- Technology

- Data Monetization Solutions for Lifescience Companies Market

Data Monetization Solutions for Lifescience Companies Market Size, Share, and Growth Forecast 2026 - 2033

Data Monetization Solutions for Lifescience Companies Market by Component (Software, Services), by Deployment (Cloud-based, On-premise), Application (Commercial Analytics, Patient Data Monetization, Clinical Trial Analytics, Real-world Evidence Analytics,

Data Monetization Solutions for Lifescience Companies Market Analysis

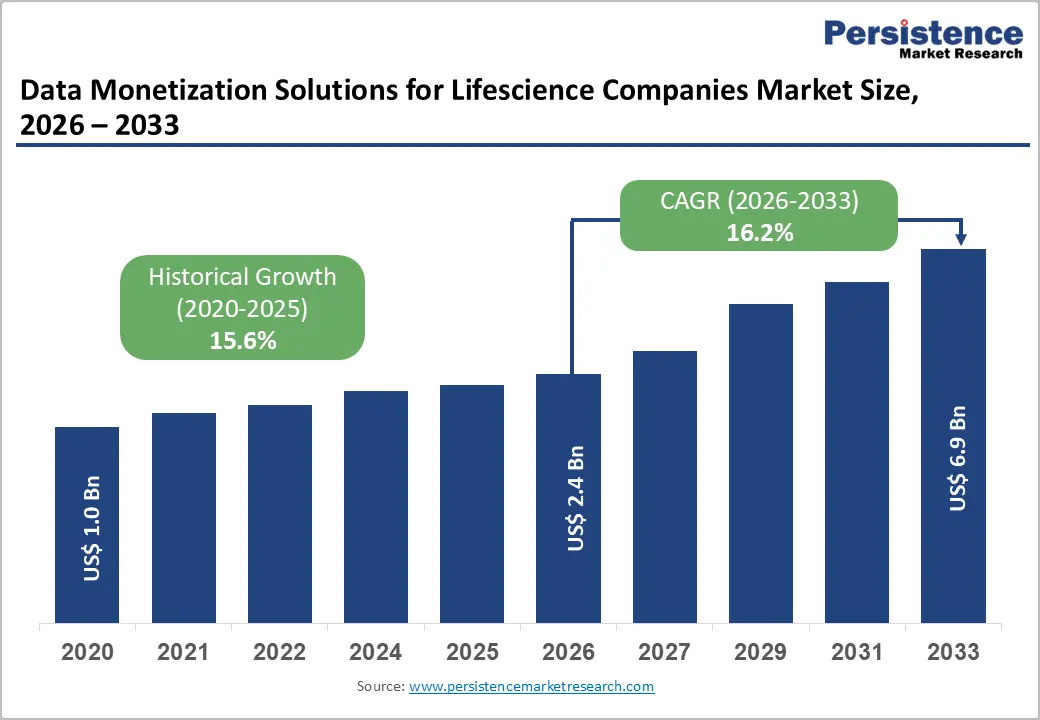

The global data monetization solutions for lifescience companies market size is expected to be valued at US$ 2.4 billion in 2026 and projected to reach US$ 6.9 billion by 2033, growing at a CAGR of 16.2% between 2026 and 2033. The market is gaining momentum as life science enterprises increasingly convert proprietary R&D, clinical, and real-world datasets into recurring revenue streams. Accelerating cloud adoption, expanding FDA-recognized real-world evidence frameworks, and rising cross-industry data partnerships are reshaping value chains. Regulatory mandates under HIPAA and GDPR, alongside the surge in AI-driven analytics, are further fueling enterprise-wide monetization initiatives globally.

Key Industry Highlights:

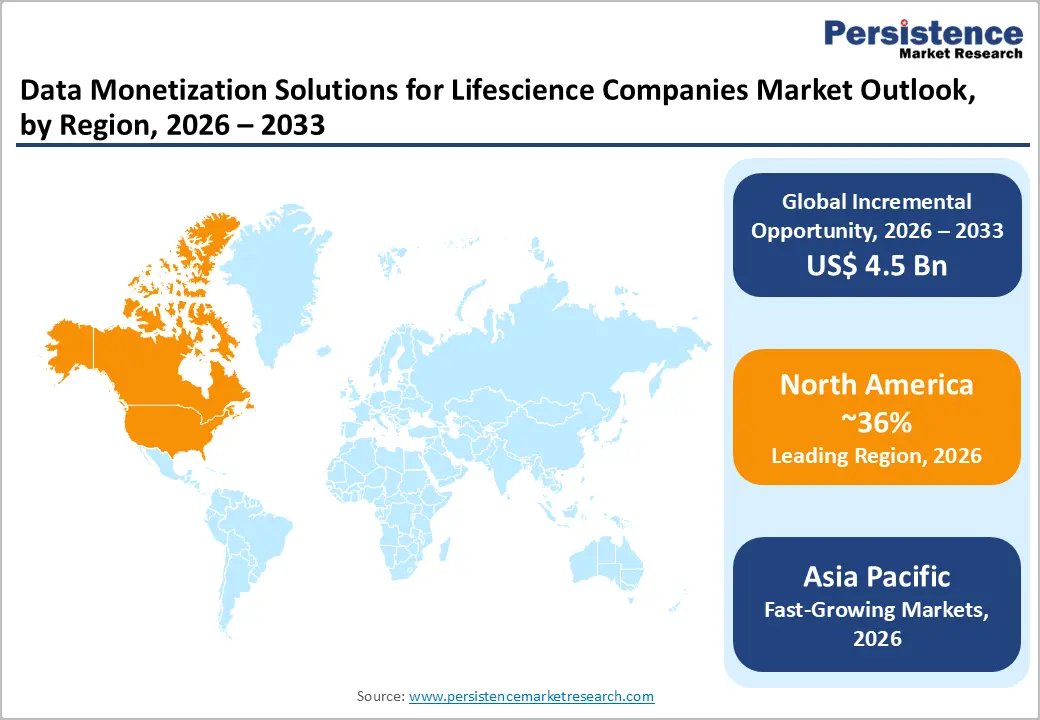

- Leading Region: North America dominates with a 36% share in 2026, driven by mature pharma-tech ecosystems and progressive FDA frameworks.

- Fastest Growing Region: Asia Pacific leads growth between 2026 and 2033, fueled by government-led digital health programs and rising R&D investments.

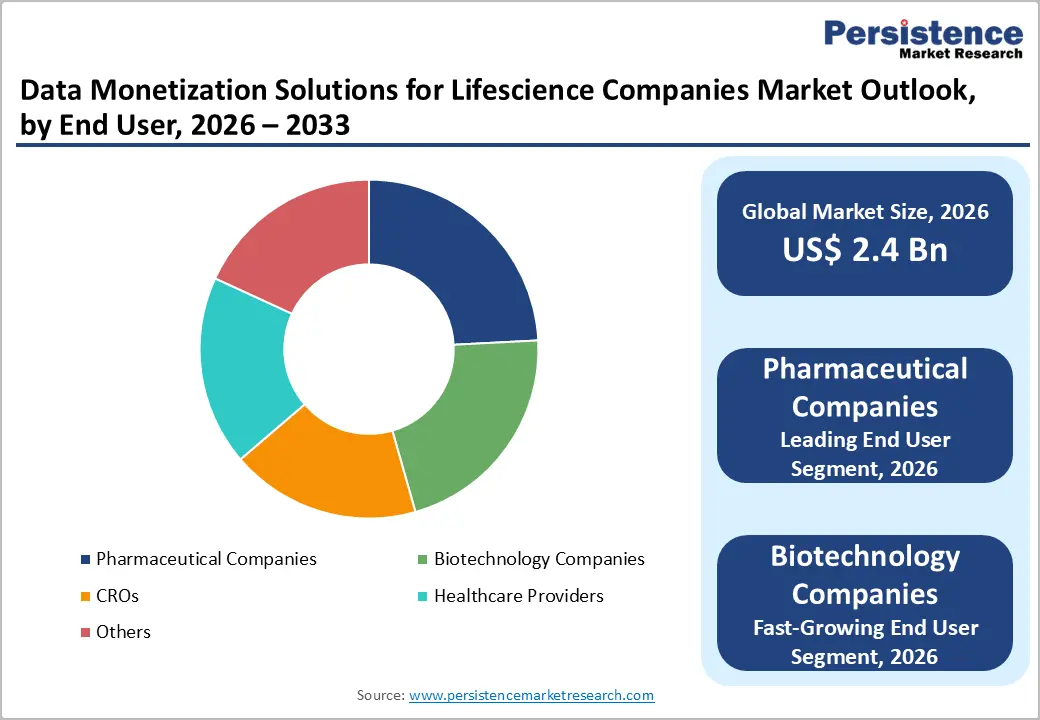

- Dominant Segment: Pharmaceutical companies are likely to register a 46% share in 2026, supported by extensive R&D pipelines and large proprietary datasets.

- Fast-Growing Segment: Biotechnology companies record fast-growth, powered by precision medicine and AI-enabled discovery platforms.

- Key Opportunity: Cloud-based deployment in Asia Pacific unlocks major potential, backed by national digital health missions in India and China.

Market Dynamics

Drivers - Surge in Real-World Evidence Adoption Driving Drug Development Decisions

The growing dependence on real-world evidence (RWE) is a dominant force driving the data monetization landscape for life science companies. The U.S. Food and Drug Administration (FDA) has approved over 90 RWE-supported regulatory submissions between 2019 and 2024, signaling broader acceptance of patient-derived datasets in approvals and label expansions across oncology, rare disease, and cardiometabolic therapy pipelines worldwide.

Pharmaceutical firms are increasingly licensing de-identified longitudinal records from health systems to accelerate therapeutic development and post-market surveillance activities. According to the National Institutes of Health (NIH), more than 60% of new clinical programs initiated in 2024 incorporated RWE components, directly boosting investment in commercial analytics and real-world evidence analytics platforms across pharmaceutical and biotechnology sectors globally.

Rapid Digital Transformation and AI Integration Across Lifescience Operations

Accelerated digital transformation across global life science enterprises is reshaping how clinical, genomic, and commercial data assets are valued and monetized. The European Medicines Agency (EMA) and FDA jointly emphasized in their 2024 AI/ML guidance the importance of structured data ecosystems to power machine-learning pipelines, regulatory submissions, and adaptive trial workflows across modern drug discovery and development environments.

Multi-billion-dollar AI partnerships between pharmaceutical innovators and cloud analytics providers underscore the rising demand for monetizable datasets across the value chain. The Organisation for Economic Co-operation and Development (OECD) reports that healthcare data volumes are expanding at over 36% annually, creating fertile ground for software, services, and cloud-based monetization platforms enabling interoperability, secure exchange, and analytical insights at scale.

Restraints - Stringent Data Privacy and Cross-Border Compliance Burdens Restraining Growth

Tightening data protection mandates pose a significant restraint to monetization efforts across global life science enterprises. The European Union GDPR framework imposes fines of up to 4% of annual global turnover for breaches. At the same time, the U.S. HIPAA regime and emerging laws in China (PIPL) and India (DPDP Act, 2023) restrict cross-border patient data flows, complicating commercial licensing arrangements between sponsors and providers.

The European Data Protection Board (EDPB) recorded over €2.1 billion in cumulative penalties through 2024, signaling rigorous enforcement across member states. These regulatory complexities raise compliance costs, slow the execution of multi-party contracts, and discourage smaller biotechnology firms and emerging digital health ventures from actively participating in cross-border commercial data exchanges and global monetization ecosystems.

Fragmented Data Standards and Persistent Interoperability Gaps Limiting Adoption

Limited interoperability across electronic health records, laboratory information systems, and clinical trial platforms remains a critical barrier to scaling data monetization. The Office of the National Coordinator for Health IT (ONC) reported that nearly 30% of U.S. hospitals still face challenges in routinely exchanging structured patient data, despite progress enabled by the 21st Century Cures Act and federal information-blocking rules.

This fragmentation reduces dataset quality, complicates licensing valuation, and delays insight generation for pharmaceutical and biotechnology clients seeking integrated analytics. Until HL7 FHIR and OMOP common data models achieve broader universal adoption across providers and life science stakeholders, the monetization potential of clinical, claims, and patient-level data will remain partially constrained globally.

Opportunities - Expansion of Patient Data Monetization Through Decentralized Clinical Trials

Decentralized clinical trial (DCT) models present a transformative opportunity for patient data monetization across the life sciences value chain. The Clinical Trials Transformation Initiative (CTTI) notes that more than 75% of trials launched in 2024 incorporated at least one decentralized element, generating continuous streams of consented wearable, genomic, and behavioral data suitable for monetizable analytics and downstream research applications.

The FDA's December 2023 final guidance on DCTs formally recognized digital health technologies as primary data sources for regulatory submissions. Biotechnology firms are leveraging such datasets to power adaptive trial designs and post-market surveillance studies. This trend aligns strongly with growth in healthcare analytics and digital health platforms, opening lucrative licensing channels for technology vendors, CROs, and patient-data exchange operators.

Rising Cloud-Based Analytics Adoption Across Emerging Asia Pacific Economies

Cloud-based deployment models are unlocking new revenue pockets, especially across the rapidly digitizing Asia Pacific region. The World Health Organization (WHO) Digital Health Strategy 2020-2025 and India's Ayushman Bharat Digital Mission are accelerating creation of nationwide health data registries. The National Health Authority of India reported more than 670 million Ayushman Bharat Health Account IDs created by mid-2024, generating vast monetizable population-level datasets.

Similarly, China's Healthy China 2030 initiative emphasizes secure data exchange platforms supporting interoperable research ecosystems and pharmaceutical innovation pipelines. Cloud-native solutions from major hyperscale providers are gaining traction among pharmaceutical and CRO clients, positioning the cloud-based segment as the fastest-growing deployment channel within global life science data monetization ecosystems through 2033.

Category-wise Analysis

Component Insights

The software segment leads the component category, accounting for nearly 62% of the global market share in 2025. Enterprise demand for AI-powered analytics suites, data lake platforms, and consent management systems has surged in tandem with broader digital transformation in pharmaceutical R&D. The U.S. Department of Health and Human Services has highlighted federated data architectures as critical infrastructure for next-generation drug development workflows.

The services segment is projected to be the fast-growing component category as life science enterprises increasingly seek consulting, integration, and managed analytics expertise. The rising complexity of data governance frameworks under HIPAA and GDPR, coupled with demand for customized monetization strategies, is fueling services adoption. Pharmaceutical and biotechnology clients are outsourcing data engineering, AI model deployment, and compliance auditing to specialized vendors with deep domain expertise.

Deployment Insights

The cloud-based deployment segment commands a leading 68% share of the global market in 2026, anchored by scalability, real-time analytics, and global accessibility advantages. The U.S. National Institute of Standards and Technology (NIST) and the European Cloud User Coalition have issued frameworks supporting compliant cloud usage across regulated industries. Cloud platforms enable secure monetization of clinical, commercial, and real-world datasets at enterprise scale across geographies.

The cloud-based segment is also positioned as the fastest-growing deployment channel through 2032, propelled by hyperscaler partnerships and AI-ready infrastructure rollouts. Major life science enterprises are migrating legacy on-premise systems to multi-cloud environments to support generative AI workloads and federated learning initiatives. Hybrid architectures combining sovereign cloud zones with global analytics layers are emerging rapidly, reinforcing the cloud's strategic role in life science data monetization.

Application Insights

Within applications, commercial analytics are likely to register a dominant share in 2026. Pharmaceutical firms rely on commercial analytics to optimize sales force deployment, brand positioning, payer engagement, and physician targeting. The American Medical Association estimates that prescription data underpins more than 80% of pharma commercial decisions in mature markets, sustaining heavy investment across prescribers, claims, and EHR-derived insights.

Real-world evidence analytics is the fast-growing application category as global regulators expand acceptance of post-market and outcomes data in label expansions, indication broadening, and reimbursement decisions. The FDA's formal RWE framework and the European Medicines Agency's DARWIN EU initiative are accelerating uptake. Pharmaceutical and biotechnology firms increasingly leverage RWE platforms to support adaptive trials, health economics studies, and value-based contracting with payers worldwide.

End-user Insights

The pharmaceutical companies segment dominates the end-user category with a 46% share of the global market in 2025, supported by sustained R&D investment and broad commercial portfolios. According to EFPIA, European pharmaceutical R&D investment exceeded €48 billion in 2024, while PhRMA reports U.S. members invested more than US$ 100 billion the same year, fueling demand for monetizable data assets.

Biotechnology companies represent the fastest-growing end-user segment by 2033, propelled by precision-medicine pipelines and expanding adoption of AI-enabled drug discovery platforms. Rising venture funding for cell, gene, and RNA-based therapies is generating vast proprietary genomic and clinical datasets. Emerging biotechs increasingly monetize these data assets through licensing deals, strategic partnerships, and co-development arrangements with larger pharmaceutical innovators and specialized analytics technology vendors.

Regional Insights

North America Data Monetization Solutions for Lifescience Companies Market Trends and Insights

North America leads the global market with a 36% share in 2025, anchored by strong pharma-tech partnerships, robust EHR penetration, and progressive regulatory acceptance of RWE. The presence of FDA-led initiatives like Sentinel and rapidly expanding cloud-based health data exchanges position the region as the center of innovation for monetizable life science data assets across clinical and commercial workflows.

U.S. Data Monetization Solutions for Lifescience Companies Market Size

The United States accounts for roughly 85% of the North American market in 2026, sustaining its position as the global innovation hub. Strong investment by Big Pharma, the 21st Century Cures Act, and high adoption of interoperable EHRs under ONC certification standards continue to drive monetization opportunities across clinical, commercial, and real-world data streams in the country.

Europe Data Monetization Solutions for Lifescience Companies Market Trends and Insights

Europe represents the second-largest market, supported by the European Health Data Space (EHDS) regulation finalized in 2024, which enables secondary use of health data for research and innovation. Strong public-private collaboration through the Innovative Medicines Initiative (IMI) and Innovative Health Initiative (IHI) programs is fueling the adoption of monetization platforms across pharmaceutical R&D hubs in Germany, the U.K., and France.

Germany Data Monetization Solutions for Lifescience Companies Market Size

Germany is Europe's largest market, contributing nearly 28% of regional revenue in 2026. The Federal Ministry of Health's Digital Healthcare Act (DVG) and the launch of the Electronic Patient Record (ePA) ecosystem strongly support monetizable clinical datasets used by leading pharma firms. Rising AI-driven discovery investments and biotech cluster expansion in Berlin and Munich further reinforce monetization momentum.

U.K. Data Monetization Solutions for Lifescience Companies Market Size

The United Kingdom accounts for roughly 22% of European revenue in 2026, reinforced by progressive digital health policies and pharma R&D investment. The NHS Federated Data Platform and active partnerships through Genomics England provide unique large-scale datasets, attracting global pharmaceutical investment into real-world evidence and patient-data analytics solutions, while the MHRA continues advancing supportive regulatory pathways for data-driven innovation.

France Data Monetization Solutions for Lifescience Companies Market Size

France contributes around 15% of European revenue in 2026, supported by a strong national digital health infrastructure and pharma R&D ecosystems. The Health Data Hub (HDH) initiative under the French Ministry of Health enables structured access to one of the world's largest national health data systems, supporting monetization opportunities for analytics vendors, biotech innovators, and contract research organizations operating across the country.

Asia Pacific Data Monetization Solutions for Lifescience Companies Market Trends and Insights

Asia Pacific is the fastest-growing region, propelled by digital health investments, government-led data infrastructures, and a thriving CRO ecosystem. China's Healthy China 2030 agenda and India's digital health mission catalyze regional growth, while Japan and South Korea drive uptake of AI-based precision medicine platforms that depend heavily on structured monetizable life science datasets across pharmaceutical, biotechnology, and academic research stakeholders.

India Data Monetization Solutions for Lifescience Companies Market Size

India represents approximately 18% of the Asia Pacific market in 2026, supported by rapidly expanding digital health adoption. The Ayushman Bharat Digital Mission and rapid expansion of clinical research outsourcing under CDSCO oversight drive demand for cloud-based monetization platforms across pharmaceutical and biotechnology firms. Rising venture capital flows into digital health startups further accelerate dataset commercialization across diagnostics and therapeutics segments.

Japan Data Monetization Solutions for Lifescience Companies Market Size

Japan holds about 21% of the regional market in 2026, anchored by strong domestic pharma R&D and mature digital health infrastructure. The Ministry of Health, Labour and Welfare's Next-Generation Medical Infrastructure Act enables anonymized health data use, while sustained R&D investments by major pharmaceutical players support the adoption of advanced analytics platforms across oncology, neurology, and rare disease pipelines nationwide.

Southeast Asia Data Monetization Solutions for Lifescience Companies Market Size

Southeast Asia contributes nearly 12% of the regional market in 2026, with rising digital health adoption across emerging economies. Singapore's HealthHub and Malaysia's MySejahtera platforms underpin growing demand for monetizable datasets. Expanding clinical trial activity and pharma investment in Indonesia, Thailand, and Vietnam make the sub-region a strategic hub for emerging monetization initiatives across pharmaceutical and biotechnology stakeholders.

Competitive Landscape

The global data monetization solutions for lifescience companies market is moderately fragmented, with leading vendors competing on data depth, regulatory compliance, AI capability, and integration breadth. Strategic alliances with cloud hyperscalers, acquisitions of niche analytics firms, and partnerships with academic medical centers remain the most active expansion levers. Vendors are aggressively scaling proprietary global patient panels and regulatory-grade datasets.

Emerging business models center on subscription-based data-as-a-service platforms, federated analytics ecosystems, and consent-based patient-data marketplaces. Key differentiators include AI-ready data lakes, interoperable architectures aligned with HL7 FHIR standards, and domain-specific machine-learning models that accelerate insight generation for pharmaceutical, biotechnology, and CRO clients worldwide.

Key Developments:

- In March 2025, IQVIA expanded its strategic partnership with NVIDIA to accelerate AI-powered drug discovery and clinical analytics, integrating advanced generative models into its global healthcare data assets.

- In November 2024, Veeva Systems launched its Vault Direct Data API, enabling pharmaceutical clients to securely monetize structured clinical and commercial datasets across enterprise applications.

- In June 2024, Oracle Health announced integration of its EHR data platform with multi-cloud analytics to enable life science firms to license de-identified patient datasets for real-world evidence generation.

Global Data Monetization Solutions for Lifescience Companies Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 1.0 billion |

|

Current Market Value (2026) |

US$ 2.4 billion |

|

Projected Market Value (2033) |

US$ 6.9 billion |

|

CAGR (2026-2033) |

16.2% |

|

Leading Region |

North America, 36% |

|

Dominant Category-1 (Component) |

Software, US$ 1.49 billion |

|

Top-ranking Category-2 (Deployment) |

Cloud-based, US$ 1.63 billion |

|

Incremental Opportunity |

US$ 4.5 billion |

Companies Covered in Data Monetization Solutions for Lifescience Companies Market

- IQVIA

- Oracle Health

- Veeva Systems

- SAS Institute

- Accenture

- Cognizant

- IBM

- Salesforce

- SAP

- Snowflake

- Microsoft

- Optum

- Clarivate

- Komodo Health

- Palantir Technologies

Frequently Asked Questions

The market is valued at US$ 2.4 billion in 2026 and projected to reach US$ 6.9 billion by 2033, growing at a CAGR of 16.2%.

Rising RWE adoption, AI integration backed by FDA and EMA guidance, and accelerated cloud-based analytics demand are the key drivers.

North America leads with a 36% share in 2025, supported by mature pharma ecosystems and progressive FDA RWE frameworks.

Patient data monetization via decentralized clinical trials and cloud-based analytics adoption across Asia Pacific markets present significant opportunities.

Leading players include IQVIA Holdings Inc., Veeva Systems Inc., Oracle Health, IBM Corporation, SAS Institute Inc., Clarivate Plc, Accenture plc, and Komodo Health, Inc..