- Biotechnology

- Cell Lysis and Disruption Market

Cell Lysis and Disruption Market Size, Share, and Growth Forecast, 2026 – 2033

Cell Lysis and Disruption Market by Product Type (Instruments, Reagents & Consumables, Kits & Reagents), Cell Type (Mammalian Cells, Bacterial Cells, Others), Application (Protein Isolation, Downstream Processing, Others), and Regional Analysis for 2026 - 2033

Cell Lysis and Disruption Market Share and Trends Analysis

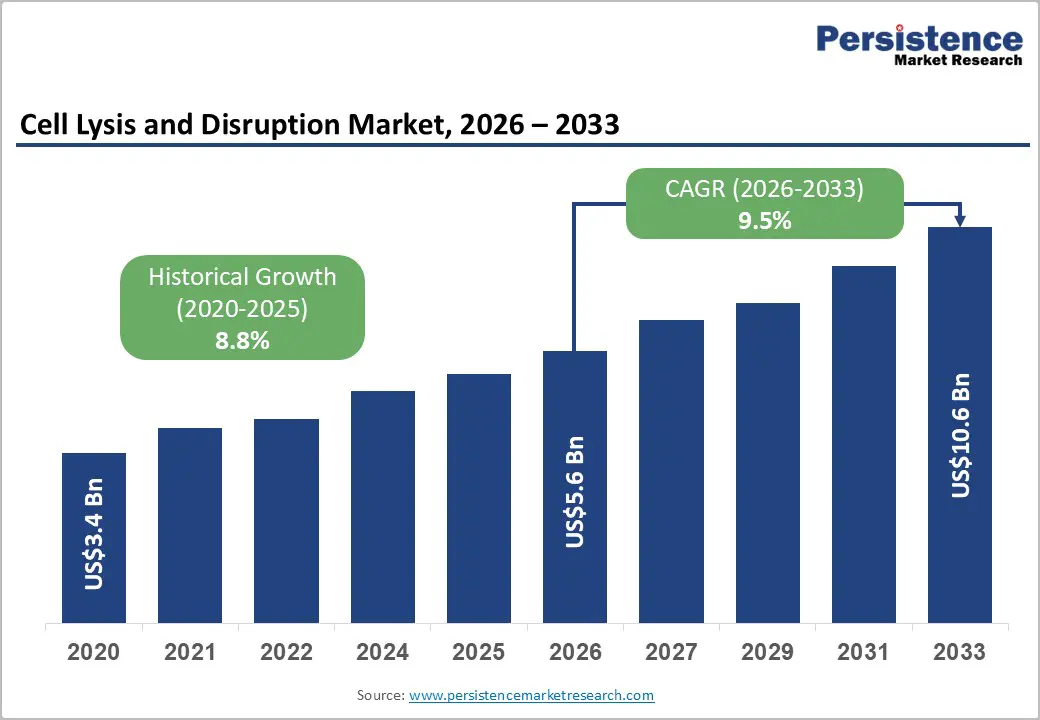

The global cell lysis and disruption market size is likely to be valued at US$5.6 billion in 2026 and is estimated to reach US$10.6 billion by 2033, growing at a CAGR of 9.5% during the forecast period from 2026 to 2033, driven by expanding biopharmaceutical production, rising genomic research activity, and increasing demand for precision diagnostic workflows.

Cell lysis and disruption market expansion reflects rapid adoption of automated sample preparation systems across biotechnology laboratories and clinical research facilities. Regulatory emphasis on biologics quality control and vaccine manufacturing efficiency continues to accelerate investment in high-throughput processing infrastructure.

Key Industry Highlights:

- Leading Product Type: Instruments are projected to hold around 41% revenue share in 2026, driven by increasing laboratory automation adoption.

- Fastest-Growing Product Type: Kits & reagents are forecast to record the fastest growth, driven by expanding molecular diagnostics applications.

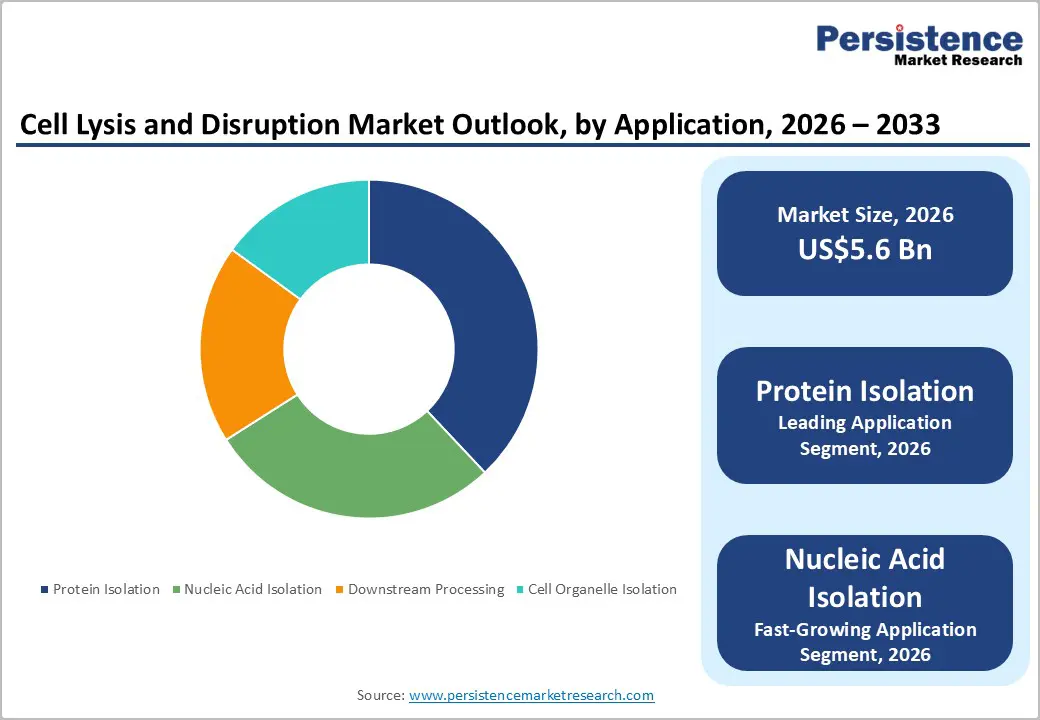

- Leading Application: Protein isolation is estimated to capture nearly 38% revenue share in 2026, driven by rising proteomics and biologics research.

- Fastest-Growing Application: Nucleic acid isolation is projected to witness the fastest growth, driven by genomic sequencing expansion.

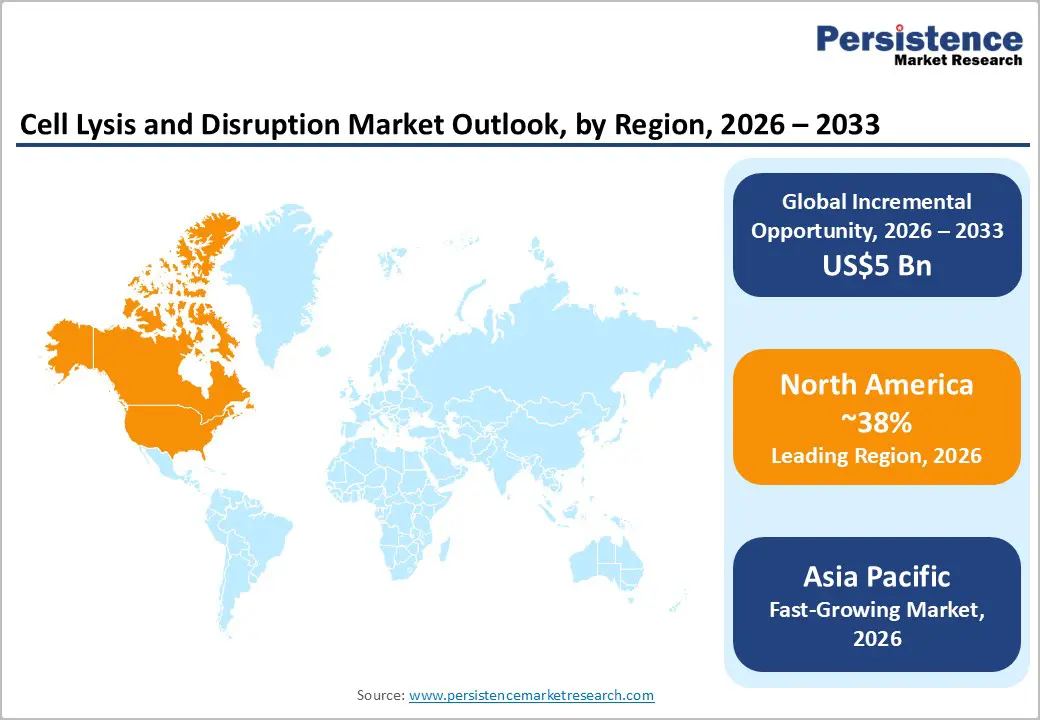

- Regional Leadership: North America is expected to secure approximately 38% market share in 2026, driven by advanced biopharmaceutical infrastructure.

- Competitive Environment: The market reflects a moderately fragmented structure, with Thermo Fisher Scientific, Danaher Corporation, and QIAGEN focusing on automation and consumable expansion.

DRO Analysis

Driver - Rising Adoption of Genomic Sequencing and Molecular Diagnostics

Rapid growth in genomic sequencing and molecular diagnostics has intensified the requirement for efficient nucleic acid extraction technologies. Cell disruption systems support sample preparation accuracy, influencing sequencing quality and diagnostic reliability. Rising adoption of precision medicine and companion diagnostics has accelerated laboratory spending on standardized extraction workflows. Research institutions are expanding investment in automated molecular biology laboratories, increasing procurement of specialized consumables and extraction reagents. Advanced cell disruption technologies are gaining wider implementation across oncology and infectious disease testing environments.

The National Institutes of Health allocated more than US$48 billion toward biomedical research programs during 2025, strengthening infrastructure for genomics and translational medicine initiatives. Expanded funding has increased procurement of sample preparation instruments across academic laboratories and clinical research centers. Higher sequencing volumes and biomarker discovery programs are generating sustained demand for scalable lysis solutions compatible with high-throughput molecular analysis platforms.

Restraint - High Cost Structure Associated with Automated Systems

Advanced disruption instruments involve significant capital investment, limiting adoption among small research laboratories and emerging biotechnology firms. Integration of automation features, contamination control mechanisms, and precision monitoring systems increases procurement expenses. Elevated maintenance requirements and consumable dependency reduce operational flexibility, creating pressure on laboratory budgets and limiting scalability across cost-sensitive environments.

Supply chain volatility affecting specialized reagents and laboratory plastics has increased production costs for manufacturers. Procurement delays for electronic components and precision engineering materials have constrained instrument availability, extending replacement cycles across laboratories. Margin pressure has intensified among mid-sized suppliers attempting to balance pricing competitiveness with expanding manufacturing and regulatory compliance costs.

Opportunity - Expansion of Cell and Gene Therapy Manufacturing

Cell and gene therapy commercialization is creating a strong demand for highly controlled extraction and disruption workflows capable of preserving biomolecule stability. Therapeutic development pipelines increasingly require scalable processing systems supporting viral vector production, engineered cell manufacturing, and genomic characterization. Companies investing in automated bioprocessing infrastructure can capitalize on expanding clinical trial activity and regulatory approvals linked to advanced therapeutic products.

Biotechnology companies are strengthening partnerships with automation providers to improve throughput efficiency and analytical consistency. Integration of closed-system processing technologies can reduce contamination risk while supporting regulatory compliance in cell therapy production facilities. Demand for customized reagent formulations and single-use processing components is expected to accelerate as clinical-stage manufacturing scales toward commercial production capacity.

Category-wise Analysis

Product Type Insights

Instruments are anticipated to secure around 41% of the cell lysis and disruption market share in 2026, reflecting increasing automation demand across biopharmaceutical and genomic laboratories. High-throughput extraction systems improve workflow reproducibility and contamination control during downstream analysis. Thermo Fisher Scientific introduced automated sample preparation solutions for molecular biology workflows, strengthening instrument adoption.

Kits & reagents are expected to be the fastest-growing segment, propelled by expanding molecular diagnostics and nucleic acid extraction applications across research institutions and healthcare laboratories. Single-use reagent systems simplify workflow integration and reduce sample handling complexity in decentralized testing facilities. QIAGEN expanded genomic sample preparation kits for sequencing applications, accelerating commercial adoption.

Cell Type Insights

Mammalian cells are poised to dominate with a forecast market share of over 46% in 2026, powered by expanding monoclonal antibody production and regenerative medicine research activities globally. These cells require controlled extraction workflows to preserve protein integrity during downstream analysis and therapeutic manufacturing. Merck KGaA expanded bioprocessing solutions supporting mammalian cell culture workflows.

Plant cells are estimated to be the fastest-growing segment, fueled by increasing agricultural biotechnology and plant-based pharmaceutical research programs worldwide. Complex plant cell wall structures require specialized disruption technologies capable of improving nucleic acid and protein extraction efficiency. Agilent Technologies expanded its molecular biology solutions supporting plant genomics applications.

Application Insights

Protein isolation is likely to be the leading segment with a projected 38% of the cell lysis and disruption market share in 2026 due to expanding proteomics research and biologics production requirements globally. Efficient protein extraction workflows support drug discovery, biomarker identification, and therapeutic manufacturing activities. Bio-Rad Laboratories introduced enhanced protein analysis preparation systems for research applications.

Nucleic acid isolation is anticipated to be the fastest-growing segment, fueled by accelerating genomic sequencing and molecular diagnostics adoption across clinical and research laboratories globally. Efficient extraction technologies improve sequencing reliability and diagnostic precision in oncology and infectious disease applications. Roche expanded its molecular diagnostic infrastructure to support automated nucleic acid workflows.

Regional Insights

North America Cell Lysis and Disruption Market Trends

North America is expected to lead with an estimated 38% share in 2026, supported by large-scale biologics manufacturing, advanced genomic research infrastructure, and rapid laboratory automation adoption. Strong investments in precision medicine and molecular diagnostics are increasing the deployment of automated extraction systems across pharmaceutical and biotechnology facilities.

U.S. Cell Lysis and Disruption Market Insights

The U.S. is projected to account for nearly 85% of North America's market share in 2026, supported by extensive biotechnology research funding and strong biologics production infrastructure. The National Institutes of Health continues to support genomic sequencing and translational medicine initiatives, increasing procurement of automated extraction platforms.

Canada Cell Lysis and Disruption Market Insights

Canada is expected to contribute around 15% of North America's revenue share in 2026, driven by increasing biotechnology investments and healthcare research modernization programs. Government-supported life sciences expansion is encouraging adoption of advanced molecular biology workflows across academic and diagnostic laboratories.

Europe Cell Lysis and Disruption Market Trends

Europe is projected to capture around 27% of the global market share in 2026, due to strong pharmaceutical manufacturing infrastructure and expanding precision healthcare initiatives. Regulatory focus on biologics safety and advanced therapeutic production is increasing the implementation of automated extraction technologies across research and industrial facilities.

Germany Cell Lysis and Disruption Market Insights

Germany is projected to account for approximately 24% of Europe’s revenue in 2026, supported by its well-established industrial biotechnology sector and robust pharmaceutical manufacturing base. Ongoing investments in vaccine production facilities and biologics research infrastructure are driving demand for automated sample preparation and extraction technologies. Additionally, Sartorius AG continues to enhance its bioprocessing portfolio, supporting protein extraction, purification, and downstream processing applications across the biotechnology industry.

U.K. Cell Lysis and Disruption Market Insights

The U.K. is projected to account for approximately 18% of the European market in 2026, driven by the continued expansion of genomic medicine and oncology diagnostics programs. Government-backed precision healthcare initiatives are accelerating the adoption of laboratory automation technologies across clinical, academic, and research settings. Furthermore, Oxford Nanopore Technologies and Bio-Rad Laboratories are advancing sequencing and molecular analysis capabilities, supporting the growing demand for efficient and high-throughput diagnostic workflows.

Asia Pacific Cell Lysis and Disruption Market Trends

Asia Pacific is forecast to be the fastest-growing region in 2026, stimulated by expanding biotechnology manufacturing capacity and rising healthcare research investment. Pharmaceutical outsourcing growth and vaccine production expansion are increasing the adoption of automated disruption systems and reagent technologies.

China Cell Lysis and Disruption Market Insights

China is projected to contribute around 32% of Asia Pacific's revenue share in 2026, driven by strong domestic biologics manufacturing expansion and genomic research investment. Government-backed biotechnology development initiatives are increasing the procurement of molecular biology automation systems across pharmaceutical and academic institutions. WuXi AppTec and BGI Genomics are strengthening sequencing and sample preparation capabilities supporting high-throughput workflows.

India Cell Lysis and Disruption Market Insights

India is projected to account for approximately 16% of Asia Pacific revenue in 2026, driven by the growth of biosimilar production and increasing investments in biotechnology research. Ongoing expansion of government-supported biotechnology parks and genomic sequencing programs is fostering greater adoption of advanced extraction technologies across the sector. Additionally, companies such as Biocon Limited and Syngene International are strengthening the country's biotechnology ecosystem through continued investments in biologics manufacturing and molecular diagnostics capabilities.

Competitive Landscape

The global cell lysis and disruption market is moderately fragmented, with competition shaped by automation capabilities, reagent portfolio expansion, and downstream processing integration strategies. Major participants include Thermo Fisher Scientific, Danaher Corporation, Merck KGaA, Bio-Rad Laboratories, and QIAGEN. Companies are prioritizing scalable extraction technologies supporting genomics, proteomics, and biopharmaceutical manufacturing applications across high-throughput laboratory environments.

Strategic competition is increasing through product innovation, collaborative research partnerships, and manufacturing expansion initiatives. Companies are strengthening recurring revenue generation through consumable and reagent portfolio development aligned with automated laboratory workflows. Integration of artificial intelligence, contamination control systems, and digital monitoring technologies is reshaping competitive positioning across molecular biology and biotechnology processing applications.

Key Industry Developments:

- In April 2026, Ferrotec introduced Ferrobeads DNA/RNA isolation kits featuring high-efficiency magnetic bead-based technology to improve nucleic acid extraction yield, scalability, and workflow flexibility across manual and automated molecular biology applications.

- In November 2025, QIAGEN unveiled QIAsymphony Connect at AMP 2025, introducing a next-generation automated nucleic acid purification platform designed to enhance sample traceability, increase throughput, and improve workflow efficiency for precision oncology and genomic research applications.

- In April 2025, QIAGEN expanded its digital PCR portfolio by launching new cell and gene therapy-focused assays and kits, strengthening biopharma quality control and improving precise nucleic acid quantification for advanced therapeutic manufacturing workflows.

Companies Covered in Cell Lysis and Disruption Market

- Thermo Fisher Scientific

- Danaher Corporation

- Merck KGaA

- Bio-Rad Laboratories

- QIAGEN

- Sartorius AG

- Agilent Technologies

- Roche

- Becton, Dickinson and Company

- PerkinElmer

- Miltenyi Biotec

- Takara Bio Inc.

- Promega Corporation

- Bio-Techne Corporation

- Lonza Group

Frequently Asked Questions

The global cell lysis and disruption market is projected to reach US$5.6 billion in 2026.

Expansion of biopharmaceutical manufacturing infrastructure, increasing genomic and proteomics research activity, and rising adoption of automated laboratory workflows across diagnostic and therapeutic development applications are driving growth.

The cell lysis and disruption market is poised to witness a CAGR of 9.5% from 2026 to 2033.

Expansion of cell and gene therapy manufacturing, integration of artificial intelligence-enabled laboratory automation systems, and increasing demand for high-throughput molecular diagnostics and precision medicine workflows are creating significant growth opportunities.

Some of the key market players include Thermo Fisher Scientific, Danaher Corporation, Merck KGaA, Bio-Rad Laboratories, and QIAGEN.