysis systems. Leading companies include Thermo Fisher Scientific, Agilent Technologies, Danaher Corporation, Waters Corporation, Shimadzu Corporation, and Bruker Corporation, which collectively account for a substantial portion of global revenue.

Competition is no longer based solely on instrument performance. Vendors are now competing through integrated ecosystems that combine instruments, software, automation, consumables, data analytics, and service contracts. This strategy creates long-term customer retention, especially among pharmaceutical, biotechnology, semiconductor, and environmental testing laboratories. AI-enabled workflow optimization, predictive maintenance, and laboratory automation have become key differentiators.

Key Industry Developments:

- In January 2026, Velaris acquired Markes International, a specialist in gas chromatography and GC-MS sample preparation technologies. Velaris stated that the acquisition would strengthen its laboratory automation portfolio and broaden capabilities in thermal desorption, sample concentration, and volatile organic compound analysis.

- In May 2025, Waters completed the acquisition of Halo Labs for approximately US$35 million. The company noted that the acquisition supports its strategy of extending analytical solutions for emerging biologics, including CAR-T cell therapies and advanced biopharmaceutical manufacturing.

- In February 2025, Paeonia Industries acquired Savant Group, a provider of analytical testing equipment and lubricant analysis technologies. The acquisition was intended to expand Paeonia's scientific instrumentation footprint in North America and strengthen its testing and research capabilities for industrial applications.

Companies Covered in Analytical Instrumentation Market

- Thermo Fisher Scientific, Inc.

- Waters Corp.

- Shimadzu Corp.

- Danaher

- Agilent Technologies, Inc.

- Bruker Corp.

- PerkinElmer, Inc.

- Mettler Toledo

- Zeiss Group

- Bio-Rad Laboratories, Inc.

- Illumina, Inc.

- Eppendorf SE

- F. Hoffmann-La Roche AG

- Sartorius AG

- Avantor, Inc.

- Others

Frequently Asked Questions

The global analytical instrumentation market is projected to be valued at US$61.4 billion in 2026.

The market is expected to reach US$96.1 billion by 2033.

Key market trends include integration of AI and automation in laboratories and surging adoption of cloud-based analytical software.

Instruments are expected to be the leading product type with a share of nearly 64.2% in 2026, as laboratories continue upgrading to high-precision systems to handle complex biologics, gene therapies, and advanced material analysis.

The market is expected to grow at a CAGR of 6.6% from 2026 to 2033.

Thermo Fisher Scientific, Inc., Waters Corp., Shimadzu Corp., and Danaher are a few key market players.