- Medical Devices

- Vagus Nerve Stimulation (VNS) Market

Vagus Nerve Stimulation (VNS) Market Size, Share and Growth Forecast, 2026-2033

Vagus Nerve Stimulation (VNS) Market by Product (Implantable VNS Device, External Non-invasive VNS Device), Application (Epilepsy, Depression, Migraine, Others), and Regional Analysis for 2026 - 2033

Vagus Nerve Stimulation (VNS) Market Share and Trends Analysis

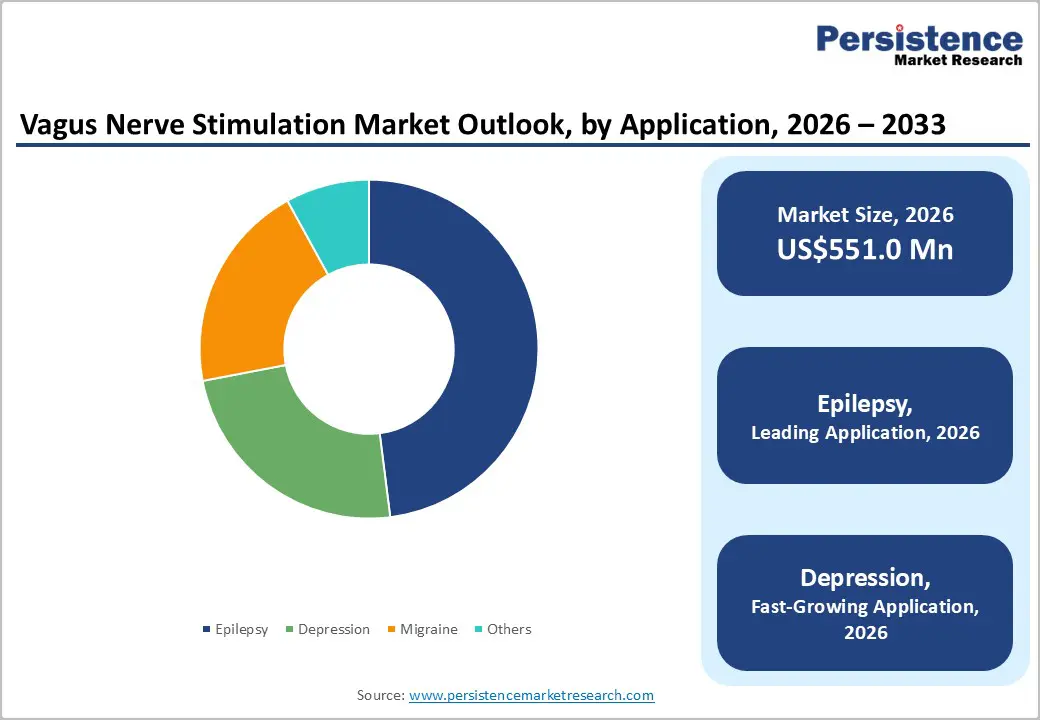

The global vagus nerve stimulation market size is likely to be valued at US$551.0 million in 2026 and is projected to reach US$1,026.8 million by 2033, growing at a CAGR of 9.3% during the forecast period from 2026 to 2033, driven by rising prevalence of neurological disorders such as epilepsy, depression, and migraine, along with growing adoption of neuromodulation therapies as adjunct or alternative treatments.

According to the U.S. Food and Drug Administration (FDA) and the National Institute for Health and Care Excellence (NICE), VNS therapy is clinically validated for treatment-resistant conditions. Advancements in implantable and non-invasive devices are improving patient compliance, while increasing healthcare spending and awareness of neuromodulation therapies continue to support market growth across developed and emerging economies.

Key Industry Highlights:

- Disease Burden Dynamics: Epilepsy and depression continue to dominate demand drivers in the vagus nerve stimulation market, supported by rising global neurological disorder prevalence and increasing reliance on neuromodulation therapy devices for treatment-resistant cases.

- Product Leadership: Implantable VNS devices are estimated to account for around 72% revenue share in 2026, while external non-invasive VNS devices are projected to grow at the fastest pace through 2033 due to improved patient compliance, lower procedural risk, and expanding outpatient adoption.

- Application Trends: Epilepsy is estimated to hold approximately 48% revenue share in 2026, while depression and migraine applications are expected to register the fastest growth through 2033, driven by expanding clinical validation and broader psychiatric adoption of neuromodulation therapies.

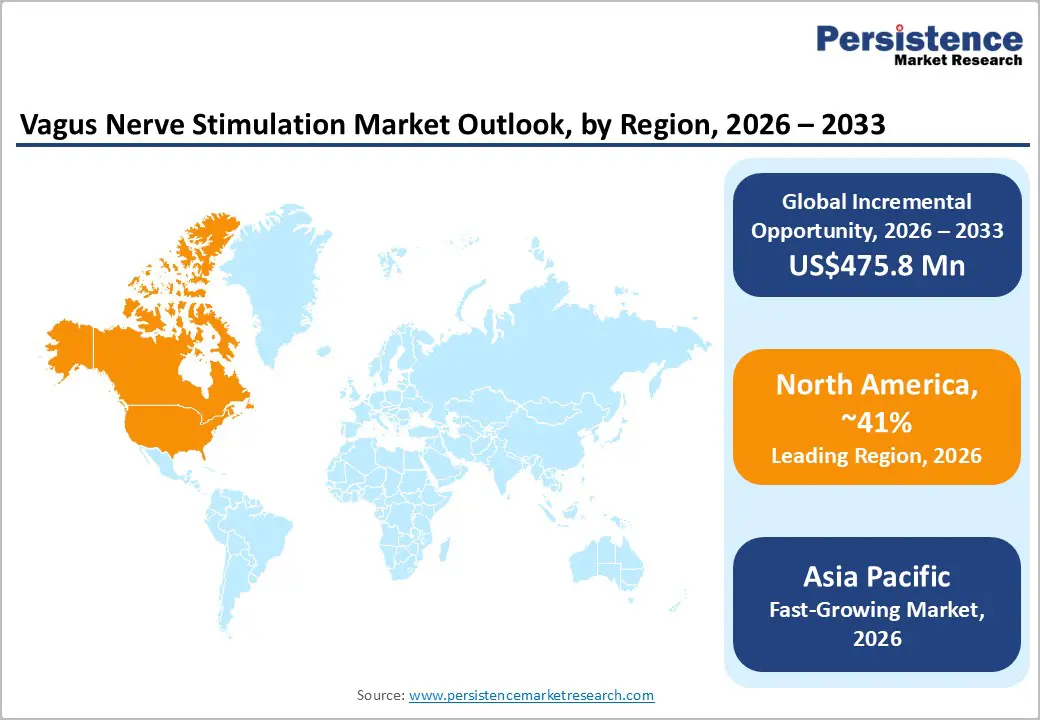

- Regional Leadership: North America is estimated to account for around 41% revenue share in 2026, while Asia Pacific is projected to be the fastest-growing region through 2033, supported by rising neurological disease burden, healthcare infrastructure expansion, and increasing access to advanced neuromodulation technologies.

- Technology Shift: Market evolution is increasingly centered on wearable neuromodulation devices, AI-enabled therapy optimization, and digitally connected VNS systems, improving real-time monitoring, treatment personalization, and patient adherence.

DRO Analysis

Driver - Rising Burden of Treatment-Resistant Neurological Disorders and Psychiatric Conditions

The global rise in epilepsy, depression, and migraine cases is a key driver of the vagus nerve stimulation market. According to the World Health Organization (WHO), approximately 50 million people suffer from epilepsy worldwide, while depression affects more than 280 million individuals globally. A significant portion of these patients remains resistant to pharmacological therapies, creating strong demand for neuromodulation devices such as VNS systems.

Clinical guidelines from the American Academy of Neurology (AAN) support VNS as an adjunct therapy for refractory epilepsy. The increasing incidence of comorbid neurological and psychiatric disorders is expanding the addressable patient pool, thereby strengthening long-term demand for both implantable and non-invasive VNS devices across hospital and outpatient settings.

Restraint - High Device Cost and Surgical Complexity Limiting Adoption

Despite strong clinical efficacy, the vagus nerve stimulation market faces structural constraints due to high implantation costs and surgical requirements. Implantable VNS systems can cost between US$20,000–40,000 per procedure, including device and surgical expenses, making affordability a major barrier in low- and middle-income countries.

Additionally, reimbursement coverage remains inconsistent across healthcare systems, particularly in Asia and parts of Latin America. The need for specialized neurosurgical expertise further limits adoption in secondary care facilities. Post-surgical complications such as hoarseness, cough, and device adjustment requirements also contribute to patient hesitation. These factors collectively restrict market penetration despite rising clinical demand, slowing adoption rates in cost-sensitive regions.

Opportunity - Expansion of Non-Invasive Vagus Nerve Stimulation Technologies

A major opportunity in the vagus nerve stimulation market lies in the rapid development of external non-invasive VNS devices. These devices eliminate surgical risks and significantly reduce treatment costs, improving accessibility across outpatient and homecare settings. Emerging applications in migraine and anxiety management are expanding clinical acceptance.

According to clinical research supported by the U.S. National Institutes of Health (NIH), transcutaneous VNS systems are demonstrating promising efficacy in reducing seizure frequency and depressive episodes. The non-invasive segment is expected to capture increasing demand from emerging economies, where healthcare infrastructure limitations restrict surgical procedures. This segment could represent a multi-hundred-million-dollar incremental opportunity by 2033, particularly in Asia Pacific and Latin America.

Category-wise Analysis

Product Insights

The implantable VNS device segment is estimated to account for around 72% revenue share in 2026, driven by established clinical adoption in drug-resistant epilepsy and treatment-resistant depression. These FDA-approved implantable systems deliver continuous vagus nerve stimulation and are widely embedded in tertiary hospital neurology workflows across North America and Europe. Their dominance is supported by strong long-term clinical outcomes and guideline-based usage in epilepsy care. Relatively high procedural costs and surgical requirements are expected to limit broader penetration in emerging healthcare systems despite steady global demand.

The external non-invasive VNS device segment is projected to expand at approximately 10.1% CAGR through 2033, supported by increasing preference for non-surgical, wearable neuromodulation therapies. These devices are gaining traction in migraine and mental health applications due to ease of use, improved patient compliance, and suitability for home-based care. Regulatory clearances for non-invasive VNS in headache-related indications and expanding tele-neurology adoption are expected to accelerate uptake. Growth momentum is further supported by rising deployment across outpatient care settings in the U.S., Europe, and selected Asia Pacific markets.

Application Insights

The epilepsy segment is estimated to hold around 48% revenue share in 2026, supported by the high prevalence of drug-resistant epilepsy and the established clinical role of VNS as an adjunct therapy. It is widely used in hospital neurology departments, particularly for patients who are unresponsive to anti-epileptic drugs or not eligible for surgical intervention. Strong clinical validation and regulatory acceptance continue to reinforce its leadership position. However, growth is expected to remain moderate due to a relatively mature and well-defined patient population.

The depression segment is projected to grow at approximately 10.5% CAGR by 2033, driven by the rising burden of treatment-resistant depression and increasing incidence of chronic migraine linked to lifestyle and stress-related factors. Clinical evidence supported by institutions such as the NIH indicates improving outcomes with VNS-based neuromodulation therapies. Expanding use of non-invasive VNS devices in psychiatric and neurology outpatient clinics is further accelerating adoption. Increasing awareness and broader acceptance of device-based mental health interventions are expected to sustain strong growth momentum globally.

Regional Insights

North America Vagus Nerve Stimulation (VNS) Market Trends

North America is estimated to account for around 41% of the global share of the vagus nerve stimulation market in 2026, driven by strong clinical adoption of implantable VNS systems and well-established reimbursement support across healthcare providers. The market is highly integrated into epilepsy, depression, and migraine treatment pathways, with widespread use in tertiary hospitals and neurology specialty centers. Increasing penetration of FDA-approved neuromodulation devices, along with growing adoption of wearable and digitally connected VNS systems, is steadily expanding usage across both inpatient and outpatient care settings.

U.S Vagus Nerve Stimulation (VNS) Market Trends

The U.S. is estimated to contribute around 85% of North America’s VNS market share, supported by strong adoption of implantable neuromodulation systems and established clinical protocols for epilepsy and treatment-resistant depression. The market is widely embedded in hospital neurology networks, with increasing uptake in migraine and psychiatric applications. Recent trends include expanding clinical trials and early adoption of non-invasive VNS devices, particularly in neurology clinics and digital health-integrated care programs.

Canada Vagus Nerve Stimulation (VNS) Market Trends

Canada is estimated to hold approximately 15% of the North America VNS market share, with adoption primarily concentrated in specialized neurology hospitals and epilepsy treatment centers. The market is gradually expanding as access to implantable VNS systems improves through structured healthcare coverage. Increasing clinical interest in non-invasive VNS therapies is supporting early adoption in migraine and mental health applications, particularly in outpatient care settings.

Europe Vagus Nerve Stimulation (VNS) Market Trends

Europe is estimated to account for around 25% of the global market share, supported by structured neurological care systems and reimbursement frameworks under the EMA regulatory environment. Adoption is steady across epilepsy and depression indications, with increasing use of both implantable and non-invasive VNS devices in hospital-based neurology care. The market reflects consistent but moderate growth, driven by strong clinical validation and gradual expansion of neuromodulation-based therapies.

Germany Vagus Nerve Stimulation (VNS) Market Trends

Germany is estimated to represent around 30% of Europe’s VNS market share, driven by strong adoption of implantable VNS therapy in epilepsy treatment centers and advanced neurosurgical infrastructure. The market is well integrated into hospital-based neurological care pathways, supporting consistent device utilization. Recent developments indicate gradual expansion toward next-generation neuromodulation systems and increasing clinical acceptance of advanced VNS applications.

U.K. Vagus Nerve Stimulation (VNS) Market Trends

The U.K is estimated to account for approximately 22% of Europe’s VNS market share, supported by structured adoption within NHS neurology pathways and evidence-based treatment protocols. The market is steadily expanding in epilepsy and depression care, with increasing clinical evaluation of neuromodulation therapies. Recent activity includes pilot adoption of non-invasive VNS devices, particularly in migraine and psychiatric outpatient applications.

Asia Pacific Vagus Nerve Stimulation (VNS) Market Trends

Asia Pacific is estimated to hold around 24% of the global share of the vagus nerve stimulation market in 2026, while being the fastest-growing region due to rising neurological disease prevalence and improving access to advanced neuromodulation therapies. Adoption is increasing across hospital neurology departments and specialty clinics, supported by expanding healthcare infrastructure and growing awareness of epilepsy and depression treatment options. Cost-efficient device availability and expanding private healthcare networks are further accelerating market penetration.

China Vagus Nerve Stimulation (VNS) Market Trends

China is estimated to account for around 38% of Asia Pacific’s VNS market share, supported by large-scale adoption in urban neurology hospitals and increasing use of neuromodulation therapies for epilepsy and psychiatric disorders. The market is gradually expanding with rising clinical acceptance of both implantable and non-invasive systems. Adoption remains concentrated in advanced hospital networks, supported by growing domestic device manufacturing capabilities and increasing treatment accessibility.

India Vagus Nerve Stimulation (VNS) Market Trends

India is estimated to hold around 18% of the Asia Pacific VNS market, with adoption increasing steadily across private hospitals and neurology specialty centers. The market is expanding due to rising diagnoses of epilepsy and migraine, along with improving access to neuromodulation therapies in urban and tier-2 cities. Increasing availability of cost-effective treatment options is supporting gradual but consistent adoption in both inpatient and outpatient neurology care settings.

Competitive Landscape

The global vagus nerve stimulation market is moderately consolidated, with leading players such as LivaNova PLC, Medtronic, and Boston Scientific accounting for a significant share of revenue, primarily driven by dominance in implantable neuromodulation systems. These companies benefit from strong FDA approvals, established hospital relationships, and deep clinical expertise in epilepsy and depression treatment. Continuous investment in R&D for next-generation neuromodulation devices, including digital monitoring and therapy optimization features, further strengthens their competitive position.

Alongside this, companies such as ElectroCore Inc. and other neurotechnology firms are expanding in the non-invasive VNS segment, targeting migraine, depression, and anxiety applications through wearable and patient-friendly devices. High regulatory barriers and clinical validation requirements limit new entrants in implantable systems, while non-invasive technologies remain more open to innovation. The market is expected to see gradual consolidation through product expansion, clinical partnerships, and selective acquisitions, alongside growing collaboration between device manufacturers and digital health companies.

Key Industry Developments:

- In June 2025, the state of Connecticut passed legislation to establish a US$2 million Neuromodulation Center of Excellence. This initiative aims to expand access for veterans to the Vivistim® PairedVNS™ System, supporting long-term stroke recovery efforts.

- In March 2025, the Bionics Institute showcased new vagus nerve stimulation research at its NAB-hosted event, highlighting potential treatments for Crohn’s disease and rheumatoid arthritis, epilepsy, and announcing a new VNS Centre of Excellence.

Companies Covered in Vagus Nerve Stimulation (VNS) Market

- Medtronic

- Boston Scientific Corporation

- ElectroCore Inc.

- Cerebral Therapeutics

- Parasym Ltd.

- NeuroPace Inc.

- SetPoint Medical

- Tianjin Hopeful Medical

- Integer Holdings Corporation

- Abbott Laboratories

- NeuroSigma Inc.

- Axonics Inc.

- Aleva Neurotherapeutics

- Synapse Biomedical Inc.

Frequently Asked Questions

The global vagus nerve stimulation market is projected to reach US$551.0 million in 2026.

Rising prevalence of epilepsy, depression, and migraine, along with increasing adoption of neuromodulation therapies, drives the market.

The vagus nerve stimulation market is expected to grow at a CAGR of 9.3% from 2026 to 2033.

Expansion of non-invasive VNS devices and growing adoption in psychiatric and migraine therapies create key market opportunities.

Key players include LivaNova PLC, Medtronic, Boston Scientific, and ElectroCore Inc.