- Healthcare Services

- U.S. Concierge Medicine Market

U.S. Concierge Medicine Market Size, Share, and Growth Forecast 2026 - 2033

U.S. Concierge Medicine Market by Membership Type -Individual Memberships, Family Memberships, Executive and Corporate Memberships, Senior-Focused Memberships), Mode of Care Delivery -In-Person Concierge Care, Virtual Concierge Care, Hybrid Concierge Care), Specialty -Primary Care, Internal Medicine, Pediatrics, Cardiology, Others), and Regional Analysis, 2026-2033

U.S. Concierge Medicine Market Size and Trend Analysis

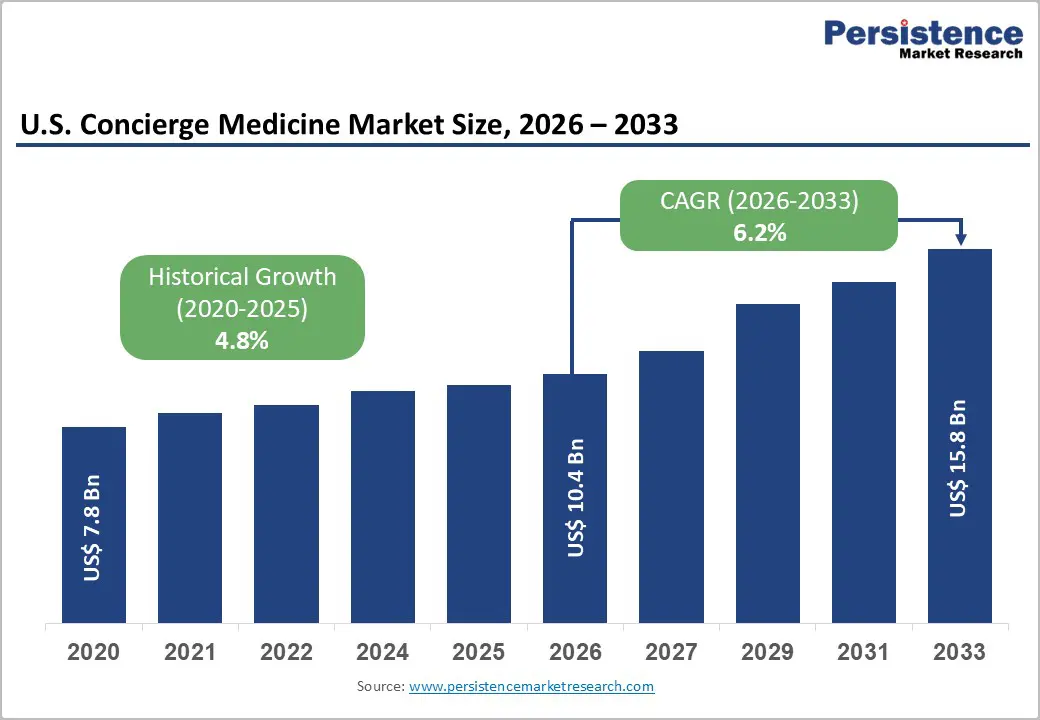

The U.S. Concierge Medicine market size is expected to be valued at US$ 10.4 billion in 2026 and projected to reach US$ 15.8 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033. It is experiencing accelerating growth driven by widespread physician burnout within conventional fee-for-service healthcare, escalating patient frustration with access limitations, and a growing high-net-worth consumer segment willing to pay premium annual membership fees for personalized, unhurried primary care.

According to the American Academy of Family Physicians (AAFP), the average primary care physician in a conventional practice manages 2,000-3,000 patients compared to 300-600 in concierge practices, enabling substantially enhanced care quality. The post-pandemic shift toward proactive preventive health management, the mainstreaming of telemedicine in hybrid concierge models, and Amazon's acquisition of One Medical signaling major corporate investment in the sector are collectively driving above-average revenue CAGR through 2033.

Key Industry Highlights:

- Leading Region - Northeast U.S.: The Northeast U.S. leads the concierge medicine market, anchored by New York City's ultra-premium boutique practices commanding US$ 10,000-80,000+ annual memberships, Boston academic medical center concierge models, and the nation's highest concentration of Fortune 500 corporate membership programs.

- Fastest Growing Region - Southeast U.S.: The Southeast is the fastest-growing region, driven by Florida's massive 65+ retiree population the highest senior demographic concentration in the U.S. MDVIP's disproportionate physician density in Miami, Boca Raton, and Palm Beach, and rapid affluent professional migration from high-tax Northern states.

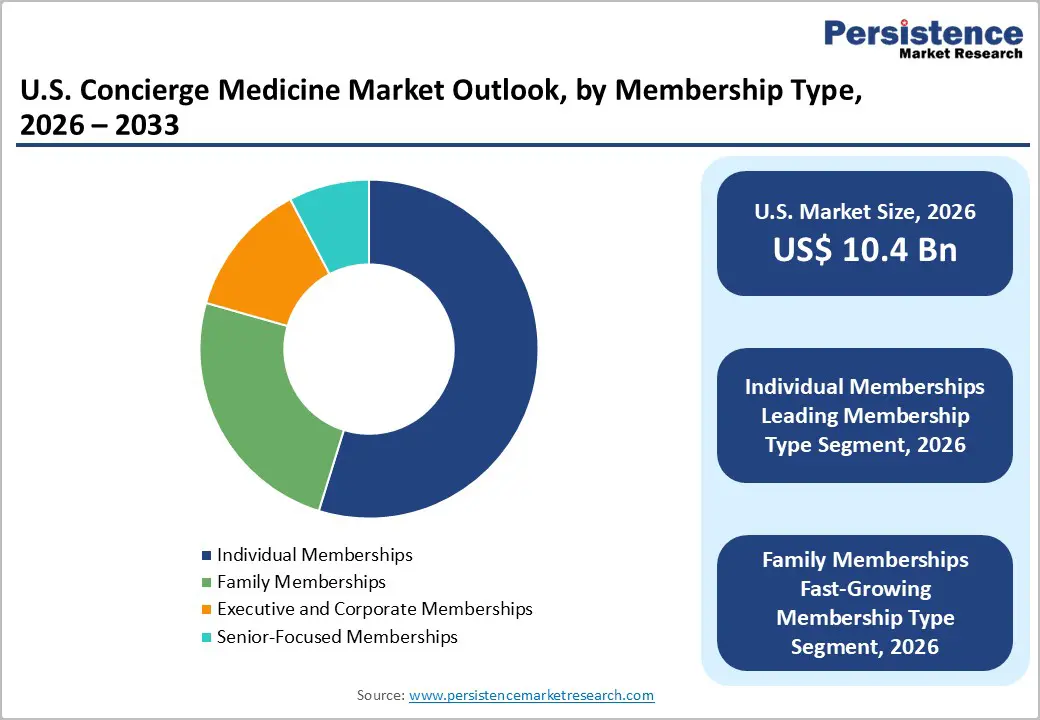

- Dominant Segment - Individual Memberships (~55% Share): Individual Memberships lead with 55% share in 2025, anchored by MDVIP's 400,000+ members at average fees of US$ 1,800-2,200 annually and SignatureMD's national physician affiliate network serving single-adult premium primary care purchasers.

- Fastest Growing Segment - Family Memberships: Family Memberships are the fastest-growing type, capturing multi-generational household healthcare consolidation trends with bundled rate value propositions from MDVIP and PartnerMD, integrating pediatric care, school physicals, and adult chronic disease management under single physician relationship.

- Key Opportunity - Hybrid Concierge Care and Amazon/One Medical Scale-up: Amazon's US$ 3.9 billion acquisition of One Medical and its bundling with Amazon Prime represents the defining opportunity to democratize concierge medicine access expanding beyond the top 20-25% income bracket toward a 170 million+ Amazon Prime subscriber addressable market.

Market Dynamics

Drivers - Primary Care Physician Shortage and Patient Access Crisis Accelerating Concierge Adoption

The United States faces a worsening primary care physician shortage that is directly propelling concierge medicine adoption among patients unwilling to accept degraded access and care quality. The Association of American Medical Colleges (AAMC) projects a shortage of up to 86,000 physicians by 2036, with primary care facing the largest deficit. In conventional practices, patients wait an average of 24 days for a new primary care appointment, according to Merritt Hawkins' Survey of Physician Appointment Wait Times. Concierge medicine directly resolves this access failure by limiting physician-patient panels to 300-600 patients, enabling same-day or next-day appointment availability, 24/7 physician direct communication, and extended appointment times averaging 45-60 minutes versus the conventional 7-minute primary care visit documented by the American Medical Association -AMA). As access deterioration worsens, the value proposition of concierge membership strengthens, driving sustained consumer demand growth.

Aging Baby Boomer Population Driving Premium Healthcare Spending and Chronic Disease Management Demand

The aging of the 76 million Baby Boomers entering their peak chronic disease burden years is creating the most powerful demographic demand wave in the history of U.S. concierge medicine. The U.S. Census Bureau projects that all Baby Boomers will be over 65 by 2030, representing a 73 million-strong senior consumer cohort with high healthcare utilization needs and critically greater financial capacity to fund premium healthcare memberships.

The Centers for Disease Control and Prevention (CDC) reports that 85% of adults aged 65+ have at least one chronic condition, and 60% have two or more. Concierge medicine's comprehensive chronic disease management capabilities, proactive preventive care protocols, and care coordination services are uniquely aligned with this demographic's complex healthcare needs, driving Senior-Focused Membership growth as the market's fastest-rising specialty segment.

Restraints - High Membership Fees Limiting Addressable Market to Affluent Demographics

Concierge medicine's annual membership fees typically range from US$ 1,500 to US$ 30,000+ per year, depending on practice model and services included, creating a significant socioeconomic barrier that limits the addressable market to high-income and upper-middle-income consumers. The U.S. Bureau of Labor Statistics (BLS) Consumer Expenditure Survey data indicate that healthcare premium spending is highly income-elastic, with lower-income quintiles unable to afford supplemental direct-pay healthcare membership costs. This pricing structure restricts concierge medicine's penetration to approximately the top 20-25% of U.S. household income brackets, creating a natural ceiling on total addressable patient population and limiting mass-market scale.

Regulatory Complexity Around Direct Primary Care and Insurance Billing Prohibition

Concierge medicine practices operate in a complex regulatory environment where membership fee structures must be carefully structured to comply with state-level direct primary care (DPC) legislation and avoid classification as insurance products requiring state insurance department licensure. As of 2024, only 26 states have enacted explicit Direct Primary Care Protection Acts, according to the Direct Primary Care Coalition, creating legal uncertainty in the remaining states. Additionally, concierge physicians who opt out of Medicare face stringent CMS restrictions under the Social Security Act, limiting service to Medicare-enrolled seniors, a significant constraint given the aging target demographic.

Opportunities - Family Membership Models: Fastest-Growing Segment Capturing Household Healthcare Consolidation

Family Memberships represent the U.S. Concierge Medicine market's fastest-growing membership category, driven by the compelling value proposition of consolidating an entire household's primary healthcare needs under a single physician relationship with comprehensive care coordination. Multi-generational families managing the healthcare needs of children, working-age adults, and aging parents are increasingly drawn to concierge practices offering bundled family membership rates that provide per-capita cost efficiencies compared to individual memberships.

According to the American Academy of Private Physicians (AAPP), the trend toward value-based, relationship-driven healthcare is accelerating post-pandemic family concierge adoption. Practices including MDVIP, LLC. and PartnerMD, LLC. are expanding family membership offerings with pediatric care integration, school physical coordination, and well-child visit protocols that differentiate their value proposition from individual-only concierge models, creating a significant market expansion opportunity.

Hybrid Concierge Care: Telemedicine Integration Expanding Geographic Reach and Membership Economics

Hybrid concierge care, combining in-person visits with unlimited telemedicine access represents the most transformative commercial model evolution in U.S. concierge medicine, enabling practice geographic expansion beyond physical office locations and improving membership economics through telehealth-efficient care delivery.

The American Medical Association (AMA) Telehealth Impact Study found that 84% of physicians reported using telehealth in 2021 post-pandemic normalization, with the majority of concierge practices now integrating digital health platforms. 1Life Healthcare, Inc. (One Medical) now part of Amazon following its US$ 3.9 billion acquisition in 2023, is pioneering at-scale hybrid concierge care delivery combining app-based communication, same-day virtual visits, and in-person care, setting a new benchmark for technology-integrated concierge medicine models that smaller practices and national platforms including Crossover Health Medical Group and WorldClinic, Inc., are emulating to attract digitally native younger professional demographics.

Category-wise Analysis

Membership Type Insights

The Individual Memberships segment leads the U.S. Concierge Medicine market by membership type, commanding approximately 55% of total market share in 2026. Individual memberships, where a single adult pays an annual retainer fee for enhanced primary care access, remain the foundational commercial structure of U.S. concierge medicine, reflecting the model's origins in serving affluent individual professionals and retirees seeking high-touch physician relationships outside managed care constraints. MDVIP, LLC, the nation's largest concierge medicine network with over 1,100 affiliated physicians and 400,000+ members, primarily operates on individual membership models with annual fees averaging US$ 1,800-2,200. Similarly, SignatureMD, Inc. and Specialdocs Consultants, LLC. anchor their physician affiliate programs on individual membership structures. Family Memberships are the fastest-growing type, driven by pediatric integration and multi-generational household healthcare consolidation trends.

Mode of Care Delivery Insights

The In-Person concierge care segment leads the U.S. concierge medicine market by mode of care delivery, accounting for approximately 51% of total market share in 2026. In-person concierge care, characterized by direct office visits with extended appointment times, home visits for certain practices, and face-to-face physical examinations and diagnostic workups, retains market leadership because the premium care experience central to concierge medicine's value proposition is most fully realized through in-person interactions. Patients paying US$ 2,000-30,000+ annually specifically value the personal physician relationship, unhurried examinations, and diagnostic thoroughness that in-person visits uniquely enable. However, Hybrid Concierge Care combining in-person and virtual access is the fastest-growing delivery mode, driven by the Amazon/One Medical technology-integrated model and the post-pandemic normalization of telemedicine among all age demographics.

Specialty Insights

The primary care specialty leads the U.S. concierge medicine market by specialty, commanding approximately 58% of total market share in 2026. Primary care is the foundational and historically dominant specialty in concierge medicine because the model directly addresses primary care's most acute market failure: access and time constraints in a high-volume, fee-for-service system that has eroded the physician-patient relationship. The American Academy of Private Physicians -AAPP) estimates that there are now over 12,000 concierge and direct primary care physicians practicing in the United States as of 2024, the vast majority offering primary care services. Platforms including MDVIP, LLC., SignatureMD, Inc., and Castle Connolly Private Health Partners, LLC. are exclusively primary care-focused. Cardiology is the fastest-growing specialty segment, driven by the CDC's reported high prevalence of cardiovascular disease as the leading cause of death among the target senior demographic.

Regional Insights

Northeast U.S. Concierge Medicine Market Trends and Insights

The Northeast U.S. accounts for an estimated 34.2% of the U.S. concierge medicine market in 2026, making it the leading regional market. Growth is supported by a high concentration of affluent households, established physician networks, and strong demand for premium healthcare services among executives, entrepreneurs, and aging populations. The region has a mature private healthcare ecosystem and widespread adoption of annual retainer-based models focused on preventive care, chronic disease management, and coordinated specialist access. Executive and corporate memberships are expanding as employers increasingly offer personalized healthcare benefits to senior leadership and high-value employees.

Southeast U.S. Concierge Medicine Market Trends and Insights

The Southeast U.S. is the fastest-growing regional market and is projected to expand at a CAGR of 11.9% through 2032. The region benefits from strong population growth, increasing numbers of affluent retirees, and rising demand for senior-focused healthcare services. Preventive medicine, cardiovascular monitoring, and chronic disease management are key areas of adoption. Lower tax environments and ongoing migration of high-income households continue to expand the addressable market for concierge practices, while physician groups are scaling membership-based models across both metropolitan and retirement-oriented communities.

West U.S. Concierge Medicine Market Trends and Insights

The West U.S. captures approximately 29.4% of the U.S. concierge medicine market in 2025 and remains the most innovation-driven region. Adoption is fueled by high digital health utilization, large concentrations of technology professionals, and strong employer-sponsored healthcare programs. Hybrid and virtual concierge models are widely adopted, combining in-person visits with telehealth, health coaching, and integrated wellness services. Corporate-sponsored memberships are growing rapidly as employers use premium healthcare access as a strategic tool for talent attraction, retention, and executive productivity.

Competitive Landscape

The U.S. Concierge Medicine market is moderately fragmented, with national platforms MDVIP, LLC. (1,100+ affiliated physicians) and 1Life Healthcare, Inc. (One Medical) competing alongside regional networks, independent boutique practices, and emerging employer-focused platforms including Crossover Health and Destination Health, Inc. Key competitive differentiators include physician network breadth, telehealth platform capability, membership pricing flexibility, specialty integration, and employer benefit program infrastructure. Strategic trends include Amazon's integration of One Medical into its Prime Health ecosystem, national network expansion through physician affiliate programs, and hybrid model innovation combining in-person care with AI-driven health monitoring.

Key Developments:

- In May 2026, HeartBeam, Inc. entered a commercial agreement with Atelier Health to expand deployment of its cardiac monitoring technology across key U.S. concierge medicine markets, including Southern California, New York, Dallas, and South Florida.

- In October 2025, Cardio Diagnostics Holdings, Inc. partnered with 15 new provider organizations across the United States, expanding adoption of its AI-enabled blood tests for the prevention, early detection, and management of coronary heart disease.

- In June 2024, Crisis24 launched the Private Strategic Group (PSG), combining executive protection with global medical concierge services for high-profile individuals, business leaders, and their families. The offering expands access to premium, on-demand healthcare support and strengthens the integration of concierge medicine within elite risk management services.

U.S. Concierge Medicine Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 26.7 Bn |

|

Current Market Value (2026) |

US$ 35.6 Bn |

|

Projected Market Value (2033) |

US$ 54.2 Bn |

|

CAGR (2026-2033) |

6.2% |

|

Dominant Application |

Chronic Pain Management, 34.8% share |

|

Top-ranking Product Type |

Oils and Extracts. 38.4% |

|

Incremental Opportunity |

US$ 18.6 Bn |

Companies Covered in U.S. Concierge Medicine Market

- SignatureMD, Inc.

- MDVIP, LLC.

- Specialdocs Consultants, LLC.

- Crossover Health Medical Group, APC

- PartnerMD, LLC.

- Castle Connolly Private Health Partners, LLC.

- Priority Physicians, PC

- Concierge Consultants & Cardiology

- Peninsula Doctor

- Destination Health, Inc.

- Campbell Family Medicine

- The Regents of the University of California -Operating as UC San Diego Health)

- 1Life Healthcare, Inc. -Operating as One Medical)

- Cypress Membership Medicine, LLC.

- WorldClinic, Inc.

- Others

Frequently Asked Questions

The U.S. concierge medicine market is projected to reach US$ 10.4 billion in 2026, having grown at a historical CAGR of 4.8% during 2020-2025. The market is forecast to expand to US$ 15.8 billion by 2033, driven by the primary care physician shortage, aging Baby Boomer demographics, and Amazon's One Medical integration, accelerating hybrid concierge model adoption at scale.

Rising demand for personalized physician access, longer consultations, preventive care, and proactive chronic disease management among affluent individuals, seniors, and corporate executives is the primary driver of the U.S. concierge medicine market.

The U.S. concierge medicine market is poised to witness a CAGR of 6.2% from 2026 to 2033.

The key growth opportunity lies in expanding employer-sponsored executive health memberships and hybrid virtual concierge care to serve a broader high-income and professionally insured population.

Leading companies include MDVIP LLC. -1,200+ affiliated physicians, 400,000+ members), 1Life Healthcare Inc. -One Medical/Amazon Health), SignatureMD Inc., Specialdocs Consultants LLC., Crossover Health Medical Group, PartnerMD LLC., Castle Connolly Private Health Partners LLC., WorldClinic Inc., Priority Physicians PC, Destination Health Inc., Forward Health, Marvin Health, and Cypress Membership Medicine LLC., among others. These players compete through physician network scale, telehealth integration, membership pricing flexibility, specialty breadth, and employer health benefit program development.