- Medical Devices

- Disposable Blood Bags Market

Disposable Blood Bags Market Size, Share, and Growth Forecast 2026 - 2033

Disposable Blood Bags Market by Product (Collection Bags, Transfer Bags), by Channel (Tender Sales, Private Sales), by End-user (Blood Banks, Hospitals, NGOs, Others), and Regional Analysis, 2026 - 2033

Disposable Blood Bags Market Size and Trend Analysis

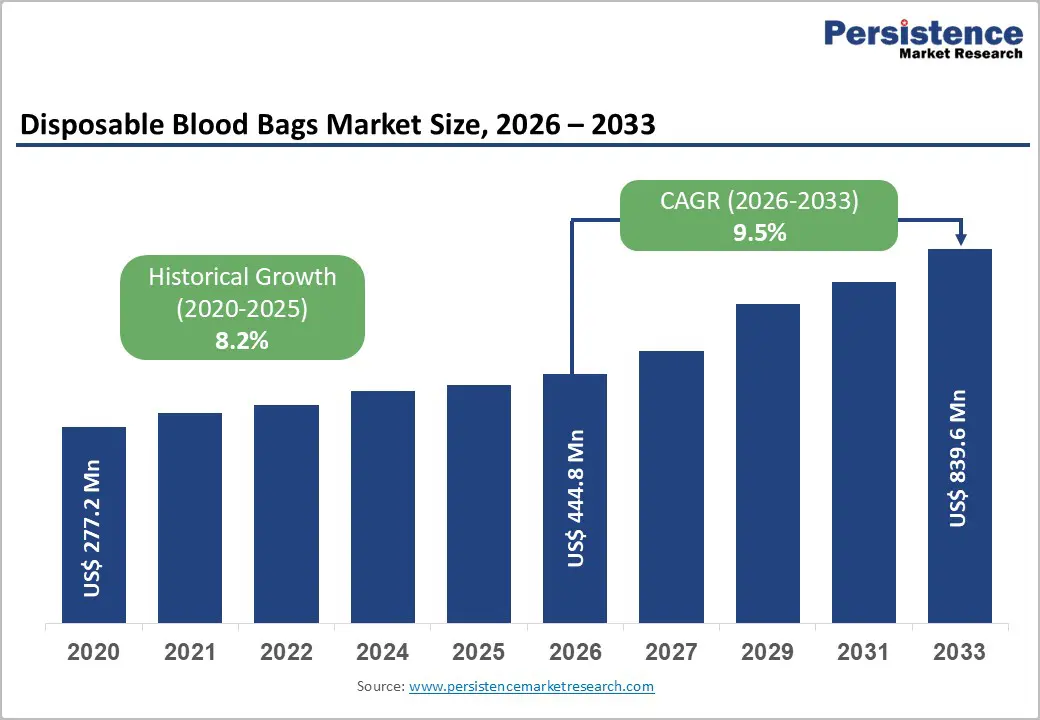

The global disposable blood bags market size is expected to be valued at US$ 444.8 million in 2026 and projected to reach US$ 839.6 million by 2033, growing at a CAGR of 9.5% between 2026 and 2033. This strong growth outlook is primarily driven by rising global blood transfusion volumes, expanding blood bank infrastructure, and escalating demand from surgical and trauma care settings worldwide.

The World Health Organization (WHO) estimates that approximately 118.5 million blood donations are collected globally each year, with demand continuing to outpace supply in low- and middle-income countries.

Increasing surgical procedure volumes, growing road accident rates, and expanding maternal healthcare programs are generating sustained institutional demand for sterile, single-use blood collection and transfer bags. Stringent regulatory standards mandating the use of DEHP-free and biocompatible plastic materials are simultaneously driving product innovation and premium pricing, supporting robust market revenue growth in the forecast period.

Key Industry Highlights:

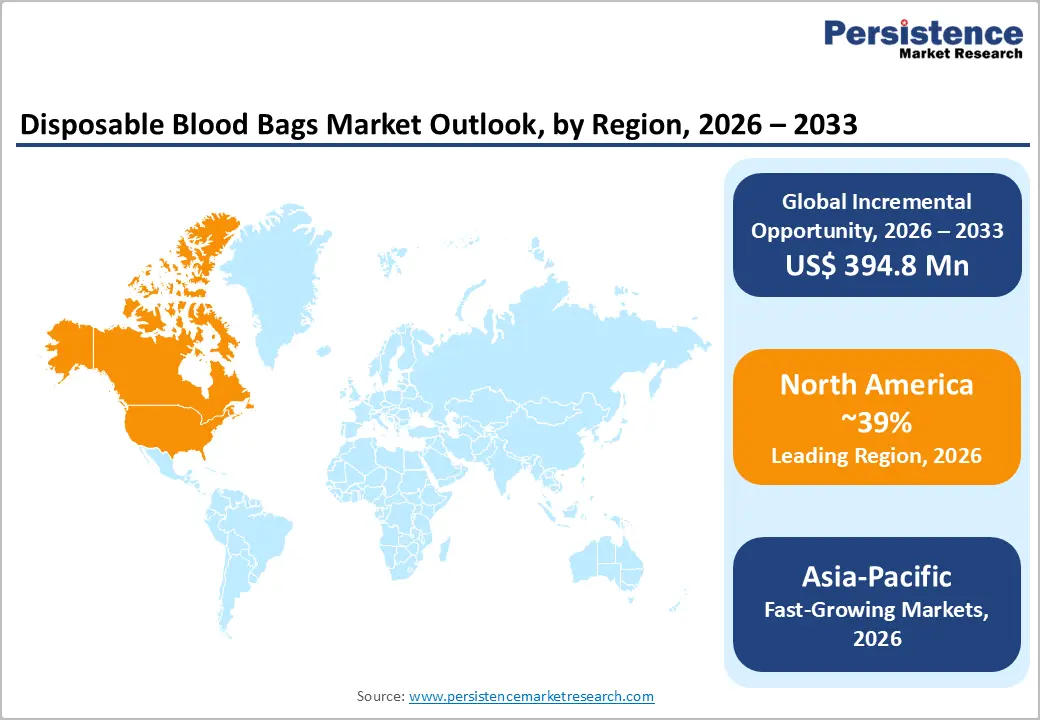

- Leading Region - North America: North America leads with approximately 39% of global market share in 2025, underpinned by the advanced blood banking infrastructure of the U.S., robust FDA oversight, and high-volume institutional procurement by organizations such as the American Red Cross.

- Fast - Growing Market - Asia Pacific: Asia Pacific is the fastest-growing region, driven by India's NBTC-led blood bank expansion, China's National Health Commission investments, and rapidly formalizing blood safety frameworks across ASEAN nations with cost-competitive regional manufacturing capabilities.

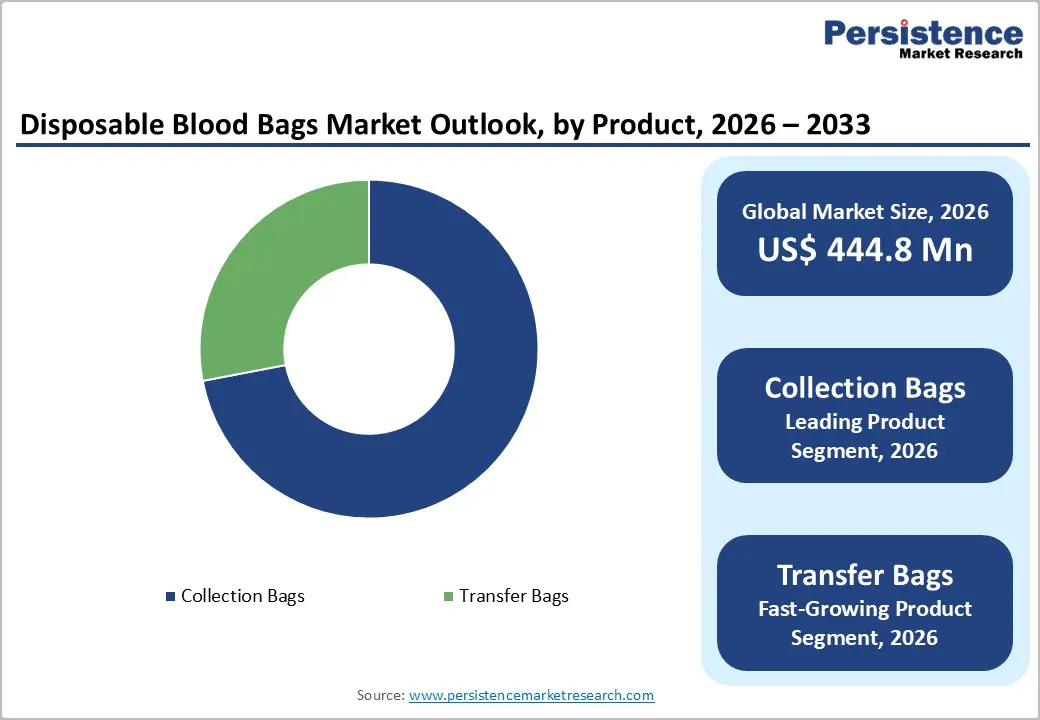

- Dominant Segment - Collection Bags: Collection Bags hold approximately 72% market share in 2025, as every blood donation requires at least one sterile collection bag. Multi-unit Double and Triple Collection Bag configurations dominate institutional procurement across accredited global blood centers.

- Fast- Growing Segment - Transfer Bags: Transfer Bags are the fastest-growing product segment, propelled by the global shift toward blood component therapy endorsed by the WHO and ISBT, requiring dedicated DEHP-free, multi-compartment bag systems for red cell, platelet, and plasma separation.

- Key Opportunity - Emerging Market Tender Programs: Government-funded blood safety programs in India, Africa, and Latin America, supported by UNICEF, PAHO, and the Gates Foundation, represent a high-volume, recurring procurement opportunity for WHO-prequalified blood bag manufacturers.

Market Dynamics

Drivers - Rising Global Blood Donation Volumes and Expanding Blood Banking Infrastructure

The consistent global increase in blood donation programs and the systematic expansion of blood banking infrastructure across both developed and developing economies represent the foremost demand driver for disposable blood bags. According to the WHO Global Status Report on Blood Safety and Availability, over 13,000 blood centers operate across 171 countries, collecting hundreds of millions of units annually.

National blood transfusion services in countries such as the United Kingdom (NHS Blood and Transplant), India (National Blood Policy), and China (National Health Commission) are actively scaling collection targets and upgrading blood bank facilities. Each blood donation unit requires multiple sterile disposable bags for collection, separation, and storage, creating a direct and proportional volume demand for blood bag products. Government-mandated blood safety programs further reinforce procurement of certified, single-use blood bags across institutional channels globally.

Market Restraints

Blood Storage Limitations and Risk of Transfusion-Transmitted Infections

Despite improvements in blood bag materials, stored blood quality degrades over time. Red blood cells remain viable for only 42 days under optimal refrigeration conditions as per AABB (American Association of Blood Banks) standards, while platelets have a shelf life of just 5-7 days. This inherent perishability creates supply chain inefficiencies and product wastage, constraining effective utilization of blood bag inventories. Furthermore, despite stringent screening protocols, risks of transfusion-transmitted infections (TTIs), including HIV, hepatitis B and C, and emerging pathogens, remain a persistent concern in lower-resourced healthcare environments, limiting blood transfusion program expansion and thereby dampening proportional demand growth for disposable blood bags in certain regions.

Opportunities - Expanding Transfer Bag Demand Driven by Component Therapy and Blood Fractionation Growth

Transfer bags used for the separation and storage of individual blood components, including red blood cells, platelets, and fresh frozen plasma, represent the fastest-growing product segment within the Disposable Blood Bags market. The global shift toward component therapy over whole blood transfusion, endorsed by the WHO and International Society of Blood Transfusion (ISBT), is driving systematic upgrade of blood processing capabilities in transfusion centers.

The WHO reports that in high-income countries, over 90% of donated blood is separated into components, a practice that is now being actively promoted in lower-income settings. Manufacturers investing in DEHP-free, multi-compartment transfer bag systems compatible with automated blood processing platforms are well-positioned to capture a significant share as blood fractionation infrastructure expands globally, particularly across the Asia Pacific, Latin America, and Africa.

Category-wise Analysis

Product Insights

Collection bags dominate the product category, likely to account for 72% of the total share in 2026. This leadership is structurally driven by the fact that every blood donation unit necessitates at least one collection bag, making collection bags the foundational consumable in the blood transfusion supply chain. Within the collection bag segment, Double Collection Bags and Triple Collection Bags are the most widely used configurations, enabling simultaneous collection and in-line separation of blood components.

The AABB Technical Manual confirms that multi-unit collection systems are the standard of care in accredited blood centers, as they minimize handling steps and contamination risk. Leading suppliers including TERUMO PENPOL, Fresenius SE & Co. KGaA, and Macopharma maintain extensive portfolios of CE-marked and FDA 510(k)-cleared collection bag configurations across all major global markets.

Channel Insights

The tender sales channel leads the channel category, accounting for approximately 58% share in 2026. Institutional procurement through government tenders conducted by national blood transfusion services, public hospital networks, and international health organizations represents the dominant purchasing mechanism for disposable blood bags in most global markets. Tender contracts typically involve large multi-year volumes with standardized product specifications, providing manufacturers with revenue visibility and scale efficiency.

In countries such as India, Brazil, China, and across Africa, public sector procurement accounts for the majority of blood bag purchases. The WHO's prequalification program for blood transfusion supplies plays a critical gatekeeping role in qualifying products for international tender participation, incentivizing manufacturers to maintain stringent quality and regulatory compliance standards to remain competitive in this high-volume channel.

Regional Insights

North America Disposable Blood Bags Market Trends and Insights

North America is dominant due to extremely high transfusion intensity, advanced emergency care systems, and structured national blood services. The U.S. alone performs tens of millions of blood component transfusions annually, supported by institutions like the American Red Cross and America’s Blood Centers.

The U.S. healthcare system also manages a very high surgical load, with millions of inpatient surgeries every year and large trauma volumes from road accidents and cardiovascular emergencies. Canada contributes through a universal healthcare system with standardized blood collection and storage protocols. High ICU admissions, oncology treatments, and transplant programs further sustain steady demand for disposable blood bags.

U.S. Disposable Blood Bags Market Trends and Insights

The U.S. leads the disposable blood bags market due to its large blood donor population, well-established healthcare infrastructure, and high volume of surgical, trauma, and transfusion procedures. The country maintains an extensive network of hospitals, blood banks, and collection centers that require reliable blood collection, storage, and transportation systems. Strong awareness regarding voluntary blood donation, advanced blood management practices, and stringent safety regulations further support market demand. Additionally, increasing cases of chronic diseases and emergency care needs contribute to the consistent utilization of disposable blood bags across healthcare facilities.

Canada Disposable Blood Bags Market Trends and Insights

Canada's disposable blood bags market is experiencing steady growth, supported by an aging population, increasing prevalence of chronic diseases, and a consistent need for blood transfusions. The country’s publicly funded healthcare system and centralized blood collection and distribution networks promote high standards of transfusion safety and quality control. Growing demand for blood components in surgical procedures, cancer treatments, and emergency care further drives market expansion. Additionally, ongoing investments in blood management infrastructure and donor programs support the widespread adoption of disposable blood bags across healthcare facilities nationwide.

Europe Disposable Blood Bags Market Trends and Insights

Europe is a critical region due to universal healthcare coverage, structured national blood transfusion services, and strong regulatory frameworks under the European Medicines Agency. Countries maintain centralized blood donation systems and high voluntary donation rates. Europe also has a high burden of chronic diseases such as cardiovascular conditions and cancer, both of which require frequent transfusions. The region has a large elderly population, increasing demand for surgeries, orthopedic procedures, and long-term hospital care. Emergency medicine systems across countries like Germany, France, and the UK ensure consistent usage of blood bags in trauma and surgical care.

Germany Disposable Blood Bags Market Trends and Insights

Germany leads the European Disposable Blood Bags Market due to its extensive healthcare infrastructure, large hospital network, and high volume of surgical and emergency procedures. The country benefits from a well-organized blood donation system and strong participation in voluntary blood donation programs. Advanced transfusion medicine practices and stringent safety standards support the widespread use of high-quality blood collection and storage products. Additionally, the growing prevalence of age-related disorders, cancer, and chronic diseases requiring regular transfusions continues to drive demand for disposable blood bags across healthcare facilities.

United Kingdom Disposable Blood Bags Market Trends and Insights

The United Kingdom's Disposable Blood Bags Market is supported by the centralized operations of the National Health Service Blood and Transplant (NHSBT), which manages blood collection, processing, and distribution nationwide. Increasing demand for blood products is driven by a growing elderly population, rising incidence of chronic diseases, and a steady volume of elective and emergency surgeries. Strong regulatory oversight and emphasis on transfusion safety encourage the adoption of advanced blood collection systems. Ongoing investments in healthcare infrastructure further contribute to consistent demand for disposable blood bags.

Asia Pacific Disposable Blood Bags Market Trends and Insights

Asia Pacific is the fast-growing region due to the rapid expansion of healthcare infrastructure, increasing surgical volumes, and rising trauma cases. A large population in countries such as India and China create high absolute demand for blood transfusions. Road traffic injuries are significantly high in the region, contributing to emergency transfusion needs. Governments are expanding blood donation programs and improving hospital access, especially in rural areas. The growing prevalence of anemia, cancer, and kidney disease also increases demand for blood components. Expansion of private hospitals and diagnostic centers further supports the adoption of disposable blood bags.

China Disposable Blood Bags Market Trends and Insights

China leads the Asia-Pacific Disposable Blood Bags Market owing to its vast healthcare infrastructure, large patient population, and growing number of surgical, trauma, and oncology procedures. The country has significantly expanded its blood collection and transfusion capabilities through healthcare modernization initiatives and investments in hospital infrastructure. Government-supported voluntary blood donation campaigns and stricter blood safety regulations continue to strengthen the national blood supply network. Additionally, increasing demand for blood components in chronic disease management and emergency care is driving sustained adoption of disposable blood bags.

India Disposable Blood Bags Market Trends and Insights

India is the fast-growing market for disposable blood bags, driven by rising healthcare expenditure, increasing trauma and accident cases, and a growing volume of surgical procedures. Expansion of private hospitals, diagnostic centers, and blood banks is creating strong demand for blood collection and storage solutions. Government initiatives, including national blood transfusion programs and awareness campaigns promoting voluntary blood donation, are improving blood availability and safety standards. Furthermore, the increasing burden of chronic diseases and expanding access to healthcare services are supporting long-term market growth.

Competitive Landscape

The global disposable blood bags market is moderately consolidated, with multinational players such as Fresenius SE & Co. KGaA, Macopharma, and Haemonetics Corporation competing alongside strong regional manufacturers, including TERUMO PENPOL and HLL Lifecare Limited. Key competitive differentiators include WHO prequalification status, DEHP-free product portfolios, and compatibility with automated blood processing systems. Strategic priorities include capacity expansion in emerging markets, tender compliance investments, and development of next-generation biocompatible and antimicrobial blood bag materials.

Subscription-based supply agreements with national blood services are an emerging business model trend, enhancing revenue predictability for leading suppliers.

Key Developments:

- February 2026: Haemonetics Corporation has received U.S. FDA clearance for its NexSys® PCS plasma collection system integrated with Persona® PLUS technology. The clearance enabled the company to commercialize an upgraded plasma collection platform designed to improve donor comfort, increase plasma yield efficiency, and enhance overall collection workflow.

- December 2024: Haemonetics Corporation announced that it had sold its whole blood assets to GVS S.p.A. The transaction involved the transfer of Haemonetics’ whole blood collection-related product portfolio to GVS, a global manufacturer of filtration and medical solutions. The divestment was part of Haemonetics’ strategic shift toward focusing more on its higher-margin plasma, apheresis, and blood management technologies.

Companies Covered in Disposable Blood Bags Market

- Grifols, S.A.

- Macopharma Bharat Transfusion Solution

- Fresenius SE & Co. KGaA

- TERUMO PENPOL Pvt. Limited

- HLL Lifecare Limited

- Span Healthcare Private Limited

- Innvol

- Haemonetics Corporation

- Neomedic International

- Medsun Biomedical Technologies Pvt. Ltd.

- Hänsler Medical

- C.Y. Medical Co., Ltd.

- EasierWay Medical

- Others

Frequently Asked Questions

The global disposable blood bags market is estimated to be valued at US$ 444.8 million in 2026.

Rising surgeries, trauma cases, blood donation programs, aging population, chronic diseases, and transfusion demand growth.

North America is the leading region, holding approximately 39% of the global market share in 2026.

Expansion in emerging healthcare infrastructure, rising blood donation systems, and demand for advanced multi-compartment bags.

Fresenius SE & Co. KGaA, Macopharma, TERUMO PENPOL Pvt. Limited, Grifols S.A., HLL Lifecare Limited, Haemonetics Corporation, Span Healthcare Private Limited.