- Technology

- In-memory Computing Market

In-memory Computing Market Size, Share, and Growth Forecast 2026–2033

In-memory Computing Market by Component (Solution, Services), by Deployment (On-premises, Cloud-based, Hybrid), Application (Real-time Data Processing & Analytics, Predictive Analysis, Financial & Risk Analytics, Image & Video Processing, Supply Chain Management, Route Optimization, Customer & Business Intelligence, Others), Vertical and Regional Analysis, 2026–2033

Global In-memory Computing Market Size and Trend Analysis

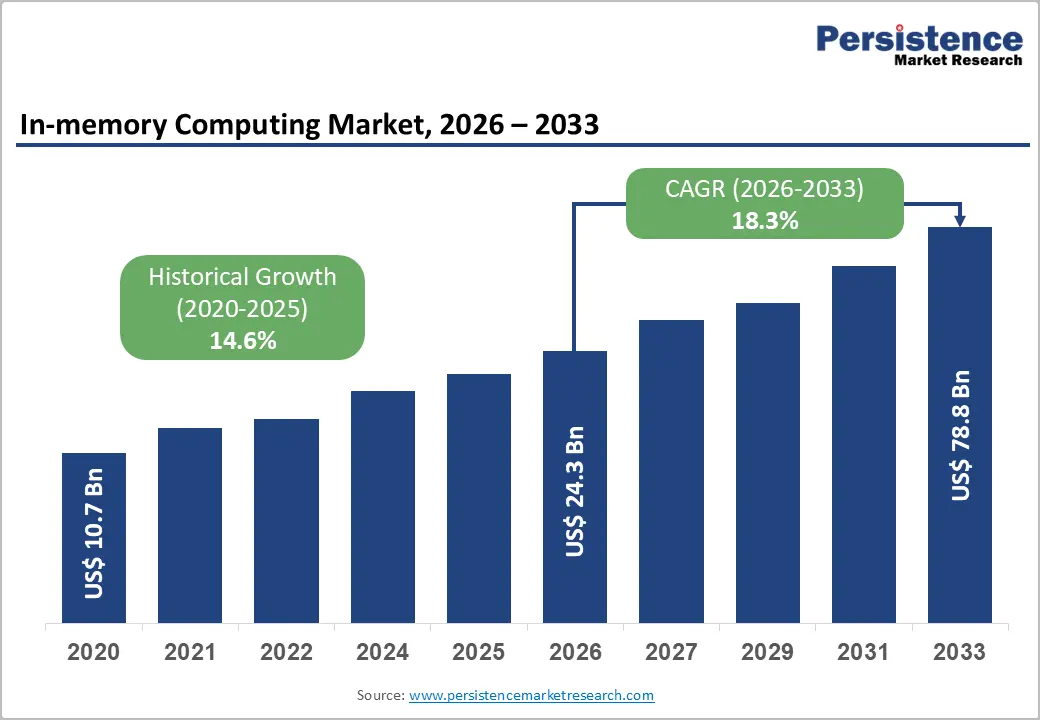

The global in-memory computing market is expected to be valued at US$ 24.3 billion in 2026 and is projected to reach US$ 78.8 billion by 2033, growing at a CAGR of 18.3% between 2026 and 2033 due to enterprise demand for ultra-low-latency data processing that traditional disk-based architectures can no longer support. Workloads such as algorithmic trading, real-time fraud detection, and AI inference increasingly require sub-millisecond response times. Conventional storage-centric systems create performance bottlenecks that are incompatible with these latency-sensitive use cases. Enterprises are shifting toward RAM-resident, in-memory computing architectures to enable real-time decision-making at scale.

Key Industry Highlights:

- Leading Offering: Solutions are likely to account for over 74% share in 2026, valued at more than US$ 17.98 billion, driven by demand for bundled platforms combining data grids, caching layers, and real-time analytics engines. These solutions reduce architectural complexity, improve scalability, and support mission-critical workloads such as trading systems, telecom operations, and real-time inventory management.

- Leading Deployment: Cloud-based deployments are poised for over 47% share in 2026, exceeding US$ 11.42 billion, driven by elastic scalability, on-demand provisioning, and global accessibility.

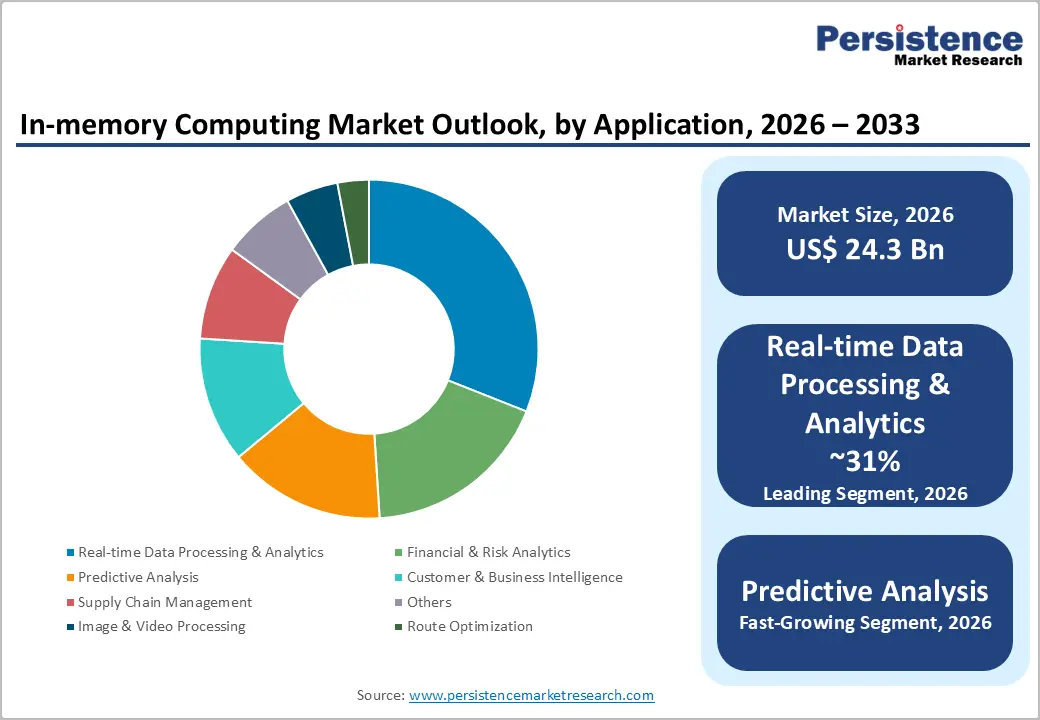

- Leading Application: Real-Time Data Processing & Analytics holds over 31.0% share in 2026, surpassing US$ 7.53 Billion, driven by high-frequency trading, fraud detection, and real-time bidding systems requiring instant decision-making from live data streams.

- Fast-Growing Application: Predictive Analytics is expanding due to the shift from batch processing to continuous AI inference, enabling real-time model scoring for credit risk, personalization, and dynamic enterprise decision systems.

- Leading Vertical: IT & Telecom accounts for over 22% share in 2026, reaching US$ 5.35 Billion, driven by real-time network orchestration, billing systems, and massive-scale event processing across distributed telecom infrastructure.

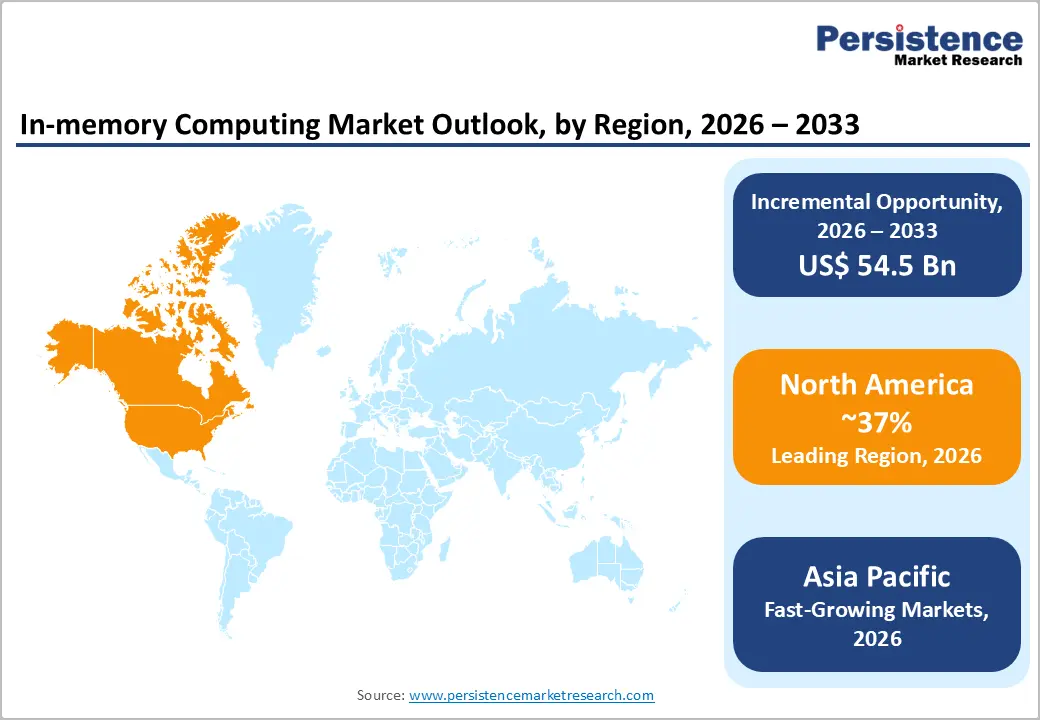

- Leading Region: North America holds over 37.0% market share in 2026, valued at US$ 8.99 billion, driven by hyperscaler dominance, AI-native enterprise ecosystems, and algorithmic trading infrastructure.

- Fastest-Growing Region: Asia Pacific expands at a CAGR of 22.9%, reaching US$ 6.56 Billion, fueled by digital payments expansion, 5G rollout, smart city initiatives, and large-scale AI deployment across China, India, Japan, and South Korea.

Market Dynamics

Drivers - Proliferation of Real-Time AI Inferencing Workloads Demanding Sub-Millisecond Data Access

The rapid scaling of AI inferencing for large language models, vector search, and edge AI is driving strict latency requirements, often below 10–50 milliseconds for real-time decisioning and even sub-millisecond thresholds in high-frequency systems. Traditional disk-based databases are increasingly inadequate, as memory-based access can be 10–100x faster than SSD-based retrieval paths, strengthening adoption of in-memory computing architectures. In regulated sectors such as banking and healthcare, the need for real-time explainability and auditability further increases reliance on continuously accessible data structures. As AI workloads transition from pilot deployments to production-scale systems, in-memory computing becomes a foundational layer for real-time inference pipelines.

Hyperscaler Investments in Distributed In-Memory Architecture for Cloud-Native Workloads

The shift toward cloud-native architectures is accelerating the adoption of managed in-memory services, particularly as over 60–70% of large enterprises are now estimated to be running multi-cloud or cloud-native workloads. Hyperscalers such as AWS, Microsoft Azure, and Google Cloud have expanded managed Redis and in-memory caching offerings to support low-latency, globally distributed applications.

These services enable sub-second response times for session management, personalization, and real-time analytics, which are critical for modern digital platforms. The move toward microservices and distributed systems further increases dependency on memory-centric data layers for state management. Combined with consumption-based pricing models, these developments are structurally expanding enterprise adoption of in-memory computing across transactional and analytical workloads.

Restraints - High Total Cost of Ownership for Large-Scale In-Memory Deployments

DRAM-intensive architecture imposes a hardware cost premium that compresses return-on-investment timelines, particularly for mid-market enterprises whose workloads do not generate sufficient latency-sensitive transaction volumes to justify the capital outlay. Enterprise-grade DRAM modules command a cost per gigabyte approximately 8–12 times that of NVMe SSD storage, and the JEDEC Solid State Technology Association's standards roadmap confirms that this gap will narrow only modestly through 2027, sustaining a structural barrier for budget-constrained buyers. New entrants face acute exposure here because incumbents with amortised infrastructure and multi-year vendor contracts can absorb memory cost volatility that would be catastrophic for challengers operating on thinner margins.

Data Security and Sovereignty Compliance Complexity Across Jurisdictions

In-memory architectures that hold sensitive datasets persistently in volatile RAM create novel compliance obligations under data residency frameworks, due to encryption-at-rest controls designed for disk-based systems do not map cleanly onto memory-resident processing pipelines. The General Data Protection Regulation (GDPR), enforced by the European Data Protection Board, and the People's Republic of China's Personal Information Protection Law (PIPL) enacted in 2021, both impose data localisation requirements that force vendors to architect geographically segmented memory clusters, adding approximately 15–25% to infrastructure deployment costs per jurisdiction. Vendors with established multi-region compliance frameworks hold a measurable competitive advantage over new entrants who must build these capabilities from scratch.

Opportunities - AI-Augmented Predictive Analytics in Healthcare and Life Sciences

Healthcare systems integrators, genomics platforms, and pharmaceutical R&D organisations represent a high-value, still underpenetrated segment for in-memory computing vendors. The increasing adoption of interoperable electronic health records under the 21st Century Cures Act and HL7 FHIR standards is generating continuous, structured clinical data streams. These workloads, ranging from population health analytics to clinical decision support and genomic analysis, require low-latency processing that often exceeds the limits of traditional disk-based databases. Vendors such as Oracle Health offer advanced healthcare analytics capabilities within broader cloud and data platform ecosystems, reflecting the shift toward real-time healthcare intelligence.

Edge Computing Convergence with In-Memory Fabric for Industrial IoT Applications

Industrial manufacturers, smart grid operators, and autonomous systems generate high-frequency sensor data that requires deterministic, low-latency processing at the edge. This creates strong demand for in-memory computing architectures deployed closer to data sources, reducing dependence on centralized cloud processing. Edge computing frameworks in Industry 4.0 environments increasingly emphasize real-time analytics, event processing, and local decision-making. In-memory data grids and distributed memory fabrics are commonly used to support sub-second anomaly detection and operational control use cases. Solutions deployed across industrial IoT platforms, including those from Siemens and in-memory technology providers such as GridGain Systems, illustrate this convergence in practice. The opportunity is further strengthened by advancements in edge hardware and emerging memory-centric interconnect technologies, enabling scalable real-time processing.

Category-wise Analysis

Component Insights

Solution segment accounts for over 74.0% of the global in-memory computing market in 2026, reaching US$ 17.98 billion, due to the need for integrated platforms that eliminate fragmented data architectures. Enterprises increasingly require bundled capabilities such as in-memory data grids, caching layers, and real-time analytics engines to reduce system complexity. It helps with ultra-low latency processing for mission-critical workloads like trading systems and real-time inventory management. Standardized solutions also reduce integration overhead and improve scalability across distributed environments.

The services segment is the fast-growing, due to the need for specialized expertise in deploying and managing complex in-memory environments. Enterprises lack internal capabilities for architecture design, performance optimization, and hybrid/multi-cloud integration. As systems become more distributed, the need for managed services and SLA-backed operations increases significantly. Organizations also require continuous tuning to maintain sub-millisecond performance at scale.

Deployment Insights

Cloud-based deployment segment accounts for more than 47% share in 2026, exceeding the value of US$ 11.42 billion, driven by the need for elastic scalability and rapid provisioning. Enterprises prefer cloud models to handle unpredictable workloads without investing in physical infrastructure. The key requirement is on-demand memory scaling for high-throughput, latency-sensitive applications such as recommendation engines and real-time analytics. Cloud deployment also supports global accessibility and faster innovation cycles. It reduces infrastructure management burden while enabling seamless integration with modern digital platforms.

Hybrid deployment is the fastest-growing model due to the need to balance regulatory compliance with performance scalability. Organizations must retain sensitive data on premises while still leveraging cloud elasticity for computed heavy workloads. This architecture supports data sovereignty requirements in regulated industries such as finance and government. Enterprises also need flexible workload mobility between environments to manage peak demand efficiently. Hybrid models are becoming essential for large-scale, regulated digital ecosystems.

Application Insights

Real-time data processing & analytics account for over 31% of the global in-memory computing market share in 2026, surpassing a value of US$ 7.53 Billion, due to the need for instant decision-making from live data streams. Businesses require sub-millisecond processing to support high-frequency transactions, fraud detection, and real-time bidding systems. It helps in eliminating storage latency to ensure continuous operational intelligence. This enables organizations to respond immediately to rapidly changing data conditions. Industries such as financial services depend on continuous risk calculation and transaction monitoring.

Predictive analysis is the fast-growing application segment due to the need for real-time machine learning inference. Enterprises are shifting from historical batch processing to continuous feature computation from live data streams. The key requirement is ultra-fast model scoring to support dynamic decision-making in areas like credit risk and customer engagement. Organizations need infrastructure capable of continuously updating predictions with minimal delay. This enables operational AI systems that function in real time rather than periodic cycles.

Vertical Insights

IT & Telecom vertical accounts for over 22% share in 2026, reaching US$ 5.35 billion, driven by the requirement to process massive volumes of network and customer data in real time. Telecom operators require ultra-low latency systems to manage billing, network orchestration, and service delivery at scale. The core necessity is high-throughput event processing to support millions of concurrent operations. In-memory computing ensures deterministic performance for critical network functions. It also enables real-time anomaly detection and rapid traffic optimization across distributed networks. This vertical depends heavily on continuous, high-speed data processing infrastructure.

Manufacturing is the fast-growing vertical due to the requirement for real-time operational intelligence in connected production environments. Smart factories generate continuous IoT data streams that require instant analysis for quality control and predictive maintenance. The objective is to reduce downtime by identifying defects and equipment failures in real time. Manufacturers also require immediate feedback loops for production optimization and process efficiency. This growth is driven by the shift toward fully digitized, automated industrial ecosystems.

Regional Insights

North America In-memory Computing Market Trends and Insights

North America accounts for over 37% of the global in-memory computing market in 2026, reaching US$ 8.99 billion, due to the highest concentration of hyperscaler cloud workloads, algorithmic trading systems, and AI-native software platforms. The region’s leadership is structurally reinforced by large-scale enterprise migration toward memory-optimized cloud instances to support real-time analytics and sub-millisecond processing demands. As Fortune 500 enterprises continue accelerating AI workload deployment, North America’s dominance is expected to remain intact through the forecast period.

The United States in-memory computing market is expected to reach US$ 7.55 billion in 2026, driven by Wall Street’s real-time risk analytics infrastructure and Silicon Valley’s AI platform ecosystems. Regulatory momentum, including the FFIEC’s 2023 updated technology risk guidance, explicitly reinforces the need for real-time data processing capabilities among systemically important financial institutions. U.S. Department of Defense modernization initiatives under the Joint Warfighting Cloud Capability (JWCC) programme are expanding adoption of in-memory architectures into defense-grade and classified workloads.

Europe In-memory Computing Market Trends and Insights

Europe in-memory computing market holds over 24.0% of the global share in 2026, surpassing US$ 5.83 billion, shaped by a dual force of regulatory compliance and real-time data infrastructure modernization. The European Data Act is accelerating demand for interoperable, cross-sector data processing systems, particularly in industrial and public digital ecosystems. Enterprises are increasingly prioritizing in-memory platforms with embedded governance, data lineage, and access-control capabilities to meet sovereignty and compliance obligations. This regulatory backdrop is reinforcing the adoption of scalable, low-latency architectures across banking, manufacturing, and telecom workloads.

Germany's in-memory computing market holds over 24.0% of the regional share in 2026, reaching US$ 1.40 billion, driven by automotive and industrial manufacturing digitization. The UK holds over 21% share due to the financial services modernization and regulatory resilience requirements from the FCA. France is expected cross the value of US$ 820 million, supported by sovereign AI initiatives and public-sector digital infrastructure investments. The demand is concentrated in real-time fraud detection, industrial process intelligence, and AI-enabled analytics platforms.

Spain market growth is led by banking-led digital transformation and fraud analytics use cases. The country’s National Recovery and Resilience Plan, receiving €163 Billion in EU Next Generation EU funds, is significantly accelerating digital transformation across financial services and public sector infrastructure. This funding enables the large-scale deployment of cloud-based and real-time in-memory analytics systems to modernize legacy IT environments. Expanding hyperscaler data centre capacity in Madrid is further reducing latency constraints and strengthening real-time workload feasibility.

Asia Pacific In-memory Computing Market Trends and Insights

Asia Pacific holds over 27.0% share of the global in-memory computing market in 2026, reaching US$ 6.56 Billion, and is expected to grow at highest rate with a CAGR of 22.9%, due to large-scale digital payments expansion, 5G network densification, and government-led smart city programmes enabling real-time urban analytics. The region is increasingly shifting enterprise architectures toward low-latency, memory-resident data processing to support AI, fraud detection, and high-frequency transactional systems.

China in-memory computing market is expected to reach a value over US$ 2.49 billion by 2026, supported by its Digital China strategy under the 14th Five-Year Plan and strong hyperscaler ecosystems. Domestic platforms such as Alibaba Cloud’s Tair in-memory database demonstrate large-scale deployment across high-volume e-commerce and real-time personalization workloads. Regulatory frameworks under the Cyberspace Administration of China are reinforcing adoption of domestic in-memory systems for security compliance, limiting foreign penetration. Japan growth is driven by precision manufacturing and financial services where deterministic low-latency processing is critical, supported by initiatives such as Society 5.0 and platforms like Fujitsu’s PRIMEFLEX systems.

India in-memory computing market is expected to exceed the value of US$ 1.12 Billion in 2026, due to the rapid scaling of UPI-based digital payments, real-time governance platforms, and enterprise-grade API ecosystems requiring sub-second response times. Strong expansion of global capability centres is further accelerating the adoption of in-memory architectures across IT services and telecom sectors. South Korea's growth is supported by semiconductor leadership, advanced DRAM availability, and national digital transformation programmes.

Competitive Landscape

The global in-memory computing market operates as a concentrated oligopoly at the enterprise platform layer, where a small group of large vendors collectively holds nearly half of total revenue through tightly integrated databases and cloud ecosystems. Companies are focusing on ultra-low latency performance, depth of hyperscaler and cloud ecosystem integration, and the breadth of industry-specific compliance certifications. A dominant strategic shift is underway toward combining in-memory compute architectures with vector database capabilities to support real-time AI inferencing workloads. Mid-tier disruptors are focusing on extending these capabilities across developer ecosystems and converting open-source adoption into enterprise-grade monetization pathways.

Key Developments:

- In May 2026, IBM and AMD announced a deeper collaboration to accelerate hybrid, sovereign, and enterprise AI workloads using AMD CPUs and GPUs on IBM Cloud. The partnership aims to enhance performance for AI training and inference by combining IBM’s software stack with AMD’s high-performance compute architecture. This collaboration is expected to strengthen real-time AI processing capabilities across hybrid cloud environments.

- In March 2026, MariaDB completed the acquisition of GridGain. The deal aims to strengthen MariaDB’s capabilities in powering low-latency, AI-driven and agentic AI workloads through in-memory data architectures. This move reflects growing industry demand for high-speed data processing to support real-time analytics and AI applications.

Global In-memory Computing Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 10.7 Billion |

|

Current Market Value (2026) |

US$ 24.3 Billion |

|

Projected Market Value (2033) |

US$ 78.8 Billion |

|

CAGR (2026–2033) |

18.3% |

|

Leading Region |

North America, 37.0% Share |

|

Dominant Application |

Real-time Data Processing & Analytics, 31.0% Share |

|

Top-ranking Vertical |

IT & Telecom, 22.0% Share |

|

Incremental Opportunity (2026–2033) |

US$ 54.5 Billion |

Companies Covered in In-memory Computing Market

- SAP

- Oracle Corporation

- Microsoft

- IBM

- Redis

- Hazelcast

- GridGain Systems

- GigaSpaces Technologies

- Software AG

- TIBCO Software

- SAS Institute

- Altibase

- Intel

- Fujitsu

- Qlik

- Others

Frequently Asked Questions

The global in-memory computing market is valued at US$ 24.30 Billion in 2026 and is projected to reach US$ 78.80 Billion by 2033, advancing at a CAGR of 18.3%, due to the need for real-time AI inferencing and ultra-low latency data processing at scale.

The growth is driven by regulatory and operational needs for real-time decision-making systems. Compliance requirements for AI transparency and financial system resilience are pushing enterprises toward in-memory architecture.

Solution segment dominates with over 74.0% share in 2026 due to enterprise demand for integrated platforms. Organizations prefer unified systems to reduce complexity and meet the need for faster deployment and lower integration risk.

North America leads with holding a share of more than 37.0% in 2026, driven by strong demand for high-speed financial and cloud workloads. The region’s need for ultra-low latency computing in trading and hyperscale cloud infrastructure reinforces its dominance.

Healthcare and life sciences present major opportunities due to rising demand for real-time clinical analytics. The need for fast, compliant, and interoperable patient data processing is driving adoption of in-memory computing platforms.

The leading companies include SAP, Oracle Corporation, Microsoft, IBM, Redis, Hazelcast, GridGain Systems, GigaSpaces Technologies, TIBCO Software, SAS Institute and among others.